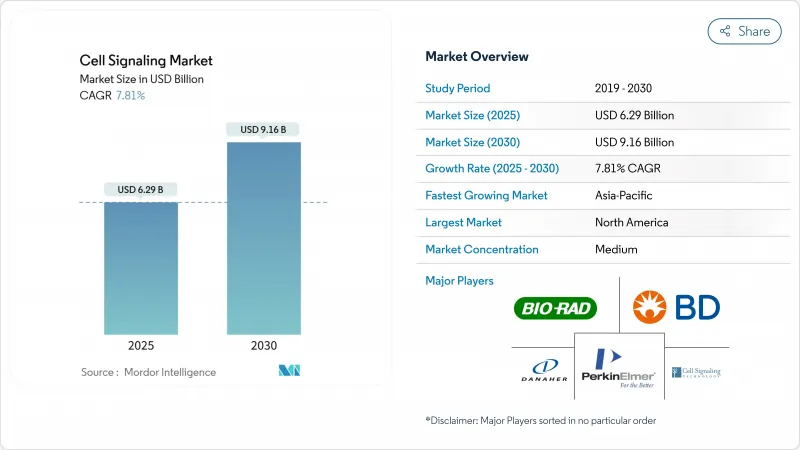

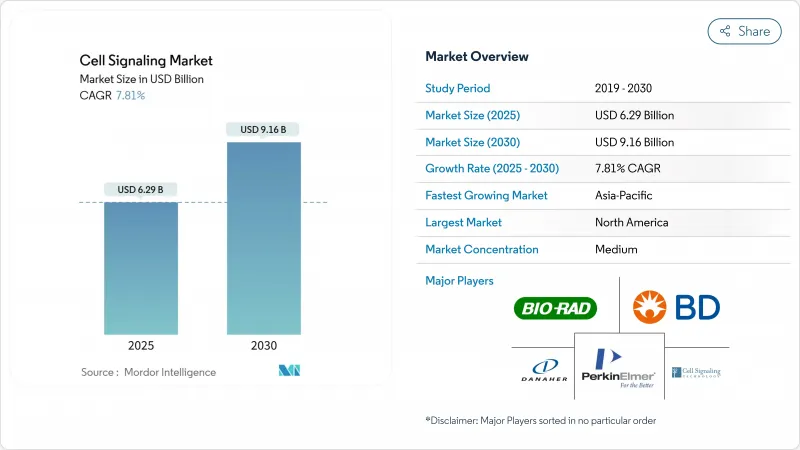

세포 신호전달 시장 규모는 2025년에 62억 9,000만 달러로 추정되고, CAGR 7.81%로 성장할 전망이며, 2030년에는 91억 6,000만 달러에 이를 것으로 예측됩니다.

자동 유동 세포 계측기, 질량 분광계, 멀티플렉스 이미징 시스템에 대한 지속적인 설비 투자를 통해 적은 수작업으로 더 풍부한 세포 데이터를 얻을 수 있습니다. 북미는 미국 국립위생연구소(NIH)의 관대한 조성금과 수용적인 규제 환경을 배경으로 리더십을 유지하고 있지만, 아시아태평양은 일본, 한국, 중국이 임상 등급의 세포 및 유전자 치료용 일회용 생물반응기의 생산 능력을 확대하고 있기 때문에 가장 빠른 성장을 보이고 있습니다. 스테로이드 불응성 급성 이식편 대 숙주병에 대한 최초의 동종간엽계 간질세포 제형인 리온실이 미국 식품의약국(FDA)에 의해 2024년에 승인됨에 따라 그 기세는 더욱 강해지고 있습니다. 선도적인 개발 기업은 분석 개발 주기를 단축하고 시약 선택을 개선하는 인공지능 모듈을 갈아 입어 소규모 경쟁사의 진입 장벽을 높이고 있습니다.

만성질환 및 자가면역질환의 이환율의 상승에 의해 CAR-T세포를 생체내에서 생성하는 모듈형 지질 나노입자 플랫폼으로 자본을 돌려주고, 장시간의 생체외 제조가 불필요해지고 있습니다. 간엽계 간질세포(MSC) 이식은 류마티스 관절염과 전신 경화증에서 설득력 있는 관해율을 계속해서 생산하고 있으며, 지불측의 수용 확대에 박차를 가하고 있습니다. 고소득 국가에서는 고령화가 진행되어 관절변성증이나 대사 증후군을 대상으로 한 재생의료 임상시험이 고도의 경로 분석과 기능적 면역 측정에 대한 수요를 더욱 가속화하고 있습니다.

