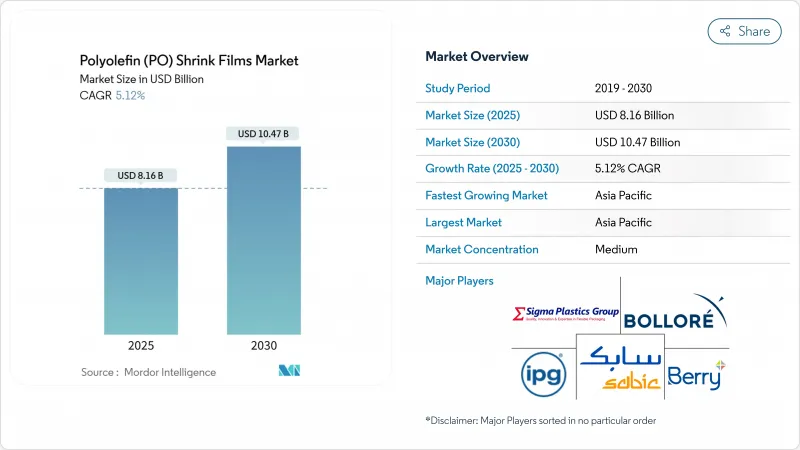

폴리올레핀 수축 필름 시장 규모는 2025년에 81억 6,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.12%로 성장할 전망이며, 2030년에는 104억 7,000만 달러에 달할 것으로 예측됩니다.

이 성장은 재료의 다양성, 재활용 가능한 솔루션에 대한 선호도가 증가 및 식품과 접촉하는 용도 분야에서 PVC의 꾸준한 대안을 반영합니다. 전자상거래의 급증, 360도 그래픽을 요구하는 브랜드 수요, 자동화 대응의 얇은 가교 등급의 급속한 전개에 의해 폴리올레핀 수축 필름 시장의 대응 가능한 용도가 확대되고 있습니다. 지역별로는 아시아 업체들이 수출용 소비재 생산 능력을 확대하는 한편, 북미 컨버터는 소비자의 신뢰를 높이는 변조 방지 포장을 중시하고 있습니다. 유럽에서는 정책적 압력으로 소비자 사용 후 재활용 원료(PCR)를 포함한 필름의 채택이 가속화되고 성능과 재활용 목표 모두에 맞는 독특한 블렌드를 장려하고 있습니다.

전자상거래의 성장으로 운송 중 상품을 보호하기 위한 탬퍼 증거(조절 방지) 폴리올레핀 수축 필름 수요가 높아지고 있습니다. 북미의 소매업체는 제품을 보호하고 소비자의 신뢰를 구축하기 위해 이러한 필름을 사용하고 있으며 온라인 쇼핑 사용자의 78%가 눈에 띄는 변조 방지 효과를 중시합니다. 인터테이프 폴리머 그룹의 ExlfilmPlus PCR은 35%의 재활용률을 갖는 폴리올레핀 수축 필름으로 보안과 지속가능성 요구를 충족합니다. 이 필름은 높은 투명성과 전자상거래 패키지의 과제에 대응하는 재생재 함량을 겸비하고 있습니다.

유럽의 식품 제조업체는 2030년까지 5%의 폐기물 감소를 목표로 하는 2024년 4월 포장법 시행 후 재활용 가능한 폴리올레핀 필름으로 축발을 옮겼습니다. 영국, 스페인, 이탈리아의 평행 플라스틱 세금은 재활용률이 30% 미만인 필름에 벌칙을 부과합니다. Clysar의 Store-Drop-Off-qualified EV-HPG는 컨버터가 식품의 안전성, 투명성 및 재활용성을 어떻게 결합하는지를 보여줍니다.

미국에서의 셰일 원료의 혼란은 이미 완성된 필름 비용의 최대 70%를 차지하는 원재료의 변동을 높이고 있습니다. OECD는 2040년까지 플라스틱 생산량이 7억 3,600만 톤에 이를 수 있으며 원료 경쟁이 치열해질 것이라고 경고합니다. 컨버터는 멀티 소싱, 짧은 수지 계약 및 처녀 원료를 PCR 펠릿으로 희석하는 레시피로 위험을 헤지합니다.

2024년 폴리올레핀 수축 필름 시장 점유율은 일반 수축 필름이 54%를 차지했으며, 저렴한 가격과 폭넓은 가공 창구에 지지를 받고 있습니다. 이 부문은 투명도가 높고 인쇄가 용이하기 때문에 슈퍼마켓의 식품용 멀티팩이나 판촉용 번들에 채용되고 있습니다. 그러나 컨버터는 천공성, 내마모성 및 얇은 프로파일로 인해 랩 불량을 일으키지 않고 보다 빠른 라인 속도를 가능하게 하는 가교 등급의 업셀을 점점 늘리고 있습니다.

