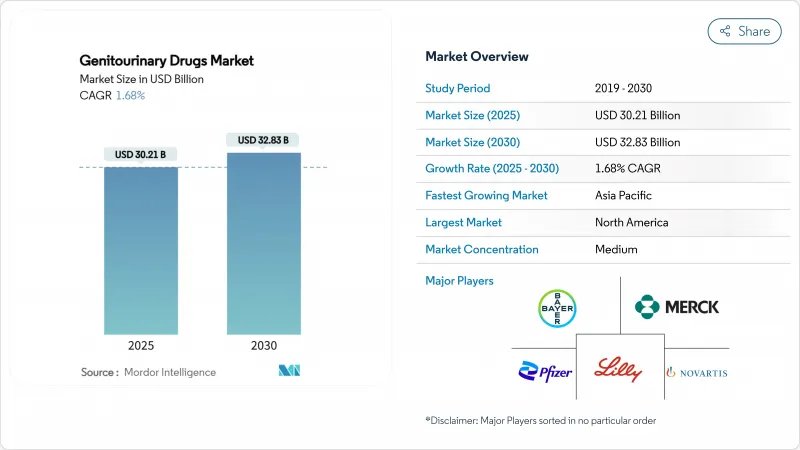

비뇨생식기 치료제 시장 규모는 2025년에 302억 1,000만 달러로 추정되고, 2030년에는 328억 3,000만 달러에 이를 것으로 예측됩니다.

고소득경제권에서 인구 동태 고령화 진행, 전립선 질환 및 실금 진단률 상승, 전문 치료제에 대한 규제 당국의 승인 가속화로 판매량 증가는 둔하고 수요는 유지되고 있습니다. 기업 수익은 만료된 블록버스터로부터 프리미엄 가격을 정당화하는 정밀 의약품, 장치 및 약물의 조합, 장시간 작용형 제제로 이동함으로써 지켜지고 있습니다. 디지털 처방 및 원격 의료는 환자 접근을 확대하고 융합 경제학을 재구성합니다. 한편, 혁신 파이프라인은 방광암, 다제 내성 요로 감염, 호르몬 관련 비뇨기과 질환 등의 미충족 요구에 대응하고 있습니다. 특허의 절벽, 항생제 내성, 치료 규정 준수 갭은 궤도를 완화하지만 비뇨생식기 치료제 시장의 기본 방향을 바꾸는 것은 아닙니다.

전립선 비대증은 60-69세 남성의 50% 이상, 85세에서는 90% 이상이 이환되어 진단률 및 치료율 향상을 촉진하고 있습니다. FDA에 의한 2025년 옵티뮴 전립선 비대증 시스템의 승인은 장치를 통한 개입으로 성 기능을 보호하면서 최대 소변 유량을 7.9mL/s에서 16.4mL/s로 개선할 수 있음을 보여줍니다. 요실금은 이미 65세 이상 여성의 25-45%에 영향을 미치고 있으며, 항콜린 작용의 부작용을 회피할 수 있는 B-3 아드레날린 작용제에 대한 수요를 부추기고 있습니다. 소변 검사 MyProstateScore 2.0은 높은 악성도 전립선 암의 94%를 검출하고 조기 단계의 치료 수요를 강화합니다. 의료 제도가 비뇨생식기 질환을 QOL(Quality of Life)의 우선사항으로 분류하는 경향이 강해지고 있으며, 이것이 보험상환의 적용 범위를 확대하여 비뇨생식기 치료제 시장의 장기적인 저견도를 지지하고 있습니다.

