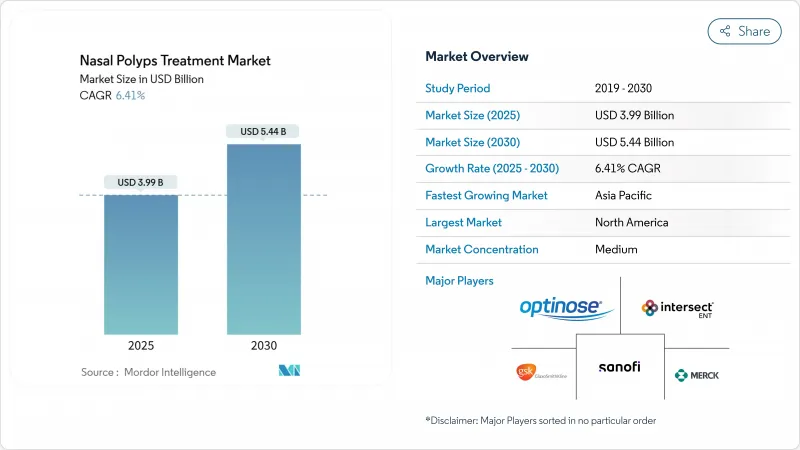

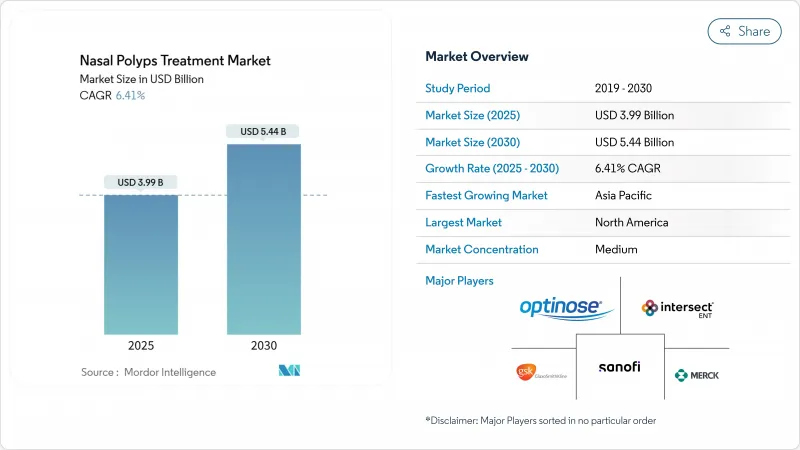

비용종 치료 시장 규모는 2025년에 39억 9,000만 달러로 평가되고, 2030년에는 54억 4,000만 달러에 이르고, CAGR 6.41%를 나타낼 것으로 예측됩니다.

의사가 광범위한 코르티코 스테로이드 사용에서 인터루킨 -4, -5, -13 신호 전달 경로를 차단하는 정확한 생물학적 제제로 이동함에 따라 수요가 증가하고 있습니다. 천식과 비용종을 동반한 만성 코 부비동염(CRSwNP)의 병존율 증가, 생물학적 제제의 신속 승인 확대, 비강내 약물 침착을 개선하는 저침습 전달 시스템의 꾸준한 보급으로 약물전달의 성장이 강화됩니다. 대형 제약 그룹이 라이프사이클 매니지먼트와 공동판촉 계약을 통해 시장 포지션을 지키는 한편, 중소 생명 공학 기업은 차별화된 작용기전에 의해 충분한 치료를 받지 않은 환자층을 타겟으로 하기 때문에 경쟁은 격화되고 있습니다. 디지털 약국 채널, 보다 광범위한 이비인후과 전문의 네트워크, 신흥국 시장의 유리한 상환 제도가 환자 접근을 더욱 확대하지만, 가격에 민감한 지역의 비용 억제 정책은 여전히 역풍입니다.