의약품 블리스터 번들, 화장품 상자 포장, 전자 기기 등이 열에 약한 내용물을 보호하기 위해 더 낮은 씰 온도를 요구하게 되어 가교 등급의 생산량은 2025-2030년 CAGR 6.88%로 성장할 것으로 예측됩니다. 아시아와 북미의 생산능력 확대로 가격차가 줄어들고 폴리올레핀계 수축 필름 시장의 기존 디스플레이 용도 이외로의 전환이 촉진됩니다.

2024년 폴리올레핀 수축 필름 시장 규모에서는 투명성과 비용 경쟁력으로 폴리에틸렌이 57%의 점유율을 유지했습니다. 다층 PE 블렌드는 낮은 오븐 체류 시간에서도 타이트한 씰을 가능하게 하기 때문에 음료캔의 다네스트나 청과일 트레이의 정평이 되고 있습니다. 가공업자는 현재 광학 특성을 희석하지 않고 브랜드의 순환성 서약을 준수하기 위해 PCR 스트림을 통합하고 있습니다.

폴리프로필렌은 더 높은 강성, 화학적 불활성, 레토르트 식품 및 의료용 키트에 바람직한 높은 열굴절점으로 인해 2030년까지 매년 7.21% 상승할 것으로 예측됩니다. 새로운 5층 공압출기는 PP와 엘라스토머 타이층을 공동 블렌딩하여 인열 강도를 높이면서 광택을 유지합니다. 이 프리미엄 믹스는 폴리올레핀 수축 필름 시장에서 컨버터를 상품화된 PE 제품과 차별화합니다.

2024년 폴리올레핀 수축 필름 시장의 매출 구성비는 아시아태평양이 38%를 차지했으며, 세계에서 가장 빠른 CAGR 7.10%로 성장이 예측됩니다. 중국의 압출업자 기반은 다국적 FMCG 포장업체와 제휴하고 인도의 리지드 패키징 붐은 도시의 소매업 성장에 대응하고 있습니다. 각 지역의 컨버터는 사내에서 플레이트리스 디지털 인쇄기를 육성하여 국내 전자상거래 급증을 포착한 신속한 프라이빗 브랜드 판촉 캠페인을 가능하게 하고 있습니다.

일본과 한국은 하이베리어 다층 기술에 주력해 수출 의약품용으로 틈새 가교 롤을 공급하고 있습니다. 폴리올레핀 수축 필름 시장에서는 에너지 효율이 높은 수축 오븐에 대한 연구개발 세액 공제가 협회의 보조금으로 활용되어 채용이 강화되고 있습니다.

북미는 미국의 옴니채널 소매 생태계를 원동력으로 하는 성숙하면서도 혁신 주도의 무대입니다. 캐나다와 멕시코는 수지 생산에 근접하고 관세면에서 우월한 무역 회랑으로 지역 공급을 보완하고 가격 변동에 대한 강도를 확보하고 있습니다.

유럽은 엄격한 규제 감독과 높은 구매력의 균형을 유지하고 있습니다. 서큘러 이코노미(순환형 경제) 지침은 컨버터에게 재활용 가능성 증명과 2027년까지 PCR 블렌드로의 전환을 촉구하고 있습니다. 독일, 이탈리아, 영국은 음료, 과자 및 의약품의 왕성한 생산으로 핵심 수요 클러스터를 형성하고 있습니다. 남부와 동부 회원국은 소매체인이 역내 포장 개요를 조화시키면서 서서히 따라오고 있습니다.

남미와 중동 및 아프리카는 규모가 작지만 점점 매력적인 프론티어입니다. 사우디아라비아의 '비전 2030'은 폴리올레핀 수축 필름 시장을 걸프 협력회의 시장으로 확장하기 위해 폴리머의 강하 분야에 대한 투자를 장려합니다.

The Polyolefin Shrink Films Market size is estimated at USD 8.16 billion in 2025, and is expected to reach USD 10.47 billion by 2030, at a CAGR of 5.12% during the forecast period (2025-2030).

Growth reflects the material's versatility, rising preference for recyclable solutions, and the steady replacement of PVC in food-contact applications. Surging e-commerce volumes, brand demand for 360-degree graphics, and the rapid roll-out of automation-ready thin-gauge cross-linked grades are expanding addressable use-cases for the polyolefin shrink film market. Across regions, Asian manufacturers scale capacity to serve export-oriented consumer goods, while North American converters emphasize tamper-evident wraps that build consumer trust. In Europe, policy pressure accelerates adoption of films containing post-consumer recycled (PCR) feedstock, encouraging proprietary blends that match both performance and recycling targets.

