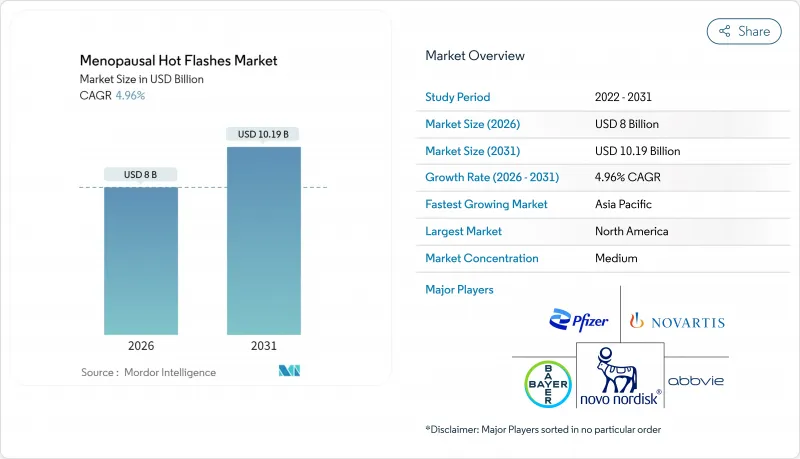

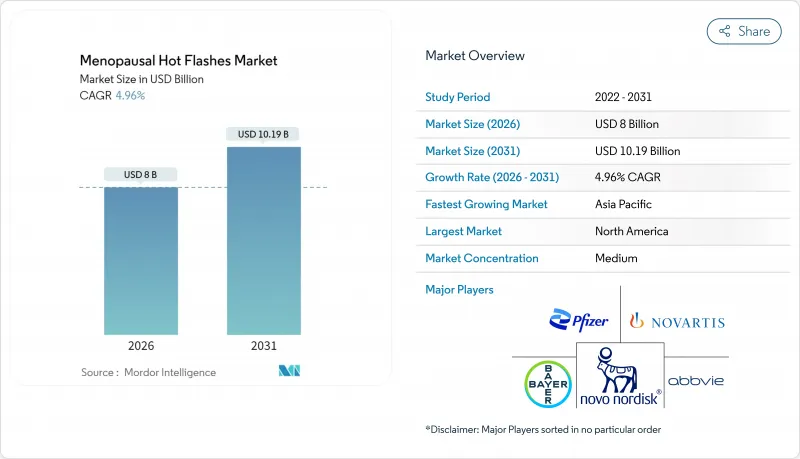

갱년기 안면 홍조 시장 규모는 2026년에 80억 달러로 추정되고 있습니다. 2025년 76억 2,000만 달러에서 성장하여, 2031년에는 101억 9,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지는 CAGR 4.96%로 확대될 전망입니다.

평균 수명이 연장됨에 따라 매년 수백만 명의 여성이 증상을 진단받고 있습니다. 한편, 최초의 NK-3 수용체 길항제와 고급 호르몬 전달 시스템의 등장으로 임상 치료 옵션이 확대되고 있습니다. 동시에 디지털 처방전의 보급, 기업 주도의 건강 증진 프로그램, 신경 펩티드 억제제에 관한 규제의 명확화가 기존의 접근 장벽을 낮추고 있습니다. 이로 인해 갱년기 안면 홍조 시장은 단발 치료에서 예방 증상 관리로 전환하고 있습니다. 다국적 기업이 비호르몬 요법 분야에서 선구자 우위성을 확보하기 위해 경쟁하는 가운데 경쟁 격화가 진행되고 있습니다. 그러나 공급망에 대한 투자와 파트너십 모델 구축을 통해 중소득 국가에서의 치료 보급도 진행되고 있습니다. 이러한 요인들이 결합되어 거시경제 사이클에서 거의 분리된 수요곡선을 강화하여 갱년기 안면 홍조 시장의 매출을 지속적인 성장으로 이끌고 있습니다.

세계의 갱년기 여성 인구는 2030년까지 12억 명에 달할 것으로 예측되며, 이는 갱년기 시장의 장기 확대 경로를 보장합니다. 평균 수명의 증가와 출산 연령의 증가로 갱년기 기간이 연장되어 증상 출현 기간과 치료 요구가 증가하고 있습니다. 일본에서는 관리되지 않은 혈관 운동 증상으로 40대 및 50대 여성의 9%가 노동력을 이탈하고 있다는 생산성 데이터가 나타나 임상 케어를 넘은 경제적 이해관계가 부각되고 있습니다. 미국의 분석에서는 안면 홍조에 직접적으로 기인하는 연간 결근 비용이 18억 달러로 전망되고 있어, 고용주가 건강 증진 예산에 갱년기 케어를 추가하는 동기가 되고 있습니다. 인구동태적인 압력은 치료법의 혁신과는 독립적으로 작용하기 때문에 혁신주기가 둔화되어도 시장에는 지속적인 성장이 발생합니다. 그 결과, 의약품 생산 능력의 계획 책정이나 디지털 지원 서비스는 보험자나 기업 구매 담당자와의 우선 거래처로서의 지위를 목표로 하는 공급자에게 전략적 과제가 되고 있습니다.

