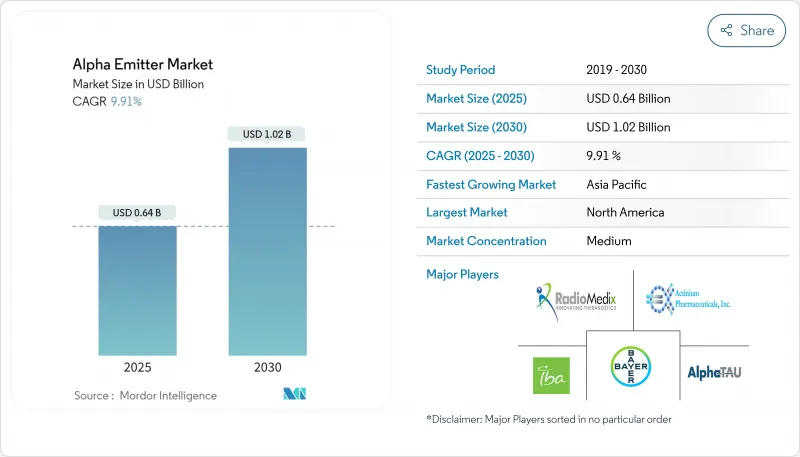

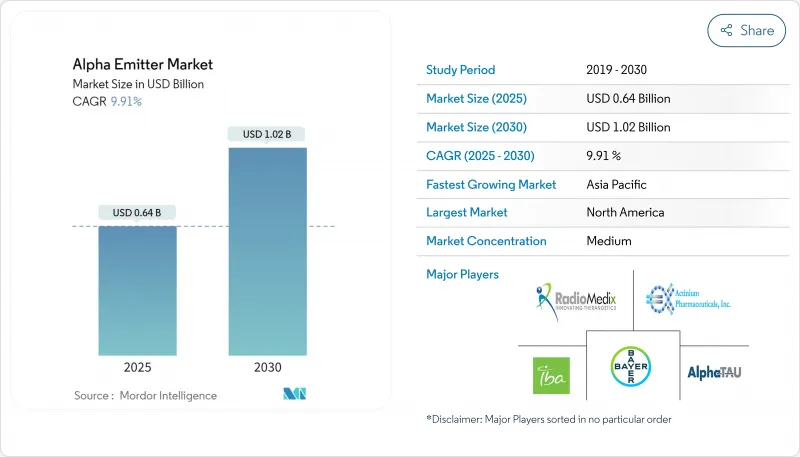

알파 방출체 시장은 2025년에 8억 3,000만 달러로 평가되었고, 2030년에 14억 4,000만 달러에 이를 것으로 예측되며, 2025-2030년의 CAGR은 11.44%를 나타낼 전망입니다.

방사성 리간드 화학의 급속한 발전, 고선형에너지전달(LET) 치료제의 임상적 수용 확대, 대형 제약사의 지속적인 투자가 시장 확장을 주도하고 있습니다. 종양학 센터들은 기존 치료에 저항하는 종양 환자에게 알파 치료를 우선적으로 적용하고 있으며, 국가 연구소가 주도하는 동위원소 생산 계획은 일부 공급 제약을 완화하고 있습니다. 동시에 진행 중인 페이로드 결합 기술 발전은 치료 적용 범위를 넓히고 정밀 전달을 가능케 하여, 종양학자들이 치료 알고리즘 초기에 알파 방출체를 도입하도록 장려하고 있습니다. 선도 기업들이 동위원소 접근권을 확보하고 후기 개발을 가속화하기 위한 인수합병을 추진함에 따라 경쟁은 여전히 치열합니다.

