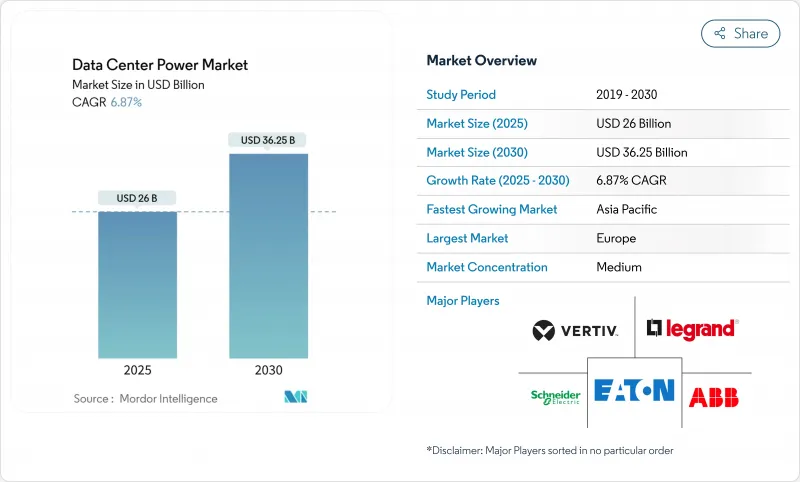

데이터센터 전력 시장 규모는 2025년에 245억 6,000만 달러, CAGR 7.25%로 성장하고, 2030년에는 348억 6,000만 달러에 달할 것으로 예측되고 있습니다.

인공지능의 확장, 적극적인 하이퍼스케일 용량의 추가, 보다 엄격한 신뢰성의 의무화는 전기 인프라의 우선순위를 재구성하고 데이터센터 전력 시장의 확대에 박차를 가하고 있습니다. 고밀도의 AI 워크로드는 기존 CPU의 3배의 전력을 소비하므로, 사업자는 보다 고전압의 배전, 액체 냉각, 그리드 인터랙티브 파워트레인으로 향하고 있습니다. 전력 회사, 규제 당국 및 클라우드 공급자가 수 기가와트의 상호 연결을 필요로 하는 대규모 프로젝트에서 발판을 정렬하면서 장비 공급업체 간의 통합이 진행되고 있습니다. 은퇴한 석탄발전소를 캠퍼스형 시설로 재이용하는 진입기업이 늘고 있는 가운데, 데이터센터 전력시장은 수동적인 에너지 소비에서 능동적인 그리드 참여로 이행하고 있으며, 언시러리 서비스를 통해 새로운 수익원을 끌어내고 있습니다.

하이퍼스케일 사업자는 중규모 도시의 전력 수요에 필적하는 캠퍼스를 운영하고 있습니다. 메타의 2GW 개발과 5.6GW 원더밸리 사이트는 클라우드 성장을 유지하는 데 필요한 규모를 보여줍니다. 슈나이더 일렉트릭은 데이터센터가 2025년 주문량의 24%를 차지하고 있음을 밝혔습니다. 전력회사의 상호연결을 단계적인 용량 해방에 연결시키는 구조화 계약은 보편화되고 있으며, 전력회사, 지주, 클라우드 테넌트 간의 리스크 배분이 개선되고 있습니다. IT 부하가 1메가와트 증가할 때마다 스위치기어, UPS, 중전압 시스템에 대한 투자가 비례하여 증가하기 때문에 데이터센터 전력 시장이 직접 이익을 얻습니다.

AI 가속기는 랙 밀도를 5-10kW에서 50-100kW로 끌어올려 48V DC 배전, 고위상수, 액냉으로의 이행을 강요합니다. Vertiv의 360AI 플랫폼은 통합 버스웨이, 냉각수 분배 및 누출 감지 제어를 통해 랙당 100kW를 지원합니다. 지속적인 열부하는 UPS 장비의 듀티 사이클을 증가시키므로 부분 부하 시 효율 곡선은 중요한 선택 지표가 됩니다. 국제에너지기구의 예측에 따르면 AI는 2029년까지 세계 전력의 1.5%를 소비할 가능성이 있으며, GPU 사용률과 동기하여 동적으로 스로틀을 전환하는 에너지 비례 전원 시스템의 긴급성이 높아지고 있습니다. 전원과 냉각을 컴팩트한 조립식 블록에 통합하는 공급업체는 운영자가 예측 가능한 배포 일정을 추구하는 동안 점유율을 얻었습니다.

