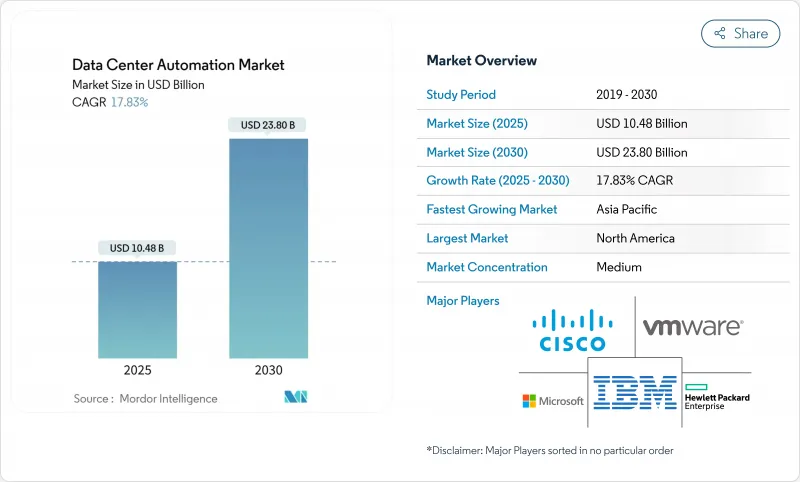

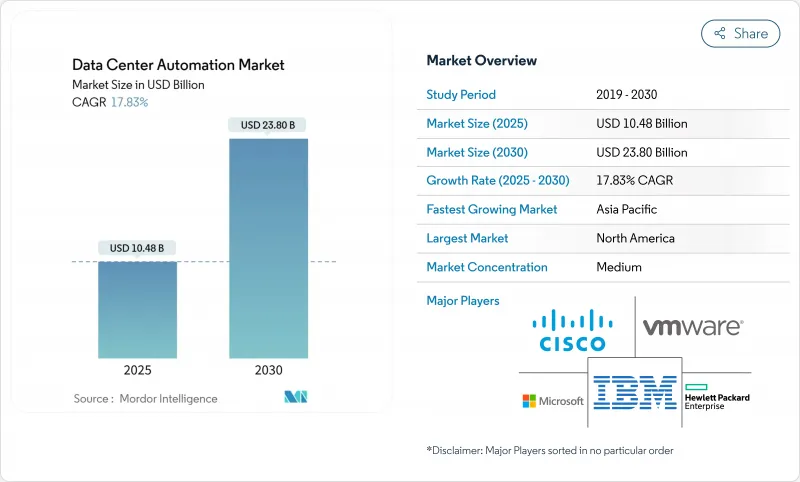

데이터센터 자동화 시장 규모는 2025년에 104억 8,000만 달러, 2030년에는 238억 달러에 이르고, 기간 중 CAGR은 17.83%를 보일 것으로 예측됩니다.

클라우드 플랫폼에 대한 의존성 증가, AI 워크로드 급증, 에너지 실적 감소에 대한 압력 증가로 인해 자동화는 운영 편의성에서 이사회 수준의 의무로 전환하고 있습니다. 하이퍼스케일을 구축하면 전력 비용을 줄이면서 서비스 품질을 유지하는 소프트웨어 정의 오케스트레이션에 대한 필요성이 증가하고 있습니다. 이와 병행하여, 모듈 설계나 액냉 시스템의 전개에서는 자동화 시스템만이 실현할 수 있는 세세한 실시간 제어가 요구되고 있습니다. 공급업체는 인프라를 자체 조정하고 하드웨어 고장을 예측하는 AI 엔진을 통합하여 노동력, 에너지 및 다운타임의 측정 가능한 절약을 실현하고 경쟁 격화가 가속화되고 있습니다. 게다가 미국 에너지부의 보고에 따르면 데이터센터의 전력 수요는 2028년까지 2배 또는 3배로 증가할 수 있으며 AI 용도가 이러한 성장의 대부분을 견인하고 있기 때문에 에너지 사용을 최적화할 수 있는 자동화 솔루션에 대한 긴급 압력이 증가하고 있습니다. 게다가 부하의 변화를 추구하고 에너지 유연성을 수익원으로 바꾸어 사업자에게 보상을 주는 성숙하고 있는 그리드 인터랙티브 프로그램에 의해 그 채택이 더욱 강화됩니다.

