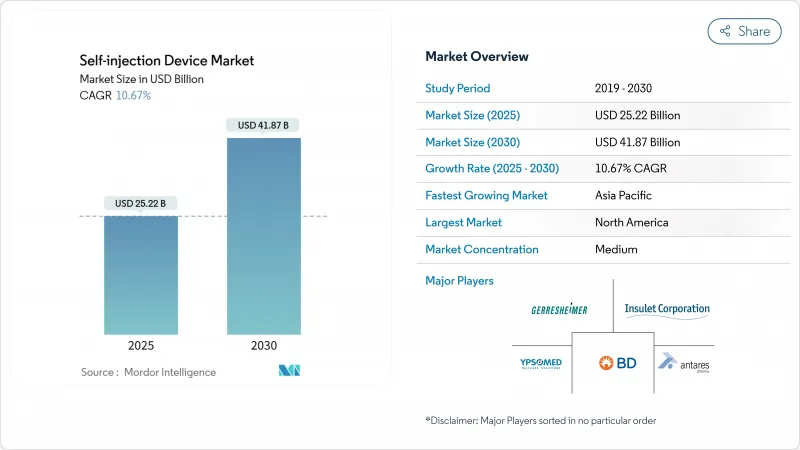

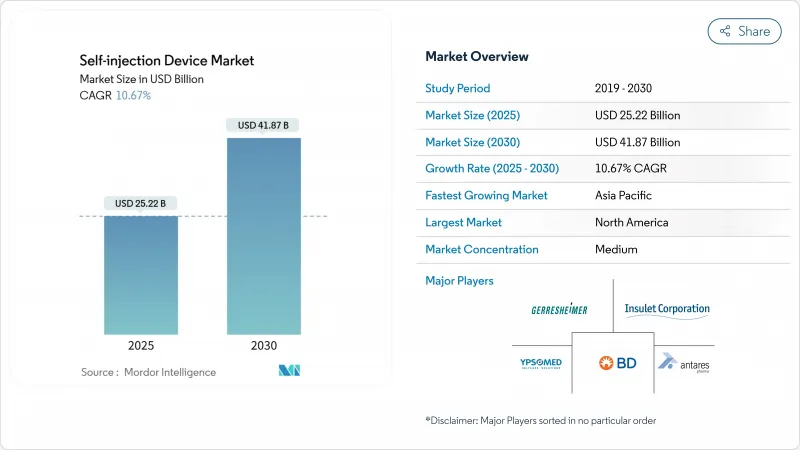

자가 주입 장치 시장 규모는 2025년 252억 2,000만 달러로 평가되었고, CAGR은 10.67%를 나타낼 것으로 예측되며 2030년에 418억 7,000만 달러에 이를 전망입니다.

성장은 세 가지 기둥에 기반합니다. 만성 질환 유병률을 높이는 인구 고령화, 환자 중심 전달 방식으로의 바이오의약품 전환, 그리고 치료를 저비용 환경에서 유지하라는 지불자의 압력입니다. 제약사, 의료기기 전문업체, 계약제조업체들은 글루카곤 유사 펩타이드-1(GLP-1) 치료제, 항암제 및 가정 내 투여용으로 개발된 기타 생물학적 제제의 생산 능력을 확대하고 있으며, 이는 첨단 주사 플랫폼에 대한 지속적인 수요를 시사합니다. 규제 조화 및 특히 미국 식품의약국(FDA)의 복합 제품에 대한 간소화된 승인 절차와 유럽연합(EU)의 진화하는 의료기기 규정(MDR) 및 은 승인 주기를 단축하고 의료기기 개선을 촉진합니다. 한편, 바이오시밀러 출시로 인해 과거 주입 센터에서만 사용 가능했던 분자들에 대한 접근성이 확대되면서 치료 장소가 환자의 가정으로 더욱 이동하고 있습니다. 노보 노디스크의 노스캐롤라이나 주 41억 달러 규모 공장 프로그램과 2024년 12월 FDA의 히크마 리라글루타이드 바이오시밀러 승인은 현재 확장을 뒷받침하는 대규모 생산 능력 구축과 저렴한 대체재라는 두 가지 동력을 요약합니다.

