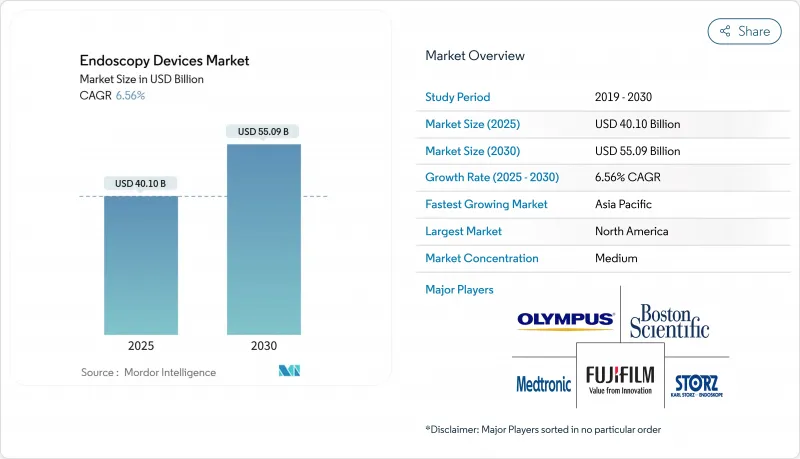

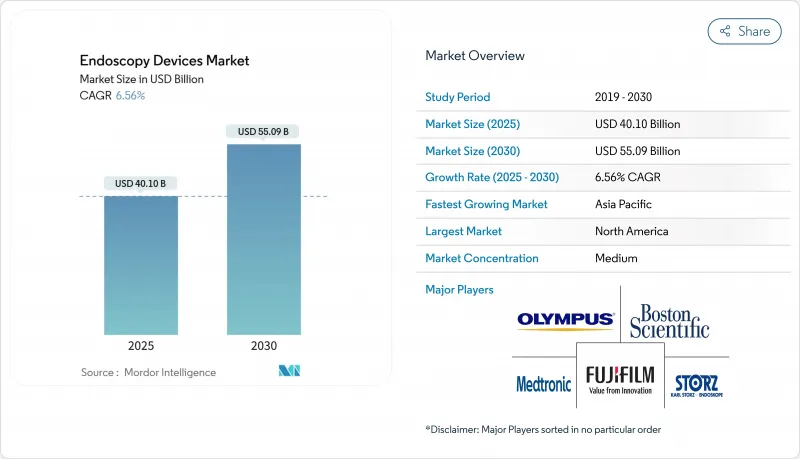

내시경 기기 시장은 2025년에 401억 달러로 평가되었고, 2030년에 약 550억 9,000만 달러에 이를 것으로 예상되며, CAGR은 6.56%를 나타낼 전망입니다.

최소 침습 수술의 확산은 병원 자본 예산을 지속적으로 재편하며, 환자의 회복 기간을 단축하고 수술실 공간을 고수익 수술에 할당할 수 있게 하는 시각화 타워 및 첨단 영상 모듈에 투자를 유도하고 있습니다. 동시에 감염 관리 의무화로 인해 일회용 또는 부분 일회용 내시경으로 조달 방향이 전환되고 있으며, 이는 재처리 노동력을 줄일 뿐만 아니라 병원 감염 관련 보상 감액도 제한합니다. 아시아태평양 지역의 성장은 보험 적용 범위 확대와 숙련된 내시경 전문의 부족이 맞물리면서 글로벌 평균을 앞지르고 있으며, 이로 인해 해당 지역 구매자들은 학습 곡선을 단축시키는 직관적인 소프트웨어 기반 플랫폼을 선호하게 되었습니다. 북미의 기존 공급업체들은 여전히 핵심 고객이지만, 일회용 십이지장내시경의 빠른 채택으로 인해 제조사들은 프리미엄 가격과 물량 기반 비용 효율성 사이의 균형을 맞추도록 압박받고 있습니다.

전문 분야를 막론하고 임상의들은 최소 침습적 중재를 중심으로 치료 경로를 재구성하고 있습니다. 자연 구멍을 통한 내시경적 로봇 수술은 제품 로드맵이 동일한 가치 제안(환자 외상 감소, 입원 기간 단축, 빠른 회복)으로 수렴하는 방식을 보여줍니다. 두 번째 차원의 함의는 병원들이 이제 영상실 및 수술실 리모델링에 대한 자본 예산 요청을 이러한 기술로 인한 처리량 증가 주장과 연계한다는 점입니다. 따라서 내시경 공급업체들은 이미지 품질뿐만 아니라 측정 가능한 워크플로우 효율성 측면에서도 점점 더 경쟁해야 합니다.

