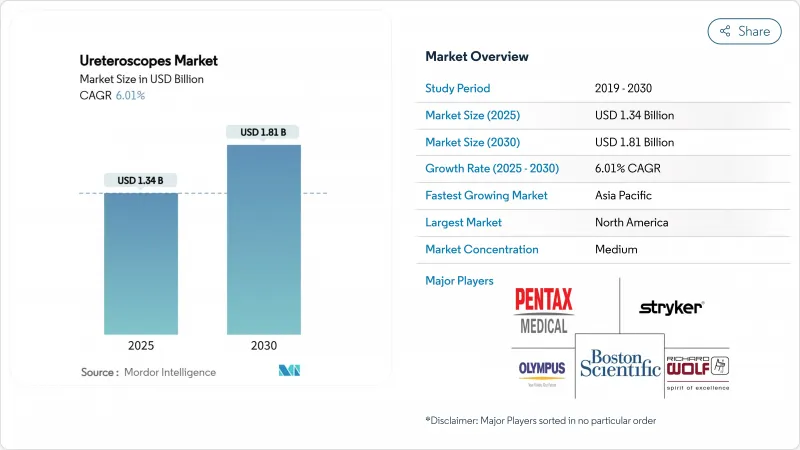

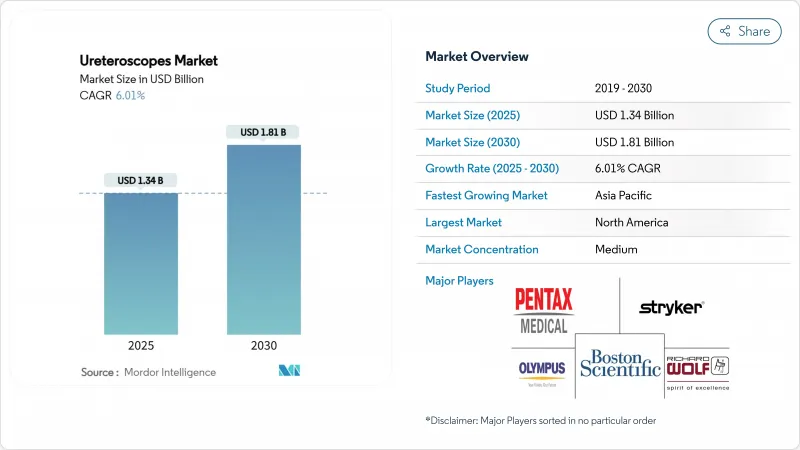

요관경 시장 규모는 2025년에 13억 4,000만 달러로 추정되고, 2030년에는 18억 1,000만 달러에 이를 것으로 예상되며, 예측 기간 CAGR 6.01%로 성장할 전망입니다.

현재의 호황은 신장 결석 발생률의 지속적인 성장, 당일 저침습 처치로의 급속한 시프트, 처치 시간을 단축하면서 가시화를 선명하게 하는 디지털 플렉서블 플랫폼의 잇따른 발매에 연결되고 있습니다. 그러나 외래수술센터(ASC)는 메디케어의 2.9% 외래환자 수수료 인상과 패스스루 코드 C1747의 지속으로 단회 사용 기구의 상환이 인상됨에 따라 보다 신속하게 규모를 확대하고 있습니다. 플렉서블 디지털 스코프가 구매를 독점하고 있는 이유는 보다 넓은 270°의 편향각과 픽셀 밀도가 높은 CMOS 센서가 결석 제거율을 높이고 있기 때문인 반면, 일회용 유형은 감염 대책과 다운타임 제로를 우선하는 환경에서 점유율을 획득하고 있습니다. 경쟁의 격렬함은 기존 기업이 재사용 가능한 포트폴리오를 지키는 것과 병행하여 광학계와 내구성에 있어서 과거의 갭을 없애는 일회용 라인을 데뷔시켜, 요관경 시장 전체의 교환 사이클을 단축함으로써 첨예화하고 있습니다.

신결석의 발생률은 2021년에 1억 600만 증례에 달했고, 현재도 상승을 계속하고 있기 때문에 내시경적 결석 제거 후보자의 파이프라인이 항상 확보되고 있습니다. 미국의 여성 유병률은 2007-2008년 6.5%에서 2017-2020년에는 9.1%로 상승했으며, 벤더는 보다 폭넓은 체격에 적합한 인체 공학을 연마하고 있습니다. 지역적인 움직임도 다양합니다. : 동유럽과 중앙아시아에서는 증례 수가 증가하고 있지만, 동아시아의 여러 나라에서는 완만한 감소가 보고되고 있으며, 그에 따라 판매 목표도 변경되고 있습니다. 연간 300만 건이 넘는 소아 결석증은 요관 외상을 억제하는 초소형 샤프트에 대한 수요를 부추겨 요관경 시장의 장기적인 성장을 지원하고 있습니다.

