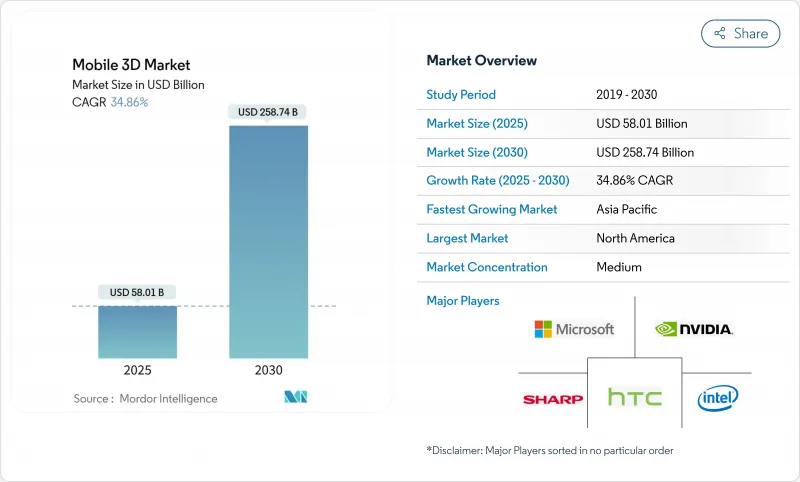

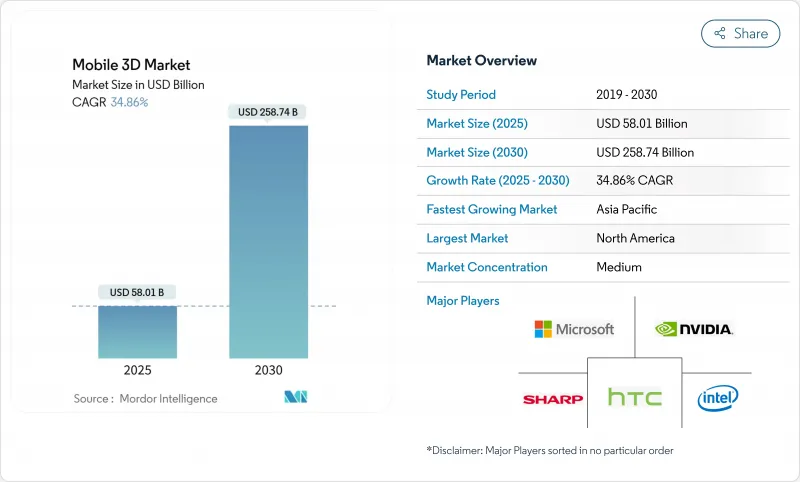

모바일 3D 시장은 2025년에 580억 1,000만 달러를 창출하고, 2030년에는 CAGR 34.86%를 나타내 2,587억 4,000만 달러에 이를 것으로 예측됩니다.

강력한 성장은 Edge AI 처리와 고급 심도 감지 모듈의 조합이 일상적인 모바일 단말기를 공간 컴퓨팅 도구로 바꾸는 것을 반영합니다. OLED 마이크로디스플레이의 비용 절감으로 스마트폰, 접이식 단말기 및 웨어러블 단말기로 고해상도 공간 컨텐츠에 대한 액세스가 확대됩니다. 비행 시간형(ToF) 센서가 모바일 이미징을 강화하는 반면, 라이트 필드 프로세서는 30fps에서 4K 홀로그램 화질에 도달하여 깊이 캡처 혁신의 다음 파도를 알려줍니다. 기업의 생산성 향상, AR 게임의 보급, 5G 네트워크의 전개가 유저 수요를 더욱 높입니다. VCSEL 이미터와 SPAD 센서를 둘러싼 공급망의 재조합이 부품 제조업체 간의 협상력을 재구성하는 한편, 열 관리와 배터리 내구성은 여전히 설계상의 제약이 되고 있습니다.

