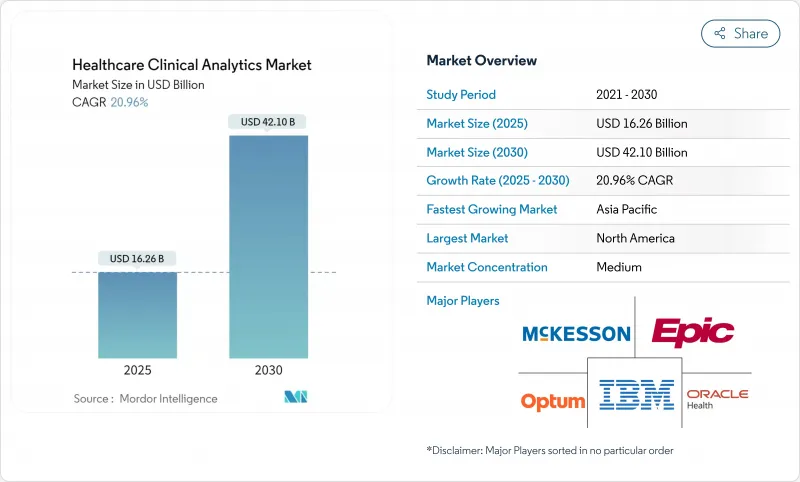

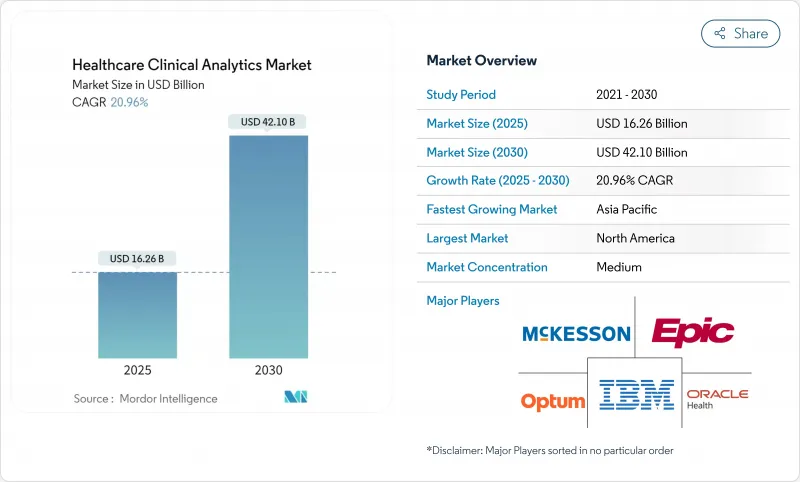

헬스케어 임상 분석 시장은 2025년 162억 6,000만 달러, 2030년에는 421억 달러에 이르고, CAGR 20.96%로 성장할 것으로 예상됩니다.

전자건강기록(EHR)의 성숙도 급상승, 인공지능(AI) 기술의 급속한 진보, 가치 기반 상환으로의 세계적인 변화는 실시간 데이터 구동형 의사결정 지원 수요를 촉매하고 있습니다. 의료 제공업체는 폭발적으로 증가하는 구조화·비구조화 의료 데이터를 비용을 억제하면서 결과를 개선하는 실용적인 통찰력으로 변환할 필요성이 높아지고 있습니다. 비용 절감 압력 격화, 노동력 부족 가운데 업무 효율 추구, 의료기기로서의 AI 대응 소프트웨어에 대한 규제의 새로운 명확화에 의해 의료 현장 전체 도입이 더욱 가속화되고 있습니다. 지역별로는 북미가 EHR의 보급과 유리한 상환규칙에 의해 명확한 리더십을 유지하고 있는 반면 아시아태평양은 대규모 디지털화 프로그램과 클라우드 인프라에 대한 액세스 확대를 배경으로 급성장하고 있습니다. 기술적 분석은 여전히 지출의 대부분을 차지하지만, 인지 분석은 고차 추론 작업을 자동화하고 임상의의 작업 부하를 줄임으로써 대응 가능한 의료 임상 분석 시장을 확대하고 있습니다.

