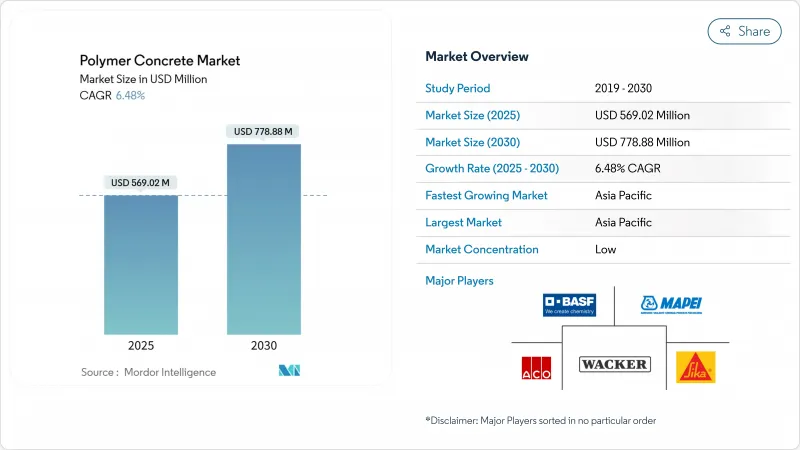

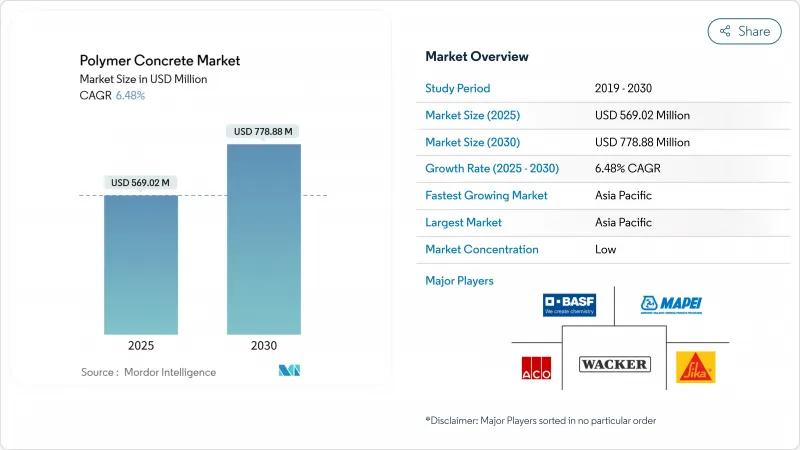

폴리머 콘크리트 시장 규모는 2025년 5억 6,902만 달러로 추정되고, 2030년 7억 7,888만 달러에 이를 것으로 예측되며, CAGR 6.48%로 성장할 전망입니다.

성장은 방청 재료를 선호하는 인프라 강화 프로그램, 데이터센터의 폐수 네트워크에 대한 지속적인 설비 투자, 유틸리티 장비의 비전도성 패드의 사용 확대에 뒷받침됩니다. 아시아태평양의 급속한 도시화, 유럽의 지속가능성에 대한 규제 강화, 바이오 바인더 기술의 진보는 전체적으로 적용 범위를 확대하고 있습니다. 선도적인 제조업체의 전략적 인수는 성능 중심의 배합 업그레이드와 함께 대부분의 지역에서 안정적인 가격 결정력 및 안정적인 마진을 지원합니다.

폴리머 콘크리트는 산과 염에 장시간 노출되어도 초기 강도의 90%까지 유지하기 때문에 지역의 공공 시설은 하수관이나 해수 담수화 플랜트의 철근 콘크리트를 에폭시 결합의 대체품으로 대체하고 있습니다. GCC 국가 정부는 염화물 환경과의 전투에서 고분자 콘크리트를 간선 및 플랜트 용기로 지정합니다. DAW Construction과 Qatar General Projects Company와 같은 지역 건설 회사는 극단적인 온도 변화를 견딜 수 있는 지역 특화형 혼합재를 출시하고 있으며, 폴리머 콘크리트 시장이 장소에 따른 화학적 특성을 활용하여 수명을 보장하고 있다고 이야기하고 있습니다.

