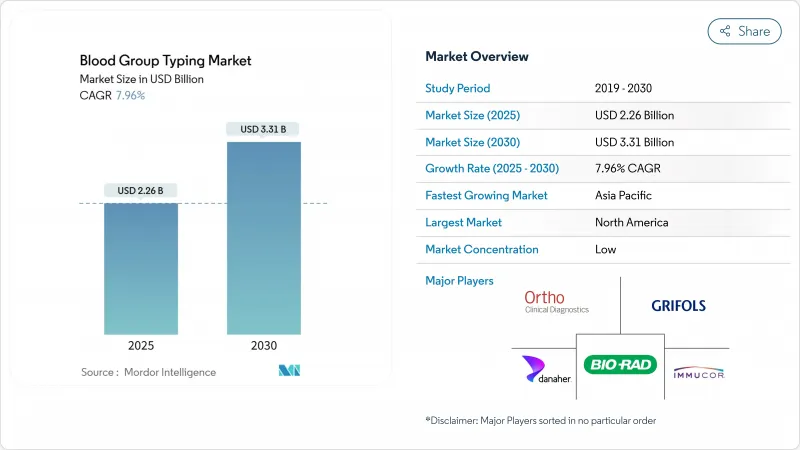

혈액형 검사 시장 규모는 2025년에 22억 6,000만 달러로 추정되고, 2030년에는 33억 1,000만 달러에 이를 것으로 예측되며, CAGR 7.96%로 성장이 전망됩니다.

이 꾸준한 확대를 지원하는 것은 수술 건수 증가, 평균 수명의 연장, 정밀 수혈 프로토콜로의 임상적 시프트입니다. 높은 처리량의 혈청 분석기부터 차세대 시퀀싱(NGS) 플랫폼에 이르기까지 급속한 기술 도입은 검사 정확도 및 처리량을 향상시켜 실험실이 복잡한 항체 검사를 며칠이 아닌 몇 시간 내에 해결할 수 있도록 합니다. 또한 특히 아시아태평양에서는 정부 자금에 의한 헌혈 활동으로 수요가 증가하여 수집된 대량의 혈액을 표준화된 검사 워크플로우로 흘릴 수 있습니다. 자동화는 검사실의 인력 부족으로 인한 갭을 메우고 있으며, 장비 벤더는 로봇 공학, 고급 광학계, 인공지능을 통합하여 보다 신속한 결과와 검사별 비용 절감을 실현하고 있습니다. 북미와 유럽에서는 병원의 통합이 진행되고 있으며 장비, 시약, 미들웨어, 아웃소싱된 레퍼런스 서비스를 하나의 구매 계약으로 통합하는 통합 플랫폼이 더욱 선호되고 있습니다.

복잡한 심혈관 치료, 외상, 종양 치료가 보편화됨에 따라 세계 수혈량은 증가의 길을 가고 있습니다. 수혈 에피소드별로 복수의 적합성 검사가 이루어지기 때문에 약간의 수기 횟수가 증가해도 시약이나 기기 수요가 확대됩니다. 응급의료는 현재 ABO-Rh형을 5분 이내에 처리할 수 있는 포인트 오브 케어 분석 장치가 필요합니다. 따라서 자동화된 워크플로우는 3차 센터와 지역 외상 네트워크 모두에서 수동 튜브 검사를 대체합니다.

사라세미아, 겸상 적혈구증, 혈액암에 대한 장기 수혈 지원은 기본적인 ABO-Rh 매칭에서 확장 항원 페노타이핑으로 일상 진료를 재구성하고 있습니다. 단일 검사에서 여러 혈액형 유전자좌를 읽는 분자 분석은 특히 다회 수혈 소아 환자에서 심각한 위험인 동종 면역을 제한합니다. 종양학 프로토콜은 화학요법 주기 동안 수혈 반응을 상쇄하기 위해 예방적 검사도 채용되고 있습니다.

일관성 없는 전력, 불충분한 콜드체인 능력 및 부족한 유지 보수 전문 지식은 아프리카와 남아시아 농촌 지역 시설의 상당한 비율로 신뢰할 수 있는 혈액형 검사을 방해합니다. 자본 투자 장애물은 NGS와 중견 자동 혈청 검사 시스템의 채택을 지연시키고 많은 시설이 감도가 낮은 수동 슬라이드 검사 및 신속 카드 검사에 의존하지 않을 수 없습니다.

소모품은 2024년 혈액형 검사 시장 점유율의 48.32%를 차지했는데, 이는 일상적인 겔 카드 및 마이크로플레이트 검사에 사용되는 시약의 빈도가 높음을 반영합니다. 그러나 NGS 기반 항원 패널과 희소 항체의 동정을 외주하는 검사실이 늘어나고 있기 때문에 서비스 카테고리는 2030년까지 연평균 복합 성장률(CAGR)이 10.45%가 될 것으로 예측됩니다. 이러한 아웃소싱 동향은 혈액형 검사 시장 규모를 확대하고, 전문적인 레퍼런스 제공업체의 대부분은 물류, 시퀀싱, 해석 보고서를 구독 계약에 따라 패키징하고 있습니다. 검사 장비는 시약 사용을 최적화하고 병원의 LIS 플랫폼과 직접 인터페이스하는 AI 대응 분석기로의 업그레이드에 견인되어 한 자리 대 중반의 성장을 유지하고 있습니다.

