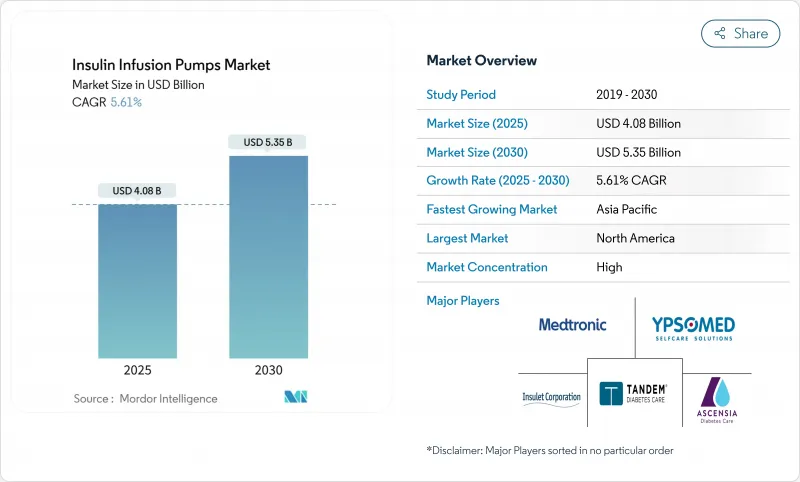

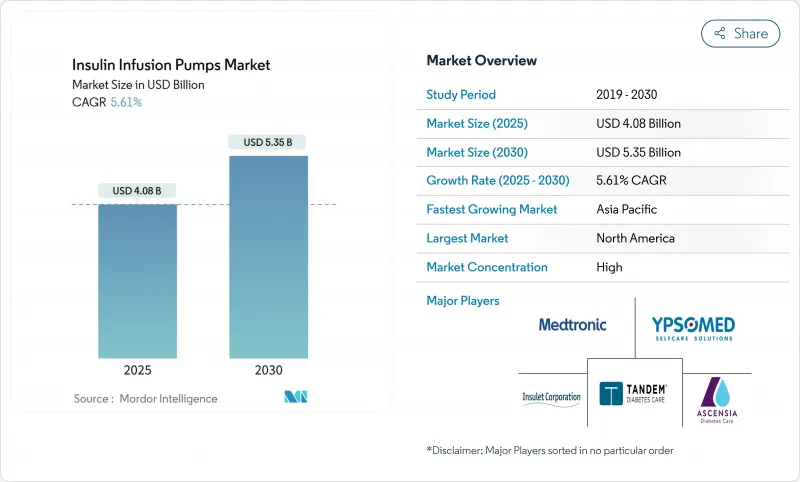

인슐린 주입 펌프 시장 규모는 2025년에 40억 8,000만 달러, 예측 기간(2025-2030년)의 CAGR은 5.61%를 나타낼 전망이며, 2030년에는 53억 5,000만 달러에 달할 것으로 예측됩니다.

수요는 지속적인 포도당 모니터링과 자동 인슐린 전달의 융합, 테더링에서 폐쇄형 루프 플랫폼으로의 전환, 2형 당뇨병 환자에 대한 광범위한 채택으로 인한 것입니다. 패치 펌프와 하이브리드 폐쇄 루프 시스템은 현재 성능 벤치마크를 설정하고 상환 확대와 소아과 승인은 사용자 기반을 확대합니다. 사이버 보안에 대한 경계, 공급망에 대한 압력, 규제의 복잡성은 계속 성장을 억제하고 있지만, 인슐린 주입 펌프 시장은 여전히 세계의 당뇨병 관리에 매우 중요합니다.

2025년 4월에 FDA가 Medtronic사의 MiniMed 780G를 승인함에 따라 자동식이 검출과 5분 이내의 인슐린 조정의 가치가 부각되고, 대규모 사용자군에서는 타임 인레인지 수치가 70%를 넘어섰습니다. 탠덤의 Control-IQ 플랫폼은 알고리즘의 정확성과 센서의 신뢰성을 보완하는 기술 경쟁을 부각시켜 동등한 이점을 보여줍니다. 인공지능은 생리적 인슐린 패턴을 모방한 복용량의 개별화를 가능하게 하고, 폐쇄 루프 플랫폼을 미래의 표준 치료로서 위치시킵니다. 임상 증명 증가는 지불자의 신뢰를 높이고 자격 기준을 확대합니다. 마케팅이 장비의 구조가 아닌 라이프 스타일의 간편함을 강조함에 따라 환자의 수용성이 높아지고 판매량 증가와 소모품의 지속적인 판매가 촉진됩니다.

