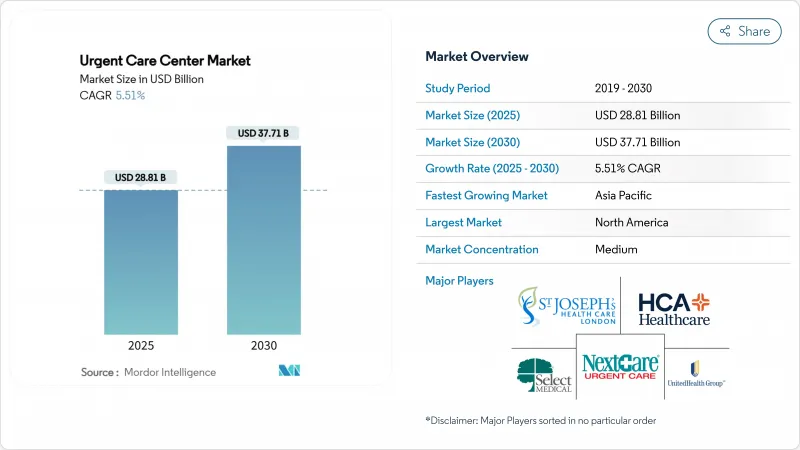

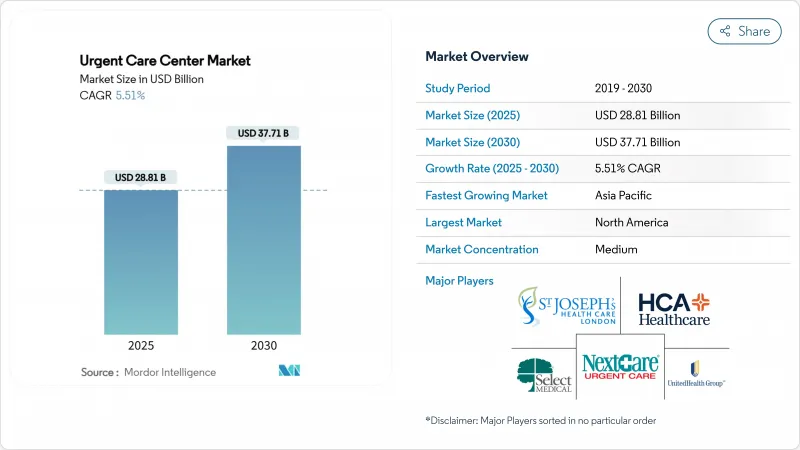

응급진료센터 시장 규모는 2025년에 288억 1,000만 달러로 평가되었고, 2030년에 377억 1,000만 달러에 이를 것으로 예측되며, 예측 기간의 CAGR은 5.51%를 나타낼 전망입니다.

해당 분야의 성장 동력은 응급진료센터 과밀화, 유통 체인과 의료 시스템 간 협력, 디지털 예약 시스템의 급속한 확산을 반영하며, 이 모든 요소가 환자를 저비용 당일 진료로 유도하고 있습니다. 기업형 체인들은 표준화된 진료 프로토콜을 통해 규모의 경제를 유지하는 한편, 병원 소유 시설들은 입원 병목 현상 해소와 진료 의뢰 체계 강화 목적으로 신규 진료소 개설을 가속화하고 있습니다. 서비스 구성 변화는 뚜렷합니다. 외상 치료가 여전히 가장 많은 내원량을 차지하지만, 운영사들이 진료소를 일차 진료 전초 기지로 재편함에 따라 예방접종 및 예방 서비스가 현재 가장 빠르게 성장하고 있습니다. 운영사들이 5,700만 명의 주민이 병원 기반 서비스에 대한 적절한 접근성을 갖추지 못한 농촌 지역으로 방향을 전환함에 따라 지리적 범위가 확대되고 있습니다. 강화된 통합, 확대되는 고급 실무 의료진(APP) 인력 수요, 가치 기반 보험 플랜의 보상 압박은 2030년까지 경쟁 역학을 형성할 것입니다.

