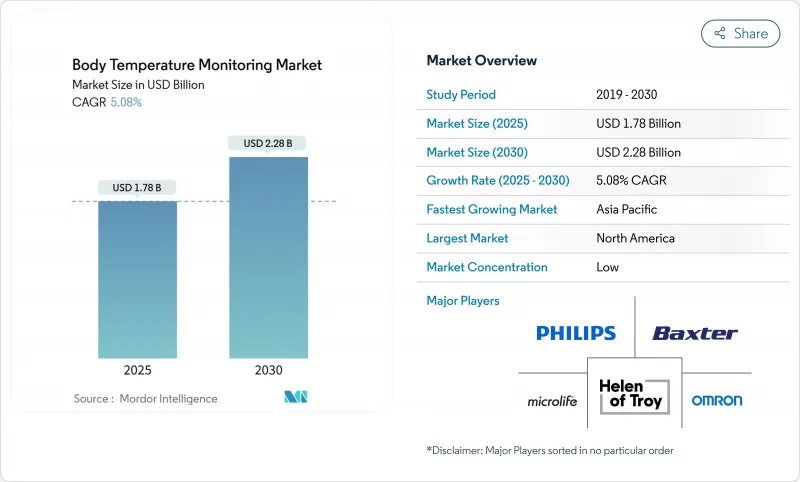

체온 모니터링 시장 규모는 2025년에 17억 8,000만 달러, 2030년에는 22억 8,000만 달러에 이르고, CAGR 5.08%를 나타낼 것으로 예측됩니다.

이 건전한 성장은 체온을 혈행 동태나 호흡기계의 데이터와 융합시키는 상시 접속의 IoT 대응 에코시스템으로 변화하고 있는 것을 반영하고 있습니다. 유행 시대의 스크리닝 루틴, 세계 인구의 고령화, 수은 기구를 단계적으로 폐지하는 규제상의 인센티브는 모두 수요를 자극하고 있습니다. 접촉형 장비는 정확도가 높고 임상적 신뢰를 유지하지만 비접촉 적외선(IR) 시스템과 웨어러블은 병원, 직장, 가정이 위생적이고 터치없는 워크플로우를 채택함에 따라 빠르게 확대되고 있습니다. 제조업체 각 회사는 수직 통합과 소프트웨어 제휴를 가속화하고 센서, 분석 및 클라우드 대시보드를 하나의 플랫폼에 통합하는 것을 목표로 하고 있습니다.

체온 검사는 병원, 학교, 기업 캠퍼스에서 현장의 위기 대응에서 영구적인 일상 업무로 전환되었습니다. 미국 식품의약국(FDA)은 대량의 온도 스크리닝 시스템의 성능에 관한 권고를 발표하고, 공공장소에서의 비접촉식 온도 스크리닝 시스템의 도입이 규제 당국에 받아들여지는 것을 시사했습니다. AI에 의해 강화된 캘리브레이션과 센서 퓨전(열 화상과 심박수 또는 SpO2 입력을 연결)으로 초기 팬데믹 기기에서 보인 위음성의 위험에 대처할 수 있게 되었습니다.

소형화된 서미스터, 보다 우수한 전력 관리 및 규제 완화된 경로는 지속적인 온도 추적을 소비자를 위한 웨어러블로 밀어 올렸습니다. Withings는 ScanWatch 2에 greenteg의 CALERA 센서를 통합하여 대량 판매 스마트 시계로 24시간 365일 핵심 체온 로깅을 가능하게 했습니다. 미국 FDA는 2025년 6월 일부 클래스Ⅱ의 임상용 전자체온계를 시판전 신고 대상에서 제외하고 발매 사이클 단축과 컴플라이언스 비용 절감을 실현했습니다.

검토를 받은 평가에 따르면, 일부 액형 적외선 온도계는 비관리 환경에서 임상 발열 스크리닝 임계값 아래로 -1°C 이상의 오류를 나타냅니다. 주변 온도, 습도 및 사용자 정렬로 인한 편차는 리콜 이벤트를 유발하고 병원 프로토콜의 레이어를 늘리므로 채택 속도가 떨어집니다. 공급업체는 교육, 자동 거리 타겟팅 및 다중 스펙트럼 모듈에 투자하고 있지만 표면 방사율의 기본 물리학은 저가 하드웨어의 오류 감소를 제한합니다.

