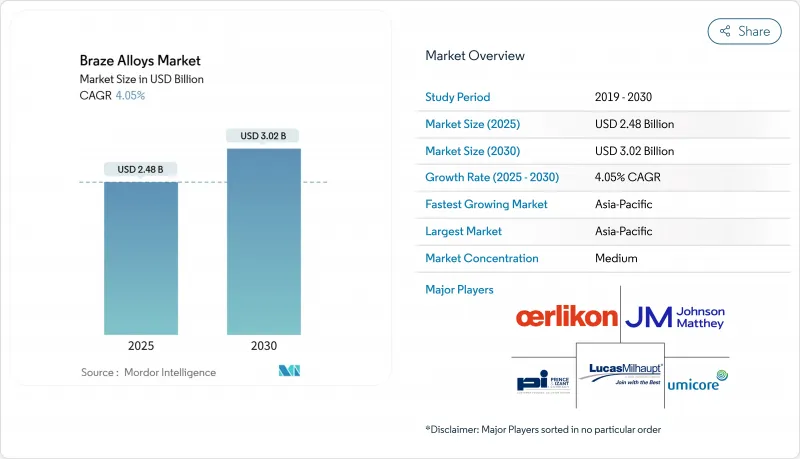

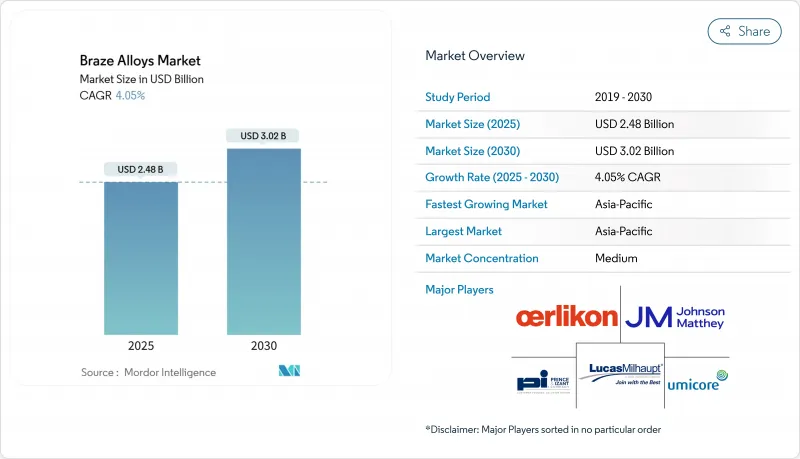

브레이징 합금 시장 규모는 2025년에 24억 8,000만 달러로 평가되었고, 2030년에 30억 2,000만 달러에 이를 것으로 예상되며 CAGR은 4.05%를 나타낼 전망입니다.

자동차 열교환기, 전기차 전력 전자기기, 첨단 항공우주 구조물에서 정밀 금속 접합 수요가 증가하며 시장이 성장세를 보이고 있습니다. 중온 공정에서 용접을 브레이징으로 꾸준히 대체함에 따라 물량이 높은 수준을 유지하는 한편, 새로운 비정질 포일 합금의 등장으로 이종 금속 조립체로의 적용 범위가 확대되고 있습니다. 중국의 2차 알루미늄 붐과 지역 전자제품 생산 능력 확장에 힘입어 아시아태평양 지역이 물량과 성장률을 주도하고 있습니다. 공급망 참여자들은 가격 중심 등급보다 고성능 제형을 선호하는 추세로, 브레이징 합금 시장 전반에 걸쳐 품질 중심 구매로 전환되고 있음을 시사합니다.