세계의 CRSwNP 유병률은 환경오염물질, 도시지역의 알레르겐, 고령화 등이 겹치면서 상승하여 세계 성인의 약 4%에 이환율이 높아지고 있습니다. 선진국 시장에서는 내시경 스크리닝의 보급에 의해 진단률은 향상되고 있지만, 신흥국에서는 이비인후과의 용량이 한정되어 있기 때문에 발견이 늦어지고 있습니다. CRSwNP 환자의 약 60%는 천식도 병발하고 있으며, 이환율을 높이고 증상의 관해가 오랫동안 지속되는 병용 요법의 필요성을 높이고 있습니다. 북미와 유럽의 납부자들은 수술의 재발과 스테로이드의 전신 사용으로 인한 경제적 부담을 이미 인식하고 있으며, 생물학적 제제의 조기 개입을 둘러싼 정책적 논의를 촉구하고 있습니다. 아시아태평양에서는 급속한 산업 확대로 대기 환경 문제가 심각해지고 있으며, 3차 병원의 건설과 함께 환자 수 증가가 현저합니다.

듀필루맙, 테제페르맙, 스타포키바트와 같은 표적 생물학적 제제는 비폐를 완화시키고, 폴립의 악성도를 낮추고, 수술률을 낮춥니다. 듀필루마브의 2024년 청소년 승인으로 미국에서 대상 환자 코호트는 약 9,000명 확대했습니다. 한편, 테제퍼맙의 3상 WAYPOINT 시험에서는 수술 개입이 98% 감소한 것으로 보고되어 경쟁 벤치마킹으로 자리매김했습니다. 의사는 생물학적 제형과 부신 피질 스테로이드 외용제를 병용하여 관리를 강화하는 경향이 있으며, 지불자는 노동 생산성 개선 및 응급 진찰 감소가 입증되면 보상을 지불합니다. 2024년 중국에서 승인된 스타포키바트는 아시아태평양에서 프리미엄 생물학적 제제의 보급을 위한 포석으로 현지 혁신을 위한 전략적 움직임을 보여줍니다. 현재 진행중인 직접 비교 시험은 종단형별 포지셔닝을 정교하게 하고 생물학적 제형 부문 내에서 점유율 이동을 진행할 것으로 보입니다.

미국에서는 듀필마브의 연간 치료비가 3만 달러를 넘어 치료 기간을 장기화시키는 사전 승인의 장애물을 도입하도록 민간 지불자에게 압력을 가하고 있습니다. 비용효과 연구는 생물학적 제형이 질 조정 생존년(QOL)에서 전신성 스테로이드 제형을 초과하는 것으로 나타났지만, 의료 보험 제도에 대한 예산적 영향은 여전히 크며, 특히 확대되는 전문 약제의 파이프라인에 추가되는 경우는 더욱 그렇습니다. 중저소득 국가에서는 생물학적 제제의 사용이 도시 지역의 자기 부담 엘리트에 국한되는 경우가 많으며 공정성 격차가 커지고 있습니다. 2028년 이후 바이오시밀러 의약품 진입으로 가격 경쟁이 완화될 수 있지만, 지급자는 전문 약물에 대한 지출 증가를 억제하기 때문에 엄격한 리베이트를 협상할 것으로 보입니다. 주사훈련과 파마코비질런스를 포함한 부수비용은 스튜어드십 주도의 상환제도에서 보편적 보험 적용을 더욱 복잡하게 하고 있습니다.

부신 피질 스테로이드는 유리한 가격 설정과 처방자에 대한 광범위한 침투를 배경으로 2024년 비용종 치료 시장에서 42.34%의 점유율을 유지했습니다. 그러나 '약제 클래스별'의 생물학적 제제는 확실한 실임상 효과와 멀티 코호트 라벨 연장에 밀려 CAGR 8.54%로 확대되고 있습니다. 항생제의 사용량은 감염에서 2형 염증으로 메커니즘이 이동함에 따라 감소하고 있습니다. 류코트리엔 변형제는 천식을 동반하는 환자를 대상으로 하는 틈새 약물이지만, 폴립의 퇴축에 있어서 단독으로의 효과는 한정적입니다.