2024년 체온 모니터링 시장의 62.58%는 접촉형이 차지했습니다. 특히 약제 투여나 패혈증의 감시로 0.2℃ 이하의 정밀도가 요구되는 경우, 이어 프로브, 디지털 봉상 체온계, 섭취 가능한 정제가 집중 치료 프로토콜을 지지하고 있습니다. 비접촉형 IR 장비는 감염 관리 지침 및 직장 배치 의무에 힘입어 2030년까지 가장 빠르게 성장하는 하위 카테고리가 될 것으로 예측됩니다. FDA가 승인한 Radius T0 및 종양학 시험에 사용되는 피부 패치와 같은 지속적인 웨어러블은 퇴원과 가정 요양의 교량을 수행하는 지속적인 측정으로의 전환을 보여줍니다. 장비 제조업체는 현재 침습적 치료를 위한 일회용 접점 프로브와 방문자 스크리닝을 위한 클라우드 연결형 IR 키오스크를 결합한 하이브리드 포트폴리오를 배치하고 있어 각 케어 현장에서 최적의 워크플로우를 선택할 수 있도록 되어 있습니다.

접촉형 프로브는 단순한 스틱형에 머무르지 않는 폭넓은 혁신을 지원합니다. 고급 급성기 병동에서는 중앙 간호 대시보드에 도킹된 케이블이 필요 없는 경구 프로브로 측정을 자동화하고 있습니다. 알고리즘 대응 데이터 스트림은 조기 패혈증 검출 모델과 투약 적정 엔진을 실현합니다. 한편, 광학계, 거리 대 스폿비, 주위 온도 보정에 있어서의 비접촉 시스템의 개선에 의해 일부 프리미엄 SKU에서는 정밀도 차이가 -0.4℃까지 축소되고 있습니다. 공급업체는 AI를 탑재하고 조준 불량이나 과도한 환경 드리프트에 플래그를 지정하여 사용자의 신뢰를 강화하고 대응 가능한 임상 사례를 확대하고 있습니다.

병원과 대규모 클리닉은 음미된 대행사에 의존하고 있으며 오프라인 채널을 통해 2024년 수익의 71.47%를 창출했습니다. 그룹 구매 조직은 체온계를 주입 펌프 및 모니터에 번들하여 임상적 증거 및 기술 서비스 계약을 제공하는 공급업체를 선호합니다. 오프라인 강도와는 달리, 체온 모니터링 시장은 소규모 클리닉과 일반 가정이 브랜드 사이트 및 마켓플레이스에 직접 주문함으로써 전자상거래의 급속한 보급을 목격하고 있습니다. 온라인 판매는 COVID-19의 폐쇄 기간 동안 급증하고 소비자가 셀프 케어의 역할을 받아들이면서 기세가 지속되었습니다. 신흥 소비자 직접 판매 브랜드는 데이터 대시보드, 앱 기반 코칭, 펌웨어 업데이트를 활용하여 가격 이외의 차별화를 도모하고 있습니다.

유통업체는 카탈로그를 디지털화하고 채우기 제어를 유지하는 클릭 및 수집 모델을 가능하게 함으로써 대응합니다. 제조업체는 구독 기반 펌웨어 분석을 시도하고 장치 배송에 추가하여 경상 수익을 창출합니다. 많은 기관 투자자들은 교정 증명서와 기술적인 서비스 교육을 필요로 하며 전자상거래 상점 프런트에서는 아직 대응할 수 없기 때문에 규제는 계속 오프라인 기반의 큰 기둥이 됩니다.

북미는 2024년 41.58%로 가장 규모가 큰 지역 점유율을 차지하며 성숙한 상환환경, 병원의 디지털화 프로그램, AI 대응 애널리틱스의 조기 도입이 혜택을 가져왔습니다. 학술의료센터와 OEM 간의 통합 파트너십은 온도, 혈중 산소 및 모션 데이터를 결합한 악화 사건을 예측하기 위해 다중 센서 플랫폼의 테스트 운영을 빠르게 진행하고 있습니다. 이 지역의 안정적인 CAGR 4.49%는 만성 질환의 유행과 지속적인 모니터링 하드웨어 상환을 하는 원격 케어 생태계의 확대에 지지되고 있습니다.