유럽비뇨기과학회 가이드라인에서는 20mm 이하의 결석에 대해서는 충격파 치료보다 요관경 검사를 권장하고 있으며, 81%-94%의 무결석률을 들고 있습니다. 당일 퇴원은 시설 비용을 절감하고, ASC의 처리 능력을 향상시키며, 머신러닝 알고리즘은 사례 선택을 간소화하고, 수술 중 예기치 않은 상황을 감소시킵니다. 이러한 요인을 결합하면 수술 건수가 증가하고 요관경 시장의 확대가 촉진됩니다.

최신 디지털 플렉서블 스코프는 20,000달러를 넘는 경우가 많으며, 연간 서비스 비용이 6,000-8,000달러 걸리기 때문에 자금난을 겪는 병원에서는 경원됩니다. 디스포저블은 수리비를 절약할 수 있지만, 1회의 처치에 드는 비용은 신흥국에서는 현지의 관세를 상회할 수 있어 요관경의 보급을 늦추고, 요관경 시장의 확대를 억제하고 있습니다.

2024년에는 요관경 시장의 58.11%를 유연한 설계가 차지하고 칼리시의 가시화를 촉진하는 픽셀 고밀도 센서와 사전 확장 없이 접근을 용이하게 하는 7.5Fr의 초슬림 샤프트에 의해 지원되고 있습니다. 2025년 5월에 발표된 6.3Fr과 7.5Fr의 일회용 스코프를 비교한 다시설 공동연구에서는 무결석률은 각각 95%와 92.9%로 보다 소형 장치로 수술 시간이 4.5분 단축되었습니다. 내구성이 중시되는 세밀리지드 시스템은 CAGR 9.21%로 성장하지만, 이는 예산에 민감한 병원이 저위험의 진입점으로 간주해 요관경 시장 전체의 규모를 미묘하게 끌어올리고 있기 때문입니다.

제조업체는 현재 광학계뿐만 아니라 소프트웨어로 차별화를 도모하고 있습니다. 보스턴 과학의 압력 모니터 층과 올림푸스의 EDOF 이미지는 입찰 결과에 영향을 미치는 부가가치 경로를 보여줍니다. 메타감사에 따르면 샤프트 지름의 세대 축소는 요관확장술의 감소 및 입원 기간의 단축과 관련이 있어 요관경 시장 전체의 건전한 교환 시기를 촉진하고 있습니다.

재사용 범위가 71.51%의 점유율을 유지하는 이유는 대량 생산 센터가 자본을 신속하게 감가 상각하고 확립된 재처리 프로토콜을 강조하기 때문입니다. 그러나 일회용 기구는 수술 후 감염률의 저하나 수리 다운타임 제로와 관련된 데이터에 밀려 CAGR 10.1%로 확대되고 있습니다. 오토클레이브가 없는 ASC에서는 휴대용 유형으로 고도의 결석 파쇄가 가능해 분산형 복도에서의 요관경 시장 규모가 확대됩니다.

비뇨기과의의 59.11%가 가격을 주요 장벽으로 하고 있지만, 총소유비용 조사에서는 수리, 멸균 노력, 스코프 손실을 집계하면 동등합니다. 리토뷰 엘리트의 270° 편향과 Full HD 센서는 많은 재사용 가능한 벤치마크와 비교하여 채용 곡선을 부드럽게 합니다.

미국 성인의 신결석 유병률이 9.25%인 것, 디지털 스코프가 널리 보급되고 있는 것이 배경에 있습니다. 2025년 외래 환자에 대한 지불은 ROI를 강화하고 대학 병원과 ASC 모두 함대 갱신을 촉구합니다. LithoVue Elite와 같은 실시간 압력 모니터 모델은 복잡한 사례를 관리하는 데 도움이 되어 프리미엄 제품에 대한 수요를 확고히 합니다.

유럽은 2위입니다. 영국과 독일에서는 일회용의 도입이 활발하고, 반대로 스칸디나비아의 바이어는 환경 지표를 중시해, 일회용의 성장을 억제하고 있습니다. 남유럽과 동유럽은 근대화 자금을 통해 잠재 수요를 발굴하고 요관경 시장의 존재감을 대륙 전체로 넓혀가고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 7.11%로 가장 급성장이 예상되고 있는 지역입니다. 일본과 한국은 재빨리 초박형 디지털 스코프를 채용해 인도는 민간병원 붐으로 수량이 늘고 있습니다. 가격대가 다르기 때문에 공급업체는 포트폴리오를 맞춤설정해야 하며 요관경 시장 규모는 프리미엄 부문 및 비용 중심 부문 모두에서 확대됩니다.

The ureteroscope market size is pegged at USD 1.34 billion in 2025 and is projected to reach USD 1.81 billion by 2030, equating to a 6.01% CAGR for the period.

