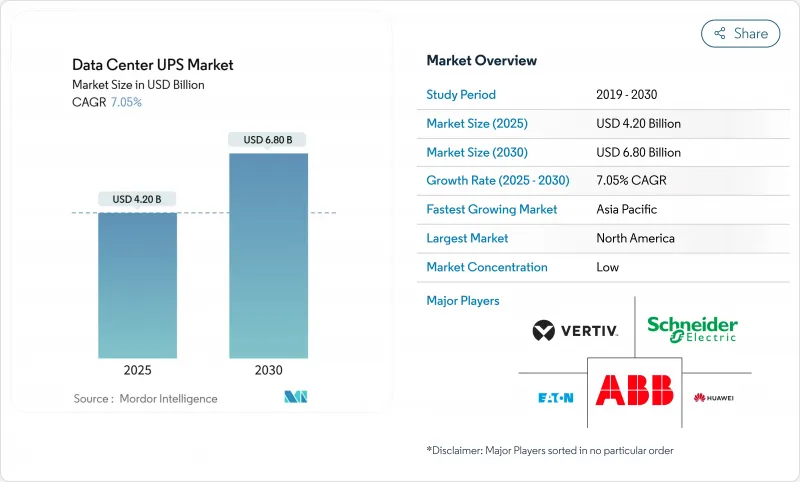

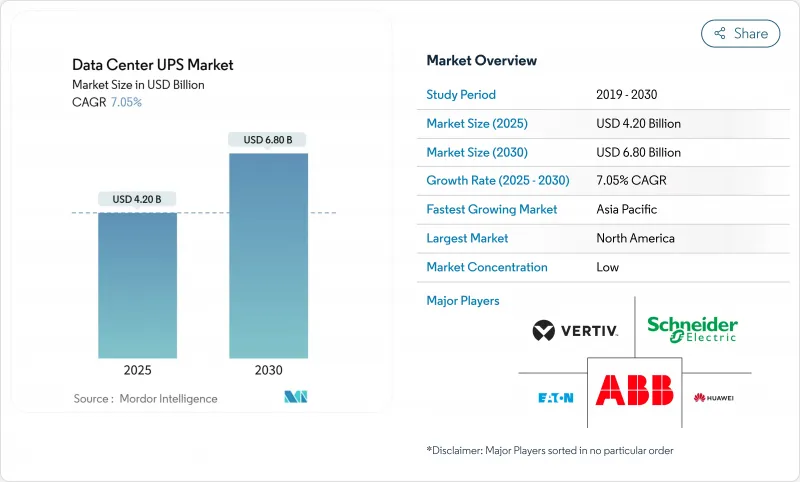

데이터센터 UPS 시장은 2025년 42억 달러에 이를 것으로 예측되며, 2030년에 68억 달러에 이를 것으로 예측되며, CAGR은 7.05%를 나타낼 전망입니다.

이 확장은 하이퍼스케일 시설 구축, 인공지능(AI) 전력 밀도 요구사항, 총소유비용을 개선하는 리튬이온 배터리 경제성과 연계됩니다. 인프라 공급업체들은 지속가능성 요구사항에 부합하는 모듈식 설계, 그리드 연동 기능, 고효율 토폴로지에 주력하고 있습니다. 2026년까지 랙 전력 밀도가 500-1,000kW 범위로 이동할 것으로 예상되면서 모든 신규 구축의 설계 규칙이 재편되고 있습니다. 전력 전자 부품의 지속적인 공급망 위험과 데이터센터 유틸리티에 대한 지역적 모라토리엄은 변동성을 초래하지만, 클라우드 공급업체의 대규모 자본 투자가 성장 동력을 유지하고 있습니다. 그 결과 데이터센터 UPS 시장은 정적 백업 장비에서 벗어나 그리드를 안정화하고 AI 워크로드를 지원하는 동적 수익 창출 자산으로 진화하고 있습니다.

마이크로소프트의 300억 달러 규모 AI 인프라 프로그램과 같은 대규모 프로젝트는 백본 클라우드 캠퍼스에 현재 요구되는 규모를 보여줍니다. 블록당 500-1,250kW 등급의 모듈식 UPS 프레임은 단계적 확장을 가능하게 하며 유휴 용량을 제한합니다. 중앙 집중식 배포는 메가와트당 자본 비용을 절감하는 동시에, 고급 배터리 모니터링 기술로 주요 교체 주기 간 운영 수명을 15년으로 연장합니다. 공급업체들은 공장 통합형 전원 홀을 통해 거의 완성된 유닛으로 출하함으로써 시운전 시간을 대폭 단축합니다. 그 결과, 각 하이퍼스케일 프로젝트가 장비와 서비스 모두에 대해 대규모 다년 구매 계약을 체결함에 따라 데이터센터 UPS 시장이 즉각적인 성장세를 보이고 있습니다.

