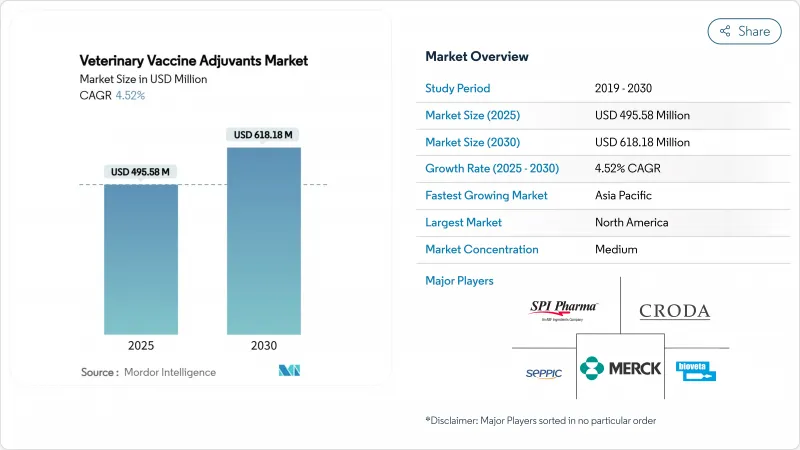

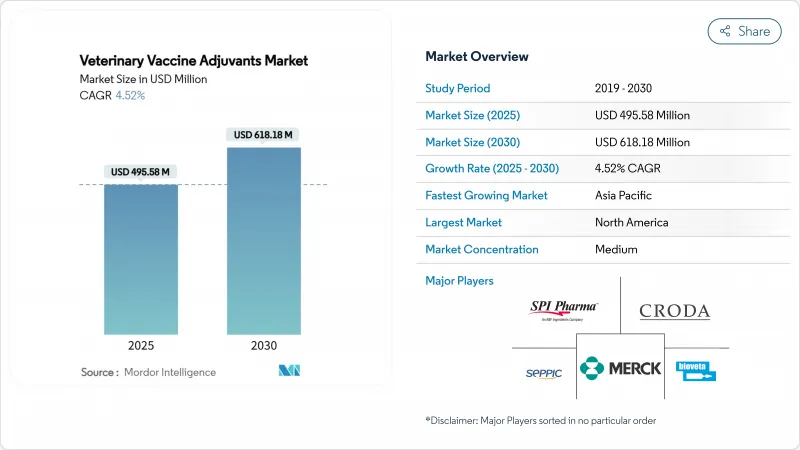

동물용 백신 보조제 시장 규모는 2025년에 4억 9,558만 달러로, 2030년에 6억 1,818만 달러에 이를 것으로 예측되며, CAGR은 4.52%를 나타낼 전망입니다.

지속적인 성장은 정밀 면역학, 신속한 생명공학 발전, 그리고 더 높은 백신 효능을 요구하는 H5N1 이후 비상 정책에 기반합니다. 이 분야는 면역 초기화 시간을 단축하고 투여량을 줄이는 mRNA 및 나노입자 혁신의 혜택을 받으며, 유제 안전성 문제는 제조사들을 폴리머 및 카보머 시스템으로 유도합니다. 가축 밀도, 글로벌 단백질 수요, 인도와 중국의 원헬스(One Health) 자금 지원이 기술 도입을 가속화하는 반면, QS-21 및 특수 지질에 대한 분산된 승인 절차와 공급 리스크는 속도를 저해합니다. 조에티스(Zoetis), 머크 애니멀 헬스(Merck Animal Health), 엘란코(Elanco)가 사포닌(saponin), TLR(Toll-like receptor), VLP(바이러스 유사 입자) 중심의 신규 진입업체들에 맞서 시장 점유율을 방위하면서 경쟁 강도가 높아지고 있으며, 이들 신규 업체들은 발병 시 가속화된 승인을 목표로 포지셔닝하고 있습니다.

