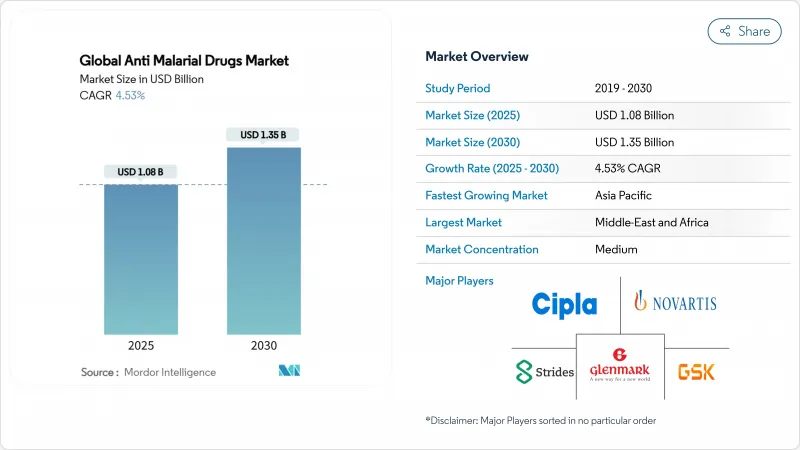

항말라리아제 시장 규모는 2025년에 10억 8,000만 달러로 평가되었고, 2030년에 CAGR은 4.53%를 나타낼 것으로 예측되며, 13억 5,000만 달러에 이를 전망입니다.

이 같은 추세는 기업들이 신종 내성균에 대응하면서도 풍토병 국가의 경제성을 유지하는 차세대 화합물을 도입함에 따라, 양 중심 성장에서 가치 주도 혁신으로의 전환을 보여줍니다. 동아프리카 전역으로 확산되는 아르테미시닌 내성은 포트폴리오 다각화를 촉진하며, 스피로인돌론 및 엔도퍼옥사이드 유사체 연구를 가속화하고 있습니다. 열대열 말라리아 원충(Plasmodium falciparum)이 여전히 임상 수요를 주도하지만, 진단 기술 발전으로 노울레시 원충(P. knowlesi)의 더 큰 부담이 드러나고 있습니다. 지리적 매출은 여전히 예방 및 연구개발(R&D) 지출이 프리미엄 가격을 주도하는 고소득 지역에서 우세합니다. 풍토병 지역 내에서는 디지털 조달 플랫폼과 급진적 치료법이 공급망과 치료 선택지를 재편하고 있습니다.

열대 기후에서의 지속적인 전파는 구매력이 낮을 때에도 기본 수요를 유지합니다. 사하라 이남 아프리카는 2023년 597,000명의 말라리아 사망자를 기록했으며, 이는 전 세계 총 사망자의 94%에 해당하지만, 가격 책정이 기부자 조달에 의존하기 때문에 수익 기여도는 상대적으로 낮았습니다. 에티오피아는 2024년 공급망 차질로 의약품 공급이 제한된 가운데 730만 건의 발병과 1,157명의 사망을 기록했습니다. 아노펠레스 스테펜시(Anopheles stephensi)의 도시 침입은 전파 패턴을 변화시켜 농촌 프로그램을 넘어선 새로운 치료 전략을 요구하고 있습니다. 이러한 집중된 부담은 풍토병 국가에서 지속적인 소비를 보장하지만, 수익 성장은 경제성 프레임워크에 의해 제한됩니다.

인도네시아의 2030년 근절 로드맵 및 인도의 2023-27 전략 계획과 같은 국가 계획은 정책적 야망을 예측 가능한 의약품 입찰로 전환합니다. 인도-부탄 및 인도-네팔 통로를 통한 국경 간 모니터링는 조달량을 집계하고 단가를 낮춥니다. 그러나 WHO는 2025년 예상되는 원조 감소가 64개 말라리아 유행국 전반의 서비스에 영향을 미쳐 공급망을 교란하고 항말라리아제 시장을 불안정하게 할 수 있다고 경고합니다. 따라서 자금 변동은 주기적 수요를 창출하여 기부 주기에 맞춰 생산을 유연하게 조정할 수 있는 공급업체에 유리합니다.

우간다, 탄자니아, 르완다, 콩고민주공화국에서 확인된 Kelch-13 469Y 돌연변이는 동남아시아 기원지를 넘어선 부분적 아르테미시닌 내성을 입증합니다. 내성 증가는 제품 수명을 단축시키고 비용이 많이 드는 재제형을 강요하며, 연구개발(R&D) 자금을 조달하지 못하는 중소 생산자들을 시장에서 밀어낼 수 있습니다. WHO의 새로운 1차 치료제 다중 병용 권고는 여러 옵션을 동시에 비축해야 하는 보건 시스템의 물류 부담을 가중시킵니다.