AI 대응 캠퍼스의 엔드 투 엔드 비용은 MW당 3,800만 달러에 육박해, 액냉은 파워트레인의 지출을 공냉 베이스의 설계에 비해 15-20배로 부풀립니다. 소규모 공동 위치 사업자는 맞춤형 중간 전압 기어, 긴 리드 변압기 및 특수 배터리에 대한 자금을 확보하기가 어렵습니다. 서비스로서의 설비계약이 대두되고 있지만, 특주 스위치기어의 2차 시장가치는 한정되어 있기 때문에 금융기관은 신중한 자세를 무너뜨리지 못하고 있습니다. 예산의 제약은 신흥국에서의 사업 확대를 늦추고 데이터센터 전력 시장의 호조로운 궤도를 약화시키고 있습니다. 자금 조달의 격차는 지주와 전력 회사가 공동 출자하는 합작 모델에도 박차를 가하고 리턴은 희박화되지만 프로젝트의 실행 가능성은 확보됩니다.

UPS 플랫폼은 2024년 데이터센터 전력 시장 점유율의 62.1%를 유지해 송전망 불안정성에 대한 마지막 방어 수단으로서의 역할을 명확히 했습니다. 리튬 이온의 채용은 계속되고 있지만, 저밀도 홀에서의 비용 우위성으로부터, 밸브 제어 납 축전지가 여전히 주류입니다. 지능형 스위치 모드 정류기는 변환 손실을 줄이고 시설 전체의 에너지 프로파일을 개선합니다. 병행하여 배전 장치는 CAGR은 7.5%를 기록했습니다. 이는 사업자가 분기 회로 모니터링, 온도 감지, 안전한 펌웨어를 통합하기 때문입니다. 발전기는 여전히 필수적이지만 수소 대응 발전기가 시험적으로 사용되고 시나리오는 변화하고 있습니다. 스위치기어 업그레이드는 AI 랙이 요구하는 고전압에 해당하며 배터리 에너지 저장 시스템은 피크 컷 및 수익 쌓기를 위해 지원됩니다.

UPS 공급업체가 그리드 서비스 모듈을 추가하고 라이드스루 성능을 저하시키지 않고 주파수 조정을 가능하게 함으로써 생태계의 역학을 변화시킵니다. Vertiv의 그리드 인터랙티브 펌웨어는 중요하지 않은 시간대에 예비 용량을 발송합니다. 델타 스마트 PDU I-Type은 고밀도 AI 인클로저를 대상으로, 미터링 기능과 원격 업그레이드 기능을 42mm 섀시에 통합합니다. 고밀도 홀 시운전에는 열 매핑, 고조파 조사 및 지속적인 펌웨어 검증이 필요하므로 서비스 수익이 증가합니다. 그 결과, 운영자는 수명 주기 지원을 외주하고 통합자의 예측 가능한 연금 형태의 수입원을 촉진하고 데이터센터 전력 시장을 풍부하게 합니다.

코로케이션 시설은 2024년 데이터센터 전력 시장 규모에서 43.8%의 점유율을 차지했습니다. 하지만 하이퍼스케일러는 CAGR 8.7%를 차지하며 애플, 마이크로소프트, 구글의 AI 호스팅 존의 자체 구축 전략에 힘쓰고 있습니다. 엔터프라이즈 캠퍼스는 컴플라이언스에 민감한 산업을 위해 지속되고 있으며, 에지 노드는 대기 시간을 줄이기 위해 인구 클러스터 근처에서 성장하고 있습니다. 하이퍼스케일러는 현장 변전소와 배터리 팜을 통합한 독자적인 전력 토폴로지를 설계하고, 코로케이션 기업은 유연한 전력 밀도와 상호 연결 패브릭으로 대응합니다.

경쟁의 긴장이 혁신을 촉진합니다. 핵심 사이트는 액체 칩 냉각과 48V 버스웨이를 차세대 홀의 표준으로 홍보하고 클라우드 대기업은 15MW 단위로 모듈 블록을 개선하고 있습니다. 양진영 모두 자본배분과 즉각적인 가동을 분리한 종량제 계약을 채용하고 있습니다. 에지 사업자는 표준화된 마이크로 파워 모듈을 도입하여 5G 배포에 보조를 맞춥니다. 이러한 전략이 얽히면 데이터센터 전력 시장에 유입되는 장비의 수량이 증가합니다.