미국에서는 어린이의 이환율이 1,000명당 3.5명을 넘어 유럽과 아시아 일부에서도 비슷한 증가세를 보이고 있습니다. 소아과학회는 우수한 혈당 조절과 야간 저혈당 감소를 이유로 펌프 요법을 제1선택 치료로 권장하고 있습니다. FDA에 의한 2세 이상의 자동 인슐린 제제의 인가에 의해 소아과의 대응 가능한 연령층이 퍼지고 있습니다. 지역등록은 임상지원이 지연된 미충족 수요를 시사하고 채택의 격차를 밝혔습니다. 제조업체는 소형 저장소, 간소화 된 사용자 인터페이스, 청소년 사용자 및 간병인의 공감을 부르는 다채로운 패치 접착제로 대응합니다.

2024년, FDA는 특정 무선 펌프가 무단 액세스나 의도파관 않은 인슐린 투여를 가능하게 하는 취약점이 있음을 지적하고 여러 클래스 i 리콜을 촉구했습니다. 그 후, 학술적 분석은 안전하지 않은 블루투스 채널을 통한 잠재적인 악용 경로를 문서화하여 엔드 투 엔드 암호화 및 변조 방지 펌웨어의 필요성을 강조했습니다. FDA의 새로운 시판 전 지침은 위협 완화 계획 및 시판 후 모니터링을 요구하고 개발 비용을 증가시키고 승인 일정을 연장합니다. 병원은 현재 공급하기 전에 상세한 사이버 보안 인증서 제출을 요청합니다. 환자에 대한 치명적인 피해는 보고되지 않지만, 위험 회피를 선호하는 지불자들 사이에는 위험 인식이 남아 있기 때문에 도입이 지연될 수 있습니다.

인슐린 펌프는 2024년 매출의 65.73%를 차지했으며, 고가격 설정과 임베디드 소프트웨어의 복잡성을 뒷받침하고 있습니다. 그러나 소모형 저장소는 하이브리드 폐쇄 루프 알고리즘이 인슐린 마이크로볼을 더 자주 조절하게 되었기 때문에 CAGR 8.01%로 급속히 확대했습니다. 폐색과 기포를 감지하는 스마트 센서를 저장소에 통합하면 환자의 안전성이 향상되고 공급업체가 교차 셀을 배포할 수 있습니다. Medtronic의 펌프와 Abbot의 포도당 센서의 조합과 같은 전략적 파트너십은 조달에 영향을 미치는 생태계 접근법의 예입니다.

소모품 역학은 경상 수익의 가시성을 향상시킵니다. 제조업체 각 사는 삽입시의 외상을 경감해, 브랜드 로열티를 높이기 위해서, 7일간 사용 가능한 연장형 주입 세트를 도입하고 있습니다. 경쟁사와의 차별화는 현재 마찰이 없는 카트리지 로딩, 잔류 인슐린 폐기물 감소, 감염 위험을 억제하는 항균 라이닝에 달려 있습니다. 이러한 기술 혁신은 성숙시장에서 장비 교환주기가 길어지더라도 판매대수 전망을 안정시킵니다.

패치 펌프는 2024년에 52.61%의 점유율을 획득했으며, CAGR은 8.74%를 나타낼 전망이며, 튜브리스로 눈에 띄지 않는 웨어러블에 대한 환자의 기호가 입증되었습니다. 정교한 산업 디자인, 방수 하우징, 자동 캐뉼라 삽입은 사용자의 편안함을 높이고 사회적 스티그마를 최소화합니다. 테더 펌프는 감소하는 경향이 있지만 대용량 저장소가 필요한 고용량 사용자 및 듀얼 호르몬 연구 프로토콜을 지원합니다. 임베디드 시스템은 수술 수술 장애물로 인해 여전히 실험적입니다.