병원 및 외래 클리닉에 공인 EHR 시스템을 도입하면 헬스케어 임상 분석 시장의 원동력이 되는 기계 판독 가능한 종단 환자 데이터를 확보할 수 있습니다. Kaiser Permanente의 Advanced Alert Monitor는 EHR 워크플로에 예측 알고리즘을 통합하여 입원 환자의 사망률을 20% 감소시켰습니다. 벤더의 로드맵은 현재 2025년 대대적인 릴리스가 예정되어 있는 Oracle Health의 차세대 플랫폼 등 임상에 내장된 AI 에이전트가 중심이 되고 있습니다. FHIR과 같은 표준화 노력은 데이터의 상호 운용성을 더욱 용이하게 하고 여러 기관의 결과 벤치마크 및 관리 갭 분석을 촉진합니다. 규제 당국이 디지털 품질 보고에 대한 보상금을 계속 제공하고 있기 때문에 EHR 주도의 애널리틱스 구매 결정은 눈사람 식으로 늘고 있습니다.

미국 식품의약국은 1,000개가 넘는 AI 대응 의료기기를 승인하고 있으며, 이는 임상용도의 머신러닝에 대한 규제 당국의 신뢰를 나타내는 이정표입니다. 예를 들어, ChristianaCare의 간략화된 예측 모델은 투명한 특징의 가중치를 통해 임상의의 신뢰를 유지하면서 90일 재입원 위험의 국기에서 78%의 정확도를 달성했습니다. 스탠포드 헬스케어의 ChatEHR과 같은 생성적인 AI 프런트엔드는 의사가 자연어로 의료진을 조회할 수 있게 하고, 정보 검색 시간을 단축하고, 번아웃을 억제할 수 있습니다. 이미지, 메모, 유전체과 같은 멀티모달 데이터를 융합하는 능력은 정밀 치료의 선택을 지원하고 헬스케어 임상 분석 시장 전체의 장기 수요를 견인합니다.

병원에 대한 랜섬웨어 공격은 2024년에 다시 급증하고, 적은 가동 중단과 규제 당국의 벌금을 모두 위협하는 이중 공갈 전술을 무기로 삼고 있습니다. 생명과학기업의 90%가 2024년 사이버 보안 예산을 늘렸으며, 개인의료정보를 보호하기 위해 현재 필요한 경계 규모가 밝혀졌습니다. EU의 GDPR(EU 개인정보보호규정)과 같은 컴플라이언스 프레임 워크는 엄격한 위반 통지의 타임라인과 엄격한 처벌을 부과하고 개방적인 데이터 교환을 연상시키고 알고리즘 훈련의 폭을 좁히고 있습니다. 첨단 공급자는 애널리틱스의 깊이와 수비 의무 간의 균형을 맞추기 위해 협력 학습 및 동형 암호화와 같은 개인 정보 보호 기술을 채택합니다. 그러나 이러한 조치는 대기 시간과 비용 오버 헤드를 증가시킵니다.

기술적 분석은 2024년 매출의 45.2%를 차지했으며, 대부분의 조직이 고차원 작업을 수행하기 전에 성능 기준을 소급적으로 시각화할 필요가 있음을 뒷받침합니다. 한편, 인지 애널리틱스는 CAGR 28.0%로 확대될 것으로 예측되어, 기술 벤더에게 헬스케어 임상 분석 시장 전체의 규모를 확대하는데 있어 매우 중요한 역할을 하는 것이 실증됩니다. 자연언어 처리와 생성적 추론에 힘입어 인지 엔진은 검사치, 화상검사, 임상메모를 자율적으로 합성하여 감별진단을 제안합니다. 스탠포드 헬스케어의 ChatEHR 시험 운용은 대화형 인터페이스가 차트 검토 시간을 단축하고 진단의 신뢰성을 높이는 방법을 소개합니다. FDA의 진화하는 제품 수명주기 전체에 대한 지침은 적응 알고리즘의 시판 전 문서 요구사항을 명확히 함으로써 이 궤도를 뒷받침하고 있습니다.