경쟁 조류는 병원 처방에도 나타나고 수술 위험이 높은 코호트에서 생물학적 제제의 사용률은 전 분기 대비 상승했습니다. 듀필루맙의 사춘기 적응, 테제페르맙의 승인 가까이의 상황, 중국의 스타포키바트 우에시는 재수술과 스테로이드의 누적 투여량을 줄이는 질환 개질 작용에 대한 관심을 강화하고 있습니다. 지불자의 모니터링은 엄격해지고 있지만, 수술실에서의 에피소드 감소와 생산성 향상으로 인한 장기적인 비용 상쇄는 생물학적 제형의 가치 이야기를 강화하고 있습니다. 2028년 이후 바이오시밀러의 파도는 차세대 사이토카인 타겟 기술 혁신의 인센티브를 유지하면서 점차 액세스의 무결성을 풀어야 합니다.

점비약은 2024년에 48.43%의 매출 점유율을 달성했으며, 환자 친화적인 투약 형태와 경증에서 중등도의 증상을 관리하는 시판되는 스테로이드 약물의 선택으로부터 혜택을 받았습니다. XHANCE의 폐쇄 구개 메커니즘으로 대표되는 호기 전달 시스템은 부비동에 대한 보다 깊은 침투와 폴립 축소 점수의 향상이 연구에 의해 확인되어 2030년까지 연평균 복합 성장률(CAGR) 8.66%를 나타낼 전망입니다. 경구 및 주사 경로는 특히 급성 악화 및 2-8주마다 생물학적 제형 투여와 같은 전신 치료에 계속 유효합니다. SINUVA와 LATERA로 대표되는 이식 가능한 장치는 장기적인 안전성 데이터 획득을 기다리는 조기 적용의 틈새 분야입니다.

새로운 솔루션은 휴대용 배터리 분무기와 클라우드 포털에 투여 규정 준수를 기록하는 센서를 결합하여 의사의 원격 모니터링을 지원합니다. 스트라이커의 LATERA 흡수성 임플란트는 적절한 측벽 붕괴 사례에서 기능적 내시경 부비동 수술과 비교하여 환자 1인당 USD 2,200을 절약할 것으로 보고되었습니다. 이러한 임플란트의 보급은 국가마다 다르며, 전문의의 스킬셋과 상환 스케줄에 달려 있습니다. 장비 제조업체가 인체 공학을 개선하고 디지털 지침을 통합함에 따라 지불자는 집중적인 수술 에피소드를 줄일 수있는 이러한 기술을 지원할 수 있습니다.

2024년 비용종 치료 시장은 북미가 42.45%의 점유율로 선도했습니다. FDA 인가 생물 제제의 왕성한 처방, 전문 약 보험 적용의 보급, 조기 진단을 촉진하는 활발한 환자 지원 단체에 지지되고 있습니다. 미국은 실시간 베네핏 체크와 제조업체의 자기부담금 프로그램을 활용하여 고가의 정가를 상쇄함으로써 이 지역의 수익의 대부분을 차지하고 있습니다. 캐나다의 각 주의 약제 계획은 의료 기술 평가에 따라 생물 제제를 꾸준히 수식에 추가하고 있으며, 멕시코에서는 민간 보험 풀의 확대에 의해 부신 피질 스테로이드 스프레이와 풍선 부비강 성형술의 도입이 가속화되고 있습니다. 현재 진행 중인 지불자 협상으로 인해 액세스가 다양화되고 있지만, 상업 기반의 꾸준한 섭취로 인해 이 지역의 리더십은 흔들리지 않게 되었습니다.

유럽은 균형 잡힌 성장을 보여 주며, EMA에 의한 심사의 일원화가 다국적 제제의 우에시를 효율화하고 있습니다. 독일과 영국은 임상연구망을 정비하고 엄격한 비용효과 기준을 채용함으로써 생물학적 제제의 상환을 위한 입찰 경쟁과 리스크 분담 계약을 가속화하고 있습니다. 프랑스와 이탈리아는 전문의 의양 프로그램과 국민 모두 보험 제도의 혜택을 받아 수술의 순서 대기를 짧게 해, 생물학적 제제의 채용을 안정시키고 있습니다. 스페인은 제3차 이비인후과의 정비가 진행되고, 거시경제가 개선되고 있기 때문에 수술건수에 크게 공헌하는 나라로서 대두되고 있습니다. EU의 인구동태 고령화와 직장의 웰빙 의무화는 장기적인 수요를 지원합니다.