실험실 관리자는 NGS의 자본 집약적 특성을 선적 도입의 주된 이유로 꼽았습니다. 한편, 시약 공급업체는 자동 분석기가 미량 반응 패드를 보다 절약적으로 사용하게 되어 가격 압력에 직면하고 있습니다. 그럼에도 불구하고 총 검사량 증가로 겔 카드, 완충액, 대조군 혈청의 안정적인 수익원이 확보되었습니다. 장비 제조업체는 96 웰에서 384 웰까지 확장 가능한 모듈식 설계를 통해 차별화를 도모하고 계절에 따라 변동하는 수요에 대응하는 생산 능력을 확보하고 있습니다.

PCR 및 마이크로어레이 플랫폼은 2024년 부문 수익의 37.23%를 달성했지만 NGS는 항원 커버리지의 깊이를 반영하여 12.45%의 연평균 복합 성장률(CAGR)로 상승할 것으로 예측됩니다. NGS 시약의 혈액형 검사 시장 규모는 여전히 기존의 혈청학적 시약보다 낮지만, 레퍼런스 센터에서의 급속한 보급으로 인해 그 차이가 줄어들고 있습니다. 다중 유전자좌 시퀀싱은 단일 분석으로 Rh, Kell, Kidd, Duffy의 돌연변이를 해결하고 만성적으로 수혈되는 환자의 정밀 매칭 정책을 지원합니다.

혈청학적 검사는 여전히 당일 ABO-Rh 검사의 최전선의 주력이지만, 임상의는 현재 복잡한 표현형 판정에는 NGS에 의한 확인이 필수적이라고 생각하고 있습니다. Microfluidics와 래터럴 플로우 카세트는 필요한 교육을 최소화하기 때문에 자원이 제한된 환경과 긴급한 발판이 됩니다. 따라서 하이브리드 워크플로가 일반적입니다. 슬라이드 또는 컬럼 응집 시험을 통해 즉시 적합성을 확인하고 하루 후에 NGS 데이터가 도착하여 확장 적합성 판정을 정교하게 합니다.

북미는 엄격한 규제 감독, 높은 헬스케어 지출, 전자동 면역 혈액 검사를 우선하는 성숙한 병원 네트워크를 통해 2024년 매출의 33.45%를 차지하고 있습니다. 2025년에 혈청학 및 분자생물학 통합 워크스테이션이 FDA로부터 인가된 것은 이 지역이 겔 카드 처리와 반사형 NGS 및 AI 기반 판독을 융합한 기술에 의욕적임을 보여줍니다. 노동 시장이 가까워지기 때문에 검사실은 작업시간이 적은 워크 어웨이형 분석 장치에 기울어 져 장비 교체 사이클이 더욱 가속화됩니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 8.92%로 가장 높을 것으로 예측됩니다. 인도, 인도네시아, 베트남에서는 전국적인 헌혈 확대로 대량의 시료가 공적 및 사적 검사 채널에 유입되고 있으며, 중국에서는 지방 센터에서의 자동 시약 렌탈 프로그램이 급속히 진행되고 있습니다. 일본은 종양학과 이식을 위한 분자 타이핑의 급속한 보급에 견인되어 1인당 검사 보급률이 가장 높습니다. 한국과 중국의 지역 제조업체가 중가격대의 검사기기에 진입해, 가격과 애프터서비스로 구미의 기존 제조업체에 과제하고 있습니다.

유럽은 한 자릿수 중반의 안정적인 성장을 유지합니다. EU의 의료기기 규제는 하모나이즈되어 엄격한 성능 확인이 의무화되고 있지만, 독일, 프랑스, 북유럽에서는 상환의 틀이 검체량과 낭비를 생략하는 하이스펙 분석 장치의 채용을 뒷받침하고 있습니다. 한편 중동 및 아프리카에서는 진전에 편차가 있습니다. 걸프 협력 회의 국가들은 3차 병원을 위한 최고급 분석 장비를 수입하고 있지만, 사하라 이남의 많은 시설들은 전력 공급 불안정으로부터 수동 슬라이드 검사에 의존하고 있습니다. 남미에서는 브라질의 헤모비지런스 개혁으로 여러 주를 다루는 집중형 검사 허브에 자본 주입이 진행되고 있어 기세가 증가하고 있습니다.

The blood typing market size was valued at USD 2.26 billion in 2025 and is forecast to reach USD 3.31 billion by 2030, advancing at a 7.96% CAGR.

