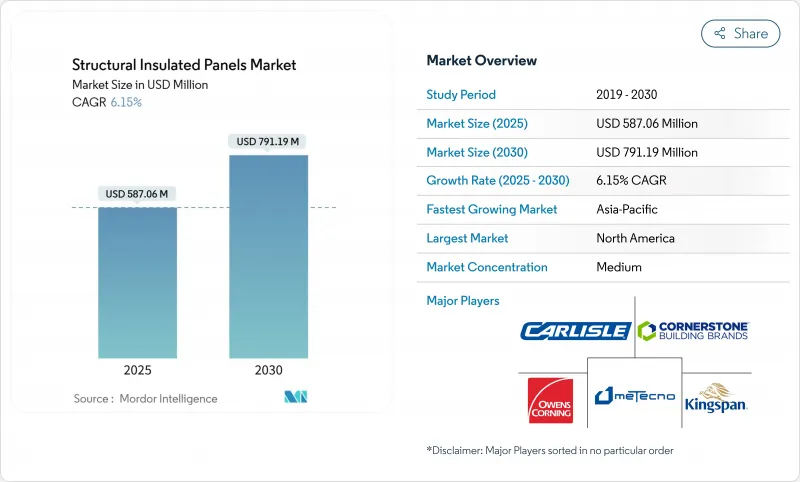

구조용 단열 패널 시장의 2025년 시장 규모는 5억 8,706만 달러로, 2030년에는 7억 9,119만 달러에 이를 것으로 예측되며, CAGR은 6.15%를 나타낼 전망입니다.

강한 기세는 에너지 효율 규제 강화, 조립식 가속화, 콜드체인 인프라 확대로 인한 것입니다. 북미가 규제면에서 주도권을 유지하는 한편, 아시아태평양은 급속한 도시화로 인해 가장 빠른 수량 증가를 기록합니다. 데이터센터 건설과 온도관리된 물류는 제품 혁신에 박차를 가하는 프리미엄 틈새를 엽니다. 한편, 배향성 스트랜드보드(OSB)공급 체인이 불안정하고 초기 비용이 높은 것이 폭넓은 보급을 방해하는 요인이 되고 있습니다.

2021년 국제 에너지 절약 기준(IECC)은 미국 연방 정부가 대출하는 주택의 성능 기준을 34.4% 늘렸습니다. 구조용 단열 패널 시장 진출기업은 SIP 벽과 지붕 조립품이 프레임을 변경하지 않고 규정 R 값을 충족하면서 공기 침입을 줄이기 때문에 이익을 얻고 있습니다. 콜로라도 주 IECC의 조기 도입은 이 국가의 에너지 코드 위원회가 SIP를 턴키 규정 준수 루트로 강조함으로써 주 의무가 즉시 재료 이동을 야기한다는 것을 입증합니다. 상업개발업자도 LEED 포인트를 확보하기 위해 SIP 외피에 주목하고 단독주택 이외 수요도 확대하고 있습니다.

콜드 스토어, 백신 저장소, 라스트마일 플루필먼트 센터는 높은 R 값의 연속 단열재가 필요합니다. PUR 및 PIR 코어 SIP는 빙점 하에서 사용하는 데 필요한 치수 안정성과 증기 장벽 특성을 갖추고 있어 기존 패널에 비해 25%의 에너지 절감이 가능합니다. 모듈식 냉장실은 공장에서 제조된 SIP를 활용하여 설치 시간을 40% 단축하고 아시아태평양 전역의 식료품, 의약품, 수산물 물류의 신속한 확장성을 지원합니다.