탠덤사의 모비가 얇고 스마트폰 전용 인터페이스로 인슐릿에 과제하고 패치 분야에서의 경쟁이 격화하고 있습니다. 신규 진출기업은 아시아태평양을 위한 저렴한 패치 옵션을 제공하고 간소화된 기능 세트와 구독 가격을 번들로 제공합니다. 무선으로 전달되는 펌웨어 업그레이드는 물리적 교환 없이 기능을 강화하여 사용자의 정착성을 높입니다.

북미는 2024년도 37.32%의 점유율로 최대 시장으로 보험 적용 범위의 폭, 선진적인 공급망, 1형과 2형 모두의 조기 수요에 지지되고 있습니다. 이 지역의 성숙한 인프라는 폐쇄 루프 업그레이드와 상호 운용 가능한 구성요소 생태계의 신속한 도입을 지원하지만, 대수 증가는 현재 신규 사용자의 순 증가보다 구매 사이클을 반영합니다. 사이버 보안 규제도 이 지역이 발단되고 있어 세계적인 설계 기준에 영향을 미치고 있습니다.

유럽은 국민 모두 보험 제도와, 결과를 벤치마크로 하는 견고한 임상 등록 덕분에, 안정된 판매 대수를 자랑하고 있습니다. 보험 상환의 틀은 다양하지만, 일반적으로 입원 비용의 삭감이 증명된 기술이 지지되고 있습니다. 통합형 펌프와 지속 포도당 모니터의 CE 마크 취득이 급속히 진행되어 경쟁력의 다양성이 촉진되고 있습니다. 중동 및 아프리카에서는 보급이 늦었지만 사우디아라비아와 UAE에서는 투자 이니셔티브에 의해 공적 당뇨병 센터에 패치 펌프를 도입하는 파일럿 프로그램이 개시되고 있습니다.

아시아태평양은 당뇨병 유병률 상승, 도시화, 중간층 보험 풀의 확대로 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 7.07%로 성장할 전망입니다. 중국의 단계적 병원 제도에서는 현재 소아 1형 유저용으로 일부 패치 펌프가 상환되고 있으며, 인도에서는 2형 성인용으로 저비용의 구독 번들이 실험적으로 도입되고 있습니다. 라틴아메리카에서는 민간 보험 회사가 가치 기반 당뇨병 프로그램을 시험적으로 도입하고 있으며, 브라질과 멕시코가이 지역의 도입을 이끌고 있습니다. 시장 진입 각 회사는 현지 언어 대응, 고온 환경에서의 접착제 처방, 유연한 자금 조달 등을 각 지역의 사회 경제적 프로파일에 적합하도록 목표로 하고 있습니다.

The Insulin Infusion Pumps Market size is estimated at USD 4.08 billion in 2025, and is expected to reach USD 5.35 billion by 2030, at a CAGR of 5.61% during the forecast period (2025-2030).

Sustained demand arises from the convergence of continuous glucose monitoring with automated insulin delivery, the transition from tethered to closed-loop platforms, and broader adoption among Type 2 diabetes patients. Patch pumps and hybrid closed-loop systems now set performance benchmarks, while reimbursement expansion and pediatric approvals enlarge the user base. Cybersecurity vigilance, supply-chain pressures, and regulatory complexity continue to temper growth, yet the insulin infusion pumps market remains pivotal to global diabetes management.

FDA approval of Medtronic's MiniMed 780G in April 2025 underscored the value of automated meal detection and five-minute insulin adjustments, pushing time-in-range figures above 70% among large user cohorts. Tandem's Control-IQ platform shows comparable benefits, highlighting a technology race that rewards algorithm accuracy and sensor reliability. Artificial intelligence enables dose personalization that mimics physiologic insulin patterns, positioning closed-loop platforms as the future standard of care. Growing clinical proof amplifies payer confidence and broadens eligibility criteria. As marketing emphasizes lifestyle simplicity instead of device mechanics, patient receptivity rises, driving incremental units and recurring consumable sales.