과부하에 시달리는 임상의들의 업무 시간을 절약한다는 점에서도 모멘텀(추진력)이 반영됩니다. 알고리즘이 구조화된 필드를 사전에 입력하고 가이드라인과 일치하는 주문을 표시함으로써 의료 제공업체는 환자와의 대면 시간을 회복할 수 있습니다. Epic과 같은 플랫폼의 기존 기업은 임상가에게 이기종 분석 포털을 전환하는 것을 강력하게 하는 대신 워크플로우 캔버스에 대규모 언어 모델의 코필럿을 직접 통합하고 있습니다. 인지 출력이 대시보드 수준의 경고에서 주문 세트의 인라인 너지로 이동함에 따라 다운스트림 사용자가 증가하고 의료 임상 분석 시장의 설치 기반이 확대됩니다. 모델 출력, 히트 맵 및 기여 기능에 대한 설명 가능성을 쌓는 공급업체는 의료 법적 위험을 억제하고 기관의 사인오프를 가속화하는 데 도움이 됩니다.

재무 분석은 2024년에 34.7%로 계속해서 최대 수익 블록을 공급합니다. 이는 수익주기 팀이 전환하는 지불자 규칙에 따라 상환을 지켜야 하기 때문입니다. 그러나 집단건강관리는 CAGR 26.5%로 가속화되어 헬스케어 임상 분석 시장에 가장 급격한 상승을 가져옵니다. 예측적 위험 점수는 COPD, 당뇨병 및 CHF의 비정상적인 값을 고액의 악화가 발생하기 전에 확인합니다. Accenture와 CCS의 PropheSee 모델은 85%의 예측 정확도를 달성하고 적극적인 아웃리치를 통해 당뇨병 환자 1인당 연간 2,200달러를 절약할 수 있습니다.

메디케어 어드밴티지의 보급률이 적격 고령자의 70%를 넘어, 캐피타티드 엔티티가 하류의 비용 리스크를 부담하는 동기부여가 됩니다. 의료 품질 개선 대시보드는 CMS의 별 평가 보너스 결제와 연동되어 재입원, HCAHPS 점수 및 복약 규정 준수를 추적하는 분석 모듈을 활성화합니다. 데이터세트가 사회적 결정 요인과 홈 디바이스의 피드를 통합함에 따라 세분화는 '고비용'에서 개인화된 차선책의 오케스트레이션으로 심화되고, 헬스케어 임상 분석 시장 규모가 확대되고, 클라우드 네이티브 플랫폼의 선행자 이익이 강화됩니다.

북미는 첨단 IT 인프라, EHR 보급, 명확한 진료 보상 인센티브에 힘입어 지역별로 가장 큰 공헌을 하고 있습니다. Epic이 미국의 급성기 병상의 42.3%를 획득한 것은 기존 워크플로우에 애널리틱스를 원활하게 번들 수 있는 기술 리더에게 규모의 우위성이 있음을 뒷받침하고 있습니다. 동시에 연방 정부의 지급 개혁과 사이버 보안 보조금은 AI 업그레이드를 위한 지속적인 자본 배분을 유지하고 의료 임상 분석 시장이 성장하고 있습니다.

유럽에서는 상호 운용성과 알고리즘의 투명성을 의무화하는 '유럽 의료 데이터 공간'과 'EU AI법' 등 획기적인 디지털 건강 규제가 가속화되고 있습니다. 독일의 의료 데이터 이용법과 프랑스의 임상 검증 패스웨이의 강화는 벤더의 전개 모델을 형성하는 엄격한 GDPR(EU 개인정보보호규정) 세이프 가드를 수반한다고 해도, 국경을 넘은 조사 네트워크에 박차를 가하고 있습니다. 이러한 이니셔티브는 모집단 규모 분석을 강화하는 표준화된 데이터 레이크를 촉진하고 이 지역의 세계 성장에 중기적인 기여를 강화합니다.

