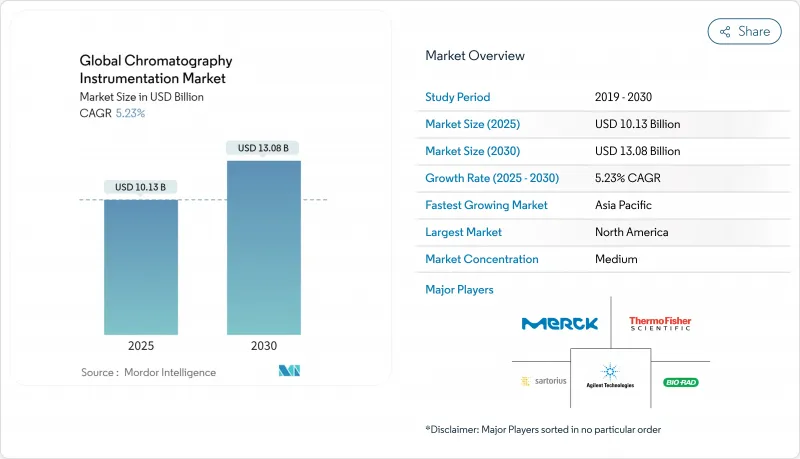

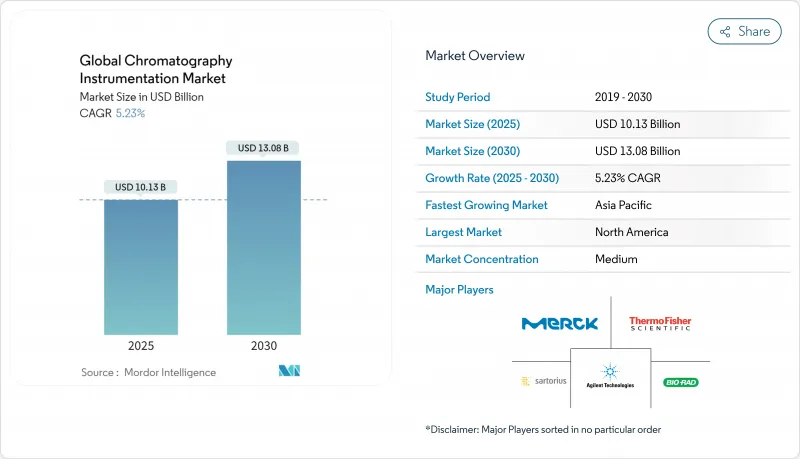

크로마토그래피 기기 시장은 2025년에 101억 3,000만 달러로 평가되었고, 2030년에 130억 8,000만 달러에 이를 것으로 예측되며, CAGR은 5.23%를 나타낼 전망입니다.

규제 감독 강화, 생물학적 제제 파이프라인 확대, 자동화 가속화로 수요가 증가하는 가운데 인공지능 기반 플랫폼은 실험실 주기 시간을 최대 40% 단축시키고 있습니다. 초고성능 시스템을 선호하는 미국 FDA의 강화된 분석 검증 지침에 힘입어 제약 및 바이오의약품 기업이 가장 큰 매출 기여도를 보이고 있습니다. PFAS 모니터링 및 식품 안전성 테스트의 병행 확장은 특히 이온 및 액체 크로마토그래피 플랫폼에 새로운 응용 분야를 추가하고 있습니다. 공급업체들은 친환경 용매 시스템, 소형화, 예측 유지보수를 지원하는 클라우드 연결 소프트웨어로 대응하고 있습니다. 핵심 컬럼 및 수지에 대한 공급망 현지화는 제조업체들이 지정학적 위험을 완화함에 따라 안정적인 장기 성장을 더욱 뒷받침합니다.

미국 FDA의 2분기(R2) 및 1분기(Q14) 업데이트된 지침은 이제 방법론의 견고성에 대한 더 강력한 증거를 요구하여 초고성능 LC-MS 플랫폼으로의 광범위한 업그레이드를 촉진하고 있습니다. 워터스의 Empower 소프트웨어는 전 세계 신약 서류의 약 80%를 이미 지원하며, 이는 품질 설계(QbD) 프로그램에서 이 기술의 핵심적 역할을 반영합니다. 항체 치료제의 금속 오염을 제거하는 생체 적합성 컬럼에 대한 수요가 특히 높습니다. 연속 생산 라인은 중요한 공정 매개변수를 사양 범위 내로 유지하기 위해 인라인 크로마토그래피 모니터링에 의존하며, 이는 계약 개발 및 제조 기관(CDMO)에 대한 계측기 판매를 강화합니다.

최신 세대의 시스템은 1,300 bar 이상의 압력을 제공하면서 자동 유지보수 절차를 실행하는 자가 진단 센서를 내장합니다. AI 엔진은 이제 실시간으로 그라디언트 프로파일을 조정하여 운영자 개입 없이 피크 용량을 향상시키고 용매 사용량을 최대 65%까지 줄입니다. 마이크로플루이딕 시료 전처리 모듈은 시약 소비를 최소화하고 처리량을 가속화하여 소규모 실험실에서도 복잡한 매트릭스를 처리할 수 있게 합니다. 장비 설치 공간은 지속적으로 축소되어 공간 제약 시설에서도 다중 설치가 가능해졌습니다. 이러한 발전은 수동 작업량을 줄여 전 세계적으로 부족한 숙련된 크로마토그래퍼 문제를 직접 해결합니다.