EPS 코어 SIP는 평균 1피트당 10-18달러이며 총 건축 비용에 대해 2-3%의 프리미엄이 걸립니다. 이는 에너지 요금 절감으로 5년 이내에 라이프사이클 회수가 가능함에도 불구하고 예산 중심 프로젝트를 저해하는 요인이 됩니다. 현재 미국에서 패널을 사용하고 있는 주택은 전체의 1-2%에 불과하고, 시공업체에 대한 인지도도 낮기 때문에 오해가 뿌리 깊습니다. 인플레이션억제법에 근거한 연방세제 우대조치로 인해 현재 차액의 일부는 상쇄되고 있지만, 신흥 시장의 가격에 대한 민감성은 여전히 판매량을 억제하고 있습니다.

EPS 패널은 2024년 매출의 79.87%를 차지하며, 건축업자가 보다 엄격한 법규제에 대응하기 위해 SIP 쉘을 채용하는 가운데, 이 재료의 비용·퍼포먼스의 밸런스의 좋은 점을 뒷받침했습니다. 구조용 단열 패널 시장 규모의 이 압도적인 점유율은 북미와 아시아태평양에서 안정적인 가격과 공급을 보장하는 EPS 생산 능력의 보급과 일치합니다. 또한 경량 보드는 운임을 줄이기 때문에 개발자는 크레인의 사용이 제한되는 지역의 토지를 이용할 수 있습니다.

2025년부터 2030년까지 EPS의 수량은 CAGR 6.29%로 성장할 것으로 구조용 단열 패널 시장은 예측했습니다. PUR/PIR 패널은 콜드 룸이나 클린 룸을 보호하는 것으로, 낮은 k값과 폐쇄 셀 강성이 높은 비용을 정당화합니다. 진공 단열과 에어로겔 코어의 개념은 넷 제로 프로토타입으로 유망시되고 있지만 가격과 취급의 복잡성에서 틈새에 머물고 있습니다. 이와 병행하여, 유리 울 코어는 음향 프로젝트를 유치하고 다기능 어셈블리를 요구하는 건축가를 위한 구조용 단열 패널 산업 툴킷의 폭을 넓히고 있습니다.

OSB 스킨은 2024년 구조용 단열 패널 시장 점유율의 57.28%를 차지하며, 프레이밍 작업자가 익숙하고 기존의 막대 벽에 사용된 패스너와의 호환성을 활용했습니다. 건축업자는 몸통 없이 직접 피복재를 설치할 수 있는 OSB의 나사 인발 강도를 높이 평가했습니다.

그러나 가이가람시에 의한 섬유 부족과 공장 화재가 공급 리스크를 부각시키고, 설계자를 스틸, 섬유 시멘트, 산화 마그네슘 스킨으로 향하게 하여, 2030년까지의 CAGR 성장률은 7.06%를 나타낼 전망입니다. 금속 페이싱은 불연성과 전자파 차폐가 중요한 데이터센터의 엔벨로프에 사용되며 MgO 보드는 습도가 높은 기후에서 내 곰팡이를 발휘합니다. 이러한 옵션은 조달을 다양화하지만, 복고풍 작업자는 공구와 패스너의 선택을 조정해야 하며 구조용 단열 패널 시장의 학습 곡선이 길어집니다.

북미는 2024년 세계 매출의 37.12%를 차지하며 미국이 그 중심이 되었습니다. 미국에서는 연방 정부 보증의 모기지에 IECC 2021이 채택되었으며 신축 주택의 주류는 SIP 수준의 성능이 되었습니다. 캐나다 제조업체들은 무역 관세 마찰에도 불구하고 국내 프레이머와 미국 프로젝트 모두에 제품을 공급하고 있으며, 이 지역의 추운 기후는 고내구성 어셈블리의 필요성을 높이고 있습니다. 버지니아, 텍사스 및 퀘벡에서는 데이터센터 건설이 급격히 진행되고 있으며 구조용 단열 패널 시장에 프리미엄 업스트림를 주입하고 있습니다.

