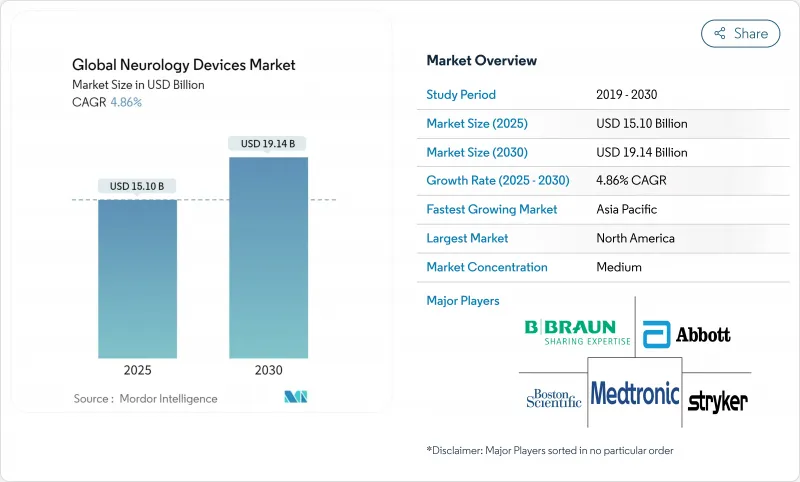

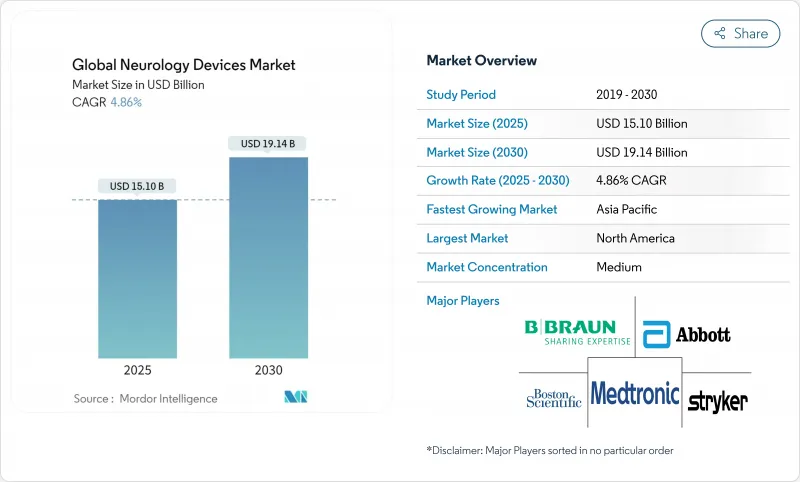

신경 기기 시장은 2025년에 151억 달러를 창출하고, 2030년에는 191억 4,000만 달러에 이르며, CAGR 4.86%를 나타낼 전망입니다.

이 성장은 에피소드 중심의 병원 중심의 개입에서 인공지능과 폐 루프 신경 자극 시스템에 의한 데이터 풍부한 예측 케어 모델로의 이동을 반영합니다. 뇌졸중, 파킨슨병, 간질, 만성 통증이 여전히 공중 보건의 최우선 과제이며, 노화로 인해 신경 질환 부담이 증가함에 따라 수요가 확대됩니다. 자본 유입, 적응형 자극 기기의 FDA 승인 취득 가속화, 기계적 혈전 제거 카테터의 획기적인 진보가 기세를 늘리고, 클로즈드 루프 기기의 상환 코드 갱신이 주요 시장에서의 지불자의 마찰을 경감합니다. 반대로 희토류 자석과 비스무트 합금을 둘러싼 공급망 리스크는 중저소득국가의 외과의 부족과 함께 신경 기기 시장의 잠재력을 충분히 발휘시키지 않는 요인이 되고 있습니다.

신경질환은 현재 세계 인구의 43%에 영향을 미치고 있으며 치료 기기의 대응 영역이 확대되고 있습니다. 뇌졸중 : 대혈관 폐색은 허혈 사례의 최대 40%를 차지하며 신속한 혈전 제거 솔루션이 필요합니다. COVID-19 및 기타 병원체에 의한 바이러스 감염 후 신경학적 후유증은 기기 사용을 더욱 향상시킵니다. 이러한 역학적 현실을 바탕으로 신경 기기 시장은 지속적으로 효과적인 개입책과 확장 가능한 만성질환 모니터링 전략을 우선시하고 있습니다.

