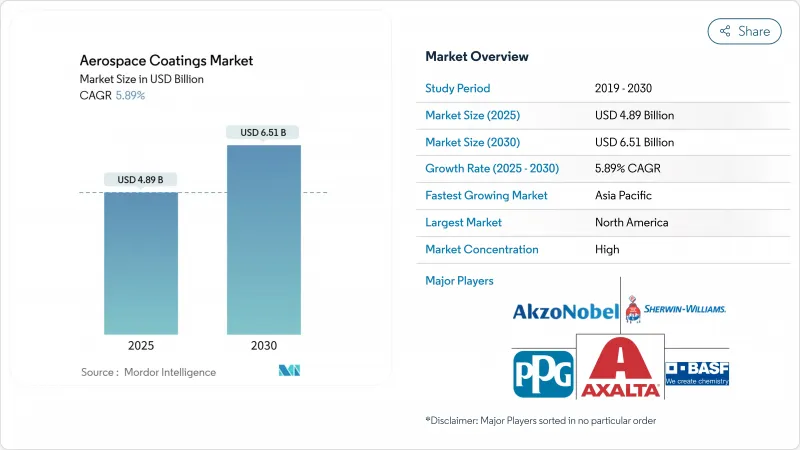

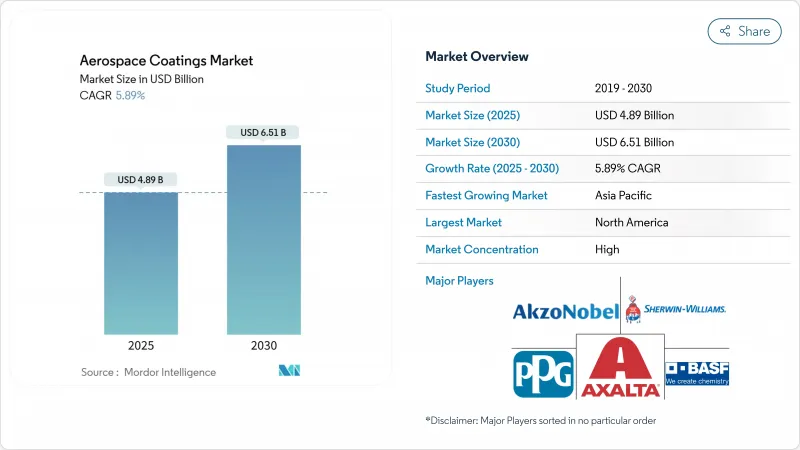

항공우주 코팅 시장 규모는 2025년에 48억 9,000만 달러로 평가되었고 예측기간 중(2025-2030년)의 CAGR은 5.89%를 나타낼 것으로 예측되며, 2030년에 65억 1,000만 달러에 달할 전망입니다.

상업용 항공기 생산 속도는 지속적인 여객 운송 회복에 힘입어 주요 성장 동력으로 남아 있으며, 복합재 중심의 기체 설계는 프리미엄 가격을 요구하는 새로운 코팅 화학 기술을 필요로 합니다. 휘발성 유기 화합물(VOC) 및 6가 크롬에 대한 규제 압박은 수성 및 크롬 프리 시스템으로의 전환을 가속화하여 공급업체들이 R&D 포트폴리오를 재조정하도록 촉구하고 있습니다. 에어버스, 보잉 및 1차 통합업체의 OEM 수요는 기본 물량을 유지하지만, 노후화된 항공에 대한 정비, 수리 및 정비(MRO) 활동이 더 빠르게 확대되면서 제품 구성과 서비스 요구 사항을 재편하고 있습니다. 지역별로는 북미가 여전히 최대 매출을 창출하지만, 지정학적 위험 완화를 위해 공급망이 인도, 중국, 동남아시아로 다각화되면서 아시아태평양 지역의 성장 속도가 가장 빠릅니다. 전반적으로 항공우주 코팅 시장은 소수의 자격을 갖춘 공급업체들이 수십 년간의 인증 노하우를 활용해 시장 점유율을 방위하고 기술 도입 속도를 주도하면서 중간 수준의 집중도를 보입니다.