아시아태평양의 2030년까지의 CAGR은 7.28%를 나타낼 전망입니다. 중국의 신축 바닥 면적 규제에는 집단 주택에서 SIP 사용을 촉진하는 그린 빌딩 비율이 포함되어 있으며, 인도의 스마트 시티 프로그램은 패널이 부지 회전을 촉진하는 모듈형의 저렴한 주택에 자금을 제공합니다. 현지 EPS수지 생산 능력과 경쟁력 있는 노동력으로 인해 납품되는 패널 비용이 낮아지고 소규모 개발업체들 사이에서도 도입이 진행되고 있습니다. 일본의 내진 기준은 경량성과 모멘트 프레임의 탄력성을 겸비한 목재와 스틸의 하이브리드 SIP 설계에 박차를 가해 건축에 널리 받아들여지고 있습니다.

유럽에서는 건물의 에너지 성능에 관한 지령에 힘입어 개수 예산을 외피 제1 전략으로 향하는 경향이 강해져 안정적인 수요가 유지되고 있습니다. 스칸디나비아의 건축업자는 크로스 라미네이트 재료를 EPS 코어와 통합하여 탄소 부정적인 모듈식 코티지를 제조합니다. 주요 3개 지역 이외에서는 중동이 지역 식량 안보를 위해 저온 저장 능력에 자금을 제공하고 칠레가 지진을 견디는 SIP 사회 주택의 프로토타입을 실험하고 있습니다.

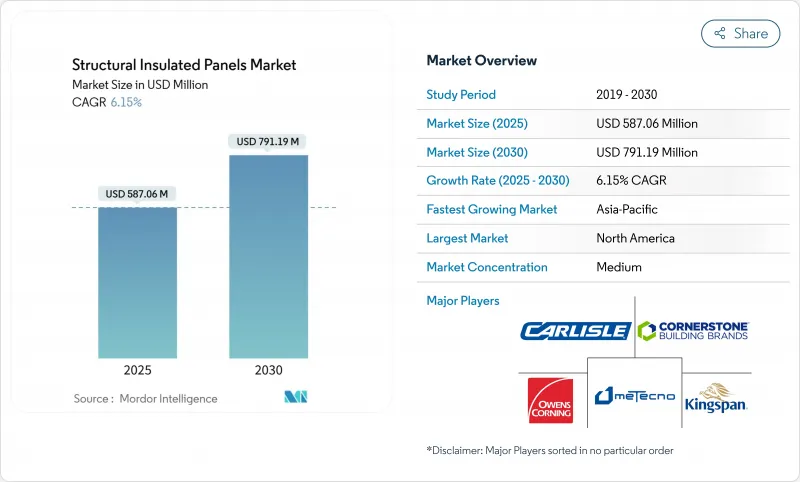

The structural insulated panels market is valued at USD 587.06 million in 2025 and is forecast to reach USD 791.19 million by 2030, advancing at a 6.15% CAGR.

Strong momentum stems from tighter energy-efficiency codes, accelerating prefabrication adoption, and expanding cold-chain infrastructure. North America retains regulatory leadership, while Asia-Pacific posts the fastest volume gains due to rapid urbanization. Data-center construction and temperature-controlled logistics open premium niches that spur product innovation. Meanwhile, supply-chain volatility for oriented strand board (OSB) and higher upfront costs remain near-term brakes on broad adoption.

Global building codes now prioritize lower operational carbon, and the 2021 International Energy Conservation Code (IECC) raises performance thresholds by 34.4% for federally financed housing in the United States. Structural insulated panels market participants benefit because SIP wall and roof assemblies cut air infiltration while meeting prescriptive R-values without additional framing changes. Colorado's early IECC adoption demonstrates how state mandates trigger immediate material shifts, with its Energy Code Board highlighting SIPs as a turnkey compliance route. Commercial developers also lean on SIP envelopes to secure LEED points, extending demand beyond single-family housing.

