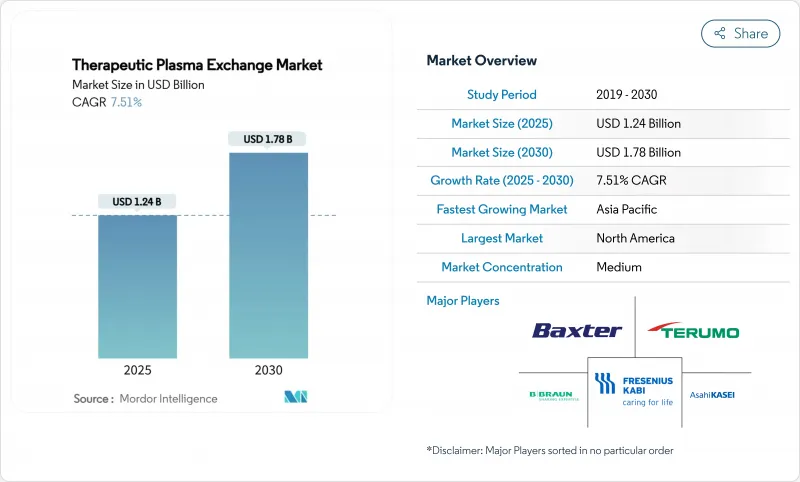

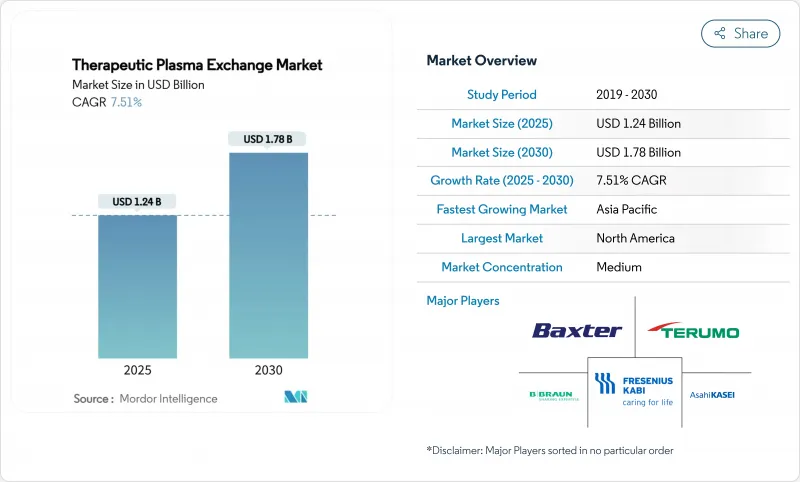

치료적 혈장교환술 시장 규모는 2025년에 12억 4,000만 달러로 평가되었고, 2030년에는 17억 8,000만 달러로 성장할 것으로 예측되며, 예측 기간 중 CAGR은 7.51%를 나타낼 전망입니다.

이러한 확장은 중증 자가면역 및 신경계 질환의 증가하는 유병률, 새로운 적응증에 걸친 임상적 검증 확대, 그리고 병원 중심 절차에서 분산형 및 가정 기반 치료 모델로의 결정적인 전환을 반영합니다. 휴대용 채혈 장치는 치료 시간을 단축하고 감염 노출을 줄이며, 익숙한 환경에서 만성 치료를 받기를 원하는 환자의 선호와 부합합니다. 미국과 서유럽의 보험 적용 확대는 빈번한 시술에 대한 주요 재정적 장벽을 제거했으며, 아시아태평양 지역의 정부 지원 현지화 프로그램은 장비와 소모품 모두의 생산 능력을 증대시키고 있습니다. 선택적 흡착 컬럼과 막 여과의 기술 융합은 공급업체들이 다중 기능 시스템을 요구함에 따라 장비 설계를 재편하고 있습니다. 동시에 FcRn 억제제와 같은 대체 약물군이 경쟁 압력을 강화하면서 장비 제조사들은 소프트웨어, 일회용 소모품, 서비스 계약을 통합된 가치 제안으로 묶어 내놓고 있습니다.

만성 자가면역 질환의 글로벌 발생률은 지속적으로 증가하고 있으며, 길랭-바레 증후군 및 중증 근무력증 환자는 치료용 혈장 교환으로 각각 92%와 81.25%의 반응률을 보였습니다. 의료 시스템은 난치성 재발에 대한 구제 요법으로 혈장 교환을 점점 더 인정하고 있으며, 이 추세는 질병 중증도가 더 높은 고소득 국가의 고령화 인구로 인해 더욱 강화되고 있습니다. 초기 증거는 또한 혈장 교환이 염증 매개체를 제거함으로써 장기 코로나 증상을 완화할 수 있음을 시사하여 환자 풀을 확대하고 있습니다. 이러한 역학적 및 임상적 요인들은 종합적으로 지속적인 시술 수요를 창출하고 다년간의 장비 교체 주기를 뒷받침합니다.