수술, 화학요법, 외부 방사선 치료를 회피하는 전이성 암 환자가 증가하면서 알파 방출 방사성 의약품에 대한 임상적 관심이 높아지고 있습니다. 라듐-223 임상시험 데이터는 전이성 전립선암에서 사망 위험을 30% 감소시킨 것으로 나타났습니다. 이러한 생존 이점은 종양학자들이 특히 기존 치료법이 효과적이지 않았던 골이주성 질환에 대해 알파 치료를 더 조기에 처방하도록 유도하고 있습니다. 혁신적 치료법에 대한 환자 옹호가 증가함에 따라 보험급여 관계자들이 지급 절차를 공식화하도록 촉진하여 도입을 더욱 가속화하고 있습니다. 분자 영상이 미세전이병소를 정확히 포착함에 따라, 알파 입자의 국소적 고선량율(LET)은 잔여 질환을 근절하는 효율적인 경로를 제공하여 다양한 종양 유형에 걸쳐 수요 증가의 선순환을 창출하고 있습니다.

알파 입자는 베타 방출체의 0.2 keV/μm 대비 80-100 keV/μm의 LET를 전달하며, 세포당 1-3회의 충돌로 이중 가닥 DNA 절단을 유발합니다. 이러한 강력한 효능은 인접한 건강한 조직을 보호하는 활동량에서도 효과적인 투여를 가능하게 하며, 저산소성 종양 틈새에서 저항성을 극복하는 특징을 지닙니다. 악티늄-225와 전립선 특이적 막 항원(PSMA) 리간드를 결합한 임상 프로그램은 베타 방출체 치료에서 진행된 환자에서도 지속적인 반응을 보고했습니다. 축적되는 증거는 종양 위원회가 알파 방출체를 표준 치료 경로에 통합하도록 설득하며 시장 모멘텀을 강화하고 있습니다.

연간 액티늄-225 생산량 1,700mCi는 약 2,800명의 환자 치료에 충분하지만, 임상시험 등록 예상 환자 수에는 미치지 못합니다. 아스타틴-211은 7.2시간의 반감기로 인해 즉시 합성 및 투여가 필요하므로 현장 사이클로트론 시설을 보유한 곳에서만 생산이 가능합니다. 제약사들은 할당량을 놓고 경쟁하여 연구 시작이 지연되고 상용화 일정이 길어지고 있습니다. 양성자 조사 및 광핵 접근법이 규모 확대를 약속하지만, 상용화까지는 수년이 더 소요될 전망이어서 단기 시장 성장을 제약하고 있습니다.

라듐-223은 전이성 전립선암 골 병변에 대한 2013년 규제 승인으로 2024년 알파 방출체 시장 점유율의 40.0%를 차지했습니다. 시장 친숙도, 메디케어 적용 범위, 강력한 안전성 데이터가 선도적 위치를 뒷받침합니다. 그러나 액티늄-225는 기업들이 강력한 접합체 설계에 활용하는 4중 알파 입자 붕괴 사슬 덕분에 2030년까지 연평균 14.2% 성장률로 가장 빠른 시장 점유율 증가를 기록할 전망입니다. 악티늄-225 제품의 알파 방출체 시장 규모는 고형 종양에서 적용 확대를 반영하여 2024년 1억 5,000만 달러에서 2030년까지 4억 6,000만 달러로 증가할 것으로 전망됩니다. 아스타틴-211은 100% 알파 방출과 7.2시간의 반감기를 바탕으로 신속한 배출이 필요한 외래 환자 환경에서 틈새 시장을 개척하고 있습니다. 딸핵종 재분포를 최소화하는 킬레이트 화합물 개발사들은 특히 미세 병변 치료를 위해 이 물질의 치료 지수를 확대하고 있습니다.

경쟁 구도는 본질적 효능보다 동위원소 가용성에 의해 점점 더 좌우되고 있습니다. 액티늄-225의 경우 바이엘-판테라(Bayer-PanTera)와 같은 독점 공급 계약은 후원사가 임상 시험 일정과 상용화 과정에서 영향력을 행사할 수 있게 합니다. 유럽의 PRIMSAP과 같은 학계-산업 컨소시엄은 접근성 확대를 위해 협력하고 있으나, 생산 능력은 여전히 파이프라인 진전의 속도 제한 요소로 남아 있습니다. 시장 진입자들은 차별화된 공급 확보를 위해 사이클로트론 생성 토륨 경로와 레이저 가속 방식을 모색 중이며, 이는 예측 기간 동안 경쟁 구도에 영향을 미칠 전략입니다.