비행 시간 및 구조화된 광원 어레이는 인물 이미지와 증강현실(AR) 오버레이의 정확한 깊이 캡처를 지원합니다. 삼성 ISOCELL Vizion 33D는 거리 측정 정밀도를 향상시키고 Apple의 iPhone 15 Pro의 공간 비디오 기능은 네이티브 3D 캡처에 대한 소비자의 의욕을 뒷받침합니다. 메타 간접 ToF 특허는 모션 블러의 경감과 전력 효율을 개선하고 컴팩트한 폼 팩터에서의 응답성을 높입니다. 로봇 공학과 자동화를 지원하는 물체 측정 정밀도로 산업 분야가 이익을 얻는다.

Instagram에서 인기있는 AR 게임과 얼굴 필터는 3D 기능의 습관적인 사용을 촉진합니다. 4만 2,000개의 Instagram 효과의 학술적 리뷰에 따르면, 미화 필터는 업로드의 20%를 차지하며 실시간 얼굴 확장에 대한 수요를 보여줍니다. Ericsson의 보고에 따르면 5G 가입자는 대역폭이 안정적이기 때문에 AR 사용이 크게 증가하고 있습니다. Qualcomm의 On-device Stable Diffusion은 15초 이내에 현실감 있는 장면을 생성하여 수백만 대의 기기에 제작자 도구를 제공합니다. 이러한 개발은 사용자 생성 3D 컨텐츠의 장벽을 낮추고 소셜 플랫폼 전체의 네트워크 효과를 증폭시킵니다.

Vision Pro의 제조 비용 1,519달러는 마이크로 OLED와 센서 어셈블리에 비싼 부담을 드러냅니다. 또한 컨텐츠 팀은 학습 곡선이 가파르기 때문에 소규모 스튜디오에서는 한계가 있습니다. 그럼에도 불구하고 Howden은 선행 투자에도 불구하고 맞춤형 AR 워크 플로우로 측정 가능한 유지 보수 비용을 보고했습니다. 구성 요소 규모가 늘어나면서 가격이 떨어지고 있지만, 특히 피처폰 전환이 진행되는 신흥 시장에서는 주류의 저렴한 가격이 중기적인 과제로 남아 있습니다.

스마트폰이 2024년 모바일 3D 시장의 72%를 차지했지만, 이는 설치 기반의 이점과 하드웨어의 연간 업데이트 주기를 반영합니다. 플래그십 터미널은 현재 ToF 어레이, AI 가속기, OLED 디스플레이를 탑재하여 공간 컴퓨팅 로드맵의 기준선을 형성하고 있습니다. 삼성의 갤럭시 S25 시리즈는 일상적인 사진을 깊이 매핑된 3D 자산으로 바꾸는 AI를 탑재한 ProVisual 이미징에서 이를 보여줍니다. Foldables는 사용자의 몰입감을 높이는 계층화된 인터페이스를 도입하고 태블릿과 노트북은 3D 협업을 더 큰 캔버스로 확장합니다.

AR/VR 안경은 현재 분자로서는 작지만 CAGR36.10%로 가장 빠르게 성장하고 있습니다. Meta의 Reality Labs는 44억 달러의 영업 손실에도 불구하고 기록적인 수익을 기록하고 잠재적인 소비자의 지지를 강조했습니다. Google과 삼성은 2026년 안드로이드 XR 안경을 발표하고 플랫폼 수준의 헌신을 보여줍니다. 이러한 장치는 몰입형 게임부터 현장 유지 보수 오버레이에 이르기까지 엔터테인먼트와 기업의 다리가 됩니다. 시장 규모가 확대됨에 따라 웨어러블 모바일 3D 시장 규모는 예측 기간 동안 스마트폰과의 차이를 줄일 것으로 보입니다.

3D 이미지 센서는 2024년 모바일 3D 시장 규모의 46.30%를 차지하며 스마트폰, 태블릿 및 헤드셋 깊이 캡처의 핵심 역할을 했습니다. 소니의 태국에서의 사업 확장은 차량용 LiDAR과 모바일 ToF 모듈 모두의 다이오드 용량을 확보하고 단기적인 병목 현상을 완화합니다. VCSEL 이미터는 여전히 공급에 제약을 받고 있으며 OEM 회사는 가능한 한 이중 조달을 촉구하고 있습니다.

