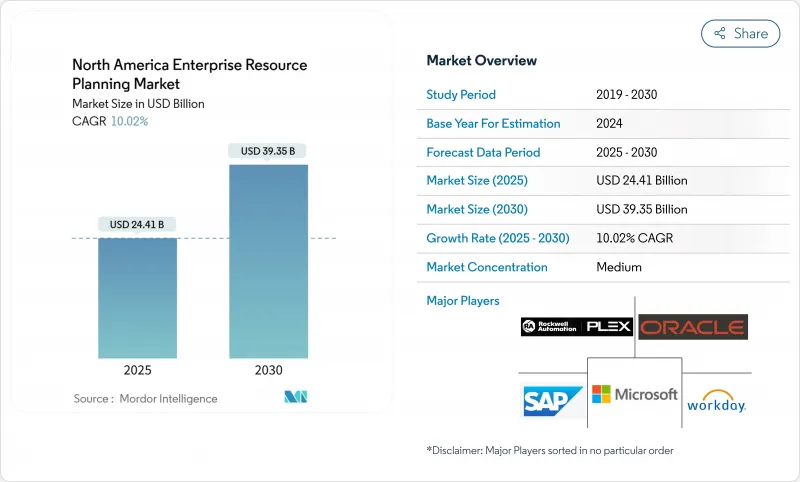

북미의 전사적 자원 관리 시장 규모는 2025년 244억 1,000만 달러, 2030년 393억 5,000만 달러에 이를 것으로 예측되며, CAGR은 10.0%를 나타낼 전망입니다.

이 확장은 레거시 On-Premise 제품군에서 기업에 민첩성, 실시간 인사이트 및 소비 기반 비용 구조를 제공하는 클라우드 네이티브 플랫폼으로의 전역 전이를 반영합니다. 또한 환경·사회·거버넌스(ESG)의 공개가 의무화됨에 따라 기업은 재무 연결 프로세스의 근대화를 강요받고 있습니다. Oracle은 2024년 매출액 87억 달러, 시장 점유율 6.63%(북미의 전사적 자원 관리)로 SAP를 제치고 지역 최대의 ERP 용도 공급업체가 되어, Tier 1 벤더간의 라이벌 관계의 격화를 돋보이게 했습니다. 미국은 주와 지방 시스템의 현대화를 계속하고 있으며, 캐나다의 디지털 도입 프로그램은 제조업의 ERP 투자를 조성하고 멕시코는 USMCA의 디지털 무역 조항을 활용하여 국경을 넘어서는 데이터 흐름을 합리화하고 있습니다.

비용, 확장성, 원격 근무 지원이 On-Premise 지향을 구축하고 클라우드 도입이 ERP 신규 도입의 기본이 되고 있습니다. 워싱턴주 클라크 카운티에서는 Workday로 전환한 후 급여 계산이 60% 빨라졌고 승인되지 않은 지출이 15% 감소했습니다. 하이브리드 아키텍처가 여전히 흔한 이유는 엄격한 기업이 민감한 데이터를 On-Premise로 유지하면서 에지 및 특수 기능을 퍼블릭 클라우드에서 확장하기 때문입니다. 제조업에서는 보안 투자가 급증하고 재무 팀은 구독 가격으로 하드웨어 업데이트주기보다 전략적 혁신에 자본 예산을 돌릴 수 있게 되었습니다. 최고정보책임자(CIO)는 기술 업그레이드와 병행하여 관계자 교육을 우선하고 문화적 채용과 아키텍처의 변화를 일치시킵니다.