Rising surgical volumes, higher life expectancy, and the clinical shift toward precision transfusion protocols underpin this steady expansion. Rapid technology adoption-from high-throughput serology analyzers to next-generation sequencing (NGS) platforms-strengthens test accuracy and throughput, while enabling laboratories to resolve complex antibody work-ups within hours instead of days. Demand also gains from government-funded blood donation drives, especially in Asia-Pacific, that channel large numbers of collected units into standardized testing workflows. Automation is closing the gap created by laboratory staffing shortages, with instrument vendors embedding robotics, advanced optics, and artificial intelligence to deliver faster results and lower per-test costs. Hospital consolidation in North America and Europe further favors integrated platforms that combine instruments, reagents, middleware, and outsourced reference services under one purchasing contract.

Worldwide transfusion volumes continue to climb as complex cardiovascular, trauma, and oncological interventions become commonplace. Each transfusion episode triggers multiple compatibility checks, so even marginal increases in procedure counts magnify reagent and instrument demand. Emergency medicine now requires point-of-care analyzers that can process ABO-Rh typing in under five minutes, a capability that high-volume hospitals in the United States and Japan already view as essential. Automated workflows are therefore replacing manual tube testing in both tertiary centers and regional trauma networks.

Long-term transfusion support for thalassemia, sickle cell disease, and hematologic cancers is reshaping routine practice from basic ABO-Rh matching to extended antigen phenotyping. Molecular assays that read multiple blood group loci in a single run limit alloimmunization, a risk especially acute in multi-transfused pediatric patients. Oncology protocols are also adopting prophylactic typing to offset transfusion reactions during chemotherapy cycles.

Inconsistent electricity, inadequate cold chain capacity, and scarce maintenance expertise hamper reliable blood typing in a sizable share of African and rural South Asian facilities. Cap-ex hurdles slow adoption of NGS and even mid-tier automated serology systems, compelling many centers to rely on manual slide or rapid card tests with lower sensitivity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Consumables accounted for 48.32% of blood typing market share in 2024, reflecting the high frequency of reagents used for routine gel card and microplate testing. The services category, however, is projected to post a 10.45% CAGR to 2030 as laboratories increasingly outsource NGS-based antigen panels and rare antibody identification. That outsourcing trend enlarges the blood typing market size for specialized reference providers, many of which package logistics, sequencing, and interpretive reports under subscription agreements. Instruments maintain mid-single-digit growth, driven by upgrades to AI-enabled analyzers that optimize reagent use and interface directly with hospital LIS platforms.

Laboratory managers cite the capital-intensive nature of NGS as the main reason for send-out adoption. Meanwhile, reagent suppliers face price pressure as automated analyzers become more frugal with micro-volume reaction pads. Despite that, rising total test volumes secure stable revenue streams for gel cards, buffers, and control sera. Instrument manufacturers differentiate through modular designs that expand from 96 to 384 well formats, aligning capacity with fluctuating seasonal demand.

PCR and microarray platforms delivered 37.23% of segment revenue in 2024, yet NGS is forecast to climb at a 12.45% CAGR, reflecting unrivaled depth of antigen coverage. The blood typing market size for NGS reagents is still below traditional serology reagents, but rapid uptake in reference centers is narrowing the gap. Multi-locus sequencing resolves Rh, Kell, Kidd, and Duffy variants in a single assay, which supports precision-matching policies for chronically transfused patients.

While serology remains the frontline workhorse for same-day ABO-Rh testing, clinicians now consider NGS confirmation indispensable for complex phenotyping. Microfluidics and lateral-flow cassettes keep a foothold in resource-constrained or emergency settings due to minimal training requirements. Hybrid workflows are therefore common: a slide or column agglutination test confirms immediate compatibility, with NGS data arriving a day later to refine extended match decisions.

The Blood Group Typing Market Report is Segmented by Product (Instruments, Consumables, and Services), Technique (Serology Assay-Based, PCR-Based & Microarray, and More), Test Type (ABO Blood Tests, Antibody Screening, and More), End User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America controlled 33.45% of revenue in 2024 thanks to stringent regulatory oversight, high healthcare spending, and a mature hospital network that prioritizes fully automated immunohematology. FDA clearances in 2025 for integrated serology-molecular workstations illustrate the region's appetite for technology that merges gel card processing with reflex NGS and AI-based interpretation. A tight labor market further accelerates instrument replacement cycles, as labs gravitate to walk-away analyzers that need fewer hands-on minutes.

Asia-Pacific is forecast to post the highest 8.92% CAGR through 2030. National blood donation expansion across India, Indonesia, and Vietnam is pouring large sample volumes into both public and private testing channels, while China is fast-tracking automated reagent rental programs in provincial centers. Japan holds the highest per-capita test penetration, driven by rapid uptake of molecular typing for oncology and transplantation. Local manufacturers in South Korea and China are entering the mid-range instrument tier, challenging Western incumbents on price and after-sales service.

Europe maintains steady mid-single-digit growth. Harmonized EU medical device regulations impose rigorous performance verification, yet reimbursement frameworks in Germany, France, and the Nordics support adoption of high-spec analyzers that reduce sample volume and waste. Meanwhile, the Middle East and Africa display uneven progress. Gulf Cooperation Council countries import top-end instruments for tertiary hospitals, whereas many sub-Saharan facilities rely on manual slide testing due to power instability. South America gains momentum as Brazil's hemovigilance reforms channel capital into centralized testing hubs that serve multiple states.