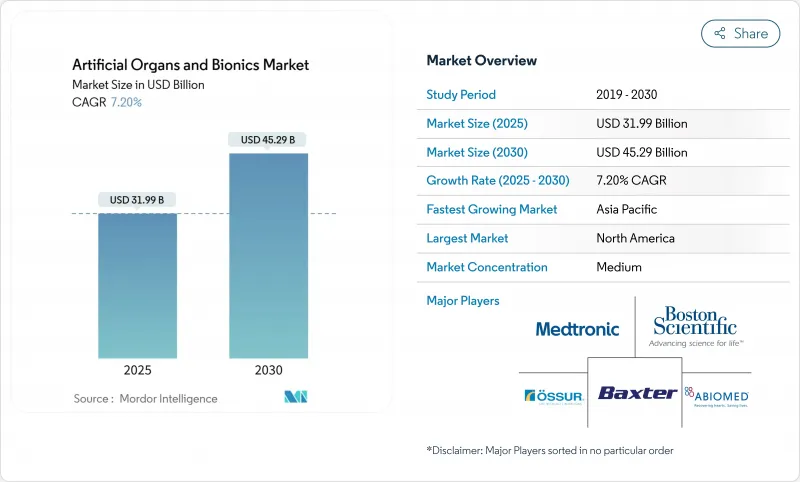

인공 장기 및 바이오닉스 시장은 2025년에 319억 9,000만 달러 규모에 이르고, 2030년에는 452억 9,000만 달러에 달할 것으로 예상되며, CAGR 7.20%를 나타낼 전망입니다.

시장 규모의 확대는 생체 재료, 소형화 전자, 3D 바이오프린팅의 획기적인 기술 혁신에 의해 형성되고 있으며, 이들 모두가 개발 기간을 단축하고, 심장혈관, 신장, 신경 보철 장치의 임상 채용을 촉진합니다. 이식 대기자 수 증가와 규제 프로그램의 신속화에 의해 전체 인공 심장, 장착형 인공 신장, 차세대 브레인 컴퓨터 인터페이스에 대한 투자에 박차가 걸리고 있습니다. 국방부가 자금을 제공하는 사지 회복 프로그램에 의해 신경 인터페이스의 노하우가 소비자용 솔루션에 흘러 들어가 보험사가 재택 바이오닉 요법을 서서히 받아들이고 있는 것으로, 치료 대상자가 확대되고 있습니다. 희토류 센서와 하이 엔드 칩을 둘러싼 공급망의 취약점은 여전히 주목점이지만, 아시아태평양의 제조 거점이 확대됨에 따라 이러한 위험은 일부 완화되고 있습니다.

퇴행성 질환은 심장 보조 장치, 인공 신장, 신경 보철의 대응 가능한 수영장을 팽창시킵니다. 심혈관계 질환은 EU에서 4,900만 명을 앓고 있으며, 기계적 순환 보조 시스템 수요를 활성화하고 있습니다. 일본의 인슐린 생산 iPS 세포 임상시험은 13만 9,000명의 1형 당뇨병 환자를 대상으로 하는 바이오인공 췌장의 기운을 부각하고 있습니다. 고령화에 의해 뇌졸중에 의한 운동장애가 증가하여 커뮤니케이션과 운동능력을 회복시키는 브레인컴퓨터 인터페이스의 무대가 정돈됩니다. 미국 퇴역군인성은 2025년도에 25개의 의지장비 관련 프로젝트를 지원하고 있으며, 장기적인 수요가 지속될 것임을 보여줍니다.

10만 3,000명 이상의 미국인이 이식을 기다리고 있습니다. 일본에서는 장기부전환자의 3% 미만만 뇌사장기 제공을 받고 있기 때문에 대체 장기에 대한 수요가 높아지고 있습니다. 2025년에 FDA가 승인한 돼지 장기의 임상시험은 이종 이식으로의 전환을 상징합니다. 카르마트 에이슨 인공 심장과 같은 브리지 투 트랜스플란트 장치는 유럽의 30명의 환자를 평균 156일 동안 살려줍니다. 중국의 45g의 소아용 인공 심장은 소아의 심장 지원에 대한 절실한 요구에 부응합니다.