인도, 브라질, 중국 전역으로 확대되는 집약적 가축 사육 시스템은 감염 위험을 높여 생산자들이 높은 항체 역가를 유지하면서 재접종 빈도를 줄이는 보조제를 선호하게 합니다. 수주에 걸쳐 항원을 서서히 방출하는 폴리머 마이크로스피어는 비용 및 콜드체인 격차로 고심하는 열대 지역 운영자들에게 매력적입니다. 연간 단백질 생산량 20% 증가를 목표로 하는 인도의 가축 확대 정책은 대규모 소 및 가금류 사육을 위한 보조제 비용 일부를 흡수하는 연방 보조금 제도를 형성합니다. 이에 따라 내열성 카보머 블렌드는 남아시아 및 동남아시아에서 입찰 성공률이 높습니다.

2024년 미국 16개 주에 걸친 H5N1 유행성 조류 인플루엔자 유제품 발병과 유럽 양 사육장에서의 블루텅병 재발은 교차 보호 및 신속한 면역 형성을 가능케 하는 보조제의 시급성을 부각시켰습니다. NS1 결핍 생백신 벡터와 TLR-4 작용매 보조제를 병용한 시험은 5일 이내에 보호 효과를 제공했으며, 이는 규제 당국이 유사 후보물질에 대한 지속적인 심사를 진행하도록 촉진했습니다.

상어 유래 스쿠알렌을 함유한 반려동물 주사제는 주사 부위 부종 경보로 인해 2024년 미국 유통업체 주문량이 두 자릿수 감소했습니다. 크로다(Croda)의 사탕수수 유래 스쿠알렌은 현재 해양 유래 성분 제거 및 규제 완화를 목표로 한 재제형 프로그램에 공급되고 있습니다. 재제형화, 안정성 확보 및 재허가 절차는 출시를 12-18개월 지연시키고 매출원가를 증가시킬 수 있습니다.

2024년 동물용 백신 보조제 시장에서 입자 및 나노입자 기술이 38.43%의 압도적 점유율을 기록한 반면, 폴리머 및 카보머 시스템은 2030년까지 6.32%의 가장 빠른 연평균 성장률(CAGR)을 보일 것으로 예상됩니다. 이러한 지속적인 성장은 특히 대규모 가축 군집의 반복적 처리를 억제하려는 지역에서, 제조사들이 정밀한 항원 방출 및 용량 절감 기능에 부여하는 가치를 반영합니다. 60-150nm 크기의 나노입자는 수지상 세포 흡수를 향상시켜 추가 접종 횟수를 줄이고 인건비를 절감합니다. 원료 알루미늄은 비용 상한선이 엄격한 지역에서 여전히 선호되나, 강력한 T세포 반응을 유발하지 못하는 한계로 인해 향후 수익 잠재력이 제한됩니다. 식물 추출 및 조직 배양 기술로 공급이 안정화되면서 사포닌 유도체(특히 식물성 QS-21)가 주목받고 있습니다. 이는 칠레 비누나무에 대한 압박을 완화하고 ESG 점수를 개선합니다.

MPLA의 TLR-4 작용과 스쿠알렌 미세액적체를 결합한 복합 유화제는 IgA 분비를 촉진하여 가금류 호흡기 백신으로 매력적입니다. 종간 인플루엔자 유출이 식량 안보를 위협하는 비상 키트에는 병원체 유래 CpG 올리고뉴클레오타이드가 등장합니다. 알루미늄 및 인산칼슘을 둘러싼 오랜 규제 데이터베이스는 여전히 저가 제형에 포함되도록 보장하며, 특히 사하라 이남 아프리카 전역의 국가 지원 소 브루셀라증 예방 사업에 활용됩니다. 반면 나노입자와 폴리머 마이크로스피어는 원가(COGS)가 높음에도 불구하고, 항생제 무첨가 브랜드화가 고가 원료 사용을 정당화하는 덴마크와 스페인의 수출 지향형 돼지 사육 사업에서 점유율을 확대하고 있습니다. 공급 충격으로 대량 항원 가격이 상승할 때 매력적인 지표인 항원 부하량의 1/3로 바이러스 중화 역가를 약속하는 VLP 기반 보조제의 대학 스핀아웃이 증가함에 따라 경쟁은 더욱 치열해질 전망입니다.