차세대 LC-MS 장비는 종종 50만 달러를 초과하며, 서비스 계약으로 인해 연간 추가 12%의 비용이 발생하여 학계 및 진단 실험실의 예산을 압박합니다. 반도체 관세로 인해 부품 비용이 상승할 위험이 있어 업그레이드가 지연될 수 있습니다. 제조사 및 리셀러의 인증 중고 프로그램은 1만 4,000달러라는 저렴한 진입점을 제공하지만, 제한된 보증 범위로 인해 수명 주기 위험이 증가할 수 있습니다. 복잡한 생물학적 분석 샘플당 총 분석 비용은 종종 100달러를 초과하여 일부 시설이 내부 투자 대신 외부 검사를 의뢰하도록 강요합니다.

액체 크로마토그래피 시스템은 2024년 매출의 56.8%를 차지하며 제약, 환경, 임상 분야에서 광범위한 적용성을 반영했습니다. 액체 플랫폼 크로마토그래피 장비 시장 규모는 2024년 57억 5천만 달러에 달했으며, 민감한 생체분자의 금속 흡착을 최소화하는 생체적합성 하드웨어의 부양으로 5.1% CAGR 성장할 것으로 전망됩니다. 절대 규모는 작지만 초임계 유체 장비는 제약업계의 친환경 키랄 분리 수요에 힘입어 가장 빠른 8.9% CAGR을 기록할 것입니다. 가스 크로마토그래피 제조사들은 헬륨 의존도를 낮추기 위해 수소 운반체용 시스템 재설계에 나서고 있으며, 음용수 규정 준수를 위한 이온 크로마토그래피의 중요성이 부각되고 있습니다. 소모품, 특히 PFAS 및 항체 분석용으로 설계된 컬럼은 반복적 수익을 창출하며 공급업체를 자본 지출 주기에서 보호합니다. 미국과 유럽에서 아가로즈 수지 생산 현지화는 사용자를 태평양 횡단 물류 위험으로부터 보호하여 납기 단축과 가격 안정성을 높입니다.

기술적 차별화는 이제 내장형 분석 기능에 집중됩니다. 기기는 모든 매개변수 변화를 기록하여 실험실 정보 시스템에 공급되는 추적 가능한 디지털 트윈을 생성합니다. 공급업체들은 고장 예측이 가능한 컬럼 상태 대시보드를 통합하여 데이터 무결성을 보호하고 재실험을 줄입니다. 소형 자동 시료 주입기와 용매 절약형 그라디언트 펌프는 크로마토그래피 분해능을 유지하면서 친환경 화학 규정을 준수합니다. 이러한 추세는 액체 시스템의 지속적인 리더십을 보장하며 크로마토그래피 기기 시장의 전반적인 성장 궤도를 뒷받침합니다.

북미는 2024년 글로벌 매출의 38.7%를 유지했으며, 이는 집중적인 제약 R&D 파이프라인과 고급 분석 검증을 의무화하는 엄격한 FDA 감독에 기반합니다. 써모 피셔의 20억 달러 규모 생산 능력 확장 프로그램과 같은 국내 확장 프로젝트는 장비 및 소모품 접근성을 개선하여 교체 주기와 신규 설치를 지원합니다. 반도체 국내 생산 유치를 위한 연방 인센티브는 계측기 부품 공급을 보호하여 생태계 회복탄력성을 강화합니다.

유럽은 확고한 기반을 유지하지만, 더 엄격해진 용매 및 폐기물 규제로 인해 친환경 기술의 조기 도입이 촉진되고 있습니다. 실험실들은 환경 지침 준수를 위해 저유량 UHPLC 및 수소 운반 가스 솔루션으로 전환하고 있습니다. EU 호라이즌 연구 기금은 차세대 검출 방법 개발을 지속적으로 지원하며 지역 혁신 파이프라인을 유지하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 7.8% 성장률로 주요 성장 동력을 대표합니다. 중국과 인도는 계약 연구 기관, 백신 제조사, 제네릭 의약품 제조업체의 사업 확대로 지역 수요의 절반 이상을 차지합니다. 식품 안전 검사 강화 및 산업 오염 억제를 위한 정부 정책이 추가로 주문량을 촉진합니다. 일본 및 한국 기업들은 플랫폼 엔지니어링 분야에서 선두를 유지하며, 고정밀 부품을 전 세계로 수출하고 크로마토그래피 기기 시장의 글로벌 위상을 강화하고 있습니다.

The chromatography instrumentation market is valued at USD 10.13 billion in 2025 and is forecast to reach USD 13.08 billion by 2030, advancing at a 5.23% CAGR.