로봇 무릎은 5만 1,000달러에 달할 수 있으며, 민간 보험 회사는 종종 인공 관절 환불에 상한선을 두고 있기 때문에 환자는 6자리 자기 부담액에 노출됩니다. 콜로라도 주 메디케어 패리티 법은 보험 적용 의무에 대한 진전의 편차를 보여줍니다. 수술과 후속 조치를 포함한 인공 심장 치료의 총액은 1인당 USD 50만 달러를 초과 할 수 있으므로 도입은 의료 자원의 풍부한 센터로 제한됩니다. 비용의 벽은 상환율이 장비 가격보다 늦어진 신흥 시장에서 더욱 날카로워지고 있습니다.

2024년 인공 장기 및 바이오닉스 시장의 70.26%를 인공장기가 차지했습니다. 이식 부족이 보조 인공 심장과 신흥 바이오 인공 신장 수요를 지원하기 때문입니다. 바이오닉스는 2030년까지의 CAGR이 8.25%를 나타낼 것으로 예측되고 있는데, 이는 소형화된 브레인 컴퓨터 인터페이스가 음성과 미세한 운동 제어를 용이하게 하기 때문입니다. 심장 기구의 인공 장기 및 바이오닉스 시장 규모는 티타늄으로 만들어진 전체 인공 심장의 FDA 획기적인 태그에 의해 지원되며 CAGR 7.8%를 나타낼 것으로 예측됩니다.

Roivios는 브레이크 스루 지정을 취득하고 미국에서 주요 임상시험을 준비하는 신장 보조 시스템에 임상적인 기세를 볼 수 있습니다. 바이오프린트된 간 구조와 유전자 편집된 돼지 간은 초기 단계 연구를 진행하고 있으며 파이프라인의 두께를 보여줍니다. 신경 생물학의 성장은 사용자의 의도에 몇 밀리 초에 적응하는 AI 주도 제어 알고리즘에 의해 증폭됩니다. 이러한 혁신은 인공 장기 및 바이오닉스 시장의 장기 수익 전망을 지원합니다.

북미는 확립된 FDA의 패스트트랙 프레임워크와 견조한 벤처 자금을 배경으로 2024년 인공 장기 및 바이오닉스 시장에서 38.82%의 점유율을 유지했습니다. 2024년 미국에서 공개된 투자 기회는 20억 달러를 넘었고, 그 절반은 심장과 신경 보철 신흥 기업에 투자되었습니다. 이 지역은 상환 인프라가 성숙하고 있기 때문에 조기 도입이 계속 유리하지만, 지불자가 비용 효과를 음미하기 때문에 가격에 대한 감도가 높아지고 있습니다.

아시아태평양은 CAGR 10.62%로 가장 급성장하고 있는 지역이며, 그 견인역이 된 것은 모든 혈액형에 있어서 2년간의 보존 가능 기간을 유지하는 일본의 만능 인공 혈액입니다. 중국의 트리플 통합 뇌척추 인터페이스는 하반신 불수한 환자가 몇 주 만에 지상 보행을 되찾을 수있게 해주며 국내 기업을 신경 보철의 최첨단에 위치시켰습니다. 45g의 소아용 인공 심장은 중요한 틈새 시장을 충족하고 지역의 임상 리더십을 강화했습니다.

유럽은 이식에 대한 교량요법으로 CE마크를 취득한 인공심장 Aeson을 개발한 Carmat사 등을 통해 기술면에서 리더십을 유지하고 있습니다. 독일의 이식 센터에서는 최초의 완전 이식형 인공 심장의 재택 의료 환경에의 퇴원이 보고되어, 실임상에서의 검증의 폭이 넓어졌습니다. 장기 보존 관류 시스템의 병행적인 노력으로 기증자 장기의 수급 격차는 더욱 밀접해지고, 유럽은 인공 장기 및 바이오닉스 시장의 높은 혁신 사분면 안에 확고하게 들어갔습니다.

The artificial organs and bionics market is worth USD 31.99 billion in 2025 and is forecast to reach USD 45.29 billion in 2030, advancing at a 7.20% CAGR.