5억 3,700만 명 이상의 성인이 당뇨병을 앓고 있으며, 암 발병률은 2000년 이후 47% 증가했습니다. 이러한 수치는 가정 내 주사 치료에 대한 지속적인 수요를 창출합니다. 2024년 8월 인슐릿(Insulet)의 스마트어저스트(SmartAdjust) 승인은 시설 부담을 줄이면서 다중 질환 관리를 가능하게 하는 자동화 인슐린 전달 플랫폼에 대한 규제 당국의 지지를 보여줍니다. 제약 파이프라인은 이제 동반 질환을 해결하는 약제들을 단일 고점도 제형으로 묶어 연결된 자가 주입 장치를 통해 투여 가능하게 함으로써, 치료 순응도를 개선하고 지불 주체가 부담하는 비용을 억제하고 있습니다. 유럽, 북미 및 아시아 일부 지역의 고령화 인구 구조는 이 촉진요인의 장기적 영향을 증폭시킵니다.

팬데믹 시대의 원격의료 경험은 사생활 보호와 유연성을 제공하는 자가 투여 도구에 대한 수요를 강화했습니다. 코헤러스 바이오사이언스의 '우데니카 온바디(UDENYCA ONBODY)'는 2024년 2월 출시되어 중성구감소증 환자가 페그필그라스팀 투여를 위해 두 번째 병원 방문을 피할 수 있게 했습니다. 블루투스 지원 펜 주입 장치를 통한 실시간 복약 모니터링 및 투여량 피드백은 안전성 우려를 완화하고, 병원 외부로 치료를 전환하려는 보험사 요구와 부합합니다. 디지털 인터페이스에 익숙한 젊은 세대는 이제 연결형 장치를 프리미엄 기능이 아닌 표준으로 기대하며, 이는 중기 성장을 뒷받침합니다.

유럽 의회가 2024년 10월 MDR(의료기기 규정) 마감일 수정을 표결한 사례는 인증 지연이 제품 출시를 지연시키고 준수 비용을 부풀릴 수 있음을 보여주었습니다. 글로벌 출시 복합 제품의 경우 이 비용이 5천만 달러를 초과할 수 있습니다. FDA는 체내 주입 장치를 특별 성능 관리 대상인 Class II 기기로 분류하여 설계 검증 단계를 추가함으로써 승인 기간을 18개월까지 연장시킬 수 있습니다. 소규모 혁신 기업들은 지역별 동시 제출을 위한 자본이 부족한 경우가 많아, 전담 규제 팀을 보유한 대기업들의 영향력이 강화되고 있습니다.

펜 주입 장치는 성숙한 제조 인프라와 의료진의 친숙도에 힘입어 2024년 자가 주입 장치 시장 점유율 47.67%를 차지하며 가장 높은 매출을 기록했습니다. 펜 주입 장치 시장 규모는 2030년까지 연평균 8.4%의 안정적인 성장률로 189억 달러에 달할 것으로 전망됩니다. 그러나 생물학적 제제의 농도와 용량이 증가함에 따라 웨어러블 주입 장치는 12.56%의 성장률로 다른 모든 제품군을 앞지르고 있습니다. 스테바나토 그룹의 버티바(Vertiva) 온바디 시스템은 수 분에 걸쳐 최대 10mL를 투여할 수 있어, 기존 정맥 주입에 의존하던 항암 및 희귀질환 치료에 활용될 전망입니다. 자가 주입 장치는 아달리무맙과 에타너셉트의 바이오시밀러 여과 기술이 일차 진료로 확대되면서 여전히 탄탄한 하위 부문으로 자리매김하고 있습니다. 바늘 없는 장치는 기술적으로 매력적이지만, 가격 및 규제 장벽으로 인해 즉각적인 영향력은 제한적입니다.

혁신의 두 번째 물결은 기기 연결성에 집중됩니다. 웨어러블 펌프 내 블루투스 모듈은 투여 기록을 클라우드 대시보드로 전송해 의료진에게 세밀한 복약 준수 현황을 제공합니다. 제약사들은 이제 치료 패키지 차별화와 의료기술평가를 위한 실세계 증거 수집을 위해 기기에 앱을 번들로 제공합니다. 데이터 아키텍처가 핵심 요소로 부상함에 따라 기기 제조사들은 기계 공학 역량과 함께 사이버 보안 역량을 구축해야 하며, 이는 신규 진입자의 진입 장벽을 높이고 소프트웨어와 하드웨어 팀 간 협업 필요성을 증대시킵니다.