에폭시는 2024년 매출의 52%를 차지하였고, 폴리머 콘크리트 시장 내에서 가장 큰 점유율을 차지하며, 2030년까지 CAGR 7.21%로 성장이 예측됩니다. 우수한 접착 강도와 내산성이 이 두 가지 리더십을 지원합니다. 최근의 동적 부하 조사를 통해 에폭시 혼합물은 반복 충격 하에서도 높은 피크 응력을 유지하는 것으로 확인되었으며, 이는 철도의 침목과 다리 포장에 선호되는 특징입니다. 메틸 메타크릴레이트 등급은 교통 장애 비용이 급속히 증가하는 공항 활주로의 급속 경화 보수를 지원합니다. 아크릴레이트계와 라텍스계는 유연한 오버레이나 노후화된 기재에 대한 접착을 위한 작은 틈새를 차지하고 있습니다.

에폭시의 우위성은 첨가제 수요 패턴도 형성하고 있으며, 유리 섬유 및 실리카 분말 공급업체는 수지를 많이 포함하는 매트릭스에 대한 입자 그라데이션을 최적화하도록 촉구하고 있습니다. 폴리에스테르는 비용에 민감한 용도 분야에서 중요성을 유지하지만 압축 강도 한계로 인한 역풍에 직면합니다. 밸류체인 참가자들이 블렌딩 옵션을 확대함에 따라 폴리머 콘크리트 산업은 가격과 성능의 절충에 대응하는 맞춤형 화학물질로부터 이익을 얻고 있습니다.

2024년 점유율은 합성 수지가 80%를 차지했으며, 이는 수십년에 걸친 현장에서의 검증 결과를 반영하고 있습니다. 천연 바인더의 파일럿 연구는 젤라틴 변성 복합재료의 압축 강도가 59.6MPa를 기록하여 기술적 실현 가능성을 나타냈습니다. 순환형 재료에 대한 정부의 우대조치는 키토산, 리그닌, 알긴산을 부분적인 대체 재료로 평가하도록 연구실을 뒷받침하고 있습니다. 이 조사 파이프라인은 2030년까지 천연 수지의 CAGR이 7.56%임을 뒷받침하고 있습니다.

생산자는 화석 유래의 함량을 60%로 억제한 하이브리드 시스템을 도입함으로써 마이그레이션 전략의 매핑을 실시했습니다. 스칸디나비아와 일본의 조기 채용자는 그린 인증을 받은 시민 작품용으로 파일럿 배치를 구입해, 향후 수년에 폴리머 콘크리트 시장에 파급하는 수요 포켓을 만들어 내고 있습니다. 기술 자료는 수지 및 골재와의 상용성, 유동학 제어, 장기 내후성에 계속 초점을 맞추었습니다.

아시아태평양은 2024년에 41.5%의 점유율을 차지했고, 중국의 일대일로(Belt and Road) 회랑의 업그레이드와 인도의 스마트 시티 하수도 개수에 지지되고 있습니다. 지역 연구기관은 국내 제조업체와 협력하여 열대 습도와 황산염이 많은 토양의 배합을 조정하여 지역 공급망을 강화하고 있습니다. 아시아태평양의 폴리머 콘크리트 시장 규모는 폐수 처리 능력의 확대와 급속한 데이터센터 건설에 자극을 받으며 2030년까지 연평균 복합 성장률(CAGR) 7.45%로 확대될 것으로 예측됩니다.

북미는 인프라 투자 및 고용 촉진법(Infrastructure Investment and Jobs Act)이 교량 데크 오버레이, 해안선 보호, 탄력성 있는 에너지 자산에 자금을 제공하고 있기 때문에 안정적인 성장을 유지하고 있습니다. 유럽에서는 엄격한 탄소 규제 및 마이크로 플라스틱 규제에 의해 내구성이 높고 유지관리가 용이한 소재의 채용이 가속하고 있습니다.

중동 및 아프리카에서는 해수 담수화 플랜트, 지역 냉각수로, 화학약품 터미널에서 수요 증가를 기록하고 있습니다. 남미에서는 브라질 항구 확장, 바이오연료 시설 및 광업 자산이 활동의 중심이며, 폴리머 콘크리트는 산성 및 연마성 운전 조건 하에서 수명 주기 절약을 제공합니다.