OLED 마이크로디스플레이는 기세가 있어 연률 35%의 성장을 이루고 있습니다. LG디스플레이와 중국의 진입기업이 성막라인을 증강하고 리드타임을 단축하고 있어 비용 곡선이 하향으로 구부러지고 있습니다. 디스플레이 기술 혁신은 또한 전용 3D GPU와 지연을 급증시키지 않고 고픽셀 밀도를 관리하는 ISP 수요에도 박차를 가하고 있습니다. 부품 비용이 낮아 채택이 촉진되어 공정 개선의 원가가 되고 시장 세분화의 혁신 주기가 활발해지고 있습니다.

모바일 3D 시장 보고서는 3D 지원 모바일 기기(스마트폰, 태블릿 등), 기기 구성 요소(3D 이미지 센서, 3D GPU/ISP 등), 3D 기술(ToF(Time-Of-Flight), Structured-Light 등), 3D 용도(모바일 게임, 지도 및 탐색, 애니메이션 및 3D 컨텐츠 제작, 기타)

2024년 모바일 3D 시장 점유율은 북미가 40%로 최상위를 차지했고, 기업 투자와 높은 재량 소득이 뒷받침 Meta의 누적 AR/VR 지출은 1,000억 달러를 넘어, 지역의 연구 개발의 기세를 가속시키고 있습니다. 산업 기업은 AR 대응 워크플로우에 의한 생산성 향상을 보고하고, 소비자는 최첨단의 3D 기능을 소개하는 프리미엄 스마트폰을 용이하게 채용합니다.

아시아태평양은 2030년까지의 CAGR이 41.02%로 성장의 페이스메이커입니다. 중국의 3D 산업용 카메라 매출은 로봇 수요를 배경으로 2024년에는 23억 6,200만 위안(3억 3,400만 달러)에 달했습니다. 이 지역은 모바일 부가가치로 GDP에 8,800억 달러 공헌하고 있으며, 공급자인 동시에 수요의 중심지이기도 합니다. 한국과 일본 기업이 디스플레이와 홀로 프로세서 연구를 추진하고 베트남과 인도의 수탁 제조업자가 AR웨어러블의 새로운 조립 명령을 흡수합니다.

유럽에서는 자동차 및 항공우주 산업에서 인더스트리 4.0 프로젝트에 견인되어 꾸준한 보급이 기록됩니다. 규제는 안전한 데이터 처리를 지원하고 에지 AI 3D 도구의 평가판을 기업에 촉구합니다. 중동 및 아프리카와 라틴아메리카는 아직 막 시작된 시장이지만, 5G의 보급과 도시화가 진행되고, 하드웨어의 비용이 내려가면, 보급이 가속될 가능성이 있습니다.

The Mobile 3D market generated USD 58.01 billion in 2025 and is forecast to reach USD 258.74 billion by 2030, advancing at a 34.86% CAGR.

Robust growth reflects the pairing of edge-AI processing with advanced depth-sensing modules that turn everyday handsets into spatial-computing tools. Declining OLED micro-display costs widen access to high-resolution spatial content across smartphones, foldables, and wearables. Time-of-Flight (ToF) sensors strengthen mobile imaging while Light-Field processors reach 4K hologram quality at 30 fps, signaling the next wave of depth-capture innovation. Enterprise productivity gains, AR gaming uptake, and 5G network rollouts further elevate user demand. Supply-chain reshuffles around VCSEL emitters and SPAD sensors reshape bargaining power among component makers, while thermal management and battery endurance remain design constraints.

Time-of-Flight and structured-light arrays now underpin precise depth capture for portrait imaging and augmented-reality overlays. Sony expanded its Thai laser-diode plant in 2024 to meet surging demand, adding 2,000 jobs to scale VCSEL output.Samsung's ISOCELL Vizion 33D boosts range accuracy, and Apple's spatial-video feature on iPhone 15 Pro underlines consumer appetite for native 3D capture. Meta's indirect-ToF patent improves motion-blur mitigation and power efficiency, enhancing responsiveness in compact form factors. Industrial sectors gain from object measurement precision that supports robotics and automation.

