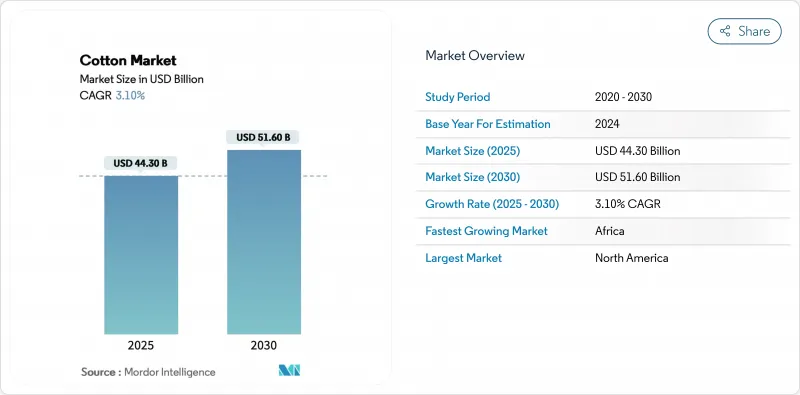

면시장 규모는 2025년 443억 달러로 평가되었고, 예측기간 중 CAGR은 3.1%를 나타낼 전망이며, 2030년에 516억 달러에 달할것으로 예측됩니다.

지속가능성 요구사항이 지속적으로 강화되면서 재배자들은 수익성을 보호하면서도 자원 사용량을 줄이기 위해 위성 유도 종자 배치부터 센서 기반 관개 일정 관리에 이르는 정밀 농업 도구를 도입하고 있습니다. 특히 위구르 강제 노동 방지법과 같은 추적성 규제의 부상은 글로벌 조달 지도를 재편하고 유통업체들을 종단간 디지털 가시성 확보로 이끌고 있습니다. 동시에, 대량 시장 의류 소매업체들 사이에서 BCI(Better Cotton Initiative) 인증이 기본 조달 요건으로 자리잡으며, 규정을 준수하는 생산자들에게 협상력이 기울어지고 있습니다. 셀룰로오스 섬유의 경쟁 압력은 여전히 구조적 역풍으로 작용하지만, 기후 스마트 관개 시스템 업그레이드와 AI 기반 수확량 예측 시스템은 선진국 농가의 마진 회복력을 향상시키고 있습니다.

방글라데시는 2025년까지 세계 최대 린트 수입국이 될 전망이며, 수직 통합 방적 공장이 프리미엄 원사 계약을 충족하기 위해 균일한 섬유 길이와 강도를 추구함에 따라 수입량이 800만 베일에 달할 것으로 예상됩니다. 소수의 아시아 제조 클러스터에 집중된 수요는 베일 단위 데이터로 섬유 특성을 인증할 수 있는 재배자들에게 안정적인 가격 프리미엄을 보장합니다. 관세 불확실성에도 불구하고 베트남은 경쟁력 있는 노동 비용과 성숙한 항만 물류를 활용해 정책 리스크를 상쇄하며 주요 수입처 지위를 유지하고 있습니다. 서아프리카산 린트는 높은 마이크로네어 값과 아프리카 상인들이 원산지에서 농약 잔류물 기준 준수를 보장할 수 있다는 점에 힘입어 방글라데시 소비량의 점유율을 확대 중이며, 2022-23 회계연도에는 39%를 차지했습니다. 이러한 구매 패턴은 역사적으로 미국에서 동아시아로 이어지던 무역 흐름을 다각화하여 방적공장과 상인 모두의 운송 위험을 줄이는 데 기여합니다.

현재 22개국 213만 명 이상의 농민이 BCI 프로토콜 하에서 운영되며, 이 프로그램은 농업 분야에서 가장 큰 독립 검증 지속가능성 체계로 자리매김했습니다. 글로벌 소매업체들은 최근 보고 주기 동안 BCI 동등 면화 구매량을 40% 증가시켜, 자발적 약속으로 시작된 것을 공급업체 계약의 필수 항목으로 전환했습니다. 이 기준은 물 사용량과 농약 사용량 감소 외에도 성별 포용성 지표와 같은 사회적 안전장치를 포함하여 인도와 파키스탄의 소규모 농가에 추가 개발 자금을 지원합니다. 대량 균형 관리 체인 모델은 인증 면화와 일반 면화를 혼합하면서도 거래 비용을 낮게 유지할 수 있게 하여 소매업체의 도입을 가속화합니다. H&M, 타겟, 인디텍스 등 기업들의 2030년까지 인증된 지속가능 프로그램에서 100% 면화 조달 발표는 규정을 준수하는 면화 가공업체 및 상인들에게 지속적인 수요 가시성을 보장합니다.