보잉은 737 시리즈 제트기를 월 38대 생산 중이며, 생산량을 42대로 늘리기 위해 연방항공청(FAA)의 승인을 추진 중입니다. 에어버스는 공급망 문제로 초기 800대 계획이 축소된 가운데, 2025년까지 770대의 제트 여객기를 인도할 계획입니다. 각 좁은 동체 항공기에는 프라이머, 탑코트, 특수 마감재로 약 150-200갤런이 소요되므로, 단위 수 증가만으로도 도장량에 배가 효과가 발생합니다. 제조사들의 초점이 비용에서 납품 신뢰성으로 전환되면서, 자격을 갖춘 도장 업체들은 계약상 더 큰 영향력을 행사할 수 있게 되었습니다. 연비 효율 모델을 중심으로 한 기체 현대화 프로그램이 이러한 추세를 유지하고 있으나, 엔진 및 객실 내장재 부족으로 인해 도장 작업 일정이 차질을 빚거나 공급업체들이 안전 재고를 더 많이 보유해야 하는 상황도 여전히 발생합니다.

2010년 이후 신규 항공기 설계에서 탄소섬유강화플라스틱(CFRP)의 비중은 매년 증가하고 있습니다. 복합재는 알루미늄과 다른 열팽창 계수를 가지므로 도료는 더 높은 탄성과 강력한 접착 촉진제가 필요합니다. 자동화된 레이업 기술은 부품이 고온 경화 과정에 노출되게 하여 공급업체로 하여금 열안정성을 위해 수지 재구성을 요구합니다. PPG의 크로메이트 프리 에어로크론 전기 도장 프라이머와 AkzoNobel의 복합재용 수성 에폭시는 차세대 제품에서 지속가능성과 기판 호환성이 어떻게 융합되고 있는지 보여줍니다.

미국 환경보호청(EPA)의 2025년 에어로졸 코팅 규정은 반응성 한계를 강화하는 한편, 캘리포니아 남부 대기질 관리국(SCAQMD)은 더 엄격한 기준을 제시하며 선도하고 있습니다. 유럽은 이미 REACH 규정에 따라 육가 크롬을 단계적으로 폐지하고 있습니다. 규정 준수를 위해 제형 개발사들은 수성 또는 고고형분 시스템으로 전환해야 하며, 이는 도포 복잡성을 높이고 때로는 내구성을 희생시키기도 합니다. 성능 저하 없이 저배출 화학 기술을 확보한 공급업체들은 선점 효과를 얻을 수 있습니다.

에폭시 시스템은 2024년 항공우주 코팅 시장의 58.19% 점유율을 차지했으며, 금속 및 복합재 기판 모두에 우수한 접착력을 발휘하여 우위를 유지하며 연평균 6.11% 성장할 것으로 전망됩니다. 이 점유율은 항공우주 코팅 시장 규모에 가장 큰 기여를 의미하며, 제형 개발업체의 수익 가시성을 뒷받침합니다. 폴리우레탄은 우수한 자외선 저항성으로 인해 최상층 코팅재로 선호되며, 아크릴은 신속한 경화가 필수인 틈새 시장에서 활용됩니다.

인증 관행이 에폭시의 주도적 위치를 공고히 하지만, 공급업체들은 규제 금지를 회피하기 위해 크롬 프리 버전 개발에 투자 중입니다. 불소수지 및 실리콘 블렌드는 엔진 카울링과 배기 시스템의 고온 틈새 시장을 개척하고 있습니다. 에폭시가 양적 우위를 유지하는 가운데, 특수 수지들이 점진적인 마진 확보가 예상됩니다.

수성 코팅으로의 전환은 오염 부과금 및 보건 및 안전 규정 강화에 의해 주도되고 있습니다. 아크조노벨의 최신 프라이머는 수성 시스템이 이제 습식 경화 환경에서 달성 불가능하다고 여겨졌던 접착력 및 유연성 목표를 충족할 수 있음을 보여줍니다. 그럼에도 사막 기반 항공기 등 급속 부식 위험이 높은 극한 기후 환경에서는 도입이 더딘 실정입니다.