북미는 강력한 보험 적용, 높은 생물학적 제제 보급률, 조기 연결형 기기 도입 덕분에 2024년 글로벌 매출의 38.54%를 차지했습니다. BD의 주입 장치 배럴 생산 능력 확대와 FDA의 디지털 헬스 추가 기능에 대한 명확한 지침에 힘입어, 해당 지역의 자가 주입 장치 시장 규모는 2030년까지 연평균 9.2% 성장할 전망입니다. 캐나다의 의료 기술 평가는 치료 순응도 향상을 위해 연결형 자동 주입 장치를 점점 더 많이 승인하고 있으며, 멕시코의 마킬라도라(maquiladora) 공장 확장은 미국으로의 수출을 위한 비용 효율적인 생산 통로를 창출하고 있습니다.

아시아태평양 지역은 연평균 11.56% 성장률을 기록하며, 중국 국가의약품감독관리국(NMPA)의 승인으로 가속화되고 있습니다. NMPA는 2024년 12,213개 기기를 승인했으며, 이는 현지 제조업체들이 글로벌 공급망으로 진출하는 관문 역할을 합니다. 인도의 계약개발조직(CDO)들은 유럽 제약사와 협력하여 GLP-1 펜 전용 충전·완성 라인을 구축함으로써 리드 타임과 비용을 단축하고 있습니다. 일본, 한국, 호주는 성숙한 보험급여 제도와 고령화 인구가 결합되어 고급형 연결형 기기에 대한 즉각적인 수요를 창출하고 있습니다.

유럽은 MDR(의료기기 규정) 준수 비용이 중소 기업을 제약하는 가운데, 다국적 출시를 단순화하는 통합 규정이 적용되며 중간 단일자리 수 성장률을 유지하고 있습니다. 독일의 건강보험 기금은 지불자 위험을 제한하는 성과 기반 계약과 연계될 경우 전기기계식 펜의 보험급여를 인정합니다. 영국 국립보건임상연구원(NICE)은 연결형 자가 주입 장치로 생성된 실제 세계 증거를 비용효과성 자료에 포함하도록 권고했으며, 이는 유럽연합 전역에서 디지털 기술의 광범위한 채택을 촉진할 것으로 예상됩니다. 동유럽 시장은 여전히 가격에 민감하지만, 서유럽 대비 더 빠른 속도로 바이오시밀러 아달리무맙용 일회용 펜을 도입하고 있습니다.

남미와 중동 및 아프리카는 아직 초기 단계에 있지만, 만성질환 발생률 증가와 공공 부문 조달 개혁으로 향후 10년간 수요가 증가할 전망입니다. 브라질 국가 예방접종 계획은 이미 종양학 바이오시밀러 지원을 위해 3mL 프리필드 장치 예산을 배정했으며, 사우디아라비아의 ‘비전 2030’ 의료 정책은 환자 중심 장치의 등록 절차를 신속 처리하고 있습니다.

The self-injection devices market size stood at USD 25.22 billion in 2025 and, on the strength of a 10.67% compound annual growth rate (CAGR), is forecast to reach USD 41.87 billion by 2030.

Growth rests on three pillars: population aging that drives chronic disease prevalence, the biopharmaceutical shift toward patient-centric delivery formats, and payer pressure to keep treatment in lower-cost settings. Pharmaceutical producers, device specialists, and contract manufacturers are expanding capacity for glucagon-like peptide-1 (GLP-1) therapies, oncology drugs, and other biologics formulated for at-home administration, signalling durable demand for advanced injection platforms. Regulatory harmonisation-in particular the United States Food and Drug Administration's streamlined pathways for combination products and the European Union's evolving Medical Device Regulation (MDR)-shortens approval cycles and spurs device iteration. Meanwhile, biosimilar launches are widening access to molecules once confined to infusion centres, further shifting the point of care to the patient's home. Novo Nordisk's USD 4.1 billion factory programme in North Carolina and the FDA clearance of Hikma's liraglutide biosimilar in December 2024 encapsulate the dual forces of large-scale capacity build-out and affordable alternatives that underpin the current expansion.

More than 537 million adults live with diabetes and cancer incidence has climbed 47% since 2000; these figures create a sustained pull for at-home injection therapies. Insulet's SmartAdjust clearance in August 2024 illustrates regulators' support for automated insulin delivery platforms that lower facility pressure while enabling multidisease care. Pharmaceutical pipelines now bundle agents addressing comorbidities into single high-viscosity formulations deliverable via connected autoinjectors, improving adherence and containing costs borne by payers. Ageing demographics in Europe, North America, and parts of Asia amplify the long-run influence of this driver.