남성 호르몬 결핍증은 60세 이상의 남성의 20%, 80세 이상의 남성의 50%가 앓고 있습니다. 2025년 2월, FDA는 TRAVERSE 시험을 반영하여 테스토스테론의 라벨을 개정하여 수년간의 연령선 기능 저하증 경고를 제거하고 처방자의 우려를 완화했습니다. 바이엘의 Nubeqa는 ARANOTE 시험에서 위약의 7.8%에 대해 42.6%라는 초저 PSA 반응을 보였으며, 2024년에는 약 10만 명의 환자를 치료했습니다. 수명의 장기화 및 성적 건강에 대한 기대 증가는 발기부전 치료제와 관련된 병용 요법에 대한 수요를 높이고 비뇨생식기 치료제 시장의 수익 기반을 강화합니다.

비뇨 생식기 질환 전체의 어드히어런스율은 40-70%입니다. 과민성 방광 치료제는 항콜린성 부작용으로 고생하고 6개월 이내에 50%가 중단됩니다. 비베글론과 같은 장시간 작용형 B-3 작용제는 내약성이 높습니다. 발기부전 치료제는 파트너와의 힘 관계와 성능에 대한 불안으로 인한 행동 장벽에 직면합니다. 원격 의료 기업은 매월 리필 서비스와 지속적인 상담을 통해 지속성 개선을 시도하고 있지만, 확고한 종단 데이터는 아직 출현하지 않았습니다. 어드히어런스의 갭을 메우고 비뇨생식기 치료제 시장에서의 가치 유출을 방지하기 위해 디지털 알림 및 임플란트 기반 전달 시스템이 연구되고 있습니다.

발기 부전의 비뇨생식기 치료제 시장 규모는 2024년 34.67%의 최고 점유율이었으며, 원격 의료 보급과 PDE5 제네릭의 저렴한 가격에서 2024년에 34.67%를 기록했습니다. 그러나 이 분야는 치료가 포화 상태에 가까워지고 있으며 GLP-1 유발성 기능부전 합병증의 출현에 직면하여 성장이 둔화되고 있습니다. 요실금은 CAGR 전망 3.56%로, 고령화와 진단의 개선에 의해 B-3 작동약과 저침습 디바이스-약제 하이브리드에 대한 수요가 가속해, 차이가 줄어들고 있습니다.

요로 감염 치료제는 내성 문제에도 불구하고 안정된 수익원을 유지하고 전립선암 치료제는 정밀한 안드로겐 수용체 타겟팅에 의해 프리미엄 가격을 획득하고 있습니다. TAR-200과 같은 방광암 치료제는 국소 투여가 어떻게 결과를 재정의할 수 있는지를 보여주며, 연구개발 투자는 고위험이고 비근육 침윤성 질환 틈새로 끌려가게 됩니다. 이러한 변화는 비뇨생식기 치료제 시장에서 포트폴리오의 우선 순위를 재조정합니다.

포스포디에스테라아제-5 억제제는 2024년 비뇨생식기 치료제 시장 매출의 29.54%를 차지했고, 임상적으로 널리 친숙하며 경구약으로 강하게 지지되고 있습니다. 그러나 특허의 해지로 인해 가격대가 낮아져 차별화된 제제나 병용요법으로의 이행에 박차가 걸립니다. CAGR 3.78%로 성장하는 B-3 아드레날린 작용제는 항콜린성 부작용을 억제함으로써 과민성 방광의 점유율을 획득하고 있습니다.

호르몬 요법은 FDA의 표시 명확화에 의해 기세를 늘리고, a-블로커/5a-환원효소 억제제의 고정용량 요법은 어드히어런스를 개선합니다. 뉴로키닌 길항제와 마이크로바이옴 조절제가 초기 파이프라인에 추가되어 비뇨생식기 치료제 시장의 장기적인 확대를 지원하는 시장의 다양화가 강조되고 있습니다.

북미는 성숙한 상환제도와 선구적인 원격의료 보급을 활용해 2024년 매출액의 42.45%를 창출했습니다. FDA(미국 식품의약품국)의 패스트트랙 패스웨이를 통해 TAR-200과 같은 혁신의 신속한 도입이 가능해지고, 인구동태의 고령화와 높은 전립선암 검진률로 환자 수요가 강화되고 있습니다. 제네릭 PDE5 제제의 침식은 가격 설정을 억제하고 있지만 수량은 확대되어 비뇨생식기 치료제 시장 전체의 지역별 성장을 안정시키고 있습니다.