2024년 북미의 40.43% 점유율은 임상 검증된 보조제에 대한 보상을 제공하는 미국 농무부(USDA)의 엄격한 허가 제도와 외딴 사료 공급장까지 도달하는 광범위한 콜드체인 인프라에 기반합니다. 700만 달러 규모의 캔자스 주 바이오제조 이니셔티브(Kansas State Biomanufacturing Initiative)와 같은 연방 보조금은 국내 보조제 파일럿 생산 능력 확장을 촉진하여 해외 사포닌 추출 의존도를 완화합니다. 캐나다는 미국과의 데이터 상호인정 협정으로 공급업체가 양국 시장에 걸쳐 연구 비용을 분산할 수 있는 이점을 누리며, 멕시코의 다양한 규모의 목장 환경은 마진 압박이 예상되는 지역에서 경제적인 알루미늄-오일 하이브리드 제제를 흡수합니다.

아시아태평양 지역은 인도 '원 헬스 미션(One Health Mission)'이 주립 수의학 연구소에 지속적인 예산을 투입하고, 중국이 구제역(FMD) 저항성 가축 군집을 대상으로 보조금을 지원함에 따라 가장 가파른 5.45%의 연평균 성장률(CAGR) 전망을 기록합니다. 지역별 수요는 냉장 완제품 백신 운송비를 절감하는 현지 병입 공장과 연계됩니다. 일본의 반려동물 부문은 진료 대기 시간을 단축하는 무주사 피내 패치를 선호하며, 호주의 광활한 목장 운영은 드문 가축 집합 일정에 적합한 내열성 카보머를 중시합니다.

유럽은 친환경 화학 및 복지 규범을 강조합니다. 동물용 의약품 규정은 서류 서식을 통일하지만, 탄소 발자국 지표가 용매 사용에 추가적인 심사를 가합니다. 브라질과 아르헨티나는 소-가금류 이중용도 시설을 확장하며, 할랄 수출 심사관과 항생제 감축 약속을 동시에 충족해야 하는 필요성에 따라 보조제 선택이 이루어집니다. 중동 및 아프리카 시장은 40°C 운송을 견디는 카보머 기반의 상온 안정성 혼합제를 선호하여, 입증된 상온 안정성 주장을 가진 공급업체들에게 시장 진입 기회를 제공합니다.

The veterinary vaccine adjuvants market size stands at USD 495.58 million in 2025 and is forecast to reach USD 618.18 million by 2030, advancing at a 4.52% CAGR.

Sustained growth rests on precision immunology, rapid biotechnology advances and post-H5N1 emergency policies that mandate higher vaccine potency. The sector benefits from mRNA and nanoparticle innovations that shorten immune-priming times and lower dose volumes, while oil-emulsion safety issues steer manufacturers toward polymer and carbomer systems. Livestock density, global protein demand and One Health funding in India and China accelerate technology adoption, whereas fragmented approvals and supply risks for QS-21 and specialized lipids curb velocity. Competitive intensity grows as Zoetis, Merck Animal Health and Elanco defend share against saponin-, TLR- and VLP-focused newcomers positioning for accelerated approvals during outbreak conditions.

Intensive livestock systems scaling across India, Brazil and China elevate infection risks, so producers favor adjuvants that cut revaccination frequency while preserving high titers. Polymer microspheres that meter antigen over weeks appeal to tropical operators wrestling with cost and cold-chain gaps. India's livestock push, now targeting 20% annual protein output gains, shapes federal grants that absorb part of adjuvant costs for mass cattle and poultry drives. Thermostable carbomer blends hence show strong tender success in South and Southeast Asia.