2018년부터 2023년까지 여성용 건강 관리 스타트업에 대한 벤처 자금은 314% 증가했으며, 비호르몬 연구 개발, 전문 원격 의료 네트워크, 스마트 패치 기술에 자본이 집중되고 있습니다. 공개회사의 노력도 이러한 동향을 반영하고 있으며, 바이엘은 엘린자네탄트가 피크 시 매출액 10억 달러의 잠재가치를 보유하고 있음을 전망하고, 아스텔라스 제약은 페졸리네탄트트에 22억-34억 달러의 목표를 설정하고 있습니다. 특허 만료 대책으로서 후기 개발 단계의 자산을 취득하는 M&A 활동도 활발히 일어나고 있으며, 코제트 파마슈티컬스가 메인 파마사의 여성용 헬스케어 부문을 4억 3,000만 달러에 인수한 사례가 이 통합의 흐름을 상징하고 있습니다. 자본유입의 시너지 효과로 개발기간 단축, 다시설 공동시험의 가속화가 추진되고, 갱년기 안면 홍조 시장에서의 복약 준수율과 가격 결정력을 모두 확대할 수 있는 병용 요법의 출시 가능성이 높아지고 있습니다.

2002년의 여성 건강 이니셔티브 연구 결과는 여전히 처방 습관에 영향을 미치고 있으며, 현재 미국 데이터에서는 호르몬 요법의 도입률이 약 6%로 침체하고 임상 적응 기준을 크게 밑돌고 있습니다. 새로운 시험을 통해 폐경 후 10년 이내에 치료를 시작하는 여성의 위험과 효용 간의 균형이 확인되고 있음에도 불구하고, 안전성의 우려는 뿌리깊게 남아 있습니다. 페졸리네탄트의 첨부 문서에서는 간기능 모니터링이 의무화되어 임상적인 마찰을 일으키는 것과 동시에 약물요법에 대한 소비자의 경계심을 강화하고 있습니다. 아시아 시장에서는 이 문제가 현저합니다. 증상의 중증도 점수가 서구의 비교 집단과 동등하다는 사실에도 불구하고 동아시아의 갱년기 여성에서 호르몬 요법의 사용률은 7.2%에 불과합니다. 암, 심혈관 위험, 인지기능에 미치는 영향에 대한 지속적인 논의가 유증상 인구의 상당한 비율을 '경과관찰'에 유지시켜 갱년기 안면 홍조 시장의 잠재적 대상층을 축소시키고 있습니다.

2025년 시점에서 갱년기 안면 홍조 시장에서는 호르몬 요법이 점유율 53.68%를 유지하였으며, 광범위한 임상적 인지도와 보험 적용이 뒷받침하고 있습니다. 그러나 비호르몬 치료 카테고리는 2031년까지 연평균 복합 성장률(CAGR) 7.18%로 다른 모든 카테고리를 상회하는 성장이 예상됩니다. 에스트로겐-프로게스테론 요법에 비해 우수한 내성 프로파일을 갖기 때문에 NK-3 수용체 길항제 단독의 갱년기 안면 홍조 시장 내 규모는 예측 기간 종료까지 32억 5,000만 달러를 초과할 수 있습니다. 에스트로겐+프로게스틴 제형은 자궁 내막의 과형성 위험을 줄이기 때문에 호르몬 요법의 기초로 여전히 주류입니다. 한편, 에스트로겐 단독제는 자궁절제술 후의 여성에게 적용됩니다. 에스트로겐이 금지된 환자에게는 SSRI, SNRI, 가바펜티노이드의 병용이 계속되고 있지만, 이는 적응 외 사용이기 때문에 보험 적용 범위나 광고 전개가 제한되고 있습니다. 개발 중인 데이터에 따르면, 엘린자네탄트는 12주 시점에서 위약 대비 30%의 수면 점수 개선과 안면 홍조 빈도 50% 초과 감소를 보였습니다. 허브 보충제는 규제 대상을 벗어나면서 일정한 점유율을 유지하고 있으며, 무작위화 시험의 증거가 제한되는 가운데 소비자들이 '천연' 옵션을 선호하는 경향을 반영하고 있습니다.

