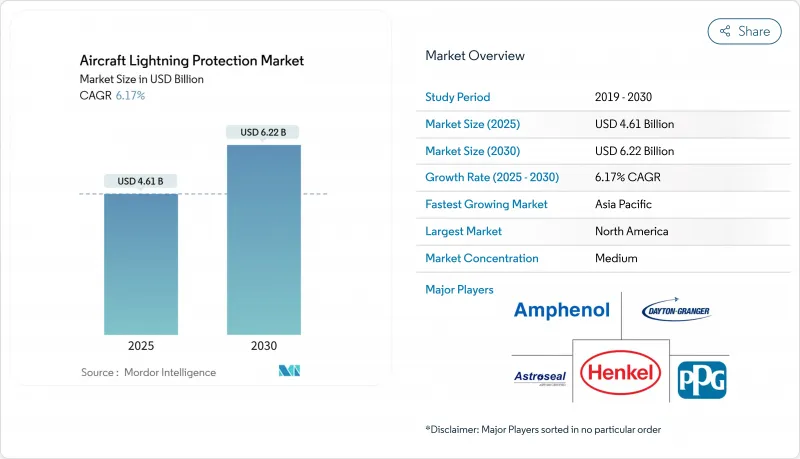

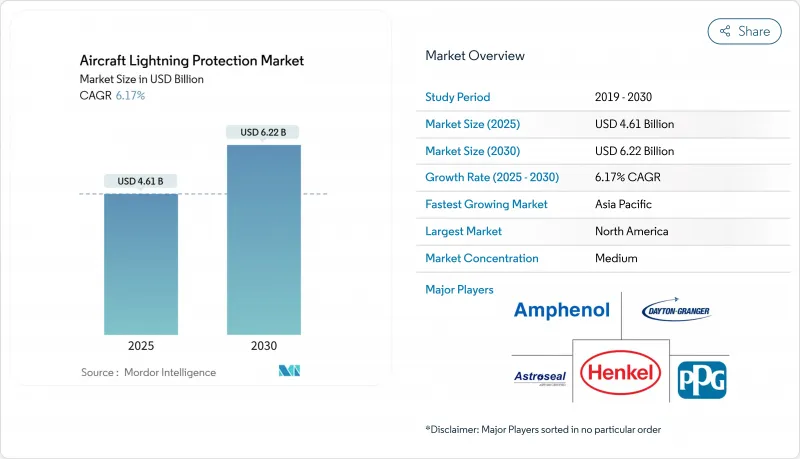

항공기 낙뢰 보호 시장 규모는 2025년에 46억 1,000만 달러로 평가되었고, 2030년에 62억 2,000만 달러에 이를 것으로 예측되며, CAGR은 6.17%를 나타낼 전망입니다.

성장은 두 가지 구조적 변화와 맞물려 있습니다. 탄소섬유 동체의 적용 확대와 전기 항공 택시 함대의 급속한 등장입니다. 복합재 기체는 기존 알루미늄 외판의 내장 전도성을 갖추지 못해, 신규 인도마다 낙뢰 에너지를 안전하게 분산시키는 전도성 포일, 메쉬, 나노 소재 코팅에 대한 수요가 증가합니다. 미국 연방항공청(FAA)과 유럽항공안전청(EASA)의 인증 규정 강화가 이 수요를 더욱 부추기는 가운데, 상업용 항공기 주문 잔고가 사상 최고치를 기록하면서 OEM 업체들은 인증된 보호 소재의 장기적 공급 확보에 나서고 있습니다. 중국이 2025년까지 270개 공항 운영을 목표로 하는 등 아시아태평양 지역의 공항 붐이 물량 증가를 가속화하고 있지만, 기술 중심지는 여전히 북미입니다. 중견 공급업체들은 경쟁 환경에서 6자리 수의 인증 테스트 비용 압박에 직면하면서, 대기업들이 M&A를 통해 역량을 통합할 수 있는 길을 열어주고 있습니다.

B787 및 A350 항공기 계열은 낙뢰 전류를 분산시키기 위해 내장형 구리 또는 알루미늄 메쉬를 사용하며, 이는 외부 본딩 스트랩 방식에서 완전히 벗어난 설계 변화를 의미합니다. 운영사들은 통합형 메쉬를 점점 더 표준으로 인식하고 있으며, 이러한 기대는 현재 좁은 동체 기체 리프레시 프로그램과 최신 지역 제트기로 확산되고 있습니다. NASA 시험 패널 결과, 경량 비금속 필름이 낙뢰 피해 깊이를 79% 감소시키면서 동시에 낙뢰 후 압축 강도를 21% 향상시키는 것으로 나타났습니다. 이로 인해 OEM 업체들은 향후 모델에 더 얇고 가벼운 층을 채택하도록 장려받고 있습니다. 따라서 소재 혁신은 단위 수요를 증폭시키는데, 각 신규 복합재 패널마다 공장 설치형 전도 경로가 필요하기 때문입니다. 이 촉진요인은 2027년까지 가장 강력한 주도력을 발휘한 후 복합재 보급률이 정점에 달하면서 안정화될 전망입니다.

