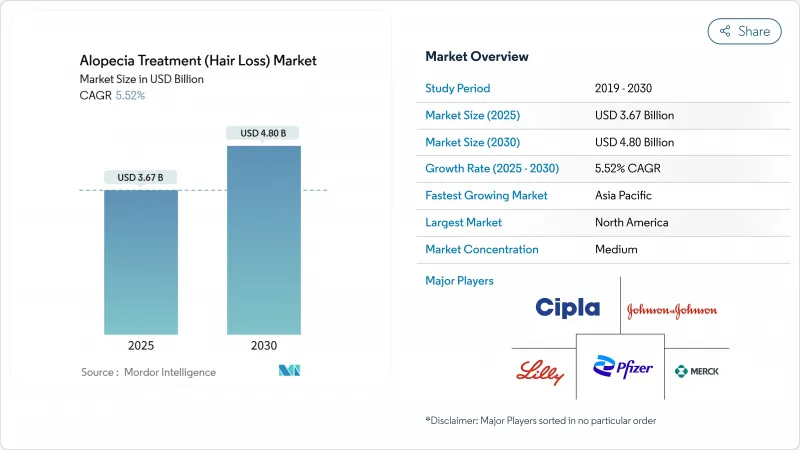

탈모증 치료 시장 규모는 2025년에 36억 7,000만 달러로 추정되고, 2030년에는 48억 달러로 확대될 것으로 예측되며, CAGR 5.52%로 성장이 전망됩니다.

이 확장은 전통적인 미녹시딜 피나스테리드의 패러다임을 넘어서는 정밀 면역 조절, 재생 의료, 가정용 장비의 임상 도입 확대를 반영합니다. 현재 3종의 경구 JAK 억제제가 심한 원형 탈모증에 대해 승인을 받았으며, 지금까지 충분한 치료를 받지 못했던 약 70만 명의 미국 환자에게 치료의 길이 열리고 있습니다. 벤처기업도 미토콘드리아 대사 조절제와 모낭 줄기세포 경로를 표적으로 하는 피내 투여형 생물제제를 발표하고 있습니다. 디지털 헬스는 이러한 혁신을 연결합니다 : 인공지능에 의한 두피 영상 진단, 원격 상담, 전자 약국은 진단주기를 단축하고 특히 젊은 소비자의 어드히어런스를 향상시킵니다.

baricitinib, ritlecitinib, deutuxolitinib의 잇따른 승인은 자가 면역 탈모증에 대한 치료 기대를 재설정했습니다. 매우 중요한 임상시험에서 성인의 30%가 24주 이내에 두피의 모발 피복률이 적어도 80%에 도달한 것으로 나타났습니다. 2034-2041년까지 특허는 선발 의약품을 보호하고 흉터성 탈모증과 같은 적응 추가를 촉진합니다. 미국, 캐나다, EU 주요 국가의 상환 제도는 심각한 원형 탈모증을 미용이 아닌 의료로 인정하고 있으며, 탈모증 치료에 대한 접근성을 개선하고 탈모증 치료 시장을 확대하고 있습니다. 제조업체 각사는 경구 JAK 억제제가 5년 이내에 중증 탈모증 부문의 15-20%를 획득할 수 있다고 예측했습니다.

AI를 활용한 두피 이미지 분석은 주관적인 등급을 픽셀 수준에서 정량화로 대체합니다. 470,000개의 이미지 트레이닝 세트에서 FDA에 등록된 플랫폼은 환자를 최적의 요법에 맞추고 컴플라이언스를 추적함으로써 77.7%의 발모 성적 향상을 가져왔습니다. 클리닉은 이러한 도구를 유전자 및 호르몬 패널과 통합하고 비용이 많이 드는 시행착오 사이클을 줄이는 큐레이트된 프로토콜을 만들고 있습니다. 5,000만 달러를 넘는 벤처 투자는 알고리즘에 의한 의사결정 지원이 3년 이내에, 특히 지방에 서비스를 제공하는 원격 피부과 네트워크에서 표준이 될 것이라는 확신을 강조하고 있습니다.