Pandemic-era exposure to telehealth strengthened demand for self-administration tools that offer privacy and flexibility. Coherus BioSciences' UDENYCA ONBODY came to market in February 2024, letting neutropenia patients avoid a second clinic visit for pegfilgrastim. Real-time adherence monitoring and dosing feedback delivered through Bluetooth-enabled pen injectors lessen safety concerns and align with payers' desire to shift care outside hospitals. Younger cohorts comfortable with digital interfaces now expect connected devices as standard rather than premium features, supporting mid-term growth.

The European Parliament's October 2024 vote to revise MDR deadlines showed how certification backlogs can stall product introductions and inflate compliance costs, which can top USD 50 million for a globally launched combination product. The FDA treats on-body injectors as Class II devices subject to special performance controls, adding design-verification layers that can lengthen timelines by 18 months. Smaller innovators often lack the capital for parallel submissions across regions, consolidating power among larger companies with dedicated regulatory teams.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Pen injectors generated the highest revenue, holding 47.67% self-injection devices market share in 2024, supported by mature manufacturing infrastructure and clinician familiarity. The self-injection devices market size for pens is projected to reach USD 18.9 billion by 2030 at a steady 8.4% CAGR. Wearable injectors, however, outpace every other product class at a 12.56% rate as biologic concentrations and volumes rise. Stevanato Group's Vertiva on-body system dispenses up to 10 mL over several minutes, lending itself to oncology and rare-disease regimens once limited to intravenous infusion. Auto-injectors remain a resilient sub-segment, buoyed by biosimilar filtration of adalimumab and etanercept into primary care. Needle-free devices, although technologically compelling, still confront price and regulatory hurdles that curb immediate impact.

A second wave of innovation focuses on device connectivity. Bluetooth modules in wearable pumps transmit dosing logs to cloud dashboards, giving physicians granular adherence visibility. Pharmaceutical firms now bundle apps with devices to differentiate therapy packages and gather real-world evidence for health-technology assessments. As data architecture becomes integral, device makers are forced to build cybersecurity competencies alongside mechanical engineering capabilities, raising entry barriers for new entrants and intensifying collaboration needs between software and hardware teams.

The Self-Injection Device Market Report is Segmented by Product (Pen Injectors, Auto-Injectors, Wearable Injectors, and Needle-Free Injectors), Usage (Disposable and Re-Usable), Application (Diabetes & Other Hormonal Disorders, Auto-Immune Diseases, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.54% of global revenue in 2024 thanks to robust reimbursement, high biologic penetration, and early connected-device adoption. The region's self-injection devices market size is on track to grow 9.2% per year through 2030, supported by BD's expanded syringe-barrel capacity and the FDA's clear guidance on digital-health add-ons. Canada's health-technology assessments increasingly endorse connected autoinjectors for adherence improvement, while Mexico's maquiladora site expansions create a cost-efficient production corridor for export into the United States.

Asia-Pacific, expanding at an 11.56% CAGR, is propelled by China's National Medical Products Administration, which approved 12,213 devices in 2024, a gateway for local manufacturers scaling into global supply chains. India's contract-development organisations are pairing with European pharma to build fill-finish lines dedicated to GLP-1 pens, compressing lead times and costs. Japan, South Korea, and Australia combine mature reimbursement systems with ageing populations, creating immediate demand for high-end connected devices.

Europe sustains mid-single-digit growth as MDR compliance costs restrain smaller players even while harmonised rules simplify multi-country launches. Germany's sickness funds reimburse electromechanical pens when paired with outcomes-based contracts that cap payer risk. The UK's National Institute for Health and Care Excellence (NICE) has invited real-world evidence generated by connected autoinjectors into cost-effectiveness files, a move expected to encourage broader digital uptake across the bloc. Eastern European markets remain cost-sensitive but are adopting disposable pens for biosimilar adalimumab at faster clips than Western peers.

South America and the Middle East & Africa are at earlier stages, yet rising chronic-disease incidence and public-sector procurement reforms point to higher volumes over the decade. Brazil's national immunisation plan has already earmarked budget for 3 mL prefilled devices to support oncology biosimilars, while Saudi Arabia's Vision 2030 healthcare push fast-tracks registration of patient-centric devices.