4세대 흡입 카테터, 스티어러블 마이크로카테터, 300mT/m 구배 MRI 스캐너는 절차 시간을 단축하고 진단 정확도를 향상시킵니다. 혈전 제거 기기에 내장된 실시간 알고리즘은 패스트 패스의 성공을 향상시키고 다운스트림 비용을 절감합니다. 로봇공학, 증강현실, AI의 상호작용으로 신경외과의사의 학습 곡선이 빨라져 노동력 부족에 대처할 수 있습니다. 임상적 역치 상승으로 기술 업그레이드는 연구개발 집약 기업의 점유율을 강화하고 진입장벽을 강화함으로써 신경 기기 업계의 롱테일 공급업체에 영향을 미칩니다.

척수 자극 임플란트의 비용은 3만 5,000-7만 달러, 재수술은 1만 5,000-2만 5,000 달러이며, 보험 미가입층에의 보급은 한정적입니다. 발거율은 주로 효능 손실로 10% 가까이에 이르며 총소유비용에 대한 불안이 높아지고 있습니다. 인도에서는 동맥류 수리를 위한 박리 가능한 코일이 10%의 수입 관세가 걸려 MD DI의 가격 장애물을 더욱 높이고 있습니다. 이러한 비용 장벽은 임상적 필요성에도 불구하고 보급을 늦추고 있습니다.

기계적 혈전 제거술과 흐름 다이버터 임플란트가 급성 허혈성 뇌졸중의 표준 치료가 되었기 때문에 인터벤셔널 시스템은 2024년에 신경 기기 시장의 38.78%를 차지했습니다. EXCELLENT 레지스트리 데이터에 따르면 EMBOTRAP retriever의 최종 재관류율은 94.5%이며 의사의 신뢰가 높아지고 있습니다. 신경 진단 모니터, 뇌척수액 션트, 신경 자극 임플란트는 모두 병원 조달 예산의 중심이며, 스티어러블 마이크로카테터와 같은 플랫폼 업그레이드는 자본 교체 사이클을 활발하게 하고 있습니다.

CAGR 5.34%를 기록한 재활 및 착용가능한 장비는 수술 후 및 만성 질환의 집에서 모니터링을 점점 더 가능하게 합니다. 귀걸이형 EEG 웨어러블은 발작의 전조를 파악하고, 긴급 입원을 줄이고, 정기적인 서비스 수익을 확대합니다. 여기서 경쟁 장벽은 하드웨어보다 오히려 데이터 분석 IP에 달려 있으며 하이테크 기업의 진입을 촉구하고 있습니다. 결과적으로 기존 카테터와 션트공급업체는 성숙한 극장 기반 제품의 성장 둔화를 헤지하기 위해 포트폴리오를 다양화하고 있습니다.

2024년 매출은 북미가 40.67%의 점유율을 차지하며 최고가 되었습니다. 캐나다의 단일 지불 모델은 전국적인 폐쇄 루프 SCS 시험에 자금을 제공하고 멕시코는 관민 파트너십을 통해 MRI 조달을 가속화하고 있습니다.

아시아태평양은 중국의 BCI 로드맵과 일본의 원격 의료 파일럿에 힘입어 CAGR 7.13%의 최고 속도를 기록하고 있습니다. 정부 보조금은 국내 플로우 다이버터 제조를 촉진하고 수입에 대한 의존도를 낮추고 지역 챔피언을 강화합니다. 인도에서는 고령화 사회가 확대됨에 따라 디테이쳐블 코일 매출이 두 자릿수 성장을 기록하고 있지만 가격면에서의 격차는 여전히 남아 있습니다.

유럽은 의료기기 규정 하에서 임상 가치의 실증을 중시하고 안정적으로 공헌하고 있습니다. 독일에서는 수두증의 발생률이 상승하여 션트 수요를 뒷받침하고 있습니다. 한편 영국에서는 AI를 활용한 뇌졸중 치료법을 시험적으로 도입하고 있으며, 이는 유럽 전역으로 확대될 가능성이 있습니다. 반면 스위스에서는 FDA 승인을 받을 수 있으며, 미국을 중심으로 한 제조업체들에게는 두 시장에서의 출시가 효율화됩니다.

