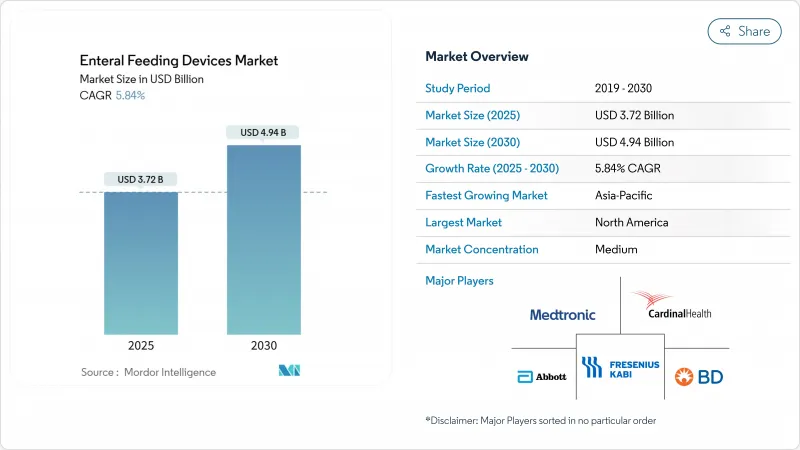

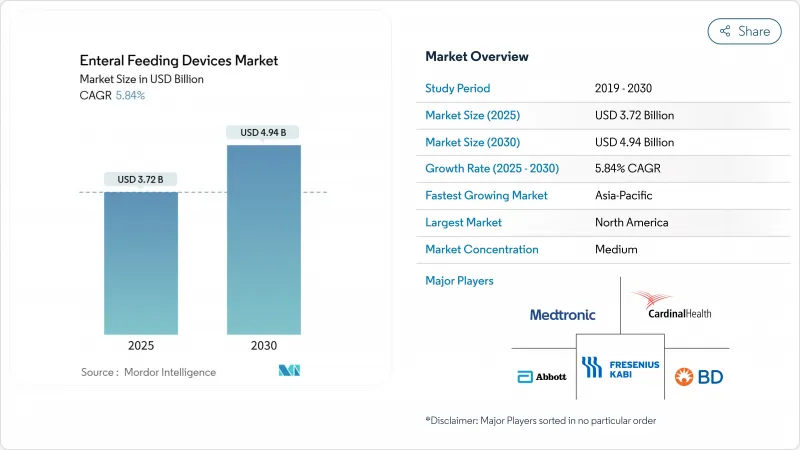

경장영양 기기 시장은 2025년에 37억 2,000만 달러, 2030년에는 49억 4,000만 달러에 이르고, CAGR 5.84%로 성장할 전망입니다.

이 확장은 기존공급 방법에서 안전성, 디지털 연결성 및 ENFit 준수 피팅을 중심으로 구축된 시스템으로의 꾸준한 전환을 반영합니다. 인구통계학적 압력, 특히 수명 연장과 만성 질환의 유병률 증가가 기준 수요를 강화하고 있습니다. ISO 80369-3 표준에 대한 조기 준수는 명확한 경쟁 테코가 되어 새로운 커넥터 포맷용으로 제품 라인을 재설계할 수 있는 제조업체는 보상되는 한편, 적응하기 위한 자원이 부족한 기업의 통합이 가속하고 있습니다. 엄격한 안전 설계와 스마트팜프, 원격 모니터링, 직관적 인 인터페이스를 결합한 장비 제조업체는 환자의 집과 외래 센터로의 케어 시프트와 관련된 성장을 얻기 위해 현재 가장 유리한 입장에 있습니다.

더 많은 케어가 병동에서 가정 거실로 이동하고 있습니다. 무선 모듈을 탑재한 휴대용 펌프를 통해 간호사가 원격으로 영양 보급을 감독할 수 있게 되어, 쾌적성을 향상시키면서 입원 비용을 삭감할 수 있게 되었습니다. 미국 및 유럽의 일부 보험사에서는 이러한 처방에 환불을 실시하여 재택 채택을 강화하고 있습니다. 간병인이 최소한의 훈련으로 펌프를 안전하게 작동할 수 있도록 장비 인터페이스가 간소화되었습니다. 그러나 많은 아시아태평양과 라틴아메리카의 의료 제도에서는 상환 제도의 격차가 보급을 늦추고 있으며, 그 결과 경경장영양 기기 시장은 양극화되고 있습니다.