FDA는 지속성 발기 부전 및 기분 장애와 같은 배합 외 피나스테리드와 관련된 32건의 부작용 보고를 기록하고 경고 및 약국의 모니터링 강화를 촉구했습니다. 경구 JAK 억제제는 감염과 심혈관계 위험에 대한 경고를 받기 때문에 위험이 낮은 환자는 외용제와 주사제를 대체하는 것을 선호하는 임상의도 있습니다. 이러한 안전성 프로파일은 상담 시간을 증가시키고, 치료 개시를 지연시키며, 탈모증 치료 시장의 성장을 억제할 수 있습니다.

남성형 탈모증은 2024년에 탈모증 치료 시장 점유율의 37.23%를 유지했고, 평생 유병률, 저비용 미녹시딜과 제네릭 피나스테리드를 이용할 수 있다는 점이 관건이 되었습니다. 이 분야의 탈모증 치료 시장 규모는 기존 제품이 제1선택약으로서 존속하고 있기 때문에 꾸준히 확대될 것으로 보입니다. 그러나 파괴는 임박해 있습니다. Pelage Pharmaceuticals의 PP405는 미토콘드리아의 피루브산 운반체를 표적으로 함으로써 초기 임상시험에서 비벨라스 모발 수를 6배로 증가시켜 전략적 투자자로부터 1,400만 달러를 모았습니다. 원형 탈모증의 치료에 혁명을 일으킨 것과 같은 JAK 클래스의 혜택을 받는 원형 탈모증은 CAGR 7.36%의 페이스로 추이하고 있어, 2030년까지 수익 격차를 줄일 가능성이 있습니다. 파이프라인 검토는 안드로겐성 탈모증에 대한 후보 약물만으로 100개 이상 나열되어 있으며, 메커니즘에 특화된 개입으로의 이동을 보여줍니다.

2차 효과는 자가면역 아형의 세분화를 포함합니다. 임상의는 현재 표면적 증상이 아니라 인터페론 시그니처와 사이토카인의 이점을 통해 환자를 계층화하고 그에 따라 면역조절제를 조절하고 있습니다. 견인성 탈모증은 과거에는 상담과 스테로이드 외용제로 대처할 뿐이었지만, 장치를 이용한 오플로딩과 재생 보조제가 임상시험에서 유망시되어 새로운 관심을 모으고 있습니다. 이러한 추세를 종합하면 탈모증 치료 시장은 정밀한 표현형 분류와 여러 치료법의 조합으로 정의됩니다.

2024년 매출의 62.65%는 남성 소비자이며, 이는 임상적 유병률의 높이와 치료에 대한 문화적 수용의 확립 때문입니다. 그러나 여성이 CAGR 6.85%에서 가장 빠르게 성장하는 코호트입니다. AI가 유도하는 패턴 인식은 여성형 탈모에 전형적인 확산성으로 정수리를 온존한 증상을 밝혀, 조기 진단을 촉진합니다. deutuxolitinib의 임상 데이터는 50세 미만의 여성에서 더 강한 연주 효율을 나타내며 성별에 특화된 투여 시험을 촉진합니다(clinicaltrials.gov). 안전성 프로파일이 개선됨에 따라, 국소 마이크로캡슐화 제형은 전신에 대한 노출을 피하고 과거의 최기형성 우려를 극복하고 있습니다.

전자상거래 키트는 처방전, 보충제, 저출력 레이저 기기를 현관 끝까지 전달해주기 때문에 한때는 여성 환자의 족쇄가 되었던 스티그마(낙인)를 줄일 수 있습니다. 인플루언서 주도 교육 캠페인은 탈모를 미용 걱정에서 치료 가능한 병리로 높이고 탈모증 치료 시장을 남녀 평등으로 밀어 올립니다.

북미는 2024년 매출의 42.32%를 차지했는데, 이는 FDA의 브레이크스루 지정에 따라 2년 이내에 3개의 경구 JAK 억제제의 승인이 가속되었기 때문입니다. 보험 적용이 결정됨에 따라 심각한 원형 탈모증이 보험 적용 가능한 염증성 질환으로 분류되어 환자 비용 부담이 줄어 들었습니다. Pelage Pharmaceuticals에 의한 1,400만 달러의 자금 주입으로 대표되는 견고한 벤처 자금 조달은 활기찬 파이프라인을 지원합니다. 국경을 넘어선 치료는 여전히 흔합니다. 미국 거주자는 저렴한 비용의 이식 수술을 위해 멕시코에 가고 캐나다 환자는 미국의 원격 약국에서 공식화된 외용제를 구입하고 탈모증 치료 시장의 지역 통합을 강화하고 있습니다.