AR games and face filters popularized by Instagram drive habitual use of 3D features. Academic review of 42,000 Instagram effects found beautification filters represented 20% of uploads, illustrating demand for real-time facial augmentation. Ericsson reports that 5G subscribers show materially higher AR engagement due to stable bandwidth. Qualcomm's on-device Stable Diffusion generates photorealistic scenes under 15 seconds, opening creator tools to millions of handsets. These developments lower barriers for user-generated 3D content and amplify network effects across social platforms.

Vision Pro's manufacturing cost of USD 1,519 exposes the premium burden of micro-OLED and sensor assemblies. Content teams also face steep learning curves, limiting smaller studios. Howden nonetheless reports measurable maintenance savings from custom AR workflows despite upfront spend. Component scale-up is pushing prices lower, yet mainstream affordability remains a mid-term challenge, especially in emerging markets where feature-phone transitions still play out.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Smartphones captured 72% of the Mobile 3D market in 2024, reflecting the installed base advantage and annual hardware refresh cycles. Flagship handsets now bundle ToF arrays, AI accelerators, and OLED displays, forming the baseline for spatial computing roadmaps. Samsung's Galaxy S25 series exemplifies this with AI-powered ProVisual imaging that turns everyday photos into depth-mapped 3D assets. Foldables introduce layered interfaces that deepen user immersion, while tablets and notebooks extend 3D collaboration to larger canvases.

AR/VR eyewear commands a smaller numerator today but posts the fastest ascent at 36.10% CAGR. Meta's Reality Labs, despite USD 4.4 billion operating losses, booked record revenue, underscoring latent consumer pull. Google and Samsung will debut Android XR glasses in 2026, signaling platform-level commitment. These devices bridge entertainment and enterprise, from immersive games to on-site maintenance overlays. As volumes scale, the Mobile 3D market size for wearables will close the gap with smartphones over the forecast window.

3D image sensors held 46.30% of the Mobile 3D market size in 2024, serving as the cornerstone for depth capture across phones, tablets, and headsets. Sony's Thai expansion secures diode capacity for both automotive LiDAR and mobile ToF modules, easing short-term bottlenecks. VCSEL emitters remain supply-constrained, prompting OEMs to dual-source where possible.

OLED micro-displays are the momentum story, growing 35% annually. Cost curves bend downward as LG Display and Chinese entrants ramp deposition lines, shortening lead times. Display innovation also spurs demand for dedicated 3D GPUs and ISPs that manage higher pixel densities without latency spikes. The components segment illustrates a virtuous loop: lower part costs lift adoption, which in turn funds further process improvements, keeping the Mobile 3D market innovation cycle brisk.

The Mobile 3D Market Report is Segmented by 3D Enabled Mobile Devices (Smartphones, Tablets, and More), Device Components (3D Image Sensors, 3D GPUs/ISPs, and More), 3D Technology (Time-Of-Flight (ToF), Structured-Light, and More), 3D Applications (Mobile Gaming, Maps and Navigation, Animations and 3D Content Creation, and More), and Geography.

North America led with a 40% Mobile 3D market share in 2024, buoyed by enterprise investments and high discretionary income. Meta's cumulative AR/VR outlay topping USD 100 billion amplifies regional R&D momentum. Industrial firms report productivity gains from AR-enabled workflows, while consumers readily adopt premium smartphones that showcase bleeding-edge 3D features.

Asia Pacific is the growth pacesetter at a 41.02% CAGR through 2030. China's 3D industrial camera revenue reached CNY 2.362 billion (USD 334 million) in 2024 on the back of robotics demand. The region contributes USD 880 billion of mobile value-added to GDP, positioning it as both supplier and demand center. Korean and Japanese firms push display and holo-processor research, while contract manufacturers in Vietnam and India absorb new assembly mandates for AR wearables.

Europe records steady take-up driven by Industry 4.0 projects in automotive and aerospace. Regulation supports secure data handling, encouraging enterprises to trial edge-AI 3D tools. Middle East and Africa and Latin America remain nascent Mobile 3D markets, yet rising 5G penetration and urbanization lay groundwork for accelerated adoption once hardware costs dip.