Size expansion is being shaped by converging breakthroughs in biomaterials, miniaturized electronics, and 3-D bioprinting, all of which compress development timelines and lift clinical adoption of cardiovascular, renal, and neuro-prosthetic devices. Stretched transplant waiting lists and fast-track regulatory programs are spurring investment in total artificial hearts, wearable artificial kidneys, and next-generation brain-computer interfaces. Defense-funded limb-restoration programs have unlocked neural-interface know-how that is flowing into civilian solutions, while insurers' gradual acceptance of home-based bionic therapies broadens the treated population. Supply-chain fragilities surrounding rare-earth sensors and high-end chips remain a watchpoint, yet growing regional manufacturing footprints in Asia-Pacific are easing part of that exposure.

Degenerative ailments are swelling the addressable pool for cardiac assist devices, renal replacements, and neuro-prosthetics. Cardiovascular disease affects 49 million people in the EU, energising demand for mechanical circulatory support systems. Japan's insulin-producing iPS-cell trials underscore momentum behind a bioartificial pancreas for 139,000 local type 1 diabetes patients. Ageing populations translate into rising stroke-related motor deficits, setting the stage for brain-computer interfaces that restore communication and mobility. The U.S. Department of Veterans Affairs is backing 25 prosthetics-oriented projects in FY 2025, signalling continuing long-term demand.

More than 103,000 Americans wait for transplants; in Japan, fewer than 3% of organ-failure patients receive brain-dead donations, reinforcing demand for alternatives. FDA-sanctioned pig-organ trials in 2025 are emblematic of the shift toward xenotransplantation. Bridge-to-transplant devices such as the Carmat Aeson artificial heart have kept 30 European patients alive for an average of 156 days. China's 45-gram pediatric artificial heart answers an acute need in children's cardiac support.

Robotic knees can reach USD 51,000, and private insurers often cap prosthetic reimbursement, leaving patients exposed to six-figure out-of-pocket bills. Colorado's Medicare-parity law illustrates patchy progress on coverage mandates. Total artificial heart therapy, including surgery and follow-up, can surpass USD 500,000 per person, restricting uptake to high-resource centers. The cost barrier is sharper in emerging markets, where reimbursement rates lag device prices.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Artificial organs commanded 70.26% of the artificial organs and bionics market in 2024 as transplant shortages sustained demand for ventricular assist devices and emerging bioartificial kidneys. Bionics is tracking an 8.25% CAGR to 2030, aided by miniaturised brain-computer interfaces that now facilitate speech and fine-motor control. The artificial organs and bionics market size for heart devices alone is projected to expand at 7.8% CAGR, supported by FDA breakthrough tags for titanium total artificial hearts.

Clinical momentum is evident in renal assist systems where Roivios obtained breakthrough designation and is preparing U.S. pivotal trials. Bio-printed liver constructs and gene-edited pig livers are progressing through early-phase studies, signalling pipeline depth. Neuro-bionics growth is amplified by AI-driven control algorithms that adapt in milliseconds to user intent. Collectively, these innovations anchor long-term revenue visibility across the artificial organs and bionics market.

The Artificial Organs and Bionics Market Report is Segmented by Device Type (Artificial Organs [Artificial Heart, Artificial Kidney, and More] and Bionics [Vision Bionics, Ear Bionics, and More]), Technology (Implantable Devices and Wearable Devices), End User (Hospitals & Surgical Centres, Home-Care and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.82% share of the artificial organs and bionics market in 2024 on the back of an established FDA fast-track framework and robust venture funding. Investors topped USD 2 billion in disclosed U.S. deals during 2024, half of which went to cardiac and neuro-prosthesis start-ups. The region's mature reimbursement infrastructure continues to favour early adoption, yet price sensitivity is rising as payers scrutinise cost-effectiveness.

Asia-Pacific is the fastest-growing region with a 10.62% CAGR, catalysed by Japan's universal artificial blood that maintains two-year shelf life across all blood types. China's triple-integrated brain-spine interface enabled paraplegic patients to regain over-ground walking within weeks, positioning domestic players at the cutting edge of neuro-prosthetics. Pediatric device innovation is also notable: a 45-gram artificial heart designed for small children filled a vital niche, reinforcing regional clinical leadership.

Europe sustains a technology leadership role through companies such as Carmat, whose Aeson artificial heart received CE marking as a bridge-to-transplant therapy. German transplant centres reported the first fully implantable artificial-heart discharge to home care, broadening real-world validation. Parallel initiatives in organ-preservation perfusion systems further tighten the supply-demand gap for donor organs, keeping Europe firmly inside the high-innovation quadrant of the artificial organs and bionics market.