아시아태평양의 CAGR은 6.56%로 가장 빠르고, 중국의 2억 5,000만 명의 탈모 인구와 중간층의 헬스케어 지출 증가가 그 요인이 되고 있습니다. 킨터 퍼머슈티칼사의 프로키잘타미드 외용제는 혁신의 현지화를 추진하는 중국의 움직임을 반영하여 후기 단계로 이행했습니다. 일본은 난치성 사례에 대한 리틀시티닙을 2023년에 조기 승인하였고, 한국은 국내 레이저 캡 제조에 의해 디바이스의 리더십을 견인합니다. 인도의 제네릭 의약품은 전신 치료 비용을 절감하고, 한때는 고가였던 치료가 보다 광범위한 집단에 이용하기 쉬워졌습니다. 규제 수렴이 진행됨에 따라 크로스 라이선싱은 세계 브랜드를 현지 처방에 채택하기 쉽습니다.

유럽에서는 안전과 혁신의 균형을 이루는 EMA의 집중 심사(ema.europa.eu)를 통해 완만한 성장을 유지하고 있습니다. 각국의 의료제도는 엄격한 비용대비 효과 평가 후에 비용의 일부를 환불하고 예측은 가능하지만 보급은 완만합니다. 독일과 영국은 줄기세포와 엑소좀 연구의 선구자인 산학 클러스터를 보유하고 있습니다. 남유럽 국가에서는 미용 성형 투어리즘에 대한 수요가 증가하고 있지만, 경제적 제약으로 인해 고가의 생물학적 제제의 도입은 제한되고 있으며, 탈모증 치료 시장은 소득에 의해 계층화되고 있습니다.

The alopecia treatment market size reached USD 3.67 billion in 2025 and is projected to advance to USD 4.80 billion by 2030, translating to a 5.52% CAGR.

This expansion reflects growing clinical adoption of precision immunomodulation, regenerative medicine, and home-use devices that move care beyond the historic minoxidil-finasteride paradigm. Three oral JAK inhibitors now hold regulatory approval for severe alopecia areata, opening a therapeutic avenue for roughly 700,000 previously underserved U.S. patients. Venture-backed start-ups have also introduced mitochondrial metabolism modulators and intradermal biologics that target follicular stem-cell pathways. Digital health ties these innovations together: AI-guided scalp imaging, tele-consultations, and e-pharmacy fulfillment shorten diagnostic cycles and improve adherence, particularly among younger consumers.

Successive approvals of baricitinib, ritlecitinib, and deutuxolitinib have reset therapeutic expectations for autoimmune alopecia. Pivotal trials showed that 30% of adults achieved at least 80% scalp hair coverage within 24 weeks, a milestone unreachable with corticosteroids or topical immunotherapy. Patent coverage through 2034-2041 protects first movers and encourages additional indications such as cicatricial alopecia. Reimbursement frameworks in the United States, Canada, and major EU states now recognize severe alopecia areata as a medical-not cosmetic-condition, improving access and expanding the alopecia treatment market. Manufacturers project that oral JAK inhibitors could capture 15-20% of the severe alopecia segment within five years.

AI-enabled scalp-image analysis replaces subjective grading with pixel-level quantification. In a 470,000-image training set, an FDA-listed platform produced 77.7% better hair-growth outcomes by matching patients to optimal regimens and tracking compliance. Clinics integrate these tools with genetic and hormonal panels, creating curated protocols that cut costly trial-and-error cycles. Venture investments exceeding USD 50 million highlight confidence that algorithmic decision support will become standard within three years, particularly in tele-dermatology networks that serve rural areas.