북미는 2024년 전 세계 매출의 38.92%를 차지했으며, 이는 보잉의 워싱턴 및 사우스캐롤라이나 생산 확대와 캐나다의 지역 항공기 및 엔진 클러스터 덕분입니다. 이 지역의 성숙한 규제 생태계는 인증 절차를 간소화하여 기존 업체들에게 우위를 제공합니다. 그러나 다가오는 노동력 부족은 생산량 증가를 제한하고 더 많은 마감 작업을 멕시코로 이동시킬 수 있으며, 여러 OEM 업체들이 멕시코에 하위 조립 라인을 개설했습니다. 환경 규제도 더욱 강화되면서 항공우주 코팅 시장 전반에 걸쳐 수성 탑코트와 전기 도료 프라이머로의 전환이 가속화되고 있습니다.

아시아태평양 지역은 2030년까지 연평균 6.52%의 성장률을 기록할 것으로 예상되는 가장 빠르게 성장하는 시장입니다. 인도의 생산 상쇄 정책과 중국의 국내 대형 제트기 추진 정책으로 인해 도장 수요가 최종 조립 공장에 더 가까운 곳으로 이동하고 있습니다. 공급업체들은 관세 절감과 적시 납품 개선을 위해 지역별 혼합 공장을 건설 중입니다. 싱가포르, 말레이시아, 필리핀의 급성장하는 MRO 허브는 애프터마켓 수요를 더욱 확대합니다. 그러나 인증 역량과 숙련된 도장 인력이 여전히 부족해 기술 이전 파트너십이 핵심입니다.

유럽은 프랑스, 독일, 스페인의 에어버스 시설과 영국 및 이탈리아의 1차 복합재 전문업체를 통해 강세를 유지합니다. 엄격한 REACH 규제로 크롬 프리 프라이머의 조기 도입이 촉진되며, 유럽 공장들은 이후 글로벌화되는 지속가능성 기술 발전의 시험장으로 자리매김하고 있습니다. 브렉시트는 관세 서류 작업을 추가했으나, 양자 항공 안전 협정 덕분에 코팅 흐름에 실질적 변화는 없었습니다. 동유럽 국가들은 낮은 인건비로 부품 작업을 유치하며, 공급업체들이 신규 위성 공장을 포괄하기 위해 유통망을 확대하도록 압박하고 있습니다.

The Aerospace Coatings Market size is estimated at USD 4.89 billion in 2025, and is expected to reach USD 6.51 billion by 2030, at a CAGR of 5.89% during the forecast period (2025-2030).

Commercial aircraft build rates remain the primary growth engine, underpinned by sustained passenger traffic recovery, while composite-intensive airframe designs require new coating chemistries that command premium pricing. Regulatory pressure on volatile organic compounds (VOC) and hexavalent chromium accelerates the shift toward water-borne and chrome-free systems, prompting suppliers to recalibrate R&D portfolios. OEM demand from Airbus, Boeing, and tier-1 integrators anchors baseline volume, yet maintenance, repair, and overhaul (MRO) activity for aging fleets is expanding faster, reshaping product-mix and service requirements. Regionally, North America still generates the largest revenue pool, but Asia-Pacific shows the quickest expansion as supply chains diversify into India, China and Southeast Asia to mitigate geopolitical risk. Overall, the aerospace coatings market exhibits moderate concentration as a handful of qualified suppliers leverage decades of certification know-how to defend share and set the pace of technology adoption.

Boeing is building 737-series jets at 38 aircraft per month and is seeking Federal Aviation Administration clearance to lift output to 42 units, while Airbus aims to hand over 770 jetliners in 2025 after supply-chain headwinds clipped earlier plans for 800. Each narrow-body requires roughly 150-200 gallons of primer, topcoat, and specialty finishes, so even single-digit rate hikes exert a multiplier effect on coating volume. Builder focus has shifted from cost to delivery reliability, giving qualified coating vendors greater contractual leverage. Fleet modernisation programs centred on fuel-efficient models sustain this momentum, though shortages in engines and cabin interiors can still disrupt paint-shop slots and force suppliers to hold more safety stock.