미국 혈장분리학회(ASA)는 2024년 가이드라인에서 87개 질환에 걸쳐 치료적 혈장교환에 1-3등급 권고사항을 부여하며 적응증 범위가 확대되고 있음을 강조했습니다. 2025년 발표된 무작위 연구에서는 교환 시술 후 신경학적 합병증이 있는 코로나19 환자의 사이토카인 수치가 현저히 감소한 것으로 나타났습니다. 이집트 소아과학회 회보의 소아 데이터는 성인과 유사한 안전성 결과를 확인하여 소아에서의 조기 개입을 장려했습니다. 증가하는 증거 기반은 처방자의 주저함을 줄이고 병원 프로토콜 통합을 가속화하며 전 분야에 걸쳐 시술 건수를 점진적으로 증가시킵니다.

최고급 장치는 단위당 10만 달러를 초과하며, 일회용 키트는 시술당 1,000-1,200달러의 추가 비용이 발생합니다. 이는 라틴 아메리카와 아프리카의 소규모 병원들이 감당하기 어려운 수준입니다. 팬데믹 이후 공급망 충격으로 수지 및 막 가격이 상승하여 2024년 컬럼 비용이 15% 증가했습니다. OEM 업체들이 임대, 사용량 기반 요금제, 서비스 번들을 제공하지만, 신흥 경제국의 의료 예산 압박으로 교체 주기가 지연되고 차세대 플랫폼 도입이 미뤄지고 있습니다.

2024년 치료용 혈장 교환 시장 규모에서 채혈기(Apheresis machines)가 48.65%를 차지하며 모든 질환 범주에서 핵심 시술 장비로서의 위상을 입증했습니다. 그러나 의료진이 최소한의 혈장 대체로 선택적 병원체 제거를 요구함에 따라 컬럼 및 흡착기(Columns and adsorbers)는 2030년까지 연평균 9.65% 성장률을 보일 전망입니다. 통합형 장치는 이제 원심 분리 기능과 흡착 카트리지를 결합하여, 동일한 콘솔 내에서 전혈장 제거와 항체 특이적 여과 사이를 전환할 수 있게 합니다. 제조사들은 센서 기반 항응고제 적정, 폐쇄형 시스템 일회용품, 클라우드 기반 성능 분석을 통해 차별화하며, 이를 통해 시술 시간을 35분 미만으로 단축합니다.

반복적 소모품 수익은 여전히 핵심 요소입니다. 튜브 세트, 식염수, 항응고제, 대체 유체는 설치 기반당 고객 생애 가치의 약 60%를 차지합니다. 이에 기존 시장 참여자들은 하드웨어 임대와 장기 소모품 계약을 묶어 예측 가능한 현금 흐름을 확보합니다. 원격 문제 해결 및 프로토콜 라이브러리를 가능하게 하는 소프트웨어 업데이트는 경쟁을 가격에서 플랫폼 생태계 점유율로 전환시켜 고객 의존도를 심화시키고 저비용 신규 진입자의 잠재적 대체 가능성을 억제합니다.

북미는 2024년 치료용 혈장 교환 시장 점유율 41.23%로 우위를 점했으며, 높은 소모품 비용을 상쇄하는 강력한 메디케어 및 민간 보험사 환급 제도가 이를 뒷받침했습니다. 2025년 FDA의 Aurora Xi 혈장분리 시스템 승인에 따라 경쟁이 심화되고 기존 콘솔 간 가격 안정화가 촉진되었습니다. 캐나다 주정부들은 최근 미국 요금과 수수료 체계를 조화시켜 국경 간 시술 유출을 줄이고 국내 수요를 안정화했습니다.

아시아태평양 지역은 8.43%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 중국의 ‘건강중국 2030’ 계획이 300개 군 병원에 혈장분리 인프라를 지원하며 성장 동력을 제공합니다. 테루모의 1,500만 달러(약 200억 원) 항저우 공장 확장은 스펙트라 옵티아 키트의 현지 공급을 확보해 수입 관세를 낮추고 배송 시간을 40% 단축시켰습니다. 일본과 한국은 성숙한 설치 기반을 유지하지만, 인구 고령화와 이식 프로그램 확대로 인한 성장 여력이 남아 있습니다. 인도의 의료 관광 성장으로 경쟁력 있는 혈장 교환 패키지를 제공하는 민간 병원으로 국제 환자가 유입되고 있습니다.

유럽은 꾸준하지만 더딘 확장을 보이고 있습니다. 보편적 보험 적용이 접근성을 높였으나, 2024년 혈장 공급 부족으로 많은 EU 국가들이 원료 혈장의 40%를 미국에서 수입해야 했으며, 이로 인해 유럽혈액연합(European Blood Alliance)은 추가로 200만 명의 기증자를 모집하고 있습니다. 중동 및 아프리카 시장은 초기 단계이지만 걸프협력회의(GCC)의 3차 의료 허브 투자로 지원받고 있으며, 브라질과 아르헨티나는 공공-민간 병원 네트워크를 통해 남미 지역의 도입을 주도하고 있습니다.

The therapeutic plasma exchange market size stands at USD 1.24 billion in 2025 and is projected to grow to USD 1.78 billion by 2030, translating into a 7.51% CAGR during the forecast period.