The FDA recorded 32 adverse-event reports tied to compounded topical finasteride, including persistent erectile dysfunction and mood disorders, prompting warning letters and heightened pharmacy oversight. Oral JAK inhibitors carry boxed warnings for infections and cardiovascular risks, leading some clinicians to favor topical or injectable alternatives in lower-risk populations. These safety profiles increase counseling time and may delay initiation, tempering growth in the alopecia treatment market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Androgenic alopecia maintained 37.23% of alopecia treatment market share in 2024, anchored by lifelong prevalence and the availability of low-cost minoxidil and generic finasteride. The alopecia treatment market size for this segment is set to expand steadily as legacy products remain first-line therapy. Yet disruption is imminent. Pelage Pharmaceuticals' PP405 increased non-vellus hair counts sixfold in early trials by targeting mitochondrial pyruvate carriers, attracting USD 14 million from strategic investors. Alopecia totalis, benefiting from the same JAK class that revolutionized alopecia areata care, is pacing a 7.36% CAGR and could narrow the revenue gap by 2030. Pipeline reviews list more than 100 candidates against androgenic alopecia alone, signifying a shift toward mechanism-specific interventions.

Second-order effects include greater segmentation of autoimmune subtypes. Clinicians now stratify patients by interferon signature and cytokine dominance rather than surface presentation, tailoring immunomodulators accordingly. Traction alopecia-once addressed only by counseling and topical steroids-gains new interest as device-based offloading and regenerative adjuncts show promise in trials. Collectively, these trends point to an alopecia treatment market that will be defined by precision phenotyping and multi-modal combinations.

Male consumers accounted for 62.65% of 2024 revenue owing to higher clinical prevalence and established cultural acceptance of treatment. However, women represent the fastest-growing cohort at 6.85% CAGR. AI-guided pattern recognition reveals diffuse, vertex-sparing presentations typical of female pattern hair loss, driving earlier diagnosis. Clinical data from deutuxolitinib showed stronger response rates in women under 50, prompting gender-specific dosing studies [clinicaltrials.gov]. As safety profiles improve, topical micro-encapsulated formulas avoid systemic exposure, overcoming historical teratogenicity concerns.

Tele-dermatology also narrows access gaps: discreet e-commerce kits deliver prescriptions, supplements, and low-level-laser devices to the doorstep, reducing stigma that once deterred female patients. Influencer-led education campaigns elevate hair loss from cosmetic worry to treatable medical condition, pushing the alopecia treatment market toward gender parity.

The Alopecia Treatment Market Report is Segmented by Disease Type (Androgenic Alopecia, Alopecia Areata, Scarring (Cicatricial) Alopecia, and More), Gender (Male and Female), Route of Administration (Oral, Intravenous, Other Route of Administrations, and More), End User (Hospital, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 42.32% of 2024 revenue because FDA breakthrough designations accelerated three oral JAK inhibitor approvals within two years. Coverage determinations now classify severe alopecia areata as a reimbursable inflammatory disorder, easing patient cost burdens. Robust venture funding, exemplified by Pelage Pharmaceuticals' USD 14 million infusion, supports a vibrant pipeline. Cross-border care remains common: U.S. residents travel to Mexico for lower-cost transplant surgery, while Canadian patients purchase compounded topicals from U.S. tele-pharmacies, tightening regional integration inside the alopecia treatment market.

Asia-Pacific delivers the fastest 6.56% CAGR, anchored by China's 250 million hair-loss population and rising middle-class healthcare spending. Kintor Pharmaceutical's proxalutamide topical advanced into late-stage review, reflecting China's push to localize innovation. Japan fast-tracked ritlecitinib in 2023 for intractable cases, while South Korea drives device leadership with domestic laser-cap manufacturing. Indian generics reduce systemic therapy costs, making once-premium treatments accessible to a broader cohort. As regulatory convergence improves, cross-licensing will help global brands enter local formularies.

Europe sustains moderate growth through centralized EMA reviews that balance safety with innovation [ema.europa.eu]. National health systems reimburse partial costs after rigorous cost-effectiveness appraisals, producing predictable but slower uptake. Germany and the United Kingdom host academic-industry clusters that pioneer stem-cell and exosome research. Southern European countries see stronger demand for cosmetic surgery tourism, although economic constraints limit adoption of high-priced biologics, keeping the alopecia treatment market stratified by income.