제조사들은 브레이징을 선호하는데, 이는 더 낮은 온도에서 재료를 접합하여 항공우주 및 전자 응용 분야의 정밀 공차 조립체에 중요한 모재 금속 특성을 보존하기 때문입니다. 로 브레이징(Furnace brazing)은 단일 공정으로 다중 접합을 통합하여 순차적 용접 단계를 제거하고, 인력을 절감하며, 변형을 최소화합니다. 개선된 충전재 화학 성분은 이제 용접 접합 강도와 맞먹으면서 더 높은 피로 저항성을 제공하여, 복잡한 얇은 벽 구조물에 브레이징을 최적의 공정으로 만듭니다. 자동차 부품 공급업체들은 수동 용접 수리에서 배치 브레이징으로 전환한 후 알루미늄 라디에이터 라인에서 더 짧은 택트 타임을 보고합니다. OEM 업체들이 린 제조를 추진함에 따라 이 촉진요인은 중온 범위 전반에 걸쳐 브레이징 합금 시장을 강화하고 있습니다.

전기차와 터보차저 내연기관 모두 소형 열 관리 시스템을 요구합니다. 알루미늄-실리콘 충전재는 주행 거리와 연비에 중요한 경량화 목표를 저해하지 않으면서 누출 방지 접합부를 형성합니다. A2L 냉매 도입으로 접합부 무결성 요구사항이 강화되어 충전재 사용량이 더욱 증가하고 있습니다. NOCOLOK과 같은 플럭스 기술은 제어된 분위기 용로에서 균일한 습윤을 제공하여 1차 열교환기 공장에서 연간 수백만 단위의 생산량을 지원합니다. 이러한 요인들은 알루미늄 브레이즈에 대한 단기 수요 급증으로 이어져 APAC, NAFTA, 유럽 전역의 자동차 클러스터에서 브레이즈 합금 시장을 끌어올리고 있습니다.

구리와 은은 공급 병목 현상과 인프라 수요로 인해 가격 급등락을 보입니다. 원자재 급등은 충전재 생산자의 마진을 압박하며, 이들은 금속 헤지나 고객에게 비용 전가로 대응하지만 가격 민감도가 높은 HVAC 및 백색가전 부문에서 주문 연기 위험에 직면합니다. 이러한 변동성으로 일부 제조업체는 기계적 체결 방식을 고려하게 되어 단기 사이클 동안 브레이징 합금 시장에 하방 압력을 가합니다. 균형 잡힌 조달 전략과 귀금속 함량을 낮춘 합금 재구성은 이러한 제약을 부분적으로 상쇄하지만, 노출 위험을 완전히 중화시키지는 못합니다.

구리 기반 충전재는 2024년 매출의 35.86%를 차지하며 자동차, HVAC 및 일반 산업 라인에서 광범위한 적용성을 입증했습니다. 사용자들은 구리의 열전도성, 적정 용융점 및 플럭스와의 호환성을 높이 평가하여 브레이징 합금 시장을 이 금속 계열에 고정시키고 있습니다. 은 함유 등급은 접합 저항이 중요한 프리미엄 전자 제품에 사용되며, 금 합금은 가혹한 환경에서 미세 부식 틈새 시장을 채웁니다.

니켈과 코발트를 주축으로 한 기타 비금속은 고온 안정성이 전기차 배터리 모듈 및 터빈 부품에 적합하여 2030년까지 연평균 4.71%의 가파른 성장률을 보일 전망입니다. 애리조나 주립대는 800°C에서 10,000시간 후에도 1120MPa 항복 강도를 유지하는 구리-탄탈-리튬 합금을 시연하며 고급 구리 변형체 개발 방향성을 입증했습니다. 이러한 발전은 구리의 양적 우위를 위협하지 않으면서 특수 고열 등급 브레이즈 합금 시장 규모를 확대합니다.

2024년 브레이징 합금 시장에서 로드 및 와이어 제품이 30.94%를 차지했습니다. MRO 기술자들은 토치 작업에 익숙한 이 형태를 선호하며, 소량 생산 업체들은 낮은 진입 비용을 높이 평가합니다. 분말, 페이스트, 포일 형태는 특수 전자 및 항공우주 접합부에 적용되며, 기하학적 요구사항이 있을 때 정밀한 합금 배치를 제공합니다.