고해상도 광학 기술, 3D 영상, 소프트웨어 강화 대비 플랫폼은 초기 병변 검출을 개선했습니다. 예를 들어 올림푸스의 EVIS EXERA III는 좁은 대역 영상(NBI)과 듀얼 포커스 기술을 활용해 대장내시경 검사 중 선종 발견률을 높입니다. 의료 제공자에게 이는 더 작은 조직 부피를 선택적으로 생검할 수 있는 신기술로 이어지며, 이는 병리 검사 결과를 신속하게 제공할 뿐만 아니라 대규모로 소모품 비용을 절감합니다. 이러한 최적화는 외래 시설이 품질 기준을 충족하면서도 경쟁력 있는 보험 급여율을 유지할 수 있게 합니다.

적응증 확대 속도가 숙련된 내시경 전문의의 글로벌 공급량을 앞질렀습니다. 미국 위장관 내시경 학회(ASGE)는 ERCP 및 EUS와 같은 고급 시술이 장기간의 멘토링을 필요로 하여 신속한 자격 인증을 저해한다고 강조합니다. 공급업체에게 실용적인 결과는 통합 가이드 소프트웨어, 표준 치료 체크리스트, 인공지능 지원 내비게이션을 갖춘 시스템에 대한 신흥 시장이 등장하고 있다는 점입니다. 훈련 기간을 단축하는 기기는 활용률을 개선하여, 경쟁적인 자본 요청 사이에서 결정하는 관리자들의 비즈니스 사례를 강화합니다.

위장 내시경은 2024년 시장 점유율 54.9%를 차지하며 대장 내시경 및 상부 위장관 진단에 대한 높은 의존도를 반영했습니다. 그러나 비만 수술 재수술 및 자궁내막증 치료와 같은 적응증 확대로 복강경 검사는 2030년까지 연평균 8.9% 성장할 것으로 전망됩니다. 이러한 추세는 다학제적 수술실 팀이 복강경 및 내시경 모드 전환이 가능한 모듈식 타워 구성을 추진할 수 있음을 시사하며, 이는 고량 위장관 수술실과 유연한 다학제 수술실 간 조달 전략을 효과적으로 분할할 수 있습니다.

내시경 초음파(EUS) 역시 미국에서 증가하는 상부 위장관 EUS 시술 건수로 입증되듯 주목받고 있습니다. EUS가 병기 결정과 췌장신경절 신경절제술 같은 치료적 중재를 모두 용이하게 하기 때문에, 병원들은 이 기술을 진단 비용 센터가 아닌 수익 증대 보조 수단으로 포지셔닝하기 시작했으며, 이로 인해 예산 권한이 방사선과에서 위장관과로 미묘하게 이동하고 있습니다.

재사용 내시경은 2024년 기준 82% 점유율로 여전히 우세하지만, 일회용 제품은 연간 12.5% 성장 중입니다. 일회용 내시경과 표준 장치를 비교한 연구에 따르면 재처리 시간이 약 48분에서 10분 미만으로 단축되어 일일 처리량이 실질적으로 3배 증가합니다. 대부분의 외래수술센터(ASC)가 빡빡한 일일 일정으로 운영된다는 점을 고려하면 이 처리량 증가는 매우 매력적입니다. 진료 시간을 연장하지 않고도 룸당 추가 2-3건의 시술이 가능해지면 EBITDA 마진을 실질적으로 개선할 수 있습니다.

이러한 파급 효과로 시설 관리자들이 감염 위험 완화와 환경적 영향을 동시에 고려함에 따라 폐기물 관리 및 지속가능성에 대한 관심이 높아지고 있습니다. 이러한 이중적 고려사항은 향후 구매 기준을 재활용 가능 소재 및 회수 프로그램으로 전환시키는 데 영향을 미칠 것이며, 이는 제조사들에게 새로운 서비스 라인 수익 모델을 도입할 기회를 제공할 것입니다.