단일 통로 제트기의 주문 잔고는 2031년까지 가득 찬 상태를 유지할 전망입니다. 보잉과 에어버스는 확장 금속 포일 같은 특수 소재의 안정적 공급과 생산량 증대를 공개적으로 연계했습니다. PPG의 2024년 3분기 2억 9천만 달러 규모의 항공우주 코팅 주문 잔고는 이미 연장된 리드 타임으로 운영 중인 공급망의 부담을 부각시킵니다. 각 주문 잔고 감소는 번개 보호 키트에 대한 라인 장착 수요를 촉발하는 반면, 항공사가 노후 기체 수명을 연장함에 따라 지연된 납품은 점진적인 개조 기회로 이어집니다. 아시아태평양 지역 항공기 함대는 전 세계 주문 잔고의 3분의 1을 차지하며, 2026년까지 이 지역을 물량 성장의 엔진으로 자리매김하게 합니다.

200kA 임펄스 시뮬레이션이 가능한 낙뢰 실험실은 샷당 4만 달러 이상의 항공우주 요금을 청구하며, 완전한 준수 프로그램은 다양한 크기의 시험편에 수십 차례의 낙뢰 시험을 요구할 수 있습니다. 그래핀 또는 CNT 솔루션을 개발하는 스타트업들은 인증 마일스톤을 통과하기 전에 시드 자금을 소진하는 경우가 많아, 그들의 지적재산권(IP)은 대형 기존 기업들에 의해 라이선스될 수밖에 없습니다. 이러한 재정적 장벽은 전반적인 기술 다양성을 제한하고 가격 경쟁을 늦추며, 향후 성장률을 약 0.8% 포인트 감소시킬 것으로 추정됩니다.

확장 금속 포일은 오랜 사용 이력과 풍부한 인증 데이터 덕분에 2024년에도 항공기 낙뢰 보호 시장 점유율의 49.25%를 유지했습니다. 그럼에도 도금 탄소 섬유는 기존 포일의 물량 증가율을 상회하는 7.54%의 연평균 복합 성장률(CAGR)로 항공기 낙뢰 보호 시장 규모에서 점유율을 확대할 것으로 전망됩니다. 이 소재는 구조적 플라이 내에 전도성을 내장하여 무게를 줄이면서도 낙뢰 경로를 유지하는 장점이 있으며, 이는 787 기체 패널에서 검증되었습니다. 탄소 나노튜브를 적용한 연구 패널은 낙뢰 흔적이 54.8% 감소한 것으로 나타나, 나노 강화 플라이가 실험실에서 생산 라인으로 이동함에 따라 향후 성장 가능성이 예상됩니다.

교차 직조 와이어 패브릭은 검증된 생존성을 추구하는 방산 주요 업체, 특히 폭풍이 빈번한 전역에서 저고도 운용되는 회전익 항공기에 매력적입니다. 전도성 코팅은 포일 적층이 비실용적인 개조 분야에서 틈새를 메우지만, 두꺼운 코팅이 아크 열을 가두어 박리 현상을 확대할 수 있다는 연구 결과로 채택이 제한됩니다. 현재 수익 구조에는 포함되지 않지만, 초기 단계의 그래핀 필름은 고가의 구리 투입 없이 단위 면적당 무게에서 획기적 개선을 약속해 에어버스와 BAE로부터 R&D 투자를 유치 중입니다.