링과 프리폼은 반복성을 중시하는 자동차 라디에이터 라인의 수요에 힘입어 연평균 4.97% 성장률을 기록 중입니다. 사전 성형된 반지는 공정 시간을 최대 30% 단축하고 일관된 필렛 크기를 제공하여 사후 검사 재작업을 줄입니다. 로봇 공학 통합은 자동 픽 앤 플레이스가 가능한 프리폼을 선호하여 2030년까지 브레이징 합금 시장에서 평균 이상의 성장을 유지할 전망입니다.

아시아태평양 지역은 2024년 글로벌 매출의 46.28%를 차지했으며, 5.03%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상되어 동시에 최대 규모이자 가장 빠르게 성장하는 지역이 될 것입니다. 중국의 2차 알루미늄 부문은 신에너지 차량 및 인프라 수요 증가로 연간 13% 성장하며 알루미늄 기반 충전재 수요를 끌어올리고 있습니다. 일본의 정밀 제조업체와 한국의 전자 조립업체들은 첨단 용광로 라인을 설치하며 지역 전문성을 심화시키고 있습니다. 임금 상승과 ESG 규제로 일부 생산 능력이 베트남과 태국으로 이동하기 시작했지만, 확고한 공급망으로 인해 브레이징 합금 시장의 중심은 여전히 아시아태평양 지역에 있습니다.

북미는 고성능 니켈 및 코발트 충전재를 요구하는 항공우주 엔진 및 방위 전자 프로그램에 힘입어 견고한 2위를 유지하고 있습니다. 미국의 리쇼어링 정책과 인플레이션 감축법(IRA)은 현대식 용광로 업그레이드에 자본을 집중시키고 있으며, 멕시코의 자동차 수출 증가는 알루미늄 라디에이터 소비를 가속화하고 있습니다. 숙련된 노동력 부족과 간헐적인 구리 가격 급등은 절대적 성장을 억제하지만 브레이징 합금 시장의 모멘텀을 저해하지는 않습니다.

유럽의 성숙한 산업 기반은 자동차, HVAC, 일반 엔지니어링 전반에 걸쳐 꾸준한 수요를 창출합니다. 엄격한 RoHS 및 REACH 규정은 카드뮴 프리 및 무연 변형재의 신속한 채택을 촉진합니다. 독일의 전기차 플랫폼 출시로 알루미늄-실리콘 충전재 수요가 증가하고, 영국의 항공우주 복합재 클러스터는 금속-세라믹 접합을 위한 비정질 포일로의 전환을 모색 중입니다. 순환 경제 지침은 재활용 용접재에 대한 틈새 시장을 열어주며, 해당 지역의 브레이징 합금 시장에 미묘한 성장 경로를 시사합니다.

The braze alloys market size stands at USD 2.48 billion in 2025 and is on track to reach USD 3.02 billion by 2030, reflecting a 4.05% CAGR.

The market gains strength from growing demand for precision metal joining in automotive heat exchangers, EV power electronics, and advanced aerospace structures. Steady substitution of welding by brazing in medium-temperature operations keeps volumes high, while new amorphous foil alloys widen the application window into dissimilar metal assemblies. Asia-Pacific dominates volume and growth, supported by China's secondary aluminum boom and regional electronics capacity expansions. Supply chain participants now favor high-performance formulations over price-driven grades, indicating a shift toward quality-led purchasing across the braze alloys market.

Manufacturers favor brazing because it joins materials at lower temperatures, which preserves base metal properties critical for tight-tolerance assemblies in aerospace and electronics applications. Furnace brazing consolidates multiple joints in a single cycle, eliminating sequential welding steps, cutting labor, and minimizing distortion. Improved filler chemistries now match welded joint strength while offering higher fatigue resistance, making brazing the process of choice for complex thin-wall structures. Automotive suppliers report shorter takt times in aluminum radiator lines after switching from manual weld repair to batch brazing. As OEMs push lean manufacturing, this driver strengthens the braze alloys market across medium-temperature ranges.