아르테미시닌 유도체는 글로벌 치료 지침에 힘입어 2024년 항말라리아제 시장 점유율의 46.43%를 차지했습니다. 노바티스의 시파르가민으로 대표되는 스피로인돌론계 약물은 아르테미시닌 내성 균주에 대한 효능을 유지하기 때문에 연평균 6.56%의 성장률을 보이고 있습니다. 항엽산제와 아릴 아미노알코올계 약물은 복합 요법 및 예방 분야에서 틈새 시장을 유지하고 있습니다. 엔도퍼옥사이드 유사체는 교차 내성 없이 과산화물 기반 활성을 모방하는 초기 파이프라인 단계에 있습니다.

이러한 전환은 단일 기전 실패에 대한 전략적 헤징을 의미합니다. FIKK 키나제 억제제 및 염색질 리모델러 등 다른 약물 유형도 연구 중이며, 기생충 생물학을 교란할 새로운 경로를 제시하고 있습니다 [SCiencedaily.com]. 규제 승인 기간이 여전히 길기 때문에 자본력이 풍부한 대기업이 이러한 자산의 승인을 이끌어내는 데 가장 유리한 위치에 있습니다.

말라리아 원충은 2024년 항말라리아제 시장 규모의 63.12%를 차지합니다. 개선된 PCR 진단법으로 P. knowlesi의 급속한 증가가 드러나고 있으며, 특히 인간-원숭이 접촉이 인수공통감염 확산을 주도하는 말레이시아와 인도네시아 일부 지역에서 6.99%의 연평균 성장률(CAGR)을 보이고 있습니다. 간 내 잠복포자를 가진 간발성 말라리아 원충은 근본적 치료 요법이 필요하기 때문에 여전히 수요가 높습니다.

종별 맞춤형 치료법이 점차 도입되고 있습니다. 브라질과 태국이 간발성 말라리아에 대한 단회 투여 근본 치료법을 도입한 것은 말라리아 치료에서 정밀 의학으로의 전환을 의미합니다. 광범위한 채택은 일차 진료 환경에서의 진단 정확도에 달려 있습니다.

2024년 북미의 항말라리아제 시장 점유율 39.56%는 여행자, 군대, 연구 기관을 대상으로 한 프리미엄 예방약 판매에서 비롯되었습니다. 2024년 수입 사례는 총 1,772건으로, 비유행 지역에서도 여전히 신뢰할 수 있는 치료법이 필요함을 확인시켜 주었습니다. FDA의 규제 주도권은 연구개발 투자를 더욱 공고히 합니다. 그러나 선택적 여행에 대한 의존도는 경제 침체 시 약국 수요를 급격히 위축시킬 수 있는 위험에 해당 부문을 노출시킵니다.

아시아태평양 지역은 중산층 인구 확대에 따른 의료 인프라 투자와 정부의 환자 발견 강화로 2030년까지 연평균 5.43% 성장할 것으로 전망됩니다. 통합 모니터링 및 근절 계획과 함께 해당 지역의 항말라리아제 시장 규모도 증가할 것입니다. 글로벌 펀드가 확인한 4억 7,800만 달러의 자금 부족은 혼합 금융에 대한 지속적인 의존도를 보여줍니다. 메콩강 유역 지역의 아르테미시닌 내성은 스피로인돌론계 약물과 삼중 ACT(항말라리아 복합요법)에 대한 관심을 촉진합니다. G6PD 검사 장벽이 완화되면 P. vivax의 우세로 인해 근치적 치료법 채택이 보장됩니다.

유럽, 중동 및 아프리카, 남미는 여전히 이질적인 양상을 보입니다. 유럽 수요는 여행자 예방 및 기초 연구 중심으로 안정적이지만 저성장 수익을 창출합니다. 사하라 이남 아프리카의 질병 부담은 꾸준한 조달을 보장하지만 가격 상승을 제한합니다. 아프리카 백신 보급은 돌파 감염 및 혼합 감염 치료제와 병행될 것이며, 복합 요법 사용 증가 가능성을 내포합니다. 남미 아마존 유역은 근절 단계에 가까워져 약물 조달이 후속 치료 및 수입 사례 관리로 전환되고 있습니다.

The anti-malarial drugs market size reached USD 1.08 billion in 2025 and is forecast to reach USD 1.35 billion by 2030 at a 4.53% CAGR.

This progression shows a shift from volume-led growth to value-driven innovation as companies introduce next-generation compounds that fight emerging resistance while preserving affordability for endemic countries. Artemisinin resistance spreading through East Africa is forcing portfolio diversification, spurring research into spiroindolone and endoperoxide analogues. Plasmodium falciparum continues to dominate clinical demand, yet improved diagnostics are revealing a larger burden from P. knowlesi. Geographic revenue still favors high-income regions where prophylaxis and R&D spending drive premium pricing. Inside endemic areas, digital procurement platforms and radical cure therapies are reshaping supply chains and treatment choices.