유럽이 2024년 매출액 점유율 34.18%로 선두를 차지했습니다. 사업자는 에너지 효율 지침을 충족하기 위해 레거시 시설을 고효율 UPS 및 배터리 스토리지로 개조합니다. Sines DC와 같은 석탄 발전소의 전환은 기존 계통 연계와 해수 취수 라인을 재사용하여 환경에 미치는 영향을 억제하면서 도입을 가속화합니다. 벤더는 풍력이 풍부한 지역의 송전망을 안정화시키는 그리드 인터랙티브 UPS를 공급하여 지속가능한 설계에서 유럽 대륙의 리더십을 강화하고 있습니다. 기업 바이어는 재생 가능한 원산지 보증이 인터넷 제로 서약을 지원하고 데이터센터 전력 시장 전체의 장비 수요를 유지하기 위해 유럽 사이트를 선호합니다.

아시아태평양은 정부가 클라우드 코리도에 자금을 공급하고 토지, 섬유, 전력에 보조금을 내고 있기 때문에 CAGR이 가장 빠른 9.2%입니다. 2024년 하반기 시점에서 아시아태평양의 생산 IT 용량은 12,206MW로 14,338MW가 건설 중입니다. Microsoft는 인도와 일본에서 수십억 달러 규모의 계획을 발표하고 사업 확대의 규모를 강조하고 있습니다. 중국이 PUE 상한 규제를 실시해, 고효율 전력 부품의 발주가 가속. 인도의 디지털 개인 데이터 보호법은 국내 호스팅을 추진하고 신재생 에너지 클러스터에 가까운 새로운 캠퍼스를 자극합니다. 동남아시아 국가들은 하이퍼스케일러를 유치하기 위해 감세 조치를 취하여 스위치기어, UPS, 스마트 PDU의 조달 파이프라인을 더욱 확대하고 있습니다.

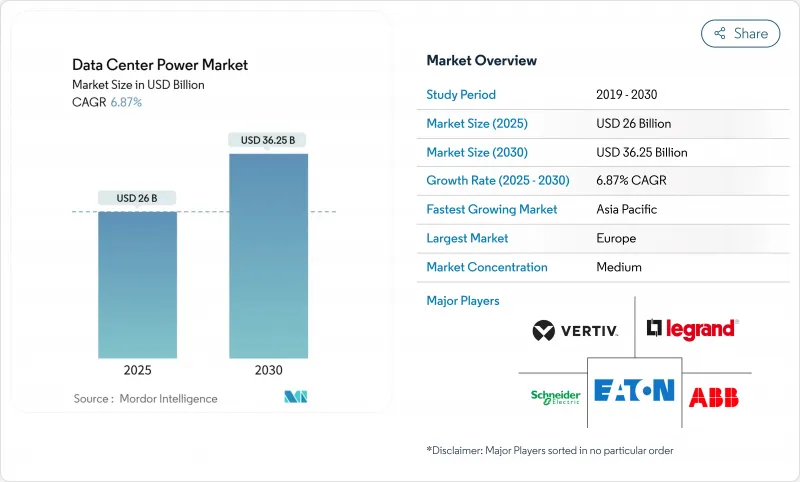

The data center power market size is expected to be valued at USD 24.56 billion in 2025 and is projected to advance at a 7.25% CAGR, reaching USD 34.86 billion by 2030.

Growing deployment of artificial intelligence, aggressive hyperscale capacity additions, and stricter reliability mandates are reshaping electrical infrastructure priorities and fueling expansion in the data center power market. High-density AI workloads consume three times more electricity than conventional CPUs, pushing operators toward higher-voltage distribution, liquid cooling, and grid-interactive power trains. Consolidation among equipment suppliers is strengthening as utilities, regulators, and cloud providers align on large-scale projects that require multi-gigawatt interconnections. With more operators repurposing retired coal plants for campus-style facilities, the data center power market is transitioning from passive energy consumption to active grid participation, unlocking new revenue streams through ancillary services.

Hyperscale operators are commissioning campuses that equal the electricity demand of medium-sized cities. Meta's 2 GW development and the 5.6 GW Wonder Valley site illustrate the scale now required to sustain cloud growth. Orders for modular, factory-integrated power trains are rising sharply, and Schneider Electric disclosed that data centers made up 24% of its incoming orders in 2025. Structured agreements tying utility interconnections to phased capacity releases are becoming common, improving risk allocation among utilities, landlords, and cloud tenants. The data center power market benefits directly because every incremental megawatt of IT load drives proportional investment in switchgear, UPS, and medium-voltage systems.