비호르몬 요법의 보급 확대에 의해 치료를 포기하고 있던 유방암 생존자나 심혈관 위험을 보유한 환자가 치료를 시작하면서 갱년기 안면 홍조 치료의 대상 환자층이 확대하고 있습니다. 안전성 표시의 성숙과 실세계 데이터의 축적에 따라, 주요 제조업체는 소비자용 직접 캠페인과 의사 교육 환경 조성을 조합한 다각적 프로모션을 전개 중입니다. 더불어, 보험사와의 계약은 성과 기반이 주류가 되어, 결근률의 감소나 수면 관련 병존 질환의 경감에 기여하는 제품이 높이 평가되는 추세에 있습니다. 이러한 요인들이 합쳐져 2031년까지 비호르몬 제제의 매출이 전체의 3분의 1 이상을 차지하고 갱년기 안면 홍조 치료제 업계 전체의 경쟁 구도를 크게 바꿀 수 있습니다.

경구 정제는 2025년 매출의 48.05%를 차지하였으며 이는 갱년기 안면 홍조 시장에서 의사의 친숙한 처방 습관과 성숙한 유통 인프라를 명확하게 보여줍니다. 그러나 경피 흡수 시스템은 양호한 심혈관 위험 프로파일과 복용량 조정의 용이성을 바탕으로 2031년까지 가장 높은 7.28%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 경피 에스트로겐 제제는 초기 통과 효과를 회피하여 혈전 위험을 줄이고 비만과 흡연 경력이 있는 여성에 대한 표준 권장 치료법이 되었습니다. MenoPatch 등의 신규 참가 제품에 의해 임상의는 3-4주간에 투여량을 조정 가능하게 되어, 복약 지속을 방해하기 쉬운 시행착오 기간을 대폭 단축할 수 있습니다.

주사제와 외용제는 엄격한 약동학 관리 및 복합 호르몬 투여를 필요로 하는 특정 환자층에게 여전히 중요하지만, 투여의 복잡성과 통원 비용이 보급의 장벽이 되고 있습니다. 향후 블루투스 대응 복약 준수 추적 기능을 갖춘 스마트 패치로 경피 흡수제의 도입이 더욱 확대될 수 있습니다. 특히 보험자측이 심혈관계의 안전성과 관련된 장기적인 비용 절감 효과를 인식하면 더욱 확대될 전망입니다. 따라서 현재 개발 파이프라인이 예정대로 진행되면 경피흡수제와 관련된 갱년기 안면 홍조 시장 규모는 2031년까지 21억 5,000만 달러를 넘어설 수 있습니다.

북미는 2025년 시점에서 갱년기 안면 홍조 시장에서 매출의 42.10%를 차지하였고, 유리한 환급 제도, 높은 진단률, 비호르몬계 신약의 신속한 도입이 그 배경에 있습니다. FDA의 페졸리네탄트 승인과 엘린자네탄트의 심사 계속으로, 이 지역은 치료 도입의 최전선에 위치하고 있습니다. 고용주는 연간 18억 달러의 생산성 손실을 산정하고 있으며, 인사부문이 갱년기 여성 지원제도에 대한 자금 제공을 촉구함으로써 처방량이 증가하고 있습니다. 캐나다는 미국과 비슷한 움직임을 보였으며, 2024년에 베오자의 승인을 통해 주별 지급자 대상 범위를 통일했습니다. 한편 멕시코에서는 중산층의 확대로 민간보험의 보급이 진행되고 있지만, 기반은 여전히 작은 수준입니다.