The current upswing is tied to sustained growth in kidney-stone incidence, a rapid shift toward same-day minimally invasive procedures, and a succession of digital flexible platform launches that sharpen visualization while trimming procedure time. Hospitals still anchor procedure volume; however, ambulatory surgical centers (ASCs) are scaling faster as Medicare's 2.9% outpatient rate hike and the continued pass-through code C1747 lift reimbursement for single-use devices. Flexible digital scopes dominate purchasing because wider 270° deflection angles and pixel-dense CMOS sensors elevate stone-free rates, while single-use variants win share in settings that prioritize infection control and zero downtime. Competitive intensity has sharpened as incumbents defend reusable portfolios and, in parallel, debut disposable lines that erase historic gaps in optics and durability, shortening replacement cycles across the ureteroscope market.

Kidney-stone incidence hit 106 million cases in 2021 and continues to climb, providing a constant pipeline of candidates for endoscopic stone removal. The gender gap narrows each year; U.S. prevalence among women rose from 6.5% in 2007-2008 to 9.1% in 2017-2020, prompting vendors to refine ergonomics that suit broader anatomies. Regional dynamics vary: Eastern Europe and Central Asia register rising case loads, whereas several East-Asian nations report modest declines, steering sales targets accordingly. Pediatric stone disease, exceeding 3 million annual cases, fuels demand for ultra-miniature shafts that limit ureteral trauma, underpinning long-term growth in the ureteroscope market.

European Association of Urology guidelines now recommend ureteroscopy ahead of shock-wave therapy for stones under 20 mm, citing stone-free rates between 81%-94%. Same-day discharge cuts facility costs and boosts ASC throughput, while machine-learning algorithms streamline case selection, reducing intra-operative surprises. Combined, these factors enlarge procedural volume, reinforcing expansion of the ureteroscope market.

A modern digital flexible scope often exceeds USD 20,000 and carries USD 6,000-8,000 in annual service, deterring cash-strapped hospitals. Although disposables bypass repair bills, their per-procedure expense can outstrip local tariffs in emerging economies, slowing uptake and tempering ureteroscope market expansion.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Flexible designs held 58.11% of the ureteroscope market in 2024, buoyed by pixel-dense sensors that boost calyceal visualization and ultra-slim 7.5 Fr shafts that ease access without prior dilation. A multicenter study published in May 2025 comparing a 6.3 Fr and 7.5 Fr disposable scope logged stone-free rates of 95% and 92.9%, respectively, and shaved operative time by 4.5 minutes with the smaller device. Semi-rigid systems, prized for durability, grow at 9.21% CAGR because budget-sensitive hospitals regard them as a low-risk entry point, subtly lifting overall ureteroscope market size.

Manufacturers now differentiate through software rather than optics alone. Boston Scientific's pressure-monitoring layer and Olympus's EDOF imaging illustrate value-add pathways that influence tender outcomes. Meta-audits show a generational decline in shaft diameter correlating with fewer ureteral dilations and shorter hospital stays, fostering healthy replacement timelines across the ureteroscope market.

Reusable scopes retain 71.51% share because high-volume centers amortize capital quickly and value established reprocessing protocols. Yet single-use devices expand at a 10.1% CAGR, propelled by data linking disposables to lower post-operative infection rates and zero repair downtime. Portable form factors allow ASCs lacking autoclaves to perform advanced lithotripsy, widening ureteroscope market size in decentralized corridors.

Cost divides opinion: 59.11% of urologists cite price as the prime barrier, but total-cost-of-ownership studies show parity once repair, sterilization labor, and scope loss are tallied. Optical parity debates have subsided; LithoVue Elite's 270° deflection and full-HD sensor now match many reusable benchmarks, smoothing adoption curves.

The Ureteroscope Market Report is Segmented by Product (Flexible Ureteroscopes and Semi-Rigid Ureteroscopes), Usability (Single-Use/Disposable Ureteroscopes and Reusable Ureteroscopes), Application (Urolithiasis, and More), End User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained a 38.11% share of the ureteroscope market in 2024, fueled by 9.25% kidney-stone prevalence among U.S. adults and broad coverage for digital scopes. The 2025 outpatient payment bump bolsters ROI, encouraging both academic hospitals and ASCs to refresh fleets. Realtime pressure-monitoring models such as LithoVue Elite help manage complex cases, cementing premium-product demand.

Europe ranks second. Single-use uptake is brisk in the United Kingdom and Germany; conversely, Scandinavian buyers weigh environmental metrics, tempering disposable growth. Southern and Eastern Europe unlock latent demand via modernization funds, broadening ureteroscope market presence across the continent.

Asia-Pacific is the fastest-growing region at a 7.11% CAGR through 2030. China's centralized value-based procurement compresses pricing yet drives bulk orders; Japan and South Korea adopt ultra-slim digital scopes early, while India's private-hospital boom fuels volume growth. Divergent price tiers oblige suppliers to tailor portfolios, enlarging ureteroscope market size across both premium and cost-sensitive segments.