The Neurology Devices market generated USD 15.10 billion in 2025 and is on course to reach USD 19.14 billion by 2030, advancing at a 4.86% CAGR.

Growth reflects a shift from episodic, hospital-centric interventions to data-rich, predictive care models powered by artificial intelligence and closed-loop neuro-stimulation systems. Demand widens as stroke, Parkinson's disease, epilepsy and chronic pain remain high-priority public-health issues, and as aging populations intensify the neurological disease burden. Capital inflows, accelerated FDA clearances for adaptive stimulators and breakthroughs in mechanical thrombectomy catheters add momentum, while reimbursement code updates for closed-loop devices reduce payer friction in key markets. Conversely, supply-chain risks around rare-earth magnets and bismuth alloys, together with surgeon shortages in low- and middle-income countries, temper the Neurology Devices market's full potential.

Neurological conditions now affect 43% of the global population, expanding the addressable pool for therapeutic devices. . Stroke remains paramount: large-vessel occlusions represent up to 40% of ischemic cases and demand rapid thrombectomy solutions. Post-viral neurological sequelae following COVID-19 and other pathogens further elevate device utilization. Given these epidemiologic realities, the Neurology Devices market continues to prioritise high-efficacy interventions and scalable chronic-disease monitoring strategies.

Fourth-generation aspiration catheters, steerable micro-catheters and 300 mT/m gradient MRI scanners shorten procedure time and elevate diagnostic precision. Real-time algorithms embedded in thrombectomy devices improve first-pass success and reduce downstream costs. Interplay of robotics, augmented reality and AI prompts faster learning curves for neurosurgeons, helping address workforce deficits. By raising clinical thresholds, technology upgrades consolidate share for R&D-intensive firms and reinforce entry barriers, affecting long-tail suppliers in the Neurology Devices industry.

Spinal cord stimulation implants cost USD 35,000-70,000, while revisions add USD 15,000-25,000, limiting penetration among under-insured cohorts Journal of Pain Research. Explant rates hover near 10% owing mainly to efficacy loss, raising total-cost-of-ownership anxieties. In India, detachable coils for aneurysm repair attract import duties of 10%, compounding affordability hurdles MD+DI. Such cost vectors slow adoption despite clinical need.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Interventional systems captured 38.78% Neurology Devices market share in 2024 as mechanical thrombectomy and flow-diverter implants became standard of care for acute ischemic stroke. Data from the EXCELLENT registry showed final reperfusion rates of 94.5% with the EMBOTRAP retriever, reinforcing physician confidence. Neurodiagnostic monitors, cerebrospinal-fluid shunts and neuro-stimulation implants collectively anchor hospital procurement budgets, while platform upgrades, such as steerable micro-catheters, keep capital-replacement cycles brisk.

Rehabilitation & wearable devices, posting a 5.34% CAGR, increasingly enable post-operative and chronic-disease monitoring at home. In-ear EEG wearables capture seizure precursors, reducing emergency admissions and widening recurring-service revenue. Competitive barriers here hinge on data-analytics IP rather than hardware, inviting tech entrants. Consequently, incumbent catheter and shunt suppliers diversify portfolios to hedge against slower growth in mature theatre-based products.

The Neurology Devices Market Report Segments the Industry Into by Type of Device (Neurostimulation Devices, Interventional Neurology Devices and More), by Application (Stroke Management, Chronic Pain & Movement Disorders and More), by End User (Hospitals, Ambulatory Surgery Centers and More) and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led revenue with 40.67% share in 2024 on the back of robust payer coverage, highly skilled neurologists and R&D ecosystems. Canada's single-payer model funds nationwide closed-loop SCS trials, while Mexico accelerates MRI procurement via public-private partnerships.

Asia-Pacific posts the quickest 7.13% CAGR, propelled by China's BCI roadmap and Japan's remote-care pilots. Government grants subsidise domestic flow-diverter manufacturing, reducing import reliance and bolstering local champions. India logs double-digit growth in detachable-coil sales as its ageing cohort expands, although affordability gaps persist.

Europe remains a steady contributor, emphasising clinical-value demonstration under Medical Device Regulation. Germany's rising hydrocephalus incidence fuels shunt demand, whereas the United Kingdom pilots AI-triaged stroke pathways that may scale continent-wide. Meanwhile, Switzerland's potential recognition of FDA approvals streamlines dual-market launches, benefiting US-centric manufacturers.