아시아태평양은 인구 규모와 문화적 편견의 점진적 해소로 CAGR 6.12%로 가장 빠른 성장을 이루고 있습니다. 일본에서는 갱년기 전문센터가 운영되어 다중 진료과목 제휴에 의한 진료를 제공합니다. 이 대처는 미관리 증상에 의한 연간 생산성 손실이 120억 달러에 이른다는 데이터가 계기가 되고 있습니다. 중국에는 추정 2억 8,000만 명의 갱년기 여성이 존재하지만, 치료 보급률은 불과 5.66%에 그치고 있으며, 원격 의료나 저비용 제네릭 의약품이 보급됨에 따라 성장 여지가 매우 클 것으로 예상되고 있습니다. 호주에서는 의약품 급여 제도(PBS)에 2025년 3개의 치료제를 추가함으로써 자기 부담액이 최대 90% 줄어들어, 다른 아시아태평양 시장이 참고할 수 있는 정책의 모범 사례가 되었습니다. 유럽에서는 전국민 보험 제도가 환자 부담을 경감하고, 유럽 의약품청(EMA)의 심사가 지역 횡단적인 제품 도입을 효율화하고 있기 때문에 완만한 확대가 계속되고 있습니다. 경구 에스트로겐 제형의 공급 중단은 혁신적인 패치와 젤 제형에 새로운 시장 기회를 가져왔습니다. 또한 영국의 기업용 건강 프로그램에서는 북미의 동향과 마찬가지로 갱년기 온라인 진료에 대한 보험 적용이 시작되었습니다. 중동, 아프리카 및 남미 지역은 여전히 보급률이 낮지만 기반은 개선되고 있습니다. 도시화, 여성의 노동력 참여율 상승, 디지털 건강 검사의 도입으로 안면 홍조의 치료에 대한 접근성이 확대되고 있습니다. 그러나 보험제도의 미정비나 문화적 보수주의가 단기적인 보급을 억제하고 있으며, 2031년까지 이 지역의 갱년기 안면 홍조 시장 내 점유율은 10% 미만에 머물 것으로 예측됩니다.

menopausal hot flashes market size in 2026 is estimated at USD 8 billion, growing from 2025 value of USD 7.62 billion with 2031 projections showing USD 10.19 billion, growing at 4.96% CAGR over 2026-2031.

Growing life expectancy is adding millions of women to the symptomatic pool each year, while first-in-class NK-3 receptor antagonists and smarter hormone delivery systems are broadening the clinical tool kit. At the same time, digital prescription fulfillment, employer-backed wellness programs, and regulatory clarity around neurokinin blockers are flattening traditional access barriers, allowing the menopausal hot flashes market to move from episodic care toward proactive symptom management. Competitive intensity is rising as multinational firms race to secure first-mover advantage in non-hormonal categories, yet supply-chain investments and partnership models are also improving therapy availability in mid-income economies. Collectively, these forces reinforce a demand curve that is largely decoupled from macroeconomic cycles and position the menopausal hot flashes market for sustained top-line growth.

The global post-menopausal cohort is projected to touch 1.2 billion women by 2030, guaranteeing a long-run expansion corridor for the menopausal hot flashes market. Extended life expectancy and later childbearing have stretched the post-menopausal window, increasing symptomatic years and therapy needs. In Japan, productivity data show 9% of women in their 40s and 50s leaving the workforce due to unmanaged vasomotor symptoms, underscoring economic stakes that go beyond clinical care. U.S. analyses estimate USD 1.8 billion in annual absenteeism linked directly to hot flashes, motivating employers to add menopause care to wellness budgets. Because demographic pressure operates independently of therapeutic breakthroughs, it gives the market a durable floor even when innovation cycles slow. As a result, capacity planning for drug production and digital support services has become a strategic imperative for suppliers seeking first-call status with payers and corporate buyers.

Between 2018 and 2023 venture funding for women's health startups rose 314%, funneling capital toward non-hormonal R&D, specialized telehealth networks, and smart-patch technologies. Public-company commitments mirror this trend: Bayer values elinzanetant at USD 1 billion in peak sales potential, while Astellas targets USD 2.2-3.4 billion for fezolinetant. M&A activity is also heating up as firms acquire late-stage assets to offset patent cliffs; Cosette Pharmaceuticals' USD 430 million purchase of Mayne Pharma's women's health division exemplifies this consolidation wave. Collectively, capital inflows have shortened development timelines, accelerated multi-center trials, and increased the probability of combo-therapy launches that could expand both adherence and pricing power inside the menopausal hot flashes market.

The 2002 Women's Health Initiative findings still influence prescribing habits; current U.S. data show hormone therapy uptake languishing at roughly 6%, well below clinical eligibility thresholds. Safety anxieties persist even as newer trials confirm benefit-risk balance for women who initiate therapy within 10 years of menopause onset. Fezolinetant's label mandates liver-function monitoring, adding clinical friction and reinforcing consumer wariness toward pharmacologic intervention. Asian markets amplify the issue: only 7.2% of post-menopausal women in East Asia use hormone therapy, despite symptom severity scores comparable to Western cohorts. Ongoing debates about cancer, cardiovascular risk, and cognitive outcomes therefore keep a meaningful share of the symptomatic population in watch-and-wait mode, trimming the addressable share of the menopausal hot flashes market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hormonal therapy retained 53.68% share of the menopausal hot flashes market in 2025, buoyed by extensive clinical familiarity and insurance coverage, yet the non-hormonal category is set to outpace all others at a 7.18% CAGR to 2031. The menopausal hot flashes market size for NK-3 receptor antagonists alone could exceed USD 3.25 billion by the end of the forecast, driven by superior tolerability profiles relative to estrogen-progesterone regimens. Estrogen + progestin combinations remain the hormonal backbone because they mitigate endometrial hyperplasia risk, whereas estrogen-only pills serve women with prior hysterectomy. Parallel usage of SSRIs, SNRIs, and gabapentinoids continues for patients contraindicated for estrogen, although off-label status limits payer support and advertising reach. Pipe-line data show elinzanetant improving sleep scores by 30% over placebo at Week 12 and reducing hot-flash frequency by more than 50%. Herbal supplements keep a visible but unregulated footprint, reflecting consumer preference for "natural" options despite limited randomized-trial evidence.