고정익 제트기는 2024년 매출의 58.68%를 차지하며 항공기 낙뢰 보호 시장의 핵심 역할을 공고히 했습니다. 또한 현재 인증 지식의 대부분을 차지하므로, 소재 공급업체들은 신흥 분야를 공략하기 전에 단일 통로 구조물에서 새로운 솔루션을 정기적으로 검증합니다. 반면 eVTOL 기체는 연평균 10.21% 성장률을 보이며 분산 추진 포드와 고에너지 배터리를 도입해 다중 낙뢰 진입점을 생성합니다. EASA의 최신 특별 조건은 이제 구조적 전류 경로와 함께 배터리 열폭주를 해결하는 종합적인 시스템 수준 보호를 요구합니다.

eVTOL 부품의 항공기 낙뢰 보호 시장 규모는 2026년 이후 시제품이 양산 단계에 진입함에 따라 급증할 전망입니다. 회전익 항공기는 회전 허브가 자연스럽게 리더들을 끌어들이며 14 CFR 27.610이 요구하는 견고한 로터 팁 본딩 및 블레이드 보호층을 필요로 하기 때문에 꾸준한 틈새 시장을 유지하고 있습니다. 해당 부문 현황을 보면, 고정익 제트기의 전통적인 라인핏 물량이 10년 후반 도시 항공 이동성 함대를 주도할 경량 솔루션 연구개발(R&D)을 지원하고 있습니다.

북미는 2024년 매출의 38.45%를 차지했습니다. 이 지역은 글로벌 복합재 기체 조립, 고에너지 인증 실험실 및 1차 공급업체의 대부분을 보유하고 있기 때문입니다. FAA와의 협력을 통해 인증 절차가 간소화되어 공급업체의 시장 출시 기간이 단축됩니다. 캐나다의 틈새 공급업체들은 수지 주입용 포일을 공급하는 반면, 멕시코의 마킬라도라(maquiladora) 공장들은 객실 구역용 접합 하드웨어를 가공합니다. 생태계의 긴밀성은 프리미엄 가격 책정을 뒷받침하지만, 노동력 부족으로 인해 일정 지연 위험이 존재합니다.

아시아태평양 지역은 7.98%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. 이는 2025년까지 270개 공항을 운영하겠다는 중국의 의지에 기반하며, 각 공항이 새로운 협폭기 주문을 촉진할 것입니다. 국내 복합재 공장은 빠르게 확장되고 있으나, 지적재산권 보호는 여전히 서방의 우려사항으로 남아 있어 최신 탄소나노튜브(CNT) 보강 메쉬 기술 이전을 지연시키고 있습니다. 일본의 2024 회계연도 주문 규모가 7조 700억 엔으로 급증하면서 국방부(MoD)의 엄격한 사양이 맞물려 고전류 포일과 내식성 실런트에 대한 현지 수요를 촉진하고 있습니다. 인도 바도다라의 타타-에어버스 생산라인은 국산 낙뢰 보호 공급망 구축의 초석을 마련했으나 서구 수준에 도달하려면 20년이 소요될 전망입니다.

유럽은 기술 선도권을 유지 중입니다. 유럽항공안전청(EASA) 인증 기관은 규제 변경 조기 도입을 촉진하며, 유럽연합(Horizon) 기금 연구소는 메쉬 무게를 58% 절감하는 초박형 알루미늄 코팅 기술을 선도합니다. 중동은 걸프 항공사들의 기단 갱신을 활용해 개조 수요를 촉진합니다. 남미와 아프리카는 아직 초기 단계이지만, 브라질의 지역 제트기 수출은 향후 현지 호일 변환 라인 수요의 씨앗이 될 전망입니다.

The aircraft lightning protection market size stands at USD 4.61 billion in 2025 and is projected to reach USD 6.22 billion by 2030, reflecting a steady 6.17% CAGR.

Growth aligns with two structural shifts: the widening application of carbon-fiber fuselages and the rapid emergence of electric air-taxi fleets. Composite airframes lack the built-in conductivity of traditional aluminum skins, so every new delivery increases demand for conductive foils, meshes, and nanomaterial coatings that safely channel strike energy. Tightening FAA and EASA certification rules intensify this pull, while record commercial aircraft backlogs push OEMs to secure a long-term supply of qualified protection materials.Asia-Pacific's airport boom, led by China's target of 270 operational facilities by 2025, accelerates volume growth even as North America remains the technology nucleus. Mid-sized suppliers face cost pressure from six-figure qualification tests on the competitive front, opening paths for larger firms to consolidate capabilities through M&A.

B787 and A350 aircraft families rely on embedded copper or aluminum meshes to dissipate strike currents, marking a wholesale design departure from external bonding straps. Operators increasingly view integrated mesh as standard, and that expectation now cascades into narrow-body refresh programs and the latest regional jets. NASA test panels showed that lightweight non-metallic films can cut lightning damage depth by 79% while boosting post-strike compressive strength by 21%, encouraging OEMs to adopt thinner, lighter layers in forthcoming models. Material innovation thus compounds unit demand, as each new composite panel requires factory-installed conductive pathways. The driver delivers its strongest pull through 2027, stabilizing as composite penetration plateaus.