연구에 따르면 인도의 핑크볼웜 개체군이 이중 독소 Bt 품종에 대한 다유전자 저항성을 발달시켜 현장 수준 효능을 저하시키고 살충제 사용을 증가시키고 있습니다. 중국에서는 Cry1Ac에 대한 내성 대립유전자 빈도가 증가하여 규제 당국이 구조화된 피난처와 대체 유전자 스태킹을 의무화하도록 촉발했습니다. 실험실 분석 결과 키틴 합성 경로에서 레트로트랜스포존 유발 돌연변이가 확인되었으며, 일부 균주에서는 Vip3Aa 독소에 대해 5,000배 이상의 내성을 나타냈습니다. 과학자들은 선택 압력을 완화하기 위해 비(非)Bt 종자 25% 혼합 종자 사용을 권장하며, 현재 구자라트 전역에서 공공-민간 협력 확장을 통해 시범 운영 중입니다. 생명공학 기업들은 RNA 간섭 구조체와 CRISPR 기반 편집 기술을 통해 해충 장내 효소 합성을 억제하는 실험을 진행 중이지만, 상용화까지는 최소 5개 작기 이상 소요될 전망이어서 당분간 재배자들은 통합 해충 관리(IPM) 프로토콜에 의존해야 합니다.

면 시장 보고서는 지역별(북미, 유럽, 아시아태평양, 남미, 중동, 아프리카)으로 분할되어 있습니다. 생산 분석(수량), 소비 분석(금액 및 수량), 수출 분석(금액 및 수량), 수입 분석(금액 및 수량), 가격 동향 분석 등 시장 예측은 금액(달러)과 수량(메트릭톤)으로 제공됩니다.

북미는 2024년 글로벌 면화 가치의 38.9%를 차지하며 전 세계 최대 지역 점유율을 기록합니다. 이 지역의 우위는 정밀 파종 장비, 센서 기반 관개 시스템, 수확부터 수출 선적까지 리드 타임을 단축하는 완전 디지털화된 등급 분류 사무소에 기반합니다. 기술적 깊이는 일관된 섬유 품질을 뒷받침하여 방적공장이 가동 중단 시간을 최소화하고 더 엄격한 허용 오차 사양을 충족할 수 있게 합니다. 영구적인 베일 ID와 같은 첨단 추적 체계는 강제 노동 규정 준수를 개선하여, 강화된 감시를 받는 브랜드에게 북미산 린트를 저위험 선택지로 포지셔닝합니다.

아프리카의 5.60% CAGR 전망은 대륙의 광범위한 농업 현대화 흐름을 반영합니다. 종자, 비료, 해충 방제 투입물을 지원하는 정부 보조금 프로그램은 우대 금리 면화 가공업체 자금 지원과 연계되어 소규모 농가가 주요 곡물 외 재배 면적을 확대하도록 장려합니다. IMF 현장 보고서는 베냉의 특별경제구역이 지역 방적 프로젝트 촉매 역할을 했다고 평가하며, 이는 국내 가치 창출을 확대하고 재배자들이 원면 가격 변동으로부터 보호받는 전환점입니다. 이집트는 장섬유 면화 수출을 계속 우선시하지만, 물 부족으로 정책 입안자들은 면화와 식량 작물 생산 간 균형을 맞추어야 합니다. 이에 따라 수확량 잠재력을 보호하기 위해 고효율 점적 관개 시스템과 내염성 품종 도입이 촉진되고 있습니다. 서아프리카산 면화가 방글라데시에서 더 많은 구매량을 확보함에 따라, 상인들은 판매 포트폴리오를 다각화하여 단일 구매자 집중 위험에 대한 노출을 줄이고 있습니다.

아시아태평양은 여전히 세계 생산량의 상당 부분을 차지하지만, 구조적 장애물로 성장 속도가 둔화되고 있습니다. 인도의 해충 저항성 악화 사이클은 연구 기관들을 복합형질 종자 개발과 의무적 피난처 준수 방향으로 이끌고 있으며, 파키스탄의 기후 스마트 시범 농지는 미터 단위 관개 일정과 통합 영양소 관리로 더 나은 수익을 기록하고 있습니다. 호주는 IoT 기반 적정 관개 전략 도입으로 물 배분 제한 속에서도 면화 수확량을 유지하며 동아시아 시장 수출 안정성을 지속하고 있습니다. 중국은 여전히 독특한 사례로, 국내 소비가 수확량의 대부분을 흡수하며 정책 입안자들은 수입 할당량 제도를 통해 섬유 산업 내 가격 안정성을 관리합니다. 반면 방글라데시는 생산국보다 최대 수입국으로서의 역할이 부각되며, 이는 면화 시장이 수직적으로 전문화된 경제 구조로 재편되고 있음을 시사합니다.

The Cotton Market size is estimated at USD 44.30 billion in 2025 and is projected to reach USD 51.60 billion by 2030, at a CAGR of 3.1% during the forecast period.