생성 모델과 예측 모델은 ERP를 트랜잭션 레코더에서 지능형 오케스트레이션 엔진으로 재구성합니다. IBM과 Oracle은 현재 재정, 공급망 및 인사 워크플로우 전반에 걸쳐 정책을 준수하는 조치를 권장하는 자율 에이전트를 공동 개발하고 있습니다. NetSuite의 머신러닝을 통한 현금 모듈은 수작업으로 인보이스 입력을 줄이고 대조를 가속화하여 월말 마감을 완화합니다. 제조업은 공장 수준의 모듈에 AI를 통합하여 예지보전을 하고 이미 스마트 팩토리 기술을 도입하고 있는 95%의 기업으로 계획 밖의 다운타임 단축을 추진하고 있습니다. 의료 서비스 제공업체는 애널리틱스를 활용하여 임상 데이터와 재무 데이터를 비교하여 진료 보상 정확성과 컴플라이언스 보고를 개선합니다. 알고리즘의 편향과 데이터의 진부화는 자동화된 의사결정에 대한 신뢰를 손상시킬 수 있으므로 모든 이니셔티브는 견고한 거버넌스에 의존합니다.

종합적인 ERP 프로젝트는 라이선스 수수료와 구독 수수료뿐만 아니라 다양한 비용을 발생시킵니다. 침례 건강의 여러 해에 걸친 현대화에서 볼 수 있듯이, 데이터 마이그레이션, 비즈니스 프로세스 리엔지니어링, 직원 교육은 병원과 공공 기관의 초기 예산의 두 배가 되는 경우가 많습니다. 중소기업에서는 전임 IT 용량이 부족하기 때문에 외부 컨설턴트에 의존하고 있지만 인력이 부족하여 일당이 높아지고 일정이 늘어나고 있습니다. 클라우드 전달은 자본 지출을 억제하지만 프로세스의 표준화에 필요한 문화적 변화를 배제할 수는 없습니다. 견고한 변경 리더십 구조가 없으면 비용이 많이 드는 플랫폼이 충분히 활용되지 않아 ROI가 떨어질 위험이 있습니다.

2024년 매출은 클라우드 네이티브 스위트가 60.5%를 차지하며, 북미의 전사적 자원 관리 시장은 광범위한 기능을 갖춘 플랫폼의 강력한 기준선을 유지했습니다. 그러나 소셜/협업형 ERP는 기업이 소비자급 사용자 경험을 요구함에 따라 2030년까지 연평균 복합 성장률(CAGR)이 11.4%로 가장 빠르게 성장하고 있습니다. 지식 근로자는 재무 및 공급망 거래 내에서 활동 피드, 공유 대시보드 및 실시간 채팅을 채택하여 시스템 활용도를 높이고 승인 주기를 단축합니다. 통합된 모바일 앱은 현장과 고객사에서도 동일한 기능을 제공하여 지속적인 워크플로를 강화합니다. 공급업체의 로드맵은 소셜 요소를 선택적 모듈로 사용하는 대신 기본적으로 번들로 제공하여 전략적 가치를 강조합니다. 이윽고 이러한 채널에 내장된 인공지능 어시스턴트가 행동을 추천하거나 예외에 플래그를 붙이게 되어, 참여와 업무 효율의 연결이 깊어집니다.

재무 및 회계는 보고 및 감사의 필수 요건을 반영하여 2024년 북미의 전사적 자원 관리 시장 규모의 55.7%를 유지했습니다. 그럼에도 불구하고 공급망 및 운영 모듈은 CAGR 10.8%를 나타낼 전망입니다. 엣지 컴퓨팅과 사물 인터넷은 실시간 현장 데이터를 계획 알고리즘으로 전송하여 자재 공급 능력을 향상시키고 운전 자본을 줄입니다. 선적 예측 ETA는 옴니 채널 확약을 지원하며 자동화된 품질 검사는 반품률을 줄입니다. 한편, 노동력 부족과 이직률 상승에 직면한 제조업에서는 인적자본 모듈이 우선합니다. 고객 커머스 애드온은 주문 캡처와 인벤토리를 연결하여 전환율을 높이는 정확한 납기를 약속할 수 있도록 합니다. 재무는 여전히 시스템 오브 레코드로서 기능하고 있지만, 비즈니스 데이터 세트가 손익의 결과를 좌우하는 경우가 많습니다.

The North America enterprise resource planning market size stands at USD 24.41 billion in 2025 and is projected to reach USD 39.35 billion by 2030, reflecting a sturdy 10.0% CAGR.