The share of carbon-fibre-reinforced polymer in new aircraft designs has risen annually since 2010. Composites possess a different coefficient of thermal expansion than aluminium, so coatings need higher elasticity and tougher adhesion promoters. Automated lay-up techniques also expose parts to high-temperature cures, compelling vendors to reformulate resins for thermal stability. PPG's chromate-free Aerocron electrocoat primer and AkzoNobel's waterborne epoxy for composites illustrate how sustainability and substrate compatibility are converging in next-generation products.

The United States Environmental Protection Agency's 2025 aerosol-coating rule tightens reactivity limits, while California's SCAQMD leads the charge with even stricter thresholds. Europe is already phasing out hexavalent chromium under REACH. Compliance forces formulators toward waterborne or high-solids systems, raising application complexity and sometimes sacrificing durability. Suppliers that master low-emission chemistry without performance trade-offs gain a first-mover edge.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Epoxy systems held 58.19% share of the aerospace coatings market in 2024 and are forecast to grow at 6.11% CAGR, maintaining primacy because they bond well to both metal and composite substrates. This share translates into the largest aerospace coatings market size contribution, underpinning revenue visibility for formulators. Polyurethanes follow as the topcoat of choice due to superior UV resistance, whereas acrylics find niche use where rapid cure is mandatory.

Certification inertia anchors epoxy's leadership, yet suppliers are investing in chrome-free versions to skirt regulatory bans. Fluoropolymer and silicone blends are carving out high-temperature niches on engine cowlings and exhaust systems. As epoxy maintains volume leadership, specialised resins are expected to secure incremental margin.

Solvent-borne coatings accounted for 54.18% of the aerospace coatings market size in 2024, but their share is slowly slipping as water-borne products expand at 6.09% CAGR. Airlines and MRO shops value the faster dry-to-fly windows solvents provide, keeping them relevant for critical path tasks. Powder and electrocoat technologies, though still small, are winning spots on landing-gear and internal cavities for waste-reduction benefits.

The pivot toward water is driven by pollution levies and health-and-safety mandates. AkzoNobel's latest primer shows that water-borne systems can now meet adhesion and flexibility targets once thought unattainable in humid cure environments. Nevertheless, adoption lags in extreme-climate applications such as desert-based carriers where flash rusting risk remains high.

The Aerospace Coatings Market Report Segments the Industry by Resin Type (Epoxy, Polyurethane, and More), Technology (Solvent-Borne, Water-Borne, and Other Technologies), End User (Original Equipment Manufacturer (OEM), and Maintenance Repair and Operations (MRO)), Aviation Type (Commercial Aviation, Military Aviation, and General Aviation), and Geography (Asia-Pacific, North America, Europe, and More).

North America generated 38.92% of global revenue in 2024 on the back of Boeing's ramp-up in Washington and South Carolina, plus Canada's regional aircraft and engine clusters. The region's mature regulatory ecosystem streamlines qualification, giving incumbents an edge. A looming labour shortage, however, could cap output growth and push more finishing work to Mexico, where several OEMs have opened sub-assembly lines. Environmental regulation is also stiffer, accelerating the migration to water-borne topcoats and electrocoat primers across the aerospace coatings market.

Asia-Pacific is the fastest-growing arena, set for a 6.52% CAGR through 2030. India's production offset policies and China's push for domestic large jets relocate paint demand closer to final assembly. Suppliers are erecting regional blending plants to reduce tariffs and improve just-in-time delivery. Southeast Asia's burgeoning MRO hubs in Singapore, Malaysia and the Philippines further widen aftermarket pull. Yet certification capacity and trained applicators remain in short supply, making technology transfer partnerships critical.

Europe retains a stronghold via Airbus facilities in France, Germany and Spain, coupled with tier-1 composite specialists in the United Kingdom and Italy. Stringent REACH rules force early adoption of chrome-free primers, positioning European plants as test beds for sustainability advances that later globalise. Brexit adds customs paperwork but has not materially shifted coating flow thanks to bilateral aviation safety agreements. Eastern European nations are drawing component work through lower labour costs, compelling suppliers to broaden distribution to cover new satellite plants.