The endoscopy devices market stands at USD 40.10 billion in 2025 and is forecast to reach roughly USD 55.09 billion by 2030, reflecting a compound annual growth rate (CAGR) close to 6.56%.

Rising acceptance of minimally invasive surgery continues to reshape hospital capital budgets, drawing investment toward visualization towers and advanced imaging modules that shorten patient recovery times while freeing operating-room slots for high-margin procedures. At the same time, infection-control mandates are redirecting procurement toward disposable or partly disposable scopes, a shift that not only reduces reprocessing labor but also limits reimbursement penalties linked to hospital-acquired infections. Growth in Asia-Pacific is outpacing global averages as expanding insurance coverage collides with a shortage of trained endoscopists, prompting buyers in that region to favor intuitive, software-guided platforms that compress learning curves. Established North American providers remain anchor customers, yet their quick adoption of single-use duodenoscopes is pressuring manufacturers to balance premium pricing with volume-driven cost efficiencies.

Across specialties, clinicians are reshaping care pathways around minimally invasive interventions. Endoluminal robotics-allowing navigation through natural orifices-illustrates how product roadmaps are converging on the same value proposition: lower patient trauma, shorter admissions, and quicker recoveries. A second-order implication is that hospitals now tie capital-budget requests for imaging suites and OR renovations to claims of throughput gains driven by these technologies; therefore, endoscopy vendors must increasingly compete on measurable workflow efficiencies rather than image quality alone.

High-definition optics, 3D imagery, and software-enhanced contrast platforms have improved early-lesion detection. Olympus's EVIS EXERA III, for example, leverages Narrow Band Imaging (NBI) and Dual Focus to lift adenoma detection rates during colonoscopy. The strategic corollary for providers is the emerging ability to selectively biopsy smaller tissue volumes, which not only accelerates pathology turnaround but also reduces consumable costs at scale. That optimization, in turn, allows outpatient facilities to maintain competitive reimbursement rates while still meeting quality benchmarks.

Expanding indications have outpaced the global supply of skilled endoscopists. The American Society for Gastrointestinal Endoscopy stresses that advanced procedures such as ERCP and EUS require prolonged mentorships, deterring rapid credentialing. A pragmatic consequence for suppliers is an emerging market for systems with integrated guidance software, standard-of-care checklists, and artificial-intelligence-assisted navigation. Devices that shorten training timelines improve utilization rates, thereby strengthening the business case for administrators deciding between competing capital requests.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Gastrointestinal endoscopy secured 54.9% market share in 2024, reflecting heavy reliance on colonoscopy and upper-GI diagnostics. Yet laparoscopy is projected to rise at an 8.9% CAGR through 2030, driven by expanded indications such as bariatric revisions and endometriosis treatment. This momentum suggests that multi-disciplinary OR teams may push for modular tower configurations capable of switching between laparoscopic and endoscopic modes, effectively bifurcating procurement strategies into high-volume GI suites versus flexible multi-specialty rooms.

Endoscopic ultrasound (EUS) is also gaining traction, evidenced by rising upper-GI EUS volumes in the United States. Because EUS facilitates both staging and therapeutic interventions like celiac plexus neurolysis, hospitals have started to position the technology as a revenue-enhancing adjunct rather than a diagnostic cost center, subtly shifting budgeting authority from radiology to GI departments.

Reusable scopes still dominate with an 82% share in 2024, but disposables are growing 12.5% annually. Studies comparing disposable-sheath gastroscopes with standard devices demonstrate reprocessing times dropping from roughly 48 minutes to under 10 minutes, effectively tripling possible daily throughput. That throughput improvement is compelling when one considers that most ASCs operate on tight daily schedules; an extra two to three cases per room can materially improve EBITDA margins without extending clinic hours.

The knock-on effect is a heightened focus on waste management and sustainability, as facility managers weigh infection risk mitigation against environmental impact. This dual consideration is likely to influence future purchasing criteria toward recyclable materials and take-back programs, introducing new service-line revenue models for manufacturers.

The Endoscopy Devices Market Report is Segmented by Device Type (Endoscopes [Rigid Endoscopes, and More], Endoscopic Operative Devices [Access Devices, and More], and More), Application (Gastrointestinal, and More), Usability (Reprocessed / Reusable Devices, and More), End-User (Hospitals, Academic Medical Centers, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).