2025년에 예정된 하이퍼스케일 캠퍼스의 투자액은 2,500억 달러를 넘어 용량 계획, 열 관리, 워크로드의 라이브 마이그레이션에 걸친 자동화의 필요성이 발생하고 있습니다. 운영자는 컴퓨팅, 전력 및 냉각 리소스를 즉시 할당하고 운영자의 개입을 최소화하면서 서비스 수준 수요에 대응할 수 있는 AI 주도 컨트롤러를 중심으로 시설을 설계하고 있습니다. 자본 집약적인 확장은 현재 라우팅되고 테스트된 모듈형 블록과 결합되므로 오케스트레이션 소프트웨어는 각 블록을 즉시 발견, 기준화 및 통합해야 합니다. 세계 벤더는 수천 개의 자산에 정책을 적용하는 인텐트 기반 플랫폼에서 대응하며 구축 속도를 경쟁력 있는 무기로 바꾸고 있습니다.

데이터센터는 현재 세계 전력 사용량의 1-3%를 차지하고 있지만, AI의 보급이 가속되면 그 비율은 2030년까지 5%로 상승할 것으로 예측되고 있습니다. 유럽의 Climate Neutral Data Centre Pact(기후 중립 데이터센터 협정)와 같은 엄격한 이니셔티브는 새로운 PUE 상한을 1.3으로 설정하고 운영자는 공기 흐름, 팬 속도 및 워크로드 배치를 지속적으로 조정하는 자동화를 채택하도록 촉구하고 있습니다. AI를 활용한 제어로 초기 도입에서는 이미 냉각 전력이 최대 40% 삭감되고 있으며 검증 가능한 이산화탄소 삭감을 나타내는 사업자는 독자적인 ESG 목표를 달성해야 하는 하이퍼스케일 테넌트를 끌고 있습니다. 자동화된 지속가능성 보고는 컴플라이언스 오버헤드를 더욱 줄이고 규제 당국과의 투명성을 향상시킵니다.

많은 사업자들은 여전히 제한된 API로 독자적인 하드웨어를 운영하고 있으며 최신 오케스트레이션이 정착되기 전에 비용이 많이 드는 맞춤형 커넥터가 필요합니다. 네트워크 팀은 구성 실수로 인해 스크립트를 중지하는 것을 두려워하고 미션 크리티컬 트래픽을 처리하는 코어 스위치의 자동화를 망설이는 경우가 많습니다. 한 사이트용으로 제작된 템플릿이 다른 사이트에 깔끔하게 이식되는 경우는 거의 없으므로 레거시 시설 전체에서 설계가 표준화되지 않은 경우 롤아웃이 더욱 복잡해집니다. 공급업체는 광범위한 플러그인 마켓플레이스와 디바이스 구성을 리버스 엔지니어링하는 AI 기반 검색 도구를 지원하지만 기술 부채가 깊은 조직에서는 마이그레이션 일정이 여전히 장기화되고 있습니다.

2024년 데이터센터 자동화 시장 점유율에서 서버 자동화는 51.8%를 차지했지만 2030년까지 연평균 복합 성장률(CAGR)은 19.20%를 나타낼 전망이며, 네트워크 자동화가 가장 빠르게 성장하고 있습니다. 네트워크에 특화된 플랫폼의 성장은 마이크로서비스, 컨테이너 클러스터, 동서 트래픽 패턴의 보급에 의해 수작업에 의한 커맨드 라인의 변경이 압도적으로 많다는 것을 반영하고 있습니다. 기업은 비즈니스 의도를 장치 구성으로 변환하고 폐쇄 루프 원격 측정을 통해 결과를 검증하는 컨트롤러로 이동합니다. 이 시프트는 다운타임 인시던트를 줄이는 프로그래머블 QoS, 마이크로 세분화 및 자동 롤백 기능을 풀어줍니다.

중기적으로 오케스트레이션 제품군은 구성 관리, 성능 분석 및 컴플라이언스 검사와 같은 이전에 분리 된 기능을 역할 기반 액세스에 의해 관리되는 통합 툴 체인에 수렴합니다. AI를 활용한 진단은 대기 시간의 근원을 파악하고 개선 방법을 제안함으로써 해결까지의 평균 시간을 단축합니다. 그 결과 경영진은 네트워크 자동화를 비용센터가 아닌 전략적 투자로 파악하게 되었습니다. 기업의 30%가 2026년까지 네트워크 활동의 적어도 절반을 자동화하는 것을 목표로 하고 있으며, 인텐트 기반 네트워킹의 보급을 위한 기반이 갖추어지고 있습니다.

2024년 데이터센터 자동화 시장 규모는 Tier 3 시설이 45.20%를 차지하지만, Tier 4 시설은 99.995%의 업타임이 기대되기 때문에 CAGR은 18.34%가 됩니다. Tier 4 캠퍼스 운영자는 오케스트레이션된 페일오버 프로세스, 실시간 건전성 스코어링 및 자체 복구 메시 아키텍처에 의존합니다. 자동화된 진단 기능을 사용하면 중복 경로와 환경 센서를 1분에 수천 번 검사하여 선수를 치는 부품을 교체하고 부하를 이동합니다.