응급진료센터 대기 시간 중앙값은 2014년 이후 16% 증가하여, 낮은 중증도의 환자들이 동등한 치료를 더 낮은 비용으로 제공할 수 있는 응급진료센터로 유입되고 있습니다. RAND 연구에 따르면 비응급 응급진료센터 내원 사례의 1/3을 전환할 수 있으며, 이를 통해 연간 최대 44억 달러를 절감할 수 있을 것으로 추정됩니다. 이에 병원들은 통합 의료 네트워크 내에 응급진료센터를 편입하며, 기존 경쟁사들을 응급진료센터 혼잡 완화를 위한 처리량 협력사로 전환하고 있습니다. 가치 기반 계약이 불필요한 응급진료센터 이용을 불이익으로 삼으면서, 보험사들의 진료 장소 최적화 추진이 이러한 전환을 가속화하고 있습니다. 수요 측면과 보험사 측면의 이러한 촉진요인들은 응급진료센터 시장의 꾸준한 수요 증가를 보장합니다.

인공지능 엔진이 환자 접수, 진료 시간대 활용, 문서화를 조정합니다. CityMD의 Notable과의 다년간 협약은 연간 400만 건의 진료를 처리하는 약 200개 클리닉의 프런트엔드 업무를 자동화하며, 이는 2019년 이후 60%의 진료 급증과 맞물립니다. 설문조사에 따르면 현재 소비자의 55%가 디지털 채널을 선호하며, 74%는 예약 속도를 결정적 요소로 꼽습니다. 2022년 성인 텔레헬스 이용률은 39.3%에 달했으며, 80.5%는 기술적 장애를 경험하지 않았고 4분의 3은 방문 품질이 대면 진료와 동등하다고 평가했습니다. “원격 무제한” 모델은 가상 대기실을 없애며, 이용자의 76%가 멀티태스킹 자유를 선호하고 세션당 55분을 절약합니다. 따라서 디지털 역량은 환자 처리량을 높이고 순추천지수(NPS)를 향상시키며, 응급진료센터 시장 내 경쟁 차별화를 공고히 합니다.

미국인의 13%가 일차 진료 부족 지역에 거주하며, 2030년까지 의사 부족 규모는 4만 9,000명에 달할 전망입니다. APP(고급의료실무자) 채용은 이 격차를 완화한다(의료기관의 63%가 2025년 신규 APP 역할 추가 예정). 그러나 외래 진료 시설 중 정식 온보딩 시스템을 갖춘 곳은 70%에 불과합니다. 농촌 지역 응급진료센터의 27%에서 응급의사가 부족하여, 응급 진료 센터는 더 적은 인력으로 진료 인력 커버리지를 확대해야 합니다. APP 활용도가 높아질수록 생산성은 증가하지만, 인재 확보 경쟁으로 인건비가 상승하고 클리닉 확장 속도가 둔화되어 응급 진료 센터 시장의 연평균 성장률(CAGR)이 제한될 수 있습니다.

외상 및 부상 치료는 2024년 매출의 32.23%를 차지하며, 응급진료센터 시장의 임상 서비스 구성에서 지속적인 핵심 영역임을 입증했습니다. 현장 X선 촬영, 골절 고정, 열상 봉합은 응급진료센터(ED) 환자를 분산시키고 유리한 지불자 경제성을 제공합니다. 급성 질환 관리는 두 번째로 높은 비중을 차지하며, 호흡기 및 위장관 질환을 신속하게 처리합니다. 진단 기술 발전에는 초음파 및 고급 영상 검사가 포함되어 평균 진료 비용을 높이고 있습니다.