CAGR 2.67%로 성장하는 아시아태평양은 보험 적용 범위 확대, 도시화, 구미 승인까지 규제 지연을 단축하는 정책 개혁 등의 혜택을 받습니다. 중국의 집중조달은 비용을 낮추면서도 접근을 확대하고 있으며, 일본의 초고령화 사회는 실금치료제 및 BPH 치료제를 뒷받침하고 있습니다. 인도의 제네릭 의약품에 대한 전문 지식은 국내 수요와 수출 수요를 모두 공급하여 지역 자급률을 높이고 있습니다. 가격 압력은 엄격하고 절대적인 환자 수는 이 지역을 비뇨생식기 치료제 시장의 장기적인 성장 엔진으로 자리매김하고 있습니다.

유럽은 완만하면서도 일관된 성장을 이루고 있습니다. EMA의 일원화에 의해 승인 신청이 간소화되고 독일 등에서는 비베그론과 같은 신규 약제의 프리미엄 가격이 유지되고 있습니다. 그러나 일부 시장에서는 긴축 재정이 실시되어 각국의 상환 규칙이 세분화되어 있기 때문에 출시의 순서가 복잡해지고 있습니다. 동유럽은 건강 관리의 근대화가 EU 기준에 부합하기 때문에 점진적인 상승 여지가 있습니다. Brexit의 영향으로 영국의 승인 신청은 고립되고 비용은 약간 상승하지만 비뇨생식기 치료제 시장 수요 펀더멘털은 변하지 않습니다.

The genitourinary drugs market size is valued at USD 30.21 billion in 2025 and is forecast to reach USD 32.83 billion by 2030, reflecting a steady 1.68% CAGR.

Ongoing demographic aging in high-income economies, rising diagnosis rates for prostate disorders and incontinence, and faster regulatory approvals for specialty therapeutics sustain demand even as volume growth remains muted. Companies protect revenues by shifting from expiring blockbusters to precision medicines, device-drug combinations, and long-acting formulations that justify premium pricing. Digital prescribing and telemedicine are broadening patient access and reshaping fulfillment economics, while innovation pipelines address unmet needs in bladder cancer, multidrug-resistant urinary tract infections, and hormone-related urological problems. Patent cliffs, antibiotic resistance, and therapy-compliance gaps temper the trajectory but do not alter the fundamental direction of the genitourinary drugs market.

Benign prostatic hyperplasia affects more than 50% of men aged 60-69 and up to 90% by age 85, prompting higher diagnostic and treatment rates. The FDA's 2025 clearance of the Optilume BPH system illustrates how device-assisted interventions can improve maximum urinary flow from 7.9 mL/s to 16.4 mL/s while protecting sexual function. Urinary incontinence already impacts 25-45% of women over 65, fueling demand for B-3 adrenergic agonists that avoid anticholinergic side effects. The MyProstateScore 2.0 urine assay detects 94% of high-grade prostate cancers, reinforcing early-stage therapeutic demand. Health systems increasingly classify genitourinary disorders as quality-of-life priorities, which strengthens reimbursement coverage and underpins the long-term resilience of the genitourinary drugs market.

Testosterone deficiency touches 20% of men over 60 and 50% above 80. In February 2025, the FDA revised testosterone labels to reflect the TRAVERSE trial, removing longstanding age-related hypogonadism warnings and easing prescriber concerns. Prostate cancer incidence doubles every decade after 50; Bayer's Nubeqa treated nearly 100,000 patients in 2024 with an ultra-low PSA response of 42.6% versus 7.8% for placebo in the ARANOTE study. Longer lifespans coupled with higher expectations for sexual wellness elevate demand for erectile dysfunction therapies and related combination regimens, reinforcing the revenue base of the genitourinary drugs market.