북미는 선진적인 보험급여 제도와 국내 동위원소 생산을 바탕으로 2024년 알파 방출체 시장 매출의 45.0%를 차지했습니다. 오크리지 국립연구소의 연간 1Ci 액티늄-225 생산량은 현지 개발사들에게 안정적인 공급을 제공하며, 미국 식품의약국(FDA)의 방사성 의약품 지침은 승인을 간소화합니다. 노바티스와 릴리의 미국 내 제조 시설에 대한 지속적인 투자는 임상 단계에서 상업화 단계로의 확장성을 보장하며 지역적 우위를 공고히 합니다.

아시아태평양 지역은 가장 빠르게 성장하는 지역으로, 2030년까지 연평균 12.54%의 성장률을 기록할 것으로 전망됩니다. 일본과 한국은 성숙한 사이클로트론 네트워크와 숙련된 방사화학자를 활용해 다기관 알파 치료 임상시험을 수행하는 반면, 중국의 ‘건강중국 2030’ 계획은 첨단 종양학 치료법에 자금을 배정하고 있습니다. 쓰촨성의 토륨 표적 사이클로트론 라인을 포함한 동위원소 생산 현지화를 위한 정부 지원 노력은 수입 의존도를 완화하고 국내 혁신 생태계를 조성할 것으로 기대됩니다.

유럽은 방사화학 분야의 협력 연구 인프라와 인재 풀을 바탕으로 견고한 시장 점유율을 유지하고 있습니다. 유럽의약품청(EMA)의 방사성 의약품 중앙화 심사 절차와 ‘호라이즌 유럽’ 연구 기금이 결합되어 임상 적용이 가속화되고 있습니다. 그러나 회원국별 상이한 보험급여 규정이 시장 진입을 복잡하게 하여 균일한 도입 속도를 저해하고 있습니다. 이스라엘과 사우디아라비아 등 중동 국가들은 표적 알파 치료를 위한 전문 암 센터를 구축 중이며, 이 지역을 차세대 성장 거점으로 부상시키고 있습니다.

The alpha emitter market stands at USD 0.83 billion in 2025 and is projected to reach USD 1.44 billion by 2030, reflecting an 11.44% CAGR over 2025-2030.

Rapid advances in radioligand chemistry, growing clinical acceptance of high-linear-energy-transfer (LET) therapeutics, and sustained investment by large pharmaceutical companies are propelling expansion. Oncology centers are prioritizing alpha therapies for patients whose tumors resist conventional treatments, while isotope-production initiatives led by national laboratories are alleviating some supply constraints. Parallel progress in payload-binding technologies is broadening the therapeutic window and enabling precision delivery, encouraging oncologists to adopt alpha emitters earlier in treatment algorithms. Competitive activity remains intense, as leading firms pursue acquisitions that secure isotope access and accelerate late-stage development.

Growing numbers of metastatic cancers that evade surgery, chemotherapy, and external-beam radiotherapy are elevating clinical interest in alpha-emitting radiopharmaceuticals. Data from Radium-223 trials showed a 30% mortality-risk reduction in metastatic prostate cancer. This survival benefit is motivating oncologists to prescribe alpha therapies earlier, especially for bone-dominant disease where prior modalities underperformed. Rising patient advocacy for innovative options is prompting reimbursement stakeholders to formalize payment pathways, further boosting uptake. As molecular imaging pinpoints micro-metastases, the localized high LET of alpha particles offers an efficient route to eradicate residual disease, creating a virtuous cycle of demand growth across multiple tumor types.