예방접종 및 예방 서비스는 7.12%의 연평균 성장률(CAGR)로 가장 빠르게 확장되며, 센터를 단발성 진료 장소에서 종합 건강 관리 거점으로 재편하고 있습니다. 대규모 예방접종 캠페인과 여행의학 패키지는 예약 공백을 메우며, 인공지능 기반 분류 시스템은 표준화된 진료를 지원합니다. 세다스-시나이 연구에 따르면 가상 응급진료 알고리즘이 일반적인 증상에 대한 치료 적절성 평가에서 의사보다 우수한 성적을 보였으며, 이는 의사 결정 지원 시스템 도입의 타당성을 입증합니다. 예방 서비스의 성장세는 만성질환 검진 및 생활습관 코칭에 대한 파급 수요를 창출하며, 전국적 및 지역적 차원에서 응급진료센터 시장 내 교차판매 가능성을 높입니다.

북미 지역은 병원 외부 진료에 대한 보험 보상 제도와 확고한 클리닉 체인망에 힘입어 2024년 매출의 48.32%를 차지했습니다. 통합 기업들은 교외 지역 내 공백 시장 기회를 지속적으로 노리는 한편, 5,700만 명의 주민이 여전히 의료 서비스 부족 상태인 농촌 카운티로 사업 방향을 전환하고 있습니다. 캐롤라이나 주 전역의 CON 개혁과 테네시 주의 단계적 규제 완화는 확장을 용이하게 하고 타주 운영자의 진입을 유도하여 해당 지역 내 응급진료센터 시장 규모를 강화하고 있습니다.

아시아태평양 지역은 6.53%라는 가장 높은 연평균 성장률(CAGR) 전망을 제공합니다. 중국의 고령화 인구, 인도의 2억 7,500만 건 이상의 eSanjeevani 상담, 일본의 강력한 원격의료 도입은 응급진료의 타당성을 입증합니다. 공공-민간 협력은 물리적 클리닉과 교통 허브에 위치한 디지털 분류 키오스크를 결합하여, 미국 교외형 모델을 반영한 대량 저중증 환자 처리 모델을 창출합니다.

유럽, 중동 및 아프리카, 남미는 중간 수준의 성장을 기록합니다. 유럽의 보편적 의료 시스템은 민간 지불 규모를 제한하지만, 국경 간 원격의료와 외국인 커뮤니티가 틈새 수요를 유지합니다. 걸프 국가들은 의료 관광 회랑 내에 응급진료 시설을 배치하는 반면, 브라질과 콜롬비아는 민간 병원 내 혼합형 응급진료센터-응급진료 모델을 시험 중입니다. 통화 변동성과 규제 불투명성은 확장 속도를 늦추지만, 위험 감수성 투자자에게 지역별 프랜차이즈 진출 경로를 열어줍니다.

The urgent care center market size stands at USD 28.81 billion in 2025 and will reach USD 37.71 billion by 2030, advancing at a 5.51% CAGR over the forecast period.

Sector momentum reflects emergency-department overcrowding, partnerships between retail chains and health-systems, and rapid digital scheduling uptake, all of which steer patients toward lower-cost same-day care. Corporate chains keep scale advantages through standardized clinical protocols, while hospital-owned facilities accelerate site openings to relieve inpatient bottlenecks and to tighten referral loops. Service-mix evolution is unmistakable: trauma care still attracts the largest visit volumes, yet vaccination and preventive offerings now grow fastest as operators reposition sites as frontline primary-care hubs. Geographic reach broadens as operators pivot to rural communities where 57 million residents lack adequate access to hospital-based services. Heightened consolidation, expanding advanced-practice provider (APP) staffing needs, and reimbursement pressure from value-based insurance plans will shape competitive dynamics through 2030.

Median emergency-department wait times have risen 16% since 2014, funneling lower-acuity patients toward urgent care centers that can deliver equivalent treatment at lower cost. RAND research estimates that one-third of non-urgent ED encounters could be redirected, saving up to USD 4.4 billion annually. Hospitals consequently embed urgent care sites inside integrated delivery networks, transforming former competitors into throughput partners for ED de-congestion. Payer push toward site-of-care optimization reinforces the shift, as value-based contracts penalize unnecessary ED utilization. Collectively these demand-side and payer-side forces lock in steady volume growth for the urgent care center market.