아시아태평양은 헬스케어 지출 확대, 인프라 현대화, 환자 의식 향상과 함께 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 7.45%를 나타낼 것으로 예측됩니다. 중국 스태포키바트의 승인은 국내 혁신의 획기적인 사건으로 지역적으로 경쟁력 있는 가격대에서 현지 생산되는 모노크로날로의 문을 열었습니다. 일본의 강력한 혁신 자금과 단일 보험 제도의 틀은 생물학적 제제의 높은 보급률을 지원하며 호주와 한국은 구미 채용 곡선을 반영합니다. 인도에서는 이비인후과의 노동력 부족이 여전히 제약이 되고 있지만, 원격의료와 비감염성 질환에 대한 정책의 중점화에 의해 지난 10년 후반에는 잠재 수요가 발굴될 가능성이 있습니다. 도시와 농촌의 격차는 앞으로도 계속될 것이지만, 공립 병원의 수용 능력의 점진적 확대와 민간 보험의 보급에 의해 치료에의 액세스는 확대할 것으로 보입니다.

The nasal polyps treatment market size is valued at USD 3.99 billion in 2025 and is forecast to reach USD 5.44 billion by 2030, advancing at a 6.41% CAGR.

Demand is rising as physicians shift from broad corticosteroid use toward precision biologics that interrupt interleukin-4, -5 and -13 signaling pathways. Growth is reinforced by the high coexistence of asthma and chronic rhinosinusitis with nasal polyps (CRSwNP), the expansion of fast-track biologic approvals, and steady uptake of minimally invasive delivery systems that improve intranasal drug deposition. Competition intensifies as large pharmaceutical groups protect market positions through life-cycle management and co-promotion agreements, while smaller biotechnology companies target under-served patient segments through differentiated mechanisms of action. Digital pharmacy channels, broader ENT specialist networks, and favorable reimbursement pilots in developed markets further expand patient access, although cost containment policies in price-sensitive regions remain a headwind.

Global CRSwNP prevalence is climbing as environmental pollutants, urban allergens, and ageing populations converge, raising disease incidence to roughly 4% of adults worldwide. Diagnosis rates improve in developed markets thanks to widespread endoscopic screening, but limited ENT capacity in emerging regions delays detection. About 60% of CRSwNP patients also have asthma, compounding morbidity and increasing the need for combination therapies that deliver longer-lasting symptom remission. North American and European payers already recognize the economic burden of recurrent surgeries and systemic steroid use, prompting policy discussions around earlier biologic intervention. In Asia-Pacific, rapid industrial expansion intensifies air-quality issues, which, together with the build-out of tertiary hospitals, is generating a pronounced uptick in patient volumes.

Targeted biologics such as dupilumab, tezepelumab, and stapokibart ease nasal obstruction, reduce polyp grade, and lower surgery rates, prompting guideline updates that prioritize their use in refractory CRSwNP. Dupilumab's 2024 adolescent approval broadened the eligible U.S. cohort by about 9,000 patients, while tezepelumab's Phase III WAYPOINT trial reported a 98% cut in surgical interventions, positioning it as a competitive benchmark. Physicians increasingly combine biologics with topical corticosteroids to consolidate control, and payers reward documented improvements in work productivity and reduced emergency visits. China's stapokibart authorization in 2024 signaled a strategic move toward local innovation, setting the stage for wider Asia-Pacific penetration of premium biologics. Ongoing head-to-head trials will likely refine positioning by endotype, driving incremental share shifts within the biologics segment.

Annual dupilumab therapy exceeds USD 30,000 in the United States, placing pressure on commercial payers to deploy prior-authorization hurdles that elongate treatment timelines. Cost-effectiveness studies show biologics outperform systemic steroids in quality-adjusted life-years, yet budget impact for health plans remains substantial, particularly when layered on top of expanding specialty drug pipelines. In lower-middle-income economies, biologic usage is often limited to self-pay urban elites, widening equity gaps. Biosimilar entry after 2028 may ease price tension, but payers will still negotiate steep rebates to curb specialty spending growth. Ancillary costs, including injection training and pharmacovigilance, further complicate universal coverage in stewardship-driven reimbursement systems.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Corticosteroids retained 42.34% share of the nasal polyps treatment market in 2024 on the back of favorable pricing and wide prescriber familiarity. Yet biologic therapies within the "Other Drug Class" bracket are expanding at an 8.54% CAGR, propelled by robust real-world effectiveness and multi-cohort label extensions. Antibiotic usage is falling as mechanistic focus shifts from infectious to type 2 inflammatory drivers. Leukotriene modifiers remain niche, serving patients with comorbid asthma yet limited standalone benefit in polyp regression.