신생아 하위 부문은 세계적인 조산아 증가와 집중 치료실에서의 생존율의 향상에 의해 지원됩니다. 임상시험에 따르면 초저출생체중아는 분유 우유 영양보다 도너 우유 영양이 4일 빨리 완전 영양에 도달할 수 있기 때문에 정밀한 펌프나 소구경의 ENFit 주사기 수요에 박차를 가하고 있습니다. 스탠포드 의과 대학의 알고리즘은 영양 믹스를 자동으로 조정하여 취약한 유아의 처방 정확도를 향상시킵니다. 이러한 기술의 적층이 안전성 수준을 높여 가격을 밀어 올리고 있음에도 불구하고 저자원국의 병원에서는 주사기 펌프가 부족하고 공급 취약성이 계속되고 있습니다.

조사 대상이 된 아시아태평양 국가 중 재택 경장 영양을 위한 체계적인 자금을 제공하고 있는 것은 불과 40%에 불과하고, 병원은 기기의 보급을 약화시키는 믹서식에 의지할 수밖에 없습니다. 이러한 자금 조달의 공백으로 인해 경장영양 기기 산업은 소득 라인을 따라 분할되고 부유한 병원에는 고급 펌프가 들어가고 다른 지역에서는 벌거 벗은 튜브가 우세합니다.

2024년에는 영양 펌프가 매출액의 39.67%를 차지했으며 복용량의 정확성과 안전 경보로 우위를 주장했습니다. 용량형 유닛은 여전히 중요한 케어의 중심적인 존재이지만, 케어의 분산화에 따라 경량의 외래용 모델이 급속히 상승하고 있습니다. 튜브의 경장영양 기기 시장 규모는 CAGR 6.87%로 상승 중이며, 침대 측에서의 배치를 가이드해 X선 피폭을 삭감하는 내장 카메라가 그 원동력이 되고 있습니다. 제조업체 각 회사는 ENFit 세트를 펌프와 튜브 모두에 번들하여 케어 패스 전체에서 커넥터의 컴플라이언스를 보장합니다. 일회용 주사기 세트의 짧은 사이클에서의 교환 패턴은 경상 수익을 더욱 강화하고 경장영양 기기 시장의 이 부분에 새로운 자본을 끌어들이고 있습니다.

미국에서는 클래스Ⅱ로 분류되는 주사기에 대한 규제상의 감시가 벤더를 오투여 방지용 캡이나 컬러 큐로 향하게 했습니다. 가방이나 투여 세트는 어떠한 사료 치료에도 소모품이 필요하기 때문에 보급은 느리지만 확실한 것이 되고 있습니다. 그러나 동아시아의 의료용 플라스틱 원재료 부족은 공급망을 불안정한 상태에 노출시켜 북미와 유럽의 재조달 프로젝트에 박차를 가할 수 있습니다.

만성질환과 뇌졸중 후 치료가 치료 건수의 대부분을 차지하기 때문에 2024년 매출의 72.45%는 성인이 차지합니다. 한편, 소아·신생아 부문은 신흥국에서의 신생아 집중 치료 능력의 확대를 배경으로, CAGR 7.12%의 성장률을 보이고 있습니다. 독점적인 공여자 우유 프로토콜과 AI 구동형 영양 계산기는 완전 영양 보급까지의 시간을 단축하여 교정된 주사기와 소량 펌프 수요를 강화하고 있습니다.

신생아 전용 장비 시장 점유율은 엄격한 안전 기준과 제한된 공급업체 간의 경쟁을 반영하여 소폭이지만 프리미엄에 머물고 있습니다. 공급 갭, 특히 주사기 펌프의 부족은 일부 저자원 환경의 임상의가 성인용 장비를 유아용으로 맞추도록 강요하고 탄력있는 제조 실적의 필요성을 돋보이게합니다. 성인에 중점을 둔 디자인은 가정에서의 사용을 단순화하기 위해 소아과의 인체 공학을 도입하여 경장영양 기기 시장 전체에서 상호 수분의 이점을 입증합니다.