AI accelerators raise rack densities from 5-10 kW to 50-100 kW, forcing a move to 48 V DC distribution, higher phase counts, and liquid cooling. Vertiv's 360AI platform supports 100 kW per rack with integrated busway, coolant distribution, and leak-detection controls. Persistent thermal loads increase the duty cycle of UPS equipment, making efficiency curves at partial load a critical selection metric. International Energy Agency projections indicate AI could consume 1.5% of global electricity by 2029, reinforcing the urgency for energy-proportional power systems that dynamically throttle in sync with GPU utilization. Vendors that marry power and cooling into a compact, prefabricated block are capturing share as operators seek predictable deployment timelines.

End-to-end cost for AI-ready campuses approaches USD 38 million per MW, with liquid cooling inflating power-train expenditures by 15-20X compared with air-based designs. Smaller colocation players find it challenging to secure financing for customized medium-voltage gear, long-lead transformers, and specialized batteries. Equipment-as-a-service contracts are emerging, yet lenders remain cautious because secondary-market values for bespoke switchgear are limited. Budget restrictions slow expansion in emerging economies, tempering the otherwise robust trajectory of the data center power market. Financing gaps also spur joint-venture models where landlords and utilities co-invest, diluting returns but enabling project viability.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

UPS platforms retained 62.1% of the data center power market share in 2024, underscoring their role as the last defense against grid instability. Lithium-ion adoption continues, but valve-regulated lead-acid remains prevalent due to cost advantage in lower-density halls. Intelligent switch-mode rectifiers trim conversion losses, improving overall facility energy profiles. In parallel, power distribution units record 7.5% CAGR because operators now embed branch-circuit monitoring, temperature sensing, and secure firmware. Generators stay indispensable, yet the narrative shifts as hydrogen-ready gensets enter pilot use. Switchgear upgrades align with higher voltages demanded by AI racks, and battery energy storage systems gain favor for peak-shaving and revenue stacking.

Ecosystem dynamics shift as UPS vendors add grid services modules, enabling frequency regulation without undermining ride-through performance. Vertiv's grid-interactive firmware dispatches reserve capacity during non-critical intervals. Delta's Smart PDU I-Type consolidates metering and remote-upgrade functions into a 42 mm chassis aimed at dense AI enclosures. Services revenue rises because commissioning high-density halls requires thermal mapping, harmonic studies, and ongoing firmware validation. Consequently, operators outsource lifecycle support, driving predictable, annuity-style income streams for integrators and enriching the data center power market.

Colocation facilities held a 43.8% share of the data center power market size in 2024, thanks to shared infrastructure economics and rapid time-to-market. Yet hyperscalers post an 8.7% CAGR, propelled by Apple, Microsoft, and Google's strategies to self-build AI hosting zones. Enterprise campuses persist for compliance-sensitive industries, and edge nodes proliferate near population clusters to lower latency. Hyperscalers design proprietary power topologies, integrating on-site substations and battery farms, while colocation players counter with flexible power densities and interconnect fabrics.

Competitive tension fosters innovation: CoreSite advertises liquid-to-chip cooling and 48 V busway as standard in next-gen halls, whereas cloud majors refine modular blocks for 15 MW increments. Pay-as-you-grow contracts appear in both camps, decoupling capital allocation from immediate occupancy. Edge operators deploy standardized micro power modules to keep pace with 5G rollouts. These intertwined strategies collectively elevate equipment volumes flowing into the data center power market.

The Data Center Power Market is Segmented by Component (Electrical Solutions and Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV) and by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Europe led with 34.18% revenue share in 2024, driven by binding energy-efficiency legislation, stringent reporting rules, and aggressive renewable goals. Operators retrofit legacy facilities with high-efficiency UPS and battery storage to satisfy the Energy Efficiency Directive. Coal-plant conversions such as Sines DC repurpose existing grid interconnections and seawater intake lines, accelerating deployment while curbing environmental impact. Vendors supply grid-interactive UPS that help stabilize wind-heavy regional grids, strengthening the continent's leadership in sustainable design. Corporate buyers prefer European sites because renewable guarantees of origin support net-zero pledges, sustaining equipment demand across the data center power market.

Asia-Pacific delivers the fastest 9.2% CAGR as governments fund cloud corridors and subsidize land, fiber, and electricity. Regional capacity totaled 12,206 MW of live IT load with 14,338 MW in construction as of H2 2024. Microsoft pledged multi-billion-dollar plans in India and Japan, highlighting the scale of expansion. China enforces a national PUE cap that accelerates high-efficiency power component orders. India's Digital Personal Data Protection Act drives domestic hosting and stimulates new campuses near renewable clusters. Southeast Asian nations offer tax breaks to attract hyperscalers, further widening procurement pipelines for switchgear, UPS, and smart PDUs.