This expansion reflects rising prevalence of severe autoimmune and neurological diseases, growing clinical validation across new indications, and a decisive shift from hospital-centric procedures toward decentralized and home-based care models. Portable apheresis devices shorten treatment times, reduce infection exposure, and align with patients' preference for receiving chronic therapies in familiar environments. Reimbursement upgrades in the United States and Western Europe have removed major financial barriers for frequent procedures, while government-backed localization programs in Asia-Pacific multiply production capacity for both machines and consumables. Technological convergence of membrane filtration with selective adsorption columns is reshaping equipment design as providers demand systems capable of multiplex functionality. At the same time, alternative drug classes such as FcRn inhibitors are intensifying competitive pressure, spurring equipment manufacturers to bundle software, disposables, and service contracts into integrated value propositions.

Global incidence of chronic autoimmune diseases continues to climb, with Guillain-Barre syndrome and myasthenia gravis patients showing 92% and 81.25% response rates respectively when treated with therapeutic plasma exchange. Healthcare systems increasingly recognize plasma exchange as a rescue therapy for refractory flares, a trend amplified by aging populations in high-income countries where disease severity is greater. Early evidence also suggests plasma exchange may mitigate long-COVID symptoms by removing inflammatory mediators, thereby widening the patient pool. Collectively these epidemiological and clinical factors generate sustained procedure demand and underpin multi-year equipment replacement cycles.

The American Society for Apheresis assigned therapeutic plasma exchange a Category I-III recommendation across 87 diseases in its 2024 guidelines, highlighting broadening indication scope. Randomized studies published in 2025 demonstrated significant reductions in cytokine levels among COVID-19 patients with neurological complications following exchange sessions. Pediatric data from the Egyptian Pediatric Association Gazette confirmed safety outcomes comparable to adults, encouraging earlier intervention in children. Growing evidence base lowers prescriber hesitancy, accelerates hospital protocol integration, and fuels incremental procedural volume across specialties.

Best-in-class devices exceed USD 100,000 per unit, while single-use kits add USD 1,000-1,200 per procedure, costs that small hospitals in Latin America and Africa struggle to justify. Post-pandemic supply chain shocks elevated resin and membrane prices, inflating column costs by 15% in 2024. Although OEMs offer leasing, pay-per-use, and service bundles, strained health budgets in emerging economies translate into slower replacement cycles and deferred adoption of next-generation platforms.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Apheresis machines generated 48.65% of the therapeutic plasma exchange market size in 2024, underscoring their status as the procedural hub across all disease categories. Columns and adsorbers, however, are advancing at a 9.65% CAGR to 2030 as clinicians demand selective pathogen removal with minimal plasma substitution. Integrated devices now combine centrifugal separation with adsorption cartridges, allowing operators to toggle between whole-plasma removal and antibody-specific filtration within the same console. Manufacturers differentiate through sensor-driven anticoagulant titration, closed-system disposables, and cloud-based performance analytics that cut procedure times below 35 minutes.

Recurring consumables revenue remains pivotal: tubing sets, saline, anticoagulants, and replacement fluids contribute nearly 60% of lifetime customer value per installed base. Market incumbents thus bundle hardware leases with long-term consumable contracts, locking in predictable cash flows. Software updates enabling remote troubleshooting and protocol libraries further shift competition from price to platform ecosystem residency, deepening customer dependence and throttling potential displacement by low-cost entrants.

The Therapeutic Plasma Exchange Market Report is Segmented by Product (Apheresis Machines, Filters, Columns & Adsorbers, Disposables, and Software & Services), Indication (Neurological, Cardiovascular, Hematology, Renal, Transplant Rejection, and Other Indications), End-User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America dominated with 41.23% of therapeutic plasma exchange market share in 2024, buoyed by robust Medicare and private-payer reimbursement that offsets high consumable costs. FDA clearance of the Aurora Xi plasmapheresis system in 2025 added competition and fostered price moderation among incumbent consoles. Canada's provinces recently harmonized fee schedules with U.S. rates, reducing cross-border procedure leakage and stabilizing domestic demand.

Asia-Pacific is the fastest-growing region at an 8.43% CAGR, propelled by China's Healthy China 2030 plan that funds apheresis infrastructure in 300 county hospitals. Terumo's USD 15 million Hangzhou facility expansion secures local supply of Spectra Optia kits, lowering import tariffs and slashing delivery times by 40%. Japan and South Korea maintain mature installed bases, yet upside remains from demographic aging and transplant program expansions. India's medical tourism growth funnels international patients into private hospitals offering competitive plasma exchange packages.

Europe shows steady but slower expansion. Although universal insurance coverage facilitates access, plasma supply shortages in 2024 forced many EU countries to import 40% of their raw plasma from the United States, prompting the European Blood Alliance to seek two million additional donors. Middle East and Africa markets are nascent but supported by Gulf Cooperation Council investments in tertiary care hubs, while Brazil and Argentina spearhead South American adoption through public-private hospital networks.