Electric vehicles and turbocharged combustion engines both require compact heat management systems. Aluminum-silicon fillers form leak-tight joints without compromising lightweight targets vital for range and fuel economy. Implementing A2L refrigerants has tightened joint integrity requirements, further boosting filler volumes. Flux technologies such as NOCOLOK deliver uniform wetting in controlled-atmosphere furnaces, supporting annual throughput in the millions of units at Tier-1 heat-exchanger plants. These factors translate into high short-term pull for aluminum brazes, lifting the braze alloys market in automotive clusters across APAC, NAFTA, and Europe.

Copper and silver exhibit sharp price swings due to supply bottlenecks and infrastructure demand. Cost spikes compress margins for filler producers, who hedge metals or pass costs to customers, risking order deferrals in price-sensitive HVAC and white-goods sectors. The volatility prompts some fabricators to consider mechanical fastening, placing downward pressure on the braze alloys market during short-term cycles. Balanced sourcing strategies and alloy reformulations with lower noble-metal content partially offset the restraint, yet cannot fully neutralize exposure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Copper-based fillers generated 35.86% of revenue in 2024, underscoring their broad applicability in automotive, HVAC, and general industrial lines. Users value copper's thermal conductivity, moderate melting point, and compatibility with fluxes, which keep the braze alloys market anchored in this metal class. Silver-bearing grades serve premium electronics where joint resistivity matters, and gold alloys fill micro-corrosion niches in harsh environments.

Other base metals, chiefly nickel and cobalt, will expand briskly at a 4.71% CAGR to 2030 as their high-temperature stability suits EV battery modules and turbine components. Arizona State University demonstrated a copper-tantalum-lithium alloy sustaining 1120 MPa yield strength after 10,000 hours at 800 °C, validating the trajectory toward advanced copper variants. These developments enlarge the braze alloys market size for specialty high-heat grades without eclipsing copper's volume leadership.

Rod and wire products accounted for 30.94% of the braze alloys market in 2024. MRO technicians rely on these familiar forms for torch work, and small batch fabricators appreciate their low entry cost. Powder, paste, and foil formats address niche electronics and aerospace joints, offering precise alloy placement when geometry demands.

Rings and preforms are advancing at a 4.97% CAGR, propelled by automotive radiator lines that value repeatability. Pre-shaped rings cut cycle time by up to 30% and deliver consistent fillet size, which reduces post-inspection rework. Robotics integration favors preforms that can be picked and placed automatically, sustaining above-average growth in the braze alloys market through 2030.

The Braze Alloys Market Report Segments the Industry by Base Metal (Copper, Silver, and More), Filler Form (Powder, Paste, and More), Temperature Range (Low-Temperature, Medium-Temperature, and More), End-User Industry (Automotive, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific generated 46.28% of global revenue in 2024 and is forecast to grow at 5.03% CAGR, making it the largest and fastest region simultaneously. China's secondary aluminum segment is expanding 13% per year, driven by new energy vehicles and infrastructure, which elevates demand for aluminum-based fillers. Japanese precision manufacturers and Korean electronics assemblers install advanced furnace lines, deepening regional expertise. Rising wages and ESG regulations are starting to nudge some capacity toward Vietnam and Thailand, but entrenched supply chains keep APAC at the center of the braze alloys market.

North America holds a solid second tier, propelled by aerospace engine and defense electronics programs that specify high-performance nickel and cobalt fillers. US reshoring policies and the Inflation Reduction Act funnel capital into modern furnace upgrades, while Mexico's auto exports accelerate aluminum radiator consumption. Skilled labor shortages and intermittent copper price spikes temper absolute growth but do not derail the braze alloys market momentum.

Europe's mature industrial base delivers steady demand across automotive, HVAC, and general engineering. Strict RoHS and REACH requirements push quick adoption of cadmium-free and lead-free variants. Germany's EV platform rollout stimulates aluminum-silicon filler volumes, and the UK's aerospace composites cluster turns to amorphous foils for metal-ceramic joints. Circular-economy directives open niches for recycled filler metals, signaling a nuanced growth path for the braze alloys market in the region.