반대로, Tier 1과 Tier 2 사이트는 예산 제한에서 백업 스케줄링 및 패치 관리에 중점을두고 선택적 자동화를 추구합니다. 그러나 소프트웨어 비용 저하와 모듈러 컨트롤러 설계로 인해 진입 장벽이 낮아졌습니다. 재해 복구 오케스트레이션은 보편적인 우선순위가 되고 있습니다. 현재는 자동화된 런북이 매달리지 않고 매월 장애 조치 시퀀싱를 테스트하고 수익을 보호하면서 감사 요구 사항을 충족합니다. 이러한 기능을 통해 티어 레벨 간의 운영 격차가 점차 줄어들고 업계 전반의 기본 기대가 높아지고 있습니다.

데이터센터 자동화 시장은 솔루션별(서버 자동화, 네트워크 자동화 등), 데이터센터 계층 유형별(계층 1 및 2, 계층 3, 계층 4), 배포 형태별(On-Premise, 클라우드), 데이터센터 유형별(하이퍼스케일러/클라우드 서비스 공급자, 공동 위치 공급자 등), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 클라우드 보급과 대규모 자본 풀에 대한 액세스로 2024년 데이터센터 자동화 시장 점유율의 46.30%를 유지했습니다. 버지니아 북부와 같은 코어 회랑에서는 전력 제약이 있어 이용 가능한 메가와트를 최대한 활용하는 그리드 인터랙티브 오토메이션에 주목이 모여 있습니다. 데이터센터의 전력 수요가 2028년까지 두 배로 증가할 가능성을 보여주는 연방 정부 조사는 유휴 소비를 최소화하고 수요 반응 프로그램을 통해 유연성을 수익화하는 플랫폼에 대한 관심을 높이고 있습니다. 기업의 지속가능성 시나리오는 AI 가이드를 통한 냉각 및 용량 계획 도구의 적극적인 도입을 더욱 강화하고 있습니다.

아시아태평양은 2025-2030년 CAGR 19.45%로 가장 빠르게 성장하는 지역입니다. 중국, 일본, 인도의 국가적 이니셔티브는 로컬 클라우드 존과 에지 증축을 장려하고 노동력 부족을 보완하는 자동화의 필요성을 높이고 있습니다. 태국과 인도네시아의 수십억 달러 규모의 투자를 포함한 대규모 프로젝트에서는 액체 냉각 및 재생 가능 전원이 번들되어 첫날부터 이기종 기술을 조화시키는 오케스트레이션 계층이 필요합니다.

유럽은 성숙한 코로케이션 거점과 엄격한 환경 규제를 결합하여 고급 지속가능성 자동화의 시험대 역할을 하고 있습니다. 2030년까지 기후 변화에 좌우되지 않는 시설을 실현하겠다는 약속은 1.3 이하의 PUE 목표를 유지하고 신재생에너지 사용을 검증하는 지속적 최적화 엔진을 도입하도록 운영자를 뒷받침하고 있습니다. 수요 반응에 참여하고 열 재사용 방식에 대한 인센티브는 비즈니스 사례를 강화합니다. 사우디아라비아, 아랍에미리트(UAE) 및 남아프리카의 주요 프로젝트에서는 원격지에서의 인력 배치 제한을 극복하기 위해 인터넷 제로의 실증 포인트와 자율 운전이 필요하며, 자동화는 대출과 테넌트 확보의 필수 조건이 되고 있습니다.

The data center automation market size is estimated at USD 10.48 billion in 2025 and is forecast to reach USD 23.80 billion by 2030, registering a 17.83% CAGR over the period.

Rising reliance on cloud platforms, surging AI workloads, and growing pressure to reduce energy footprints are moving automation from an operational convenience to a board-level mandate. Hyperscale build-outs have intensified the need for software-defined orchestration that maintains service quality while trimming power bills. In parallel, modular designs and liquid-cooling rollouts demand fine-grained, real-time controls that only automated systems can deliver. Competitive intensity is accelerating as vendors embed AI engines that self-tune infrastructure and predict hardware failures, yielding measurable savings on labor, energy, and downtime. Further, the U.S. Department of Energy reports that data center electricity demand could double or triple by 2028, with AI applications driving much of this growth, creating urgent pressure for automation solutions that can optimize energy usage. Adoption is further strengthened by maturing grid-interactive programs that pay operators to shift loads, turning energy flexibility into a revenue stream.

Hyperscale campuses scheduled for 2025 investment exceed USD 250 billion, creating an automation imperative that spans capacity planning, thermal management, and live migration of workloads. Operators are designing facilities around AI-driven controllers able to allocate compute, power, and cooling resources in seconds, matching service-level demands while shaving operator intervention to a minimum. Capital-intensive expansions are now coupled with modular blocks that ship pre-wired and pre-tested, so orchestration software must instantly discover, baseline, and integrate each block. Global vendors are responding with intent-based platforms that enforce policies across thousands of assets, turning build-out velocity into a competitive weapon.