Persistent transmission in tropical climates sustains baseline demand even when purchasing power is low. Sub-Saharan Africa recorded 597,000 malaria deaths in 2023, equal to 94% of the global total, yet contributed a smaller share of revenue because pricing relies on donor procurement. Ethiopia logged 7.3 million cases and 1,157 deaths in 2024 during supply chain disruptions that limited medicine availability. Urban invasion by Anopheles stephensi is altering transmission patterns, requiring new therapeutic strategies that go beyond rural programs. This concentrated burden assures continuous consumption in endemic countries, but revenue growth remains capped by affordability frameworks.

National plans such as Indonesia's 2030 elimination roadmap and India's 2023-27 strategic plan translate policy ambition into predictable drug tenders. Cross-border surveillance along India-Bhutan and India-Nepal corridors aggregates procurement volumes and lowers unit costs. Yet WHO cautions that projected aid reductions in 2025 could affect services across 64 endemic countries, disrupting supply chains and destabilizing the anti-malarial drugs market. Funding swings therefore create cyclic demand, benefiting suppliers able to flex production in line with donor cycles.

Kelch-13 469Y mutations now identified in Uganda, Tanzania, Rwanda, and the Democratic Republic of Congo confirm partial artemisinin resistance beyond its Southeast Asian origin. Rising resistance shortens product lifecycles, compels costly reformulation, and may sideline smaller producers unable to fund R&D. WHO's new recommendation for multiple first-line therapies raises the logistical burden on health systems that must stock several options simultaneously.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Artemisinin derivatives controlled 46.43% of anti-malarial drugs market share in 2024, anchored by global treatment guidelines. Spiroindolones, represented by Novartis's cipargamin, are advancing at a 6.56% CAGR because they retain potency against artemisinin-resistant strains. Antifolates and aryl amino-alcohols keep niche relevance in combinations and prevention. Endoperoxide analogues are in early pipelines that aim to mimic peroxide-based activity without cross-resistance.

The transition indicates strategic hedging against single-mechanism failure. Other drug types such as FIKK kinase inhibitors and chromatin remodelers are under exploration, offering new pathways to disrupt parasite biology [SCiencedaily.com]. Regulatory lead times remain long, so larger firms with deeper capital are best placed to carry these assets through approval.

Plasmodium falciparum accounted for 63.12% of the anti-malarial drugs market size in 2024. Improved PCR diagnostics are uncovering a faster rise in P. knowlesi, which now grows at a 6.99% CAGR, particularly in Malaysia and parts of Indonesia where human-macaque interface drives zoonotic spillover. Plasmodium vivax retains high demand because its liver hypnozoites necessitate radical cure regimens.

Species-tailored therapies are beginning to penetrate. Brazil's and Thailand's introduction of single-dose radical cure for vivax signals movement toward precision medicine in malaria care. Broader adoption hinges on diagnostic accuracy in primary care settings.

The Anti-Malarial Drugs Market Report is Segmented by Drug Class (Aryl Amino-Alcohol Compounds, and More), Malaria Type (Plasmodium Falciparum, and More), Mechanism of Action (Treatment for Malaria, Prevention/Chemoprophylaxis, and Radical Cure), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America's dominant 39.56% share of the anti-malarial drugs market in 2024 came from premium prophylaxis sales to travelers, the military, and research institutions. Imported cases totaled 1,772 in 2024, confirming that non-endemic settings still require reliable treatments. Regulatory leadership by the FDA further anchors R&D investments. Yet reliance on discretionary travel exposes the segment to economic downturns that can quickly dampen pharmacy demand.

Asia-Pacific is forecast to grow at 5.43% CAGR through 2030 as expanding middle-income populations invest in healthcare infrastructure and governments boost case detection. The anti-malarial drugs market size here rises in tandem with integrated surveillance and elimination plans. Funding shortfalls of USD 478 million identified by the Global Fund illustrate ongoing dependency on blended finance. Resistance to artemisinin in the Greater Mekong Subregion drives interest in spiroindolones and triple ACTs. P. vivax dominance ensures radical cure uptake once G6PD testing barriers ease.

Europe, Middle East & Africa, and South America remain heterogeneous. European demand orbits around traveler prophylaxis and basic research, contributing stable but low-growth revenue. Sub-Saharan Africa's disease load secures steady procurement yet caps pricing. African vaccine deployments will coexist with drugs for breakthrough and mixed infections, potentially increasing combination therapy use. South America's Amazon basin is nearing elimination, shifting drug procurement toward follow-up care and imported case management.