아시아태평양은 중국, 인도, 일본 정부가 클라우드 인프라, AI 인재 파이프라인, 국민건강 ID 제도에 자금을 투입하고 있기 때문에 CAGR이 가장 급상승하고 있습니다. 사우디아라비아의 '비전 2030'의 건강 요소 등 공공 부문의 현대화는 그 예입니다. 이는 베이스라인 데이터의 유동성을 확립하고 공립·사립병원을 불문하고 헬스케어 임상 분석 시장을 확대하는 것입니다. 이기종 레거시 시스템과 노동력 스킬 업에는 과제가 남아 있지만, 타겟을 좁힌 투자 회랑이나 현지어의 AI 인터페이스에 의해 준비 태세의 갭은 서서히 해소되고 있습니다.

The healthcare clinical analytics market is valued at USD 16.26 billion in 2025 and is projected to reach USD 42.10 billion by 2030, advancing at a 20.96% CAGR.

Surge in electronic health record (EHR) maturity, rapid progress in artificial intelligence (AI) techniques, and the global shift to value-based reimbursement are catalyzing demand for real-time, data-driven decision support. Providers increasingly need to convert the exploding volume of structured and unstructured health data into actionable insights that improve outcomes while containing costs. Intensifying cost-reduction pressures, the search for operational efficiency amid workforce shortages and fresh regulatory clarity for AI-enabled software as a medical device further accelerate uptake across care settings. Regionally, North America maintains clear leadership because of entrenched EHR penetration and favorable reimbursement rules, whereas Asia-Pacific posts the fastest growth on the back of large-scale digitization programs and widening access to cloud infrastructure. Descriptive analytics still account for the lion's share of spending, yet cognitive analytics is expanding the addressable healthcare clinical analytics market by automating higher-order reasoning tasks and reducing clinician workload.

The installation of certified EHR systems across hospitals and ambulatory practices unlocks machine-readable, longitudinal patient data that fuels the healthcare clinical analytics market. Kaiser Permanente's Advanced Alert Monitor reduced inpatient mortality by 20% after embedding predictive algorithms inside its EHR workflow. Vendor roadmaps now center on clinically embedded AI agents, such as Oracle Health's next-generation platform, slated for broad release in 2025, which incorporates voice-enabled automation and ambient documentation to minimize charting time. Standardization efforts such as FHIR further ease data interoperability, encouraging multi-institution outcome benchmarking and care-gap analysis. With regulators continuing to reward digital-quality reporting, the result is a snowball effect in EHR-driven analytics purchasing decisions.

The U.S. Food and Drug Administration has cleared more than 1,000 AI-enabled medical devices, a milestone signaling regulatory confidence in machine learning for clinical use.Real-world deployments mirror this optimism, for instance, ChristianaCare's simplified predictive model achieves 78% accuracy in flagging 90-day readmission risk while preserving clinician trust through transparent feature weighting. Generative AI front-ends such as Stanford Health Care's ChatEHR allow physicians to interrogate charts with natural language, cutting information-retrieval time and curbing burnout. The ability to fuse multimodal data, such as images, notes, and genomics, underpins precision therapy selection and drives longer-range demand across the healthcare clinical analytics market.