The polymer concrete market size stood at USD 569.02 million in 2025 and is on track to reach USD 778.88 million by 2030, advancing at a 6.48% CAGR.

Growth is anchored in infrastructure hardening programs that prioritize corrosion-proof materials, sustained capital spending on data-center drainage networks, and expanding use of non-conductive pads for utility equipment. Rapid urbanization in Asia Pacific, tighter European sustainability mandates, and progress in bio-based binder technology collectively widen application scope. Strategic acquisitions by leading producers, coupled with performance-driven formulation upgrades, are underpinning steady pricing power and stable margins in most regions.

Regional utilities are replacing steel-reinforced concrete with epoxy-bound alternatives in sewage mains and desalination plants because polymer concrete retains up to 90% of its initial strength after prolonged acid and salt exposure researchgate.net. GCC governments, contending with aggressive chloride environments, now specify polymer concrete for trunk lines and plant vessels. Local contractors such as DAW Construction and Qatar General Projects Company have launched region-specific mixes that resist extreme temperature swings, illustrating how the polymer concrete market leverages location-tailored chemistry for lifespan assurance

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Epoxy accounted for 52% of 2024 revenue, the largest share within the polymer concrete market, and is projected to rise at a 7.21% CAGR through 2030. Superior bond strength and resistance to acids underpin this dual leadership. Recent dynamic-loading research confirmed that epoxy mixes sustain higher peak stress under cyclic impact, a feature favored in rail sleepers and bridge paving. Methyl methacrylate grades address rapid-set repairs on airport runways where traffic disruption costs escalate quickly. Acrylate and latex systems occupy small niches for flexible overlays and bonding to aged substrates.

Epoxy's dominance also shapes additive demand patterns, encouraging suppliers of chopped glass fibers and silica flour to optimize particle gradation for resin-rich matrices. Polyester retains relevance in cost-sensitive applications but faces headwinds from compressive-strength limits. As value-chain participants broaden formulation options, the polymer concrete industry benefits from tailored chemistries that serve price-performance trade-offs.

Synthetic resin held an 80% share in 2024, reflecting decades of validated field performance. Pilot studies on natural binders recorded 59.6 MPa compressive strength for gelatin-modified composites, signaling technical feasibility. Government incentives for circular materials are pushing laboratories to evaluate chitosan, lignin and alginate as partial replacements. This research pipeline supports a 7.56% CAGR for natural resin through 2030, the fastest rate in the binding-agent hierarchy.

Producers are mapping their transition strategy by introducing hybrid systems that cap fossil-derived content at 60%. Early adopters in Scandinavia and Japan are purchasing pilot batches for green-certified civic works, creating demand pockets that will ripple through the polymer concrete market in the coming years. Technical documentation continues to focus on resin-aggregate compatibility, rheology control, and long-term weathering performance.

The Polymer Concrete Market Report Segments the Industry by Polymer Type (Epoxy, Polyester, and More), Binding Agent (Natural Resin, Synthetic Resin), Application (Asphalt Pavement, Building and Maintenance, and More), End-User Industry (Residential, Commercial, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD Million)

Asia Pacific dominated sales with a 41.5% share in 2024, supported by China's Belt and Road corridor upgrades and India's smart-city sewer rehabilitation. Regional research institutes collaborate with domestic producers to tune formulations for tropical humidity and sulfate-rich soils, reinforcing local supply chains. The polymer concrete market size in Asia Pacific is projected to expand at a 7.45% CAGR through 2030, stimulated by expanding wastewater treatment capacity and rapid data-center construction.

North America maintains steady growth as the Infrastructure Investment and Jobs Act funds bridge deck overlays, shoreline protection, and resilient energy assets. Europe's stringent carbon and micro-plastic regulations accelerate the adoption of durable, low-maintenance materials.

The Middle East and Africa record rising demand in desalination plants, district cooling channels, and chemical terminals. South America's activity centers on Brazil's port expansions, biofuel facilities, and mining assets; polymer concrete offers lifecycle savings under acidic and abrasive operating conditions.