북미는 2024년 세계 지출액의 36.64%를 차지했으며, 폭넓은 상환과 ENFit의 조기 도입에 지지되었습니다. 성장률은 CAGR 5.14%로 느리지만 재택 케어 모델이나 원격 모니터링 기기에 대한 연방 정부의 장려책이 성장을 지지하고 있습니다. FDA가 소아용 의료기기의 부족에 주목하여 공급업체는 국내 성형 및 조립을 확대하여 리드타임 개선과 원재료 리스크 완화를 도모하고 있습니다.

유럽에서는 회원국 간의 승인 요건을 표준화하는 의료기기 규제가 뒷받침되고, 2030년까지 CAGR 5.57%로 성장할 전망입니다. 규칙이 통일됨으로써, 여러 국가에서의 상시에 걸리는 관리 비용이 삭감되고, 제조업체 각 사는 앱을 이용한 투여 기록 등의 차별화 기능에 집중할 수 있게 됩니다. 독일, 프랑스 및 북유럽 국가에서는 에이징 인 플레이스 정책이 특히 국가 간호 프로그램을 통한보다 광범위한 재택 먹이 채택을 촉진하고 있습니다. 특별한 의료 목적의 식품에 관한 규칙은 복잡성을 증가시키고 있지만, 컴플라이언스를 문서화할 수 있는 숙련된 기업이 유리합니다. 유럽 재택 프로그램과 관련된 경경장영양 기기 시장 규모는 지자체가 원격 영양 검사를 일상적인 노인 관리로 통합함에 따라 꾸준히 확대될 것으로 보입니다.

아시아태평양은 중국과 인도에서 병원 건설 붐과 국민 모두 보험 제도의 확대로 CAGR 6.68%로 가장 빠른 지역 속도를 기록하고 있습니다. 그러나 액세스에는 여전히 편차가 있습니다. APAC 국가 중 가정용 장 영양제를 상환하는 것은 절반 이하이기 때문에 저중소득 지역에서는 혼합 식단이 계속되고 있습니다. 인도의 유통업체인 엔테로 헬스케어는 2024년 연간 매출 성장률 22%로 성장을 지속하고, 있으며, 자금 조달 장벽이 없어지면 의료기기에 대한 강한 의욕이 나타납니다. 가격에 민감한 지역에 침투하기 위해 세계 기업은 현지 조립업체와 제휴하여 저가의 튜브와 옵션 스마트 기능을 결합한 단계적 포트폴리오를 제공합니다. 이러한 단계를 밟는 것으로, 경장영양 기기 시장에 대한 모아적인 관심을 지속적인 이익으로 전환시키는 것을 목표로 하고 있습니다.

The enteral feeding devices market stands at USD 3.72 billion in 2025 and is on track to reach USD 4.94 billion by 2030, advancing at a 5.84% CAGR.

The expansion reflects a steady switch from legacy feeding methods toward systems built around safety, digital connectivity, and ENFit-compliant fittings. Demographic pressures, especially longer lifespans and rising chronic illness prevalence, shore up baseline demand. Early compliance with ISO 80369-3 standards has become a clear competitive lever, rewarding manufacturers able to re-engineer product lines for the new connector format while accelerating consolidation among firms lacking the resources to adapt. Device makers that combine rigorous safety design with smart pumps, remote monitoring, and intuitive interfaces are now best placed to capture growth as care shifts into patient homes and outpatient centers.

More care is moving from hospital wards to living rooms. Portable pumps with wireless modules now allow nurses to supervise feeds remotely, trimming inpatient costs while improving comfort. Insurers in the United States and parts of Europe reimburse these regimens, reinforcing take-home adoption. Device interfaces have been simplified so caregivers can operate pumps safely with minimal training. However, reimbursement gaps across many Asia Pacific and Latin American health systems delay uptake, resulting in a two-speed enteral feeding devices market.