Artificial-intelligence engines orchestrate patient intake, slot utilization, and documentation. CityMD's multi-year pact with Notable automates front-end tasks for nearly 200 clinics handling 4 million visits each year, coinciding with a 60% visit surge since 2019. Surveys show 55% of consumers now prefer digital channels and 74% rate appointment speed as decisive. Telehealth reached 39.3% adult utilization in 2022; 80.5% experienced no technical glitches and three-quarters deemed visit quality equal to in-person care. "Tele-untethered" models remove virtual waiting rooms, with 76% of users favoring freedom to multitask and saving 55 minutes per session. Digital capacity therefore heightens patient throughput, lifts net promoter scores, and entrenches competitive differentiation inside the urgent care center market.

Thirteen percent of Americans live in primary-care shortage areas, and the shortfall may swell to 49,000 physicians by 2030. Employing APPs mitigates gaps-63% of medical groups intend to add new APP roles in 2025-yet formal onboarding exists in only 70% of ambulatory sites. Rural EDs lack emergency physicians in 27% of counties, pushing urgent care centers to stretch clinician coverage with leaner staffing ratios. Productivity rises when APP penetration deepens, but competition for talent inflates labor costs and may slow clinic roll-outs, tempering the urgent care center market CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Trauma and injury care accounted for 32.23% of 2024 revenue, underscoring an enduring core at the urgent care center market's clinical mix. On-site X-ray, fracture stabilization, and laceration repair divert patients from EDs and offer favorable payer economics. Acute illness management ranks second, handling respiratory and gastrointestinal conditions with rapid throughput. Diagnostic advances now include ultrasound and advanced imaging, raising average ticket size.

Vaccination and preventive offerings expand fastest at a 7.12% CAGR, reshaping centers from episodic venues to comprehensive health destinations. Mass immunization campaigns and travel medicine bundles fill scheduling valleys, while AI-driven triage engines support standardized care. A Cedars-Sinai study found virtual urgent care algorithms outscored physicians for treatment appropriateness on common complaints, validating decision-support adoption. Preventive momentum creates spillover demand for chronic-condition screening and lifestyle coaching, elevating cross-sell potential within the urgent care center market size at both national and local levels.

The Urgent Care Center Market Report is Segmented by Service (Trauma/Injury Care, and More), Ownership (Corporate Chains, Hospital/Health-System Owned, Physician Group Owned, Other Ownerships), Age Group (Pediatrics 0-17 Yrs, Adults 18-64 Yrs, Geriatrics 65+ Yrs), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 48.32% of 2024 revenue, underpinned by insurance mechanisms that reimburse out-of-hospital encounters and by well-established clinic chains. Consolidators continue to target suburban infill opportunities while pivoting toward rural counties where 57 million residents remain underserved. CON reform across the Carolinas, plus Tennessee's phased deregulation, eases expansion and invites cross-state operator entries, fortifying the urgent care center market size within the region.

Asia-Pacific provides the sharpest 6.53% CAGR outlook. China's aging demographic, India's 275-million-plus eSanjeevani consultations, and Japan's robust telemedicine adoption validate urgent care viability. Public-private partnerships blend physical clinics with digital triage kiosks located in transit hubs, yielding high-volume low-acuity throughput models that mirror U.S. suburban prototypes.

Europe, Middle East & Africa, and South America log moderate growth. European universal-care systems restrict private pay volumes, yet cross-border telehealth and expatriate communities sustain niche demand. Gulf nations deploy urgent care inside medical-tourism corridors, while Brazil and Colombia flirt with hybrid ED-urgent models inside private hospitals. Currency volatility and regulatory opacity temper speed of scale-out but open localized franchise pathways for risk-tolerant investors.