5G 밀집화와 고객 대상 분석은 컴퓨팅을 매장, 기지국, 지점으로 이동시킵니다. 엣지 사이트는 높은 주변 온도, 먼지, 최소한의 현장 인력을 견디도록 설계된 소형 UPS 장치를 요구합니다. 더 긴 작동 범위와 빠른 재충전 주기가 높은 초기 비용을 상쇄하기 때문에 리튬이온 채택이 증가합니다. 통신 사업자들은 수천 개의 엣지 캐비닛을 중앙 집중식 모니터링 포털로 통합하여 UPS 공급업체에게 정기적인 서비스 계약을 창출합니다. 수요 반응 참여는 유틸리티사가 백업 무결성을 해치지 않으면서 일시적으로 전력을 수출할 수 있는 사이트에 보상함에 따라 비즈니스 사례를 더욱 강화합니다.

라인 인터랙티브 대안은 약 1/3 저렴하여, 예산에 민감한 구매자들이 수명 주기 계산상 고효율 장치가 유리하더라도 업그레이드를 미루게 합니다. 금융 패키지와 에너지 서비스 모델이 확산되고 있지만, 조달 팀은 여전히 신중한 태도를 유지합니다. 모듈식 용량 단계적 도입은 가격 충격을 완화하지만 시장 교육이 여전히 필요합니다. 예산 지연과 노후화된 VRLA(밀폐형 납축전지) 장비의 교차 지점에서는 가동 중단 위험이 증가하지만, 단기적 재정 제약으로 인해 즉각적인 전환율은 여전히 제한됩니다.

2024년 이중변환 온라인 시스템은 미션 크리티컬 사이트에서 검증된 신뢰성을 계속 중시함에 따라 매출 기준 44.6%의 점유율로 선두를 유지했습니다. 그럼에도 핫스왑 가능한 전원 블록과 적정 규모의 초기 구축을 허용하는 모듈식/병렬 중복 프레임은 8.9% CAGR로 성장 중입니다. 고밀도 AI 시설에서 이러한 시스템은 공간 점유율을 줄이고 평균 수리 시간을 단축하여 운영자에게 실질적인 운영비 절감 효과를 제공합니다. 라인 인터랙티브 및 스탠바이 카테고리는 비용이 중복성보다 중요한 저전력 엣지 캐비닛에서 틈새 시장을 유지합니다.

데이터센터 UPS 시장은 가동 중단 없이 확장 가능한 아키텍처를 점점 더 선호하며, 공급업체들도 이에 맞춰 로드맵을 전환하고 있습니다. 슈나이더 일렉트릭의 갤럭시 VXL은 최소 설치 공간 내에서 용량을 1,250kW까지 확장하는 스택형 블록을 선보이며, 에코 모드에서 99% 효율을 제공합니다. 인력 부족으로 유지보수 일정이 압박받는 가운데, 모듈형 프레임에 내장된 자가 진단 로직은 소규모 팀으로 가동 시간을 극대화해야 하는 운영자에게 더욱 매력적입니다. 향후 병렬 구동 가능 설계는 신규 구축 및 리트로핏 주기 모두에서 기존 제품을 대체할 전망입니다.

200kVA 초과 등급 시스템은 2024년 데이터센터 UPS 시장 점유율 52.3%를 차지했으며, 2030년까지 연평균 9.3% 성장률을 기록할 것으로 예상됩니다. 수십 메가와트 규모의 하이퍼스케일 캠퍼스 및 GPU 클러스터에는 전력 분배를 간소화하고 케이블 배선을 줄이며 액체 냉각 통합을 가능하게 하는 대형 블록 유닛이 필요합니다. 후지전기(Fuji Electric)의 225-1,000kVA 시리즈처럼 동일한 330kVA 모듈을 사용해 확장성을 단순화한 제품 라인에서 해당 부문의 성장 동력이 뚜렷이 드러납니다.

중견 기업들은 여전히 20.1-200kVA 프레임에 의존하지만, 워크로드가 통합된 지역 허브로 이전되면서 시장 점유율은 축소되고 있습니다. 20kVA 미만 시스템은 통신 쉘터의 주력 제품으로 여전히 대량 출하되지만 매출 증가는 미미한 수준입니다. 고용량 리튬이온 캐비닛은 VRLA 대비 에너지 밀도를 두 배로 높여 공간 제약을 완화함으로써 컴퓨팅 랙을 위한 새로운 여유 공간을 확보하고 최상위 전력 등급에 대한 수요를 강화합니다.