아시아태평양은 CAGR 5.75%로 가장 급성장하고 있는데 이는 중간층의 헬스케어에 대한 기대 증가와 스마트 병원에 대한 정부의 자극책 때문입니다. 중국 국내 제조업체들은 규모와 부품의 수직화를 활용하여 경제적 적외선 체온계를 수출 및 국내 채널로 출하합니다. 일본의 초고령화 사회가 재택 케어용 웨어러블의 보급을 촉진합니다. 인도의 디지털 건강 정책은 농촌 클리닉에서 원격 생체 사인 키트를 장려하고 체온 모니터링 시장의 밑단을 도시의 제 3 차 의료 센터 이외에도 확장합니다. 스마트폰의 보급률이 높아 앱 중심 디바이스의 사용자 온보드가 간소화되는 한편 다국적 브랜드가 합작투자를 설립해 이종 규제 방식을 극복합니다.

유럽은 2030년까지 연평균 복합 성장률(CAGR)이 4.83%로 견조한 궤도를 유지할 전망입니다. 엄격한 데이터 보호 규칙은 장치의 암호화와 로컬 게이트웨이 스토리지 솔루션을 촉진하여 환자 신뢰를 향상시킵니다. 미나마타 조약에 근거한 수은 디바이스의 금지가 진행되어, 디지털 및 IR 유닛의 교환 사이클이 가속합니다. 중동 및 아프리카는 CAGR 5.42%로 성장해 석유수입을 제3차 헬스케어 클러스터와 공공검진 인프라로 돌려줍니다. 순례와 같은 큰 이벤트는 신속한 비접촉식 스크리닝 포털에 대한 수요를 증가시킵니다. 남미는 CAGR 5.16%로 추이하고 있으며, 공적보험사가 기본적인 기기를 업그레이드하고 민간병원이 커넥티드 모니터링 스위트를 도입하고 있습니다. 환율 변동과 수입 관세는 가격 포지셔닝에 계속 영향을 미치며 가치 엔지니어링과 현지 조립 전략이 보상됩니다.

The body temperature monitoring market size stands at USD 1.78 billion in 2025 and is forecast to reach USD 2.28 billion by 2030, advancing at a 5.08% CAGR.

The healthy growth reflects a transformation from episodic thermometry toward always-on, IoT-enabled ecosystems that fuse temperature with hemodynamic and respiratory data. Pandemic-era screening routines, an aging global population, and regulatory incentives that phase out mercury devices all continue to stimulate demand. Contact devices retain clinical trust because of accuracy, but non-contact infrared (IR) systems and wearables expand quickly as hospitals, workplaces, and households embrace hygienic, touch-free workflows. Manufacturers accelerate vertical integration and software partnerships, aiming to bundle sensors, analytics, and cloud dashboards into one platform.

Temperature checks moved from ad-hoc crisis responses to permanent daily routines in hospitals, schools, and corporate campuses. The United States Food and Drug Administration issued performance recommendations for mass thermal screening systems, signaling regulatory acceptance of non-contact public venue deployment. AI-enhanced calibration and sensor fusion-linking thermal images with heart-rate or SpO2 inputs-now address the false-negative risk exhibited in early pandemic devices.

Miniaturized thermistors, better power management, and relaxed regulatory pathways have pushed continuous temperature tracking into consumer wearables. Withings integrated greenteg's CALERA sensor into ScanWatch 2, enabling 24/7 core body temperature logging in a mass-market smartwatch. In June 2025 the US FDA exempted select Class II clinical electronic thermometers from premarket notification, shortening launch cycles and lowering compliance cost.