This expansion mirrors the region-wide migration from legacy on-premise suites to cloud-native platforms that give firms agility, real-time insights, and consumption-based cost structures. Heightened interest in AI-embedded analytics is reshaping implementation roadmaps, while mandatory environmental, social, and governance (ESG) disclosures push companies to modernize their financial consolidation processes. Oracle overtook SAP as the region's largest ERP application supplier in 2024 with USD 8.7 billion in revenue and 6.63% North America enterprise resource planning market share, underscoring a sharpening rivalry among tier-1 vendors. Governments also catalyze uptake: the United States continues to modernize state and local systems, whereas Canada's Digital Adoption Program subsidizes manufacturing ERP investments, and Mexico leverages USMCA digital-trade provisions to streamline cross-border data flows.

Cloud adoption is now the baseline for new ERP rollouts as cost, scalability, and remote-work support eclipse entrenched on-premise preferences. Clark County, Washington, recorded 60% faster payroll runs and cut unapproved spending by 15% after moving to Workday. Hybrid architectures remain common because highly regulated firms keep sensitive data on-premise while extending edge or specialty functionality in public clouds. Security investments rose sharply in manufacturing corridors, and subscription-pricing lets finance teams reallocate capital budgets to strategic innovation rather than hardware refresh cycles. Alongside technology upgrades, chief information officers prioritize stakeholder training so cultural adoption matches architectural transformation.

Generative and predictive models are reshaping ERP from transaction recorders to intelligent orchestration engines. IBM and Oracle now co-develop autonomous agents that recommend policy-compliant actions across finance, supply chain, and HR workflows. NetSuite's machine-learning accounts-payable module reduces manual invoice entry and speeds reconciliation, easing month-end close pressure. Manufacturers embed AI in plant-level modules for predictive maintenance, driving shorter unplanned downtime across the 95% of firms that already deploy smart-factory technologies. Healthcare providers leverage analytics to reconcile clinical and financial data, improving reimbursement accuracy and compliance reporting. All initiatives rely on robust governance because algorithmic bias or stale data can erode trust in automated decisions.

Comprehensive ERP projects absorb expenses that extend well beyond license or subscription fees. Data migration, business-process re-engineering, and staff training frequently double original budgets for hospitals and public agencies, as seen in multi-year modernizations at Baptist Health. SMEs rely on external consultants because they lack dedicated IT capacity, but scarce talent drives day-rates higher and stretches timelines. Cloud delivery softens capital expenditure yet does not eliminate the cultural shifts required for process standardization. Without robust change-leadership structures, expensive platforms risk under-utilization and diminished ROI.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud-native suites accounted for 60.5% revenue in 2024, ensuring the North America enterprise resource planning market retains a strong baseline of broad-function platforms. Social/collaborative ERP, however, will grow fastest at 11.4% CAGR through 2030 as corporations seek consumer-grade user experiences. Knowledge workers adopt activity feeds, shared dashboards, and real-time chat inside finance and supply-chain transactions, lifting system usage rates and shortening approval cycles. Integrated mobile apps deliver the same capabilities at job sites or customer locations, reinforcing always-connected workflows. Vendor roadmaps increasingly bundle social elements by default rather than as optional modules, underscoring their strategic value. Over time, artificial-intelligence assistants embedded in these channels will recommend actions or flag exceptions, deepening the linkage between engagement and operational efficiency.

Finance and accounting maintained 55.7% of the North America enterprise resource planning market size in 2024, reflecting mandatory reporting and audit requirements. Nonetheless, supply-chain and operations modules will expand at a 10.8% CAGR. Edge computing and the Internet of Things feed real-time shop-floor data into planning algorithms, improving material availability and lowering working capital. Predictive shipment ETAs support omnichannel commitments, while automated quality-checks cut return rates. Human-capital modules meanwhile gain priority as manufacturers confront labour shortages and rising voluntary turnover. Customer-commerce add-ons connect order capture to inventory, letting firms promise exact delivery windows that boost conversion rates. Finance still acts as the system-of-record, but operational datasets increasingly drive profit-and-loss outcomes.

The North America Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Industry Vertical (Manufacturing, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).