Adherence rates range from 40-70% across genitourinary conditions. Overactive bladder drugs suffer from anticholinergic side effects that drive 50% discontinuation inside six months. Long-acting B-3 agonists such as vibegron offer better tolerability. Erectile dysfunction regimens face behavioral barriers tied to partner dynamics and performance anxiety. Telemedicine firms attempt to improve persistence through monthly refill services and ongoing counseling, but robust longitudinal data are still emerging. Digital reminders and implant-based delivery systems are under study to close the adherence gap and safeguard value leakage from the genitourinary drugs market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The genitourinary drugs market size for erectile dysfunction stood at a leading 34.67% share in 2024, benefiting from telemedicine penetration and generic PDE5 affordability. Yet growth is slowing as the segment approaches therapeutic saturation and faces emerging GLP-1-induced dysfunction complications. Urinary incontinence, with a 3.56% CAGR outlook, is narrowing the gap as aging populations and improved diagnosis accelerate demand for B-3 agonists and minimally invasive device-drug hybrids.

Urinary tract infection therapeutics retain stable revenue streams despite resistance issues, while prostate cancer drugs capture premium pricing through precision androgen-receptor targeting. Bladder cancer interventions such as TAR-200 demonstrate how localized delivery can redefine outcomes, drawing R&D investment toward high-risk, non-muscle-invasive disease niches. Together, these shifts recalibrate portfolio priorities within the genitourinary drugs market.

Phosphodiesterase-5 inhibitors contributed 29.54% of genitourinary drugs market revenue in 2024, upheld by broad clinical familiarity and strong oral preference. Patent expiries, however, compress price points and spur a migration toward differentiated formulations and combination therapies. B-3 adrenergic agonists, growing at 3.78% CAGR, are winning share in overactive bladder by limiting anticholinergic adverse events.

Hormone therapies gain momentum after the FDA's labeling clarification, while a-blocker/5a-reductase inhibitor fixed-dose regimens improve adherence. Neurokinin antagonists and microbiome-modulating agents populate early pipelines, highlighting diversification themes that support the long-term expansion of the genitourinary drugs market.

The Genitourinary Drugs Market Report is Segmented by Disease Type (Erectile Dysfunction, and More), Drug Class (Hormonal Therapy, and More), Route of Administration (Oral, Injectable, and More), Gender (Male and Female), Distribution Channel (Hospital Pharmacies, and More), Molecular Type (Small-Molecular Type, and More), Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 42.45% of 2024 revenue, leveraging mature reimbursement systems and pioneering telehealth penetration. FDA fast-track pathways enable swift uptake of innovations such as TAR-200, and patient demand is reinforced by demographic aging and high prostate-cancer screening rates. Generic PDE5 erosion tempers pricing but expands volume, stabilizing overall regional growth for the genitourinary drugs market.

Asia-Pacific, advancing at 2.67% CAGR, benefits from expanding insurance coverage, urbanization, and policy reforms that shorten the regulatory lag behind Western approvals. China's centralized procurement lowers costs yet enlarges access, while Japan's super-aging society propels incontinence and BPH therapeutics. India's generics expertise supplies both domestic and export demand, strengthening regional self-sufficiency. Although pricing pressure is intense, absolute patient volumes position the region as a long-run growth engine for the genitourinary drugs market.

Europe delivers consistent though slower expansion. EMA centralization simplifies submissions, and countries such as Germany sustain premium prices for novel agents like vibegron. Nonetheless, austerity measures in certain markets and fragmented national reimbursement rules complicate launch sequencing. Eastern Europe offers incremental upside as healthcare modernization aligns with EU standards. Brexit forces isolated UK filings, marginally raising costs but not altering demand fundamentals for the genitourinary drugs market.