Ransomware attacks on hospitals surged again in 2024, with adversaries weaponizing double-extortion tactics that threaten both downtime and regulatory fines. Ninety percent of life-sciences firms raised cybersecurity budgets in 2024, underscoring the scale of vigilance now required to protect personal health information. Compliance frameworks such as the EU's GDPR impose tough breach-notification timelines and stiff penalties that dissuade open data exchanges, limiting algorithm training breadth. Forward-leaning providers are adopting privacy-preserving technologies, such as federated learning and homomorphic encryption, to strike a balance between analytics depth and confidentiality mandates. Yet, these measures add latency and cost overhead.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Descriptive analytics accounted for 45.2% of revenue in 2024, confirming that most organizations still need retrospective visibility into performance baselines before tackling higher-order tasks. Cognitive analytics, however, is forecast to expand at a 28.0% CAGR, validating its pivotal role in raising the overall healthcare clinical analytics market size for technology vendors. Fueled by natural-language processing and generative reasoning, cognitive engines autonomously synthesize lab values, imaging studies, and clinical notes to suggest differential diagnoses. Stanford Health Care's ChatEHR pilot showcases how conversational interfaces can compress chart review time and elevate diagnostic confidence. The FDA's evolving total product life-cycle guidance encourages this trajectory by clarifying pre-market documentation requirements for adaptive algorithms.

Momentum also reflects time savings for over-burdened clinicians. When algorithms pre-populate structured fields and surface guideline-concordant orders, providers regain face-to-face minutes with patients. Platform incumbents such as Epic embed large-language-model copilots directly inside their workflow canvas, rather than forcing clinicians to toggle between disparate analytics portals. As cognitive outputs move from dashboard-level alerts to inline nudges within order sets, downstream users multiply, expanding the installed base of the healthcare clinical analytics market. Vendors that layer explainability onto model outputs, heat maps, and contributing features help contain medical-legal risk and accelerate institutional sign-off.

Financial analytics continues to supply the largest revenue block at 34.7% in 2024 because revenue-cycle teams must defend reimbursement under shifting payer rules. Yet population health management is accelerating at a 26.5% CAGR, providing the sharpest uplift to the healthcare clinical analytics market. Predictive risk scoring pinpoints COPD, diabetes, and CHF outliers long before expensive exacerbations unfold. Accenture and CCS's PropheSee model hits 85% predictive accuracy and yields USD 2,200 annual savings per diabetic patient through proactive outreach.

Medicare Advantage penetration tops 70% of eligible seniors, incentivizing capitated entities to shoulder downstream cost risk. Quality-of-care improvement dashboards dovetail with CMS's star-rating bonus payments, turbo-charging analytics modules that track readmissions, HCAHPS scores and medication compliance. As datasets integrate social determinants and home-based device feeds, segmentation deepens from "high cost" to personalized next-best-action orchestration, widening the healthcare clinical analytics market size and reinforcing first-mover advantage for cloud-native platforms.

The Healthcare Clinical Analytics Market is Segmented by Technology Type (Predictive, and More), Application (Quality of Care Improvement, and More), Mode of Delivery (On-Premise, Web, and Cloud-Based), Product (Hardware, Services, and Software), End User (Healthcare Providers, Healthcare Payers, and More), and Geography (North America, Europe, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America remains the most significant regional contributor, propelled by advanced IT infrastructure, widespread EHR penetration, and well-defined reimbursement incentives. Epic's capture of 42.3% of U.S. acute-care beds underscores the scale advantages that accrue to technology leaders able to bundle analytics seamlessly inside existing workflows. Simultaneously, federal payment reform and cybersecurity grant funding sustain ongoing capital allocation toward AI upgrades that grow the healthcare clinical analytics market.

Europe accelerates behind landmark digital-health regulations such as the European Health Data Space and the EU AI Act, each mandating interoperability and algorithm transparency. Germany's Health Data Use Act and France's reinforced clinical-validation pathways are fueling cross-border research networks, albeit with strict GDPR safeguards that shape vendor deployment models. These initiatives encourage standardized data lakes that power population-scale analytics, reinforcing the region's medium-term contribution to global growth.

Asia-Pacific posts the steepest CAGR as governments in China, India, and Japan bankroll cloud infrastructure, AI talent pipelines, and national health-ID schemes. Public-sector modernization, such as Saudi Arabia's Vision 2030 health component, is illustrative. It establishes baseline data liquidity, expanding the healthcare clinical analytics market across both public and private hospitals. Challenges remain around disparate legacy systems and workforce upskilling, but targeted investment corridors and local-language AI interfaces are closing readiness gaps at pace.