Rising regulatory scrutiny, expanding biologics pipelines, and rapid automation are reinforcing demand, while artificial-intelligence-enabled platforms are cutting laboratory cycle times by as much as 40%. Pharmaceutical and biopharmaceutical companies account for the most significant revenue contribution, driven by the US FDA's more rigorous analytical validation guidelines that favor ultra-high-performance systems. Parallel expansion of PFAS monitoring and food-safety testing is adding new application breadth, especially for ion and liquid chromatography platforms. Vendors are responding with greener solvent systems, smaller footprints, and cloud-connected software that supports predictive maintenance. Supply-chain localization for critical columns and resins further supports stable long-term growth as manufacturers mitigate geopolitical risk.

Updated Q2(R2) and Q14 guidance from the US FDA now requires stronger evidence of method robustness, prompting widespread upgrades to ultra-high-performance LC-MS platforms. Waters' Empower software already supports roughly 80% of new drug dossiers worldwide, reflecting the technique's central role in quality-by-design programs. Demand is especially strong for biocompatible columns that eliminate metal contamination of antibody therapeutics. Continuous manufacturing lines rely on in-line chromatographic monitoring to keep critical process parameters within specification, reinforcing instrumentation sales to contract development and manufacturing organizations.

Latest-generation systems deliver pressures beyond 1,300 bar while embedding self-diagnostic sensors that trigger automated maintenance routines. AI engines now tune gradient profiles in real time, improving peak capacity without operator intervention and reducing solvent use by up to 65%. Microfluidic sample preparation modules minimize reagent consumption and accelerate throughput, allowing smaller labs to handle complex matrices. Instrument footprints continue to shrink, enabling multiplexed installations even in space-constrained facilities. These gains directly address the global shortage of trained chromatographers by reducing manual workload.

Next-generation LC-MS instruments often exceed USD 500,000, with service contracts adding another 12% annually, straining budgets in academia and diagnostic labs. Semiconductor tariffs risk pushing component costs higher, potentially delaying upgrades. Certified pre-owned programs from OEMs and resellers offer entry points as low as USD 14,000, yet limited warranty scope can raise lifecycle risk. Total analytical cost per complex bioanalytical sample frequently surpasses USD 100, forcing some facilities to outsource testing rather than invest internally.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Liquid chromatography systems captured 56.8% of 2024 revenue, reflecting broad applicability in pharma, environmental, and clinical arenas. The chromatography instrumentation market size for liquid platforms reached USD 5.75 billion in 2024 and is projected to advance at a 5.1% CAGR, buoyed by biocompatible hardware that minimizes metal adsorption of sensitive biomolecules. Supercritical fluid instruments, though smaller in absolute terms, will record the fastest 8.9% CAGR, riding pharmaceutical demand for greener chiral separations. Gas chromatography manufacturers are redesigning systems for hydrogen carriers to mitigate helium reliance, and ion chromatography gains relevance in drinking-water compliance. Consumables, especially columns engineered for PFAS and antibody analysis, drive recurring revenue and buffer suppliers from capital-spending cycles. Localization of agarose resin production in the US and Europe shields users from trans-Pacific logistics risk, improving lead times and pricing stability.

Technological differentiation now centers on embedded analytics. Instruments log every parameter change, creating traceable digital twins that feed laboratory information systems. Vendors integrate column health dashboards that predict failure, thereby protecting data integrity and reducing reruns. Compact autosamplers and solvent-saving gradient pumps align with green-chemistry mandates while preserving chromatographic resolution. These trends ensure sustained leadership for liquid systems, underpinning the overall trajectory of the chromatography instrumentation market.

The Chromatography Instruments Market is Segmented by Devices (Chromatography Systems {Gas, Liquid, and More}, Consumables {Columns, Syringes, and More}, Accessories {Column Accessories, Auto-Sampler Accessories, and More}), Application (Agriculture & Food Testing, Pharmaceutical Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America maintained 38.7% of global revenue in 2024, anchored by intensive pharmaceutical R&D pipelines and strict FDA oversight that mandate high-end analytical validation. Domestic expansion projects such as Thermo Fisher's USD 2 billion capacity program improve access to instruments and consumables, supporting replacement cycles and new installations. Federal incentives for semiconductor onshoring also protect instrument component supply, enhancing ecosystem resilience.

Europe follows with a well-established base but faces tighter solvent and waste regulations that drive early adoption of greener technologies. Laboratories pivot toward low-flow UHPLC and hydrogen carrier gas solutions to comply with environmental directives. EU Horizon research funds continue to seed next-generation detection methods, sustaining regional innovation pipelines.

Asia-Pacific represents the principal growth engine, expanding at a 7.8% CAGR to 2030. China and India jointly account for over half of regional demand as contract research organizations, vaccine producers, and generics manufacturers scale operations. Government initiatives to upgrade food-safety testing and curb industrial pollution further stimulate orders. Japanese and South Korean firms remain at the forefront of platform engineering, exporting high-precision components worldwide and reinforcing the global standing of the chromatography instrumentation market.