Cold stores, vaccine depots, and last-mile fulfillment centers require high-R-value continuous insulation. PUR and PIR-core SIPs offer the dimensional stability and vapor-barrier integrity needed for temperatures well below freezing, enabling 25% energy savings against conventional panels. Modular cold rooms leverage factory-fabricated SIPs to slash installation time by 40% and support rapid scalability for grocery, pharma, and seafood logistics across Asia-Pacific.

EPS-core SIPs average USD 10-18 per ft2, translating to a 2-3% premium on total build cost, which can deter budget-driven projects despite life-cycle payback within five years through lower energy bills. Misconceptions persist because only 1-2% of U.S. homes currently use panels, keeping installer familiarity low. Federal tax incentives under the Inflation Reduction Act now offset part of that delta, but price sensitivity in emerging markets still restrains volume.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

EPS panels held 79.87% of 2024 revenue, underlining the material's cost-performance balance as builders adopt SIP shells to comply with stricter codes. This dominant slice of the structural insulated panels market size aligns with widespread EPS manufacturing capacity, which ensures stable pricing and supply in North America and Asia-Pacific. Lightweight boards also reduce freight, letting developers tap rural lots with limited crane access.

Over 2025-2030, the structural insulated panels market expects EPS volumes to grow at 6.29% CAGR, supported by flame-retardant grades and recycled content innovations. PUR/PIR panels protect cold rooms and cleanrooms where lower k-values and closed-cell rigidity justify higher cost. Vacuum-insulated and aerogel-core concepts show promise in net-zero prototypes yet remain niche due to price and handling complexity. In parallel, glass-wool cores attract acoustic projects, broadening the structural insulated panels industry toolkit for architects seeking multifunctional assemblies.

OSB skins accounted for 57.28% of structural insulated panels market share in 2024, leveraging familiarity among framing crews and compatibility with fasteners used in conventional stick-built walls. Builders appreciate OSB's screw-withdrawal strength that supports direct cladding attachment without furring strips.

However, beetle-related fiber shortages and mill fires have spotlighted supply risk, nudging designers toward steel, fiber-cement, and magnesium-oxide skins growing at 7.06% CAGR through 2030. Metal facings serve data-center envelopes where non-combustibility and electromagnetic shielding matter, while MgO boards provide mold resistance in humid climates. These alternatives diversify procurement, although retrofit crews must adjust tooling and fastener choices, extending learning curves in the structural insulated panels market.

The Structural Insulated Panels Market Report Segments the Industry by Product (EPS (Expanded Polystyrene) Panels, Glass-Wool Panels, and More), Skin Material (Oriented Strand Board (OSB), Plywood, and More), Application (Building Wall, Building Roof, and More), End-User Industry (Residential, Commerical, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 37.12% of global revenue in 2024, anchored by the United States where IECC 2021 adoption for federally backed mortgages effectively makes SIP-level performance mainstream for new housing. Canadian manufacturers supply both domestic framers and U.S. projects despite trade-tariff friction, and the cold regional climate reinforces the need for high-R assemblies. Rapid data-center construction in Virginia, Texas, and Quebec injects a premium commercial stream into the structural insulated panels market.

Asia-Pacific logs the fastest regional CAGR at 7.28% to 2030. China's new-build floor-area quotas include green-building ratios that elevate SIP use in apartment blocks, while India's Smart Cities program funds modular affordable housing where panels accelerate site turnover. Local EPS resin capacity and competitive labor help keep delivered panel cost low, encouraging uptake even among smaller developers. Japan's seismic codes spur hybrid timber-steel SIP designs that pair light weight with moment-frame resilience, widening architectural acceptance.

Europe maintains stable demand underpinned by the Energy Performance of Buildings Directive, which increasingly channels renovation budgets into envelope first strategies. Scandinavian builders integrate cross-laminated timber skins with EPS cores to produce carbon-negative modular cottages, whereas Germany and the Netherlands drive public procurement toward low-embodied-carbon materials. Outside the big three regions, the Middle East funds cold-store capacity for regional food security, and Chile experiments with SIP social-housing prototypes that withstand seismic events.