Alpha particles deliver 80-100 keV/µm LET compared with 0.2 keV/µm for beta emitters, inflicting double-strand DNA breaks with 1-3 hits per cell. Such potency enables effective dosing at activities that spare adjacent healthy tissues, a feature that overcomes resistance in hypoxic tumor niches. Clinical programs combining actinium-225 with prostate-specific membrane antigen (PSMA) ligands reported durable responses even in patients progressing on beta-emitting counterparts. The accumulating body of evidence is persuading tumor boards to integrate alpha emitters into standard-of-care pathways, reinforcing market momentum.

Annual actinium-225 production of 1,700 mCi can treat roughly 2,800 patients, falling short of trial enrollment forecasts. Astatine-211 output is restricted to facilities with onsite cyclotrons because its 7.2-hour half-life demands immediate synthesis and administration. Pharmaceutical developers compete for allocations, delaying study starts and lengthening commercialization timelines. While proton-irradiation and photonuclear approaches promise scale, commercial deployment remains several years away, restraining near-term market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Radium-223 commanded 40.0% of alpha emitter market share in 2024 owing to its 2013 regulatory approval for metastatic prostate-cancer bone lesions. Market familiarity, Medicare coverage, and robust safety data underpin its leading position. However, actinium-225 is registering the fastest uptake, with an expected 14.2% CAGR to 2030 as firms leverage its four-alpha-particle decay chain to design potent conjugates. The alpha emitter market size for actinium-225 products is projected to rise from USD 0.15 billion in 2024 to USD 0.46 billion by 2030, reflecting widening applications in solid tumors. Astatine-211, with its 100% alpha emission and 7.2-hour half-life, is carving a niche in outpatient settings that benefit from rapid clearance. Developers of chelator chemistries that minimize daughter-nuclide redistribution are expanding its therapeutic index, particularly for microscopic disease.

Competition is increasingly shaped by isotope availability rather than inherent efficacy. Exclusive supply agreements, such as Bayer-PanTera for actinium-225, give sponsors leverage in trial timelines and commercialization. Academic-industry consortia like PRIMSAP in Europe collaborate to democratize access, yet production capacity is still the rate-limiting step for pipeline progress. Market entrants are exploring cyclotron-generated thorium routes and laser-accelerated methods to secure differentiated supply, a strategy likely to influence competitive positioning over the forecast horizon.

The Alpha Emitter Market Report is Segmented by Type of Radionuclide (Astatine-211, Radium-223, Actinium-225, Lead-212, and More), Application (Prostate Cancer, Bone Metastasis, Ovarian Cancer, Pancreatic Cancer, Endocrine Tumors, and Other Applications), End User (Hospitals, Diagnostic Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 45.0% of alpha emitter market revenue in 2024, supported by advanced reimbursement mechanisms and domestic isotope production. Oak Ridge National Laboratory's 1 Ci annual actinium-225 output provides local developers with reliable supply, while the U.S. Food and Drug Administration's radiopharmaceutical guidance streamlines approvals. Ongoing investments by Novartis and Lilly in U.S.-based manufacturing plants ensure clinical-to-commercial scalability and reinforce regional dominance.

Asia Pacific is the fastest-growing geography, forecast to post a 12.54% CAGR through 2030. Japan and South Korea leverage mature cyclotron networks and experienced radiochemists to run multicenter alpha-therapy trials, while China's Healthy China 2030 initiative earmarks funding for advanced oncology modalities. Government-backed efforts to localize isotope production-including a thorium-target cyclotron line in Sichuan-are expected to alleviate import dependence, fostering domestic innovation ecosystems.

Europe maintains a robust share via collaborative research infrastructure and talent depth in radiochemistry. The European Medicines Agency's centralized procedure for radiopharmaceuticals, combined with Horizon Europe grants, expedites clinical translation. However, fragmented reimbursement rules across member states complicate market access, slowing uniform adoption. Middle Eastern nations such as Israel and Saudi Arabia are building specialist cancer centers equipped for targeted alpha therapy, positioning the region as a secondary growth cluster.