북미는 성숙한 코로케이션 클러스터, 국내 제조를 위한 연방 인센티브, 예비 용량 수익화를 허용하는 FERC 명령 841과 같은 프레임워크의 지원으로 2024년 데이터 센터 UPS 시장에서 37.4%의 매출 점유율로 선두를 차지했습니다. 그러나 평균 4년 이상의 유틸리티 상호연결 대기 시간은 투자자들을 전력 접근이 더 빠른 2차 대도시권으로 이동시키고 있습니다. 슈나이더 일렉트릭을 비롯한 제조사들은 미국 내 생산 확대 및 납기 단축을 위해 7억 달러를 투자하기로 약속했으며, 이는 지정학적 위험을 상쇄하는 조치이기도 합니다.

아시아태평양 지역은 2030년까지 연평균 9.5% 성장률로 가장 빠른 성장세를 보일 전망입니다. 말레이시아, 인도네시아, 태국의 정책 지원으로 지역 전력 수요는 2024년 1분기 1,677MW에서 2028년 7,589MW로 증가할 것으로 예상됩니다. 싱가포르의 토지 및 전력 제약으로 인해 하이퍼스케일 프로젝트가 조호르와 바탐으로 전환되면서 국경 간 전력망 프로젝트가 확대되고 있습니다. 화웨이 같은 국내 공급업체들은 근접성과 정부 프로그램을 활용해 가격 및 맞춤화 경쟁력을 확보하며 수입 브랜드를 넘어선 출하량을 기록 중입니다. 한편 일본의 반도체 팹에 대한 수십억 달러 규모의 인센티브는 지진 안전 및 에너지 효율 규정을 모두 충족하는 UPS 시스템 수요를 증가시켜 기술적 차별화의 추가 요소를 더하고 있습니다.

유럽은 복합적인 전망을 보입니다. 에너지 효율 지침(EED)은 2030년까지 데이터센터 에너지 사용량을 11.7% 감축하도록 강제하며, 모든 리프레시 주기마다 최소 98% 효율 모듈로 업그레이드하도록 규정합니다. 독일의 엄격한 PUE 목표는 프리미엄급 UPS 장비 시장에 무게를 실어주는 반면, 네덜란드와 아일랜드는 전력 소모가 큰 신규 건설에 대한 모라토리엄을 검토하며 성장을 폴란드와 스페인으로 전환시키고 있습니다. 브렉시트는 데이터 주권 제약을 추가하여 영국 내 인프라 기반을 유지하게 합니다. 전반적으로 규정 준수 압박은 교체율을 높여 순 신규 용량이 더 엄격한 환경 심사를 받게 되더라도 고효율 UPS 수요를 지속시키고 있습니다.

The Data Center UPS market reached USD 4.2 billion in 2025 and is projected to climb to USD 6.8 billion by 2030, delivering a 7.05% CAGR.

The expansion is linked to hyperscale facility build-outs, artificial-intelligence (AI) power-density requirements, and lithium-ion battery economics that improve total cost of ownership. Infrastructure suppliers focus on modular designs, grid-interactive functions, and high-efficiency topologies aligned with sustainability mandates. Rack power densities expected to move toward the 500-1,000 kW range by 2026 are reshaping design rules for every new deployment. Ongoing supply-chain risks for power-electronic components and regional moratoriums on data-center utilities introduce volatility, yet large capital commitments from cloud providers sustain momentum. As a result, the Data Center UPS market is evolving from static back-up equipment toward dynamic, revenue-generating assets that stabilize grids and support AI workloads.

Massive projects such as Microsoft's USD 30 billion AI infrastructure program exemplify the scale now required for backbone cloud campuses. Modular UPS frames rated 500-1,250 kW per block allow stepwise expansion and limit stranded capacity. Centralized deployments cut capital cost per megawatt while advanced battery monitoring stretches operational life toward 15 years between major refresh cycles. Suppliers respond with factory-integrated power halls that ship as near-complete units, slashing commissioning times. The result is an immediate lift in the Data Center UPS market as each hyperscale project locks in large multi-year purchase agreements for both equipment and service.

5G densification and customer-facing analytics push compute to storefronts, cell towers, and branch offices. Edge sites demand compact UPS units built for higher ambient temperatures, dust, and minimal on-site staff. Lithium-ion adoption rises because longer operating envelopes and faster recharge cycles outweigh higher initial cost. Telecommunications operators aggregate thousands of edge cabinets into centralized monitoring portals, creating annuity service contracts for UPS vendors. Demand response participation further strengthens the business case as utilities compensate sites that can momentarily export power without compromising back-up integrity.