The competitive tide is evident in hospital formularies, where biologic utilization in high-surgery-risk cohorts is rising quarter-on-quarter. Dupilumab's adolescent indication, tezepelumab's near-approval status, and China's stapokibart launch intensify attention on disease-modifying results that reduce revision surgeries and cumulative systemic steroid exposure. Payer scrutiny is tightening but long-term cost offsets from fewer operating-room episodes and productivity gains strengthen the biologic value narrative. Post-2028 biosimilar waves should gradually unlock fuller access while sustaining innovation incentives for next-generation cytokine targets.

Nasal sprays delivered 48.43% revenue share in 2024, benefiting from patient-friendly formats and over-the-counter steroid options that manage mild-to-moderate symptoms. Exhalation delivery systems, led by XHANCE's closed-palate mechanism, are on track for an 8.66% CAGR by 2030 as studies confirm deeper sinus penetration and better polyp shrinkage scores. Oral and injectable routes remain relevant for systemic treatments, especially during acute exacerbations or for biologic dosing every 2-8 weeks. Implantable devices, exemplified by SINUVA and LATERA, occupy an early-adopter niche awaiting further long-term safety data.

Emerging solutions combine handheld battery-assisted atomizers with sensors that log dosing compliance to cloud portals, supporting remote physician oversight. Stryker's LATERA absorbable implant reportedly saves USD 2,200 per patient compared with functional endoscopic sinus surgery in suitable lateral wall collapse cases. Uptake of such implants remains country-specific, hinging on specialist skill sets and reimbursement scheduling. As device makers refine ergonomics and integrate digital guidance, payers may favor these technologies for their potential to lower intensive surgical episodes.

The Nasal Polyps Treatment Market Report is Segmented by Drug Class (Corticosteroids, Antibiotics, and More), Route of Administration (Nasal Sprays, Oral Tablets & Suspensions, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), End User (Hospitals, and More), Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led the nasal polyps treatment market in 2024 with 42.45% share, underpinned by strong prescribing of FDA-cleared biologics, widespread insurance coverage for specialty drugs, and active patient advocacy groups that facilitate early diagnosis. The United States accounts for the bulk of regional revenue, leveraging real-time benefits checks and manufacturer copay programs that offset high list prices. Canada's provincial drug plans steadily add biologics to formularies following health-technology assessments, while Mexico's growing private insurance pool is accelerating corticosteroid spray and balloon sinuplasty uptake. Ongoing payer negotiations create heterogeneous access, yet steady commercial uptake has cemented the region's leadership.

Europe shows balanced growth, supported by centralized EMA reviews that streamline multinational launches. Germany and the United Kingdom anchor clinical research networks and employ stringent cost-effectiveness thresholds, accelerating tender competition and risk-sharing contracts for biologic reimbursement. France and Italy benefit from specialist training programs and universal coverage, keeping surgery queues short and biologic adoption steady. Spain, with upgraded tertiary ENT hubs and improving macroeconomics, is emerging as a significant volume contributor. EU aging demographics and stringent workplace wellness mandates sustain long-term demand.

Asia-Pacific is projected to achieve the fastest 7.45% CAGR through 2030 as healthcare spending expands, infrastructure modernizes, and patient awareness rises. China's stapokibart approval marked a milestone in domestic innovation and opened the door for locally produced monoclonals at regionally competitive price points. Japan's robust innovation funding and single-payer insurance framework support high biologic penetration, while Australia and South Korea mirror Western adoption curves. India's ENT workforce shortfall remains a constraint, though tele-medicine and policy emphasis on noncommunicable diseases could unlock latent demand later this decade. Urban-rural disparities will persist, but incremental expansion of public hospital capacity and private insurance penetration is set to widen treatment access.