E-commerce growth has driven demand for tamper-evident polyolefin shrink films to secure products during transit. North American retailers use these films to protect goods and build consumer trust, with 78% of online shoppers valuing visible tamper-evidence. Intertape Polymer Group's ExlfilmPlus PCR, a polyolefin shrink film with 35% recycled content, addresses security and sustainability needs. The film combines high clarity with post-consumer recycled content, meeting e-commerce packaging challenges.

European food manufacturers pivot towards recyclable polyolefin films after April 2024 packaging legislation targeting a 5% waste reduction by 2030 . Parallel plastic taxes in the UK, Spain and Italy penalize films with under 30% recycled content. Clysar's Store-Drop-Off-qualified EV-HPG illustrates how converters combine food safety, clarity and recyclability.

Shale-feedstock disruptions in the United States heighten raw-material swings that already represent up to 70% of finished film cost. The OECD warns that plastic production may hit 736 million tonnes by 2040, intensifying feedstock competition. Converters hedge risks via multi-sourcing, shorter resin contracts, and recipes that dilute virgin inputs with PCR pellets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

General shrink film held the largest 54% polyolefin shrink film market share in 2024, underpinned by affordability and wide processing windows. The segment's clarity and ease of printing keeps it entrenched in food multipacks and promotional bundles across supermarkets. Yet converters increasingly upsell cross-linked grades where puncture resistance, scuff holdout and thinner profiles allow faster line speeds without wrap failure.

Cross-linked output is forecast to grow at a 6.88% CAGR from 2025 to 2030 as pharmaceutical blister bundles, boxed cosmetics and electronics seek lower sealing temperatures that protect heat-sensitive contents. Expanded capacity in Asia and North America narrows the price delta, encouraging switchovers that stretch the polyolefin shrink film market beyond traditional displays.

Polyethylene maintained a commanding 57% stake within the polyolefin shrink film market size in 2024, driven by transparency and cost competitiveness. Multi-layer PE blends permit tight seals even at low oven dwell times, making them a staple in beverage can dernests and produce trays. Processors now incorporate PCR streams to comply with brand circularity pledges without diluting optical properties.

Polypropylene is expected to rise 7.21% annually to 2030, buoyed by higher stiffness, chemical inertness and elevated heat-deflection points desirable for retorted foods and medical kits. New five-layer co-extruders co-blend PP with elastomer tie layers, retaining gloss while boosting tear resistance. This premium mix separates converters from commoditised PE offerings within the polyolefin shrink film market.

The Polyolefin Shrink Film Market Report Segments the Industry by Type (General Shrink Film and Cross-Linked Shrink Film), Material Type (Polyethylene and Polypropylene), Layer Structure (Monolayer and Multilayer), Application (Food and Beverage, Industrial Packaging, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific dominated the polyolefin shrink film market with 38% revenue contribution in 2024, and its projected 7.10% CAGR remains the fastest globally. China's entrenched extruder base partners with multinational FMCG packers, while India's rigid packaging boom responds to urban retail growth. Regional converters foster in-house plateless digital presses, enabling swift private-label promotion campaigns that capture domestic e-commerce surges.

Japan and South Korea focus on high-barrier multilayer technology, supplying niche cross-linked rolls for export pharmaceuticals; domestic demand leans on automation-ready thin gauges that fit compact factory footprints. Association grants channel R&D tax credits toward energy-efficient shrink ovens, reinforcing adoption inside the polyolefin shrink film market.

North America constitutes a mature yet innovation-led arena powered by the United States' omnichannel retail ecosystem. Canada and Mexico complement regional supply through proximity to resin production and tariff-favoured trade corridors, anchoring resilience against price swings.

Europe balances stringent regulatory oversight with high purchasing power. Circular economy directives push converters to certify recyclability and shift toward PCR blends by 2027. Germany, Italy and the United Kingdom represent core demand clusters owing to strong beverage, confectionery and pharmaceutical output. Southern and Eastern member states gradually catch up as retail chains harmonise packaging briefs across the bloc.

South America and the Middle East & Africa present smaller but increasingly attractive frontiers. Brazil leverages a robust petrochemical base to serve Mercosur neighbours, while Saudi Arabia's Vision 2030 encourages downstream polymer investments that extend the reach of the polyolefin shrink film market into Gulf Cooperation Council markets.