Line-interactive alternatives cost roughly one-third less, prompting budget-sensitive buyers to defer upgrades even when lifecycle math favors high-efficiency units. Although financing packages and energy-as-a-service models are gaining ground, procurement teams remain cautious. Modular capacity staging mitigates sticker shock, but market education is still required. Where deferred budgets intersect with aging VRLA fleets, risk of downtime increases, yet short-term financial constraints continue to cap immediate conversion rates.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Double-conversion on-line systems held 44.6% revenue leadership in 2024 as mission-critical sites continued to value time-tested reliability. Even so, modular/parallel-redundant frames are expanding at an 8.9% CAGR by allowing hot-swappable power blocks and right-sized initial deployments. In high-density AI halls, these systems occupy less white-space and cut mean-time-to-repair, giving operators tangible operating-expense savings. Line-interactive and standby categories maintain niche appeal in low-power edge cabinets where cost outweighs redundancy.

The Data Center UPS market increasingly prefers architectures that can be expanded without downtime, and suppliers have shifted roadmaps accordingly. Schneider Electric's Galaxy VXL showcases stackable blocks that push capacity to 1,250 kW within a minimal footprint, delivering 99% efficiency in eco-mode. As labor shortages pinch maintenance schedules, self-diagnostic logic embedded in modular frames further attracts operators who need to maximize uptime with smaller teams. Going forward, parallel-ready designs are expected to overtake incumbents in both new builds and retrofit cycles.

Systems rated above 200 kVA claimed 52.3% of Data Center UPS market share in 2024 and are tracking a 9.3% CAGR through 2030. Hyperscale campuses and GPU clusters clustered at tens of megawatts require large-block units that streamline electrical distribution, reduce cable runs, and enable liquid-cooling integration. Segment momentum is visible in product lines such as Fuji Electric's 225-1,000 kVA series that uses identical 330-kVA modules for simplified scaling.

Mid-market organizations continue to rely on 20.1-200 kVA frames, yet their share shrinks as workloads migrate into consolidated regional hubs. Systems below 20 kVA, often the mainstay in telco shelters, still ship in volume but register only incremental revenue. High-capacity lithium-ion cabinets mitigate space penalties by doubling energy density relative to VRLA, unlocking fresh white-space for compute racks and reinforcing demand for the top tier of power classes.

The Data Center UPS Market Report Segments the Industry Into UPS Type (Standby, Line Interactive, and More), Power Capacity(<=20 KVA, 20. 1-200 KVA and More), Architecture(centralized, Modular Scalable and More), Battery Type(Lithium-Ion, Lead-Acid and More) and Geography (North America, Europe, Asia, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led the Data Center UPS market with a 37.4% revenue share in 2024, supported by mature colocation clusters, federal incentives for domestic manufacturing, and frameworks such as FERC Order 841 that permit monetizing reserve capacity. Utility interconnection queues averaging more than four years do, however, push investors to secondary metros where power access is quicker. Manufacturers including Schneider Electric have committed USD 700 million to expand US production and reduce lead times, a move that also balances geopolitical risk.

Asia-Pacific is on track for the fastest 9.5% CAGR through 2030. Regional power demand is rising from 1,677 MW in Q1 2024 toward an expected 7,589 MW by 2028, thanks to policy support in Malaysia, Indonesia, and Thailand. Singapore's land and power constraints have redirected hyperscale pipelines to Johor and Batam, amplifying cross-border grid projects. Domestic suppliers such as Huawei leverage proximity and government programs to compete on price and customization, propelling unit shipments beyond those of imported brands. Meanwhile, Japan's multibillion-dollar incentives attached to semiconductor fabs increase demand for UPS systems that meet both seismic and energy-efficiency codes, adding an extra layer of technical differentiation.

Europe presents a mixed outlook. The Energy Efficiency Directive compels a 11.7% cut in data-center energy use by 2030, ensuring that every refresh cycle upgrades to at least 98% efficiency modules. Germany's strict PUE targets give market heft to premium-grade UPS equipment, while the Netherlands and Ireland weigh moratoriums on new power-hungry builds, redirecting growth to Poland and Spain. Brexit adds data-sovereignty constraints that keep a baseline of infrastructure inside the United Kingdom. Overall, compliance pressures elevate replacement rates, sustaining high-efficiency UPS demand even as net new capacity faces tighter environmental scrutiny.