The 2024 H5N1 dairy outbreak across 16 U.S. states, and bluetongue flare-ups in European sheep flocks, highlight the urgency for adjuvants enabling cross-protective, rapid immunity. Trials using NS1-deficient live vectors plus TLR-4 agonist adjuvants delivered protection within five days, which has pushed regulators to issue rolling reviews for comparable candidates.

Companion-animal injections containing shark-sourced squalene prompted site swelling alerts that trimmed U.S. distributor orders by double digits in 2024. Croda's sugarcane-derived squalene now supplies reformulation programs aimed at removing marine inputs and easing scrutiny. Reformulation, stability, and re-licensing cycles can delay launches 12-18 months and inflate cost of goods sold.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Particulate and nanoparticle technologies accounted for a dominant 38.43% slice of the veterinary vaccine adjuvants market in 2024, while polymer and carbomer systems are set to clock the fastest 6.32% CAGR through 2030. The sustained rise reflects the premium producers attach to precise antigen release and dose-sparing functionality, especially in regions seeking to suppress repeated handling of large herds. Nanoparticles sized 60-150 nm improve dendritic-cell uptake, meaning fewer booster shots and slimmer labor bills. Native alum remains popular where cost ceilings are strict, yet its inability to spark strong T-cell responses limits future revenue potential. Saponin derivatives, notably plant-based QS-21, gain favor as botanical extraction and tissue-culture methods secure supply, lessening pressure on Chilean soapbark trees and improving ESG scores.

Combination emulsions that integrate MPLA TLR-4 agonism with squalene microdroplets enhance IgA secretion, making them attractive for respiratory poultry vaccines. Pathogen-derived CpG oligonucleotides surface in emergency kits where cross-species influenza spillover threatens food security. The long regulatory databank surrounding alum and calcium phosphate still secures inclusion in value-priced formulations, especially for state-funded bovine brucellosis drives across sub-Saharan Africa. In contrast, nano-particles and polymer microspheres, despite higher COGS, gain share in export-oriented swine operations in Denmark and Spain where zero-antibiotic branding justifies premium inputs. Competition will likely intensify as universities spin out VLP-enabled adjuvants that promise virus-neutralizing titers at one-third the antigen load, a compelling metric when supply shocks raise bulk antigen prices.

The Veterinary Vaccine Adjuvants Market Report is Segmented by Type (Alum & Calcium Salts, and More), Route of Administration (Intramuscular, Subcutaneous, Intradermal, Intranasal/Mucosal, Oral), Animal Type (Livestock, Poultry, Companion Animals, Aquaculture), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America's 40.43% share in 2024 is anchored by USDA licensing rigor that rewards clinically vetted adjuvants and by an extensive cold-chain grid reaching remote feedlots. Federal grants such as the USD 7 million Kansas State Biomanufacturing Initiative catalyze domestic adjuvant pilot-lot capacity, mitigating dependence on overseas saponin extraction. Canada benefits from data reciprocity with the U.S., letting suppliers amortize studies across both markets, while Mexico's mixed-scale ranch landscape absorbs economical alum-oil hybrids where margin pressures loom.

Asia-Pacific posts the steepest 5.45% CAGR outlook as India's One Health Mission injects consistent budget lines into state veterinary labs and as China channels subsidies toward FMD-resistant herds. Regional demand collocates with local bottling plants that cut freight on chilled finished vaccines. Japan's companion animal segment rewards needle-free intradermal patches that shrink clinic dwell time, and Australia's extensive pastoral operations prize thermostable carbomers fit for infrequent muster schedules.

Europe stresses green chemistry and welfare norms; the Veterinary Medicines Regulation harmonizes dossier formats, but carbon-footprint metrics exert extra screening on solvent use. Brazil and Argentina expand dual-use cattle-poultry sites, with adjuvant selection driven by the need to satisfy both halal export auditors and antibiotic reduction pledges. Middle East and Africa markets look to shelf-stable blends-often carbomer-based-that tolerate 40 °C transit, opening lanes for suppliers with proven ambient-stability claims.