Incidence rates among children now exceed 3.5 per 1,000 in the United States, with similar uptrends in Europe and parts of Asia. Pediatric societies recommend pump therapy as first-line treatment, citing superior glycemic control and reduced nocturnal hypoglycemia. FDA clearance of automated insulin delivery for ages two and above widens the pediatric addressable pool. Regional registries reveal adoption gaps, suggesting unmet demand where clinical support lags. Manufacturers respond with smaller reservoirs, simplified user interfaces, and colorful patch adhesives that resonate with younger users and caregivers.

In 2024 the FDA flagged vulnerabilities in certain wireless pumps that could allow unauthorized access and unintended insulin delivery, prompting multiple Class I recalls. Academic analyses have since documented potential exploit pathways via unsecured Bluetooth channels, underscoring the need for end-to-end encryption and tamper-proof firmware. New FDA premarket guidance requires threat-mitigation plans and postmarket monitoring, adding development cost and elongating approval timelines. Hospitals now press suppliers for detailed cybersecurity certifications before procurement. Although no catastrophic patient harm has been reported publicly, lingering risk perception may slow adoption among risk-averse payers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Insulin pump devices retained 65.73% of 2024 revenue, underscoring their premium pricing and embedded software complexity. Consumable reservoirs, however, expanded faster at an 8.01% CAGR as hybrid closed-loop algorithms modulated insulin micro-boluses more frequently. Integration of smart sensors inside reservoirs to detect occlusions and air bubbles heightens patient safety and gives vendors cross-selling leverage. Strategic partnerships, such as Medtronic pairing its pumps with Abbott glucose sensors, exemplify an ecosystem approach that influences procurement.

Consumable dynamics also strengthen recurring revenue visibility. Manufacturers introduce extended-wear infusion sets aimed at seven-day site usage, reducing insertion trauma and driving brand loyalty. Competitive differentiation now hinges on frictionless cartridge loading, lower residual insulin waste, and antimicrobial linings that curb infection risk. These incremental innovations stabilize unit volume outlook, even when device replacement cycles lengthen in mature markets.

Patch pumps captured 52.61% share in 2024 and are on track for an 8.74% CAGR, validating patient preference for tubeless, discreet wearables. Sleek industrial design, waterproof housing, and automated cannula insertion raise user comfort and minimize social stigma. Tethered pumps, while declining, still serve high-dose users who need large reservoirs or dual-hormone research protocols. Implantable systems remain experimental due to surgical hurdles.

Competition within the patch segment intensifies as Tandem's Mobi challenges Insulet's incumbency with a thinner profile and smartphone-only interface. Emerging entrants position low-cost patch alternatives for Asia-Pacific, bundling simplified feature sets with subscription pricing. Firmware upgrades delivered over the air enhance functionality without physical replacements, reinforcing user stickiness.

The Insulin Pump Market Report Segments the Industry Into by Component (Insulin Pump Devices, Infusion Sets, Reservoirs), Pump Type (Tethered Pumps, Patch Pumps, Implantable Pumps), Patient Type (Type-1 Diabetes, Type-2 Diabetes), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America remained the largest market in 2024 with a 37.32% share, underpinned by widespread insurance coverage, advanced supply chains, and early demand from both Type 1 and Type 2 populations. The region's mature infrastructure supports swift adoption of closed-loop upgrades and interoperable component ecosystems, though unit growth now mirrors replacement cycles more than net new users. Cybersecurity regulations also originate here, influencing global design standards.

Europe contributes steady volumes thanks to universal healthcare and robust clinical registries that benchmark outcomes. Reimbursement frameworks vary but generally favor technology proven to cut hospitalization costs. Rapid CE-mark pathways for integrated pumps and continuous glucose monitors promote competitive diversity. The Middle East and Africa lag in penetration, yet investment initiatives in Saudi Arabia and the UAE spark pilot programs that introduce patch pumps into public diabetes centers.

Asia-Pacific posts the fastest 7.07% CAGR through 2030 due to rising diabetes prevalence, urbanization, and expanding middle-class insurance pools. China's tiered hospital system now reimburses select patch pumps for pediatric Type 1 users, while India experiments with low-cost subscription bundles for Type 2 adults. Latin America sits between growth extremes, with Brazil and Mexico leading regional adoption as private insurers pilot value-based diabetes programs. Market entrants target localized language support, hotter-climate adhesive formulations, and flexible financing to fit each region's socioeconomic profile.