Order books for single-aisle jets remain full well into 2031. Boeing and Airbus have publicly linked production-rate hikes to a reliable supply of specialty materials such as expanded metal foils. PPG's USD 290 million aerospace-coatings backlog in Q3 2024 highlights the strain on supply chains already running at extended lead times. Each backlog drawdown releases a wave of line-fit demand for lightning protection kits, while deferred deliveries translate into incremental retrofit opportunities as airlines stretch the life of older frames. Asia-Pacific fleets constitute a third of the global backlog, positioning the region as the volume growth engine through 2026.

Lightning simulation labs capable of 200 kA impulses charge aerospace rates exceeding USD 40,000 per shot, and a full compliance program can require dozens of strikes across multiple coupon sizes. Start-ups developing graphene or CNT solutions often exhaust seed funding before clearing certification milestones, leaving their IP to be licensed by larger incumbents. The financial hurdle constrains overall technology diversity and slows price competition, trimming growth by an estimated 0.8 percentage points over the horizon.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Expanded metal foils still held 49.25% of the aircraft lightning protection market share in 2024 due to their long service history and abundant certification data. Even so, plated carbon fiber is projected to capture a rising slice of the aircraft lightning protection market size as its 7.54% CAGR outpaces volume growth in legacy foils. The material embeds conductivity within structural plies, shaving weight while maintaining strike pathways, an advantage validated on 787 fuselage panels. Research panels with carbon nanotubes recorded 54.8% smaller strike scars, pointing to future gains as nano-reinforced plies move from lab to line.

Interwoven wire fabrics appeal to defense primes seeking proven survivability, particularly for rotorcraft operating low-level in storm-dense theaters. Conductive coatings fill retrofit niches where foil lay-up is impractical; however, studies show thick coatings can trap arc heat and enlarge delamination, limiting adoption. Though outside today's revenue pie, early-stage graphene films attract R&D capital from Airbus and BAE because they promise step-changes in areal weight without expensive copper inputs.

Fixed-wing jets generated 58.68% of 2024 revenue, cementing their role as the anchor of the aircraft lightning protection market. They also represent the majority of current certification knowledge, so material suppliers routinely validate new solutions on single-aisle structures before chasing emerging categories. In contrast, eVTOL airframes expand at a 10.21% CAGR and introduce distributed propulsion pods and high-energy batteries that create multiple strike entry points. EASA's latest special conditions now require holistic system-level protection that addresses battery thermal runaway alongside structural current paths.

The aircraft lightning protection market size for eVTOL components is forecast to multiply as prototypes enter serial production from 2026 onward. Rotorcraft remain a steady niche because their rotating hubs naturally attract leaders, demanding robust rotor-tip bonding and blade protection layers mandated by 14 CFR 27.610. The segment tableau shows traditional line-fit volume in fixed-wing jets financing R&D for lightweight solutions poised to dominate the urban air-mobility fleet later in the decade.

The Aircraft Lightning Protection Market Report is Segmented by Product Type (Expanded Metal Foils, Interwoven Wire Fabrics, and More), Aircraft Type (Fixed-Wing Aircraft, Rotorcraft, Unmanned Aerial Vehicle, and More), Fit (Line-Fit, and Retrofit), End User (Civil/Commercial, and More) and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.45% of 2024 revenue because the region hosts the bulk of global composite-airframe assembly, high-energy certification labs, and tier-one suppliers. FAA collaboration eases qualification runs, allowing vendors to compress time-to-market. Canada's niche suppliers feed resin-infusion foils, while Mexico's maquiladoras machine bonding hardware for cabin zones. Ecosystem tightness supports premium pricing, though labor shortages risk schedule slip.

Asia-Pacific posts the fastest 7.98% CAGR, underpinned by China's intent to operate 270 airports by 2025, each driving fresh narrow-body orders. Domestic composites plants scale rapidly; however, intellectual-property safeguards remain a Western concern, slowing the transfer of the latest CNT-reinforced meshes. Japan's orderbook surge to JPY 7.07 trillion in FY 2024 pairs with stringent MoD specifications, spurring local demand for high-amp foil and corrosion-resistant sealants. India's Tata-Airbus line at Vadodara lays early groundwork for an indigenous lightning-protection supply but needs two decades to match Western volume.

Europe continues as the technology vanguard. The EASA certification authority prompts early adoption of regulatory changes, and Horizon-funded labs pioneer ultra-thin aluminum coatings that cut mesh weight by 58%. The Middle East leverages fleet renewals at Gulf carriers, pushing retrofit demand. South America and Africa remain nascent, but Brazil's regional jet exports seed future requirements for local foil conversion lines.