Datacenters currently use 1-3% of global electricity, and projections suggest the share could rise to 5% by 2030 if AI uptake accelerates. Strict initiatives such as the Climate Neutral Data Centre Pact in Europe set a PUE ceiling of 1.3 for new builds, prompting operators to adopt automation that continually tunes airflows, fan speeds, and workload placements. AI-enhanced controls have already trimmed cooling power by up to 40% in early deployments, and operators showcasing verifiable carbon reductions are attracting hyperscale tenants that must hit their own ESG targets. Automated sustainability reporting is further lowering compliance overheads and improving transparency with regulators.

Many operators still run proprietary hardware with limited APIs, forcing costly custom connectors before modern orchestration can take hold. Network teams often hesitate to automate core switches that handle mission-critical traffic, fearing outages from mis-configured scripts. Lack of design standardization across legacy estates further complicates rollouts because templates built for one site rarely port cleanly to another. Vendors are responding with extensive plugin marketplaces and AI-based discovery tools that reverse-engineer device configurations, yet migration timelines remain protracted for organizations with deep technical debt

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Network Automation is the fastest-growing segment with a 19.20% CAGR projected through 2030, although Server Automation retained 51.8% of the data center automation market share in 2024. Growth in network-focused platforms mirrors the proliferation of micro-services, container clusters, and east-west traffic patterns that overwhelm manual command-line changes. Enterprises are shifting to controllers that translate business intent into device configurations, then verify outcomes through closed-loop telemetry. This shift unlocks programmable QoS, micro-segmentation, and automatic rollback capabilities that reduce downtime incidents.

In the medium term, orchestration suites are converging previously separate functions- configuration management, performance analytics, and compliance checks- into unified toolchains governed by role-based access. AI-powered diagnostics pinpoint latency roots and suggest remediations, shortening mean time to resolution. As a result, senior leadership now views network automation as a strategic investment rather than a cost center. Momentum is expected to continue as 30% of enterprises aim to automate at least half of their network activities by 2026, setting the foundation for widespread intent-based networking adoption.

Tier 3 facilities commanded 45.20% of the data center automation market size in 2024, but Tier 4 deployments are on track for an 18.34% CAGR thanks to stringent 99.995% uptime expectations. Operators of Tier 4 campuses rely on orchestrated failover processes, real-time health scoring, and self-healing mesh architectures. Automated diagnostics inspect redundant paths and environmental sensors thousands of times per minute, triggering pre-emptive part swaps or load transfers.

Conversely, Tier 1 and Tier 2 sites pursue selective automation, often focusing on backup scheduling and patch management, due to budget limits. Yet falling software costs and modular controller designs are lowering entry barriers. Disaster-recovery orchestration is becoming a universal priority: Automated runbooks now test failover sequences monthly without human intervention, fulfilling audit requirements while safeguarding revenue. These capabilities gradually narrow the operational disparities between tier levels and raise baseline expectations across the industry.

Data Center Automation Market is Segmented by Solution (Server Automation, Network Automation, and More), by Data Center Tier Type (Tier 1 and 2, Tier 3, and Tier 4), by Deployment Mode (On-Premise, Cloud), by Data Center Type (Hyperscalers/Cloud Service Providers, Colocation Providers, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 46.30% of the data center automation market share in 2024, benefiting from deep cloud adoption and access to large capital pools. Power constraints in core corridors such as Northern Virginia sharpen the focus on grid-interactive automation that maximizes every available megawatt. Federal research indicating that data-center electricity demand may double by 2028 magnifies interest in platforms that minimize idle consumption and monetize flexibility through demand-response programs. Corporate sustainability narratives further encourage aggressive deployment of AI-guided cooling and capacity-planning tools.

Asia-Pacific is the fastest-growing territory with a 19.45% CAGR expected between 2025-2030. National initiatives in China, Japan, and India incentivize local cloud zones and edge build-outs, magnifying the need for automation that can compensate for labor shortages. Large-scale projects, including multi-billion-dollar investments in Thailand and Indonesia, bundle liquid-cooling and renewable power sources, demanding orchestration layers able to harmonize disparate technologies from day one.

Europe combines mature colocation hubs with tight environmental regulation, creating a crucible for advanced sustainability automation. Commitments to achieve climate-neutral facilities by 2030 push operators to deploy continuous-optimization engines that maintain sub-1.3 PUE targets and verify renewable-energy usage. Incentives for demand-response participation and heat-re-use schemes reinforce the business case. Growing activity in the Middle East and Africa mirrors this momentum: flagship projects in Saudi Arabia, the United Arab Emirates, and South Africa require net-zero proof points and autonomous operation to overcome remote-site staffing limitations, positioning automation as a prerequisite for securing financing and tenants.