Scaling up, non-hormonal options help re-engage breast-cancer survivors and cardiovascular-risk patients who had previously abandoned therapy, thereby expanding the overall menopausal hot flashes market addressable population. As safety labeling matures and real-world evidence accumulates, major manufacturers are deploying multipronged promotion that blends direct-to-consumer campaigns with physician-education grants. In parallel, insurer contracts are increasingly outcomes-based, rewarding products that cut absenteeism and reduce sleep-related comorbidities. Combined, these forces could see non-hormonal products command more than one-third of revenue by 2031, materially changing competitive equations across the wider menopausal hot flashes industry.

Oral tablets generated 48.05% of 2025 sales, a clear testament to legacy physician comfort and mature distribution infrastructure inside the menopausal hot flashes market. However, transdermal systems are forecast to record the strongest 7.28% CAGR through 2031, propelled by favorable cardiovascular risk profiles and easier dose tailoring. Transdermal estrogen avoids first-pass hepatic metabolism, reducing thrombotic risk and making it a default recommendation for women with obesity or smoking histories. Market entrants such as MenoPatch allow clinicians to adjust dosing within 3-4 weeks, slashing the trial-and-error period that often frustrates adherence.

Injectable and topical formats remain important for niche patient sets requiring tight pharmacokinetics or combination hormone delivery, yet administration complexity and clinic-visit costs limit widespread uptake. Looking ahead, smart patches with Bluetooth-enabled adherence tracking could push transdermal adoption even higher, especially once payers recognize the long-term savings tied to cardiovascular safety. The menopausal hot flashes market size tied to transdermal modalities may therefore exceed USD 2.15 billion by 2031 if current development pipelines stay on schedule.

The Menopausal Hot Flashes Market Report is Segmented by Treatment Type (Hormonal Treatment and Non-Hormonal Treatment), Route of Administration (Oral, and More), Distribution Channel (Hospital Pharmacies, and More), Menopausal Stage (Perimenopause and Post-Menopause), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 42.10% of menopausal hot flashes market revenue in 2025, underpinned by favorable reimbursement, high diagnosis rates, and rapid incorporation of non-hormonal launches. FDA approvals of fezolinetant and ongoing review of elinzanetant keep the region at the forefront of therapeutic adoption. Employers are quantifying productivity losses at USD 1.8 billion annually, prompting HR departments to fund menopause benefits, which in turn elevate prescription volumes. Canada mirrored U.S. momentum, granting regulatory clearance for Veozah in 2024 and aligning payer coverage across provinces, while Mexico's expanding middle class is improving private-insurance penetration, albeit from a low base.

Asia-Pacific is the fastest-growing theater at a 6.12% CAGR thanks to demographic scale and gradual erosion of cultural stigma. Japan runs dedicated menopause centers that provide multidisciplinary care, an approach spurred by data showing USD 12 billion in annual productivity losses from unmanaged symptoms. China houses an estimated 280 million menopausal women, yet treatment penetration remains just 5.66%, suggesting outsized headroom for growth as telehealth and low-cost generics gain traction. Australia's Pharmaceutical Benefits Scheme addition of three therapies in 2025 slashed out-of-pocket expense by up to 90%, setting a policy template other APAC markets may emulate. Europe sustains moderate expansion as universal healthcare cushions patient costs and EMA reviews streamline pan-regional launches. Supply interruptions in oral estrogen products have opened white-space for innovative patches and gels, while corporate wellness programs in the United Kingdom now reimburse virtual menopause consults, echoing North American trends. Middle East & Africa and South America remain underpenetrated but show improving fundamentals: urbanization, rising female labor-force participation, and digital-health pilots are making hot-flash therapy more accessible. However, limited insurance frameworks and cultural conservatism still temper near-term uptake, keeping regional share below 10% of the menopausal hot flashes market through 2031.