Peer-reviewed evaluations show several forehead IR thermometers deviating by +-1 °C or more in uncontrolled environments, below clinical fever-screening thresholds. Variability from ambient temperature, humidity, and user alignment drives recall events and additional hospital protocol layers, tempering adoption pace. Suppliers invest in training, auto-distance targeting, and multi-spectral modules, yet fundamental physics of surface emissivity still limits error reduction in low-cost hardware.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The contact segment accounted for 62.58% of the body temperature monitoring market in 2024 thanks to proven accuracy and decades-long clinician familiarity. Ear probes, digital stick thermometers, and ingestible pills anchor intensive-care protocols, especially where medication dosing or sepsis surveillance requires sub-0.2 °C precision. Non-contact IR devices are forecast to be the fastest-growing sub-category through 2030, propelled by infection-control guidelines and workplace deployment mandates. Continuous wearables, such as FDA-cleared Radius T0 and skin patches used in oncology trials, illustrate a shift toward persistent measurement that bridges hospital discharge and home recovery. Device makers now position hybrid portfolios, pairing disposable contact probes for invasive procedures with cloud-connected IR kiosks for visitor screening, allowing each care setting to select the optimal workflow.

The contact segment's breadth supports innovation beyond simple sticks. High-acuity wards increasingly automate readings via cable-free oral probes docked in central nursing dashboards. Algorithm-ready data streams enable early sepsis detection models and medication titration engines. Meanwhile, non-contact system improvements in optics, distance-to-spot ratio, and ambient compensation have narrowed the accuracy gap to +-0.4 °C in some premium SKUs. Suppliers layer AI on board to flag poor aiming or excessive environmental drift, reinforcing user confidence and expanding addressable clinical cases.

Hospitals and large clinics rely on vetted distributors, generating 71.47% of 2024 revenue through the offline channel. Group purchasing organizations bundle thermometers with infusion pumps and monitors, favoring suppliers that offer clinical evidence and technical service contracts. Despite offline strength, the body temperature monitoring market witnesses rapid e-commerce uptake as small practices and households order direct from brand sites or marketplaces. Online sales surged during COVID-19 lockdowns and sustained momentum as consumers accepted self-care roles. Emerging direct-to-consumer brands leverage data dashboards, app-based coaching, and firmware updates to differentiate beyond price.

Distributors respond by digitizing catalogues and enabling click-and-collect models that preserve fulfillment control. Manufacturers experiment with subscription-based firmware analytics, creating recurring revenue on top of device shipments. Regulation continues to anchor a sizable offline base because many institutional buyers need calibration certificates and technical in-service training not yet matched by pure-play e-commerce storefronts.

The Body Temperature Monitoring Market Report is Segmented by Product (Contact [Digital Thermometers and More], Non-Contact [Non-Contact Infrared Thermometers and More], and More), Distribution Channel (Offline and Online), Application (Oral Cavity and More), End Users (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America delivered the largest regional share at 41.58% in 2024, benefiting from mature reimbursement environments, hospital digitization programs, and early adoption of AI-enabled analytics. Integration partnerships between academic medical centers and OEMs fast-track pilots for multi-sensor platforms that combine temperature, blood oxygen, and motion data to predict deterioration events. The region's stable 4.49% CAGR is underwritten by chronic disease prevalence and an expanding remote-care ecosystem that reimburses continuous monitoring hardware.

Asia-Pacific is the fastest-growing territory at 5.75% CAGR, linked to rising middle-class healthcare expectations and government stimulus for smart hospitals. China's domestic manufacturers leverage scale and component verticalization to ship economical IR thermometers into export and domestic channels. Japan's super-aged society drives home-care wearable uptake. India's digital-health policy encourages remote vital sign kits in rural clinics, broadening the body temperature monitoring market footprint beyond urban tertiary centers. High smartphone penetration simplifies user onboarding for app-centric devices, while multinational brands form joint ventures to navigate heterogeneous regulatory schemes.

Europe maintains a robust trajectory with a 4.83% CAGR to 2030. Stringent data-protection rules catalyze on-device encryption and local gateway storage solutions, improving patient trust. Mercury device bans progress under the Minamata Convention alignment, triggering accelerated replacement cycles for digital and IR units. The Middle East and Africa, growing at 5.42% CAGR, channels oil revenues into tertiary healthcare clusters and public screening infrastructure. Mass events such as pilgrimages amplify demand for rapid, non-contact screening portals. South America progresses at 5.16% CAGR as public insurers upgrade basic equipment and private hospitals install connected monitoring suites. Currency swings and import tariffs continue to influence price positioning, rewarding value engineering and local assembly strategies.