The neonatal sub-segment is buoyed by global increases in preterm deliveries and better intensive-care survival. Clinical trials show donor milk diets help very-low-birth-weight infants reach full feeds four days sooner than formula diets, spurring demand for precise pumps and small-bore ENFit syringes. Algorithms from Stanford Medicine now calibrate nutrient mixes automatically, improving prescription accuracy in fragile infants. These technology layers raise the bar for safety and push prices higher, yet shortages of syringe pumps in low-resource hospitals highlight on-going supply fragility.

Only 40% of surveyed Asia Pacific nations provide structured funding for home enteral feeds, forcing hospitals to rely on blenderized diets that undermine device penetration. Such financing vacuums split the enteral feeding devices industry along income lines, with premium pumps entering wealthy hospitals and bare-bones tubes predominating elsewhere.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2024, feeding pumps generated 39.67% of revenue, asserting dominance through dose accuracy and safety alarms. Volumetric units remain central to critical-care routines, but lightweight ambulatory models are rising fast as care decentralizes. The enteral feeding devices market size for tubes is climbing at a 6.87% CAGR, fueled by integrated cameras that guide bedside placement and cut X-ray exposure. Manufacturers bundle ENFit sets with both pumps and tubes, ensuring connector compliance across the care pathway. A short-cycle replacement pattern for disposable giving sets further strengthens recurring revenues, drawing new capital into this portion of the enteral feeding devices market.

Regulatory scrutiny over syringes, categorized as Class II in the United States, has nudged vendors toward tamper-evident caps and color cues that prevent wrong-route errors. Bags and administration sets show slower but dependable uptake because every feed regimen needs consumables. Raw-material shortages in East Asia medical-grade plastics, however, expose the supply chain to volatility and may spur reshoring projects in North America and Europe.

Adults accounted for 72.45% of 2024 sales as chronic disorders and post-stroke care dominate procedure counts. Conversely, the pediatric & neonatal bracket is advancing at 7.12% CAGR on the back of expanding neonatal intensive-care capacity in emerging economies. Exclusive donor-milk protocols and AI-driven nutrient calculators shorten time to full feeds, reinforcing demand for calibrated syringes and low-volume pumps.

The enteral feeding devices market share for neonatal-specific devices remains modest but premium, reflecting strict safety criteria and limited vendor competition. Supply gaps, notably syringe pump shortages that forced clinicians in some low-resource settings to adapt adult gear for infants, spotlight the need for resilient manufacturing footprints. Adult-focused design is now borrowing pediatric ergonomics to simplify use in the home, demonstrating cross-pollination benefits across the enteral feeding devices market.

The Enteral Feeding Devices Market Report is Segmented by Product Type (Feeding Pumps [Volumetric Pumps and More], Feeding Tubes [Nasogastric Tubes and More], and More), Age Group (Adults and More), Distribution Channel (Offline and Online), Application (Oncology and More), End-User (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 36.64% of 2024 global spend, underpinned by wide reimbursement and early ENFit adoption. Growth, although slower at 5.14% CAGR, remains supported by home-based care models and federal incentives for telemonitoring devices. The FDA's spotlight on pediatric device shortages has pushed suppliers to expand domestic molding and assembly, improving lead times and mitigating raw-material risks.

Europe posts a 5.57% CAGR through 2030, aided by the Medical Device Regulation that standardizes approval requirements across member states. Harmonized rules lower administrative costs for multi-country launches and let manufacturers focus on differentiating features like app-enabled dose logging. Aging-in-place policies across Germany, France, and the Nordics encourage wider home feed adoption, especially via national nursing programs. Food for special medical purposes rules add complexity yet favor experienced firms that can document compliance. The enteral feeding devices market size tied to European home programs is set to climb steadily as municipalities integrate remote nutrition checks into routine elder care.

Asia Pacific marks the fastest regional pace at 6.68% CAGR owing to hospital building booms and expanding universal-health schemes in China and India. Yet access remains uneven; fewer than half of APAC nations reimburse home enteral formulas, so blenderized diets persist in lower-middle-income areas. Indian distributor Entero Healthcare registered 22% annual revenue growth in 2024, evidencing strong device appetite once funding barriers fall. To penetrate price-sensitive zones, global firms ally with local assemblers and offer tiered portfolios that pair low-cost tubes with optional smart features. These steps aim to convert nascent interest into durable gains for the enteral feeding devices market.