Ongoing sustainability mandates are encouraging growers to adopt precision agriculture tools, from satellite-guided seed placement to sensor-driven irrigation scheduling, to protect profitability while lowering resource footprints. The rise of traceability regulations, especially the Uyghur Forced Labor Prevention Act, is reshaping global sourcing maps and pushing merchants toward end-to-end digital visibility. Simultaneously, Better Cotton Initiative (BCI) certification is becoming a default procurement requirement among mass-market apparel retailers, shifting bargaining power toward compliant producers. Competitive pressure from cellulosic fibers remains a structural headwind, yet climate-smart irrigation upgrades and AI-enabled yield-forecasting systems are improving margin resilience for growers in developed economies.

Bangladesh is poised to become the world's largest lint importer by 2025, with inbound volumes projected to touch 8 million bales as vertically integrated mills seek uniform fiber length and strength to meet premium yarn contracts. This concentration of demand in a handful of Asian manufacturing clusters supports stable price premiums for growers able to certify fiber characteristics with bale-level data. Vietnam remains a top destination despite tariff uncertainties, leveraging competitive labor costs and mature port logistics to offset policy risks. West African lint now satisfies a growing share of Bangladeshi consumption, 39% in fiscal 2022-23, driven by its high micronaire values and the ability of African merchants to guarantee pesticide-residue compliance at origin. These purchasing patterns help diversify global trade flows away from historical US-to-East-Asia corridors, reducing freight risk for mills and merchants alike.

More than 2.13 million farmers across 22 countries now operate under BCI protocols, making the program agriculture's largest independently verified sustainability scheme. Global retailers increased purchases of BCI-equivalent lint by 40% over the latest reporting cycle, turning what began as a voluntary commitment into a non-negotiable line item in supplier contracts. Beyond lower water and pesticide footprints, the standard embeds social safeguards such as gender-inclusion metrics, unlocking incremental development funding for smallholders in India and Pakistan. The mass-balance chain-of-custody model lets traders blend certified and conventional cotton while keeping transaction costs low, a feature that accelerates retailer adoption. Corporate announcements from H&M, Target, and Inditex to source 100% of cotton from verified sustainable programs by 2030 ensure durable forward-demand visibility for compliant ginners and merchants.

Research confirms that pink bollworm populations in India have developed multigenic resistance to dual-toxin Bt varieties, reducing field-level efficacy and driving up insecticide use. In China, resistance allele frequencies to Cry1Ac are rising, prompting regulators to mandate structured refuges and alternative gene stacking. Laboratory assays show retrotransposon-induced mutations in chitin synthase pathways, producing more than 5,000-fold resistance to Vip3Aa toxins in some strains. Scientists advocate seed mixtures containing 25% non-Bt seed to slow selection pressure, a practice now piloted across Gujarat under public-private extension programs. Biotechnology firms are experimenting with RNA-interference constructs and CRISPR-enabled edits that silence pest gut-enzyme synthesis, but commercial deployment remains at least five seasons away, leaving growers dependent on integrated pest-management protocols in the interim.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The Cotton Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America accounts for 38.9% of global cotton value in 2024, the largest regional share worldwide. The region's dominance rests on precision-planting equipment, sensor-driven irrigation, and fully digitized classing offices that compress lead times from harvest to export vessel. Technology depth supports consistent fiber quality, enabling mills to minimize downtime and meet tighter tolerance specifications. Advanced traceability schemes such as permanent bale IDs improve compliance with forced-labor regulations, positioning North American lint as a low-risk choice for brands facing heightened scrutiny.

Africa's 5.60% CAGR projection embodies the continent's broader agricultural modernization narrative. Government subsidy programs covering seed, fertilizer, and insect-control inputs are paired with concessional-rate ginner financing, encouraging smallholders to expand acreage beyond staple grains. IMF field reports credit Benin's Special Economic Zone with catalyzing local yarn-spinning projects, a shift that captures more value domestically and hedges growers against raw-lint-price swings. Egypt continues to prioritize long-staple exports, but water constraints force policymakers to balance cotton with food-crop imperatives, prompting the adoption of high-efficiency drip networks and salt-tolerant cultivars to safeguard yield potential. As West African lint secures higher offtake in Bangladesh, merchants diversify sales portfolios, reducing exposure to single-buyer concentration risks.

Asia-Pacific still accounts for a substantial share of global output, yet structural hurdles temper its growth velocity. India's escalating pest-resistance cycle pushes research institutes toward stacked-trait seeds and mandatory refuge compliance, while Pakistan's climate-smart pilot plots record better returns driven by meter-level irrigation scheduling and integrated nutrient management. Australia's adoption of IoT-enabled deficit-irrigation strategies maintains lint yields despite tightening water allocations, sustaining export reliability into East-Asian markets. China remains a unique case: domestic consumption absorbs most of its harvest, and policymakers apply import-quota levers to manage price stability inside the textile sector. In contrast, Bangladesh's role as a top importer rather than a producer underscores the cotton market's realignment toward vertically specialized economies.