Thermofisher Scientific은 4년 동안 20억 달러(연구개발 비용에 5억 달러)를 투자하여 고충격 분석 시스템의 미국 생산을 강화합니다. 이와 병행하여 오리오니스 바이오사이언시스는 제넨텍사로부터 분자 접착제 프로그램용으로 1억 500만 달러의 계약금을 획득하고 있으며, 차세대 모달리티 플랫폼에 대한 벤처 기업의 의욕을 뒷받침하고 있습니다. 아시아태평양 전역에서는 정부 펀드가 세포 치료 프로세스 개발 기지에 자금을 투입하기 시작했으며 현지 생물제제 제조업체의 기술 이전 일정을 단축하고 있습니다.

턴키 스펙트럼 사이토미터는 1대당 75만 달러를 넘어 학술 보조금 사이클을 늘리고 저소득 지역에서의 업그레이드를 늦추고 있습니다. 치료 등급의 단일클론항체 제작은 단일 적응증으로 연간 15,000-14만 달러가 소요되므로 하류 소모품 예산이 부풀어 오릅니다. 제조 수탁기관의 가동률은 50% 이하로 보고되고 있으며, 수급 미스매치가 플랫폼 소유자의 비용 회수의 과제를 악화시키고 있습니다.

내분비 신호는 2024년에 세포 신호전달 시장의 34.76%를 차지했고, 장기 스케일에서 호르몬 수용체 분석을 필요로 하는 대사 및 생식 연구를 지원합니다. 오토클린 신호전달은 CAGR로 가장 빠른 8.9%에 도달할 전망이며, 이는 종양학 프로그램에서 종양 증식을 지배하는 자가자극 루프의 해명이 진행되고 있기 때문입니다. 파라크린 신호전달은 조직 복구 모델과의 연관성을 유지하며, 시냅스 메커니즘은 신경과학 연구비 증가의 혜택을 받고 있습니다.

자기 분비 피드백에 대한 메커니즘의 해명이 진행되어 경로 선택적 억제제와 동반진단제의 설계에 박차가 걸리고 있습니다. 파라크린에 대한 인사이트는 림프절 케모카인 구배를 가져오도록 프로그램된 나노입자 캐리어에 영감을 주었습니다. 이러한 진보가 함께, 세포 신호전달 시장은 경로 생물학을 정밀 치료제로 전환하는 데 확실히 초점을 맞추었습니다.

2024년 매출의 55.67%를 장비가 차지했는데, 이는 실험실의 핵심 인프라를 구성하는 분석 워크스테이션의 고가의 티켓 가격을 반영하고 있습니다. 그러나 소모품은 분석량에 따라 시약 주문이 반복되기 때문에 CAGR은 9.6%가 되어 이를 웃도는 기세입니다. 특히 분산형 CRO 시설에서는 유동 세포 계측용 스키드, 고해상도 이미징 칩, 마이크로플루이딕스 카트리지 교체 주기가 주류가 되고 있습니다.

재조합 항체는 기존의 폴리클로날 시약보다 특이성이 우수하기 때문에 소모품 수요도 증가하고, 지금까지 미국의 실험실에서 연간 18억 달러의 비용이었던 재현성의 실패가 줄어듭니다. 항체 검증 데이터 세트를 제공하는 공급업체는 고객의 점착성을 높이고 마진을 증가시킬 수 있습니다.

북미는 NIH 보조금의 안정성, 벤처 캐피탈의 두께, 재생 후보의 규제 심사를 단축하는 FDA 지침에 힘입어 2024년 세계 매출의 42.45%를 창출했습니다. Thermo Fisher의 여러 해에 걸쳐 20억 달러의 국내 설비 증강은 고처리량 장치에 대한 수요 지속에 대한 공급업체의 자신감을 뒷받침하고 있습니다. 승인되지 않은 줄기세포 치료를 허용하는 주법이 제정되었고, 선도적인 스폰서는 컴플라이언스의 단편화를 피해야 합니다.

각국 정부가 바이오프로세스 세제 우대조치를 확대하고 희소질환 치료법의 승인 촉진책을 전개하는 가운데 아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 8.45%로 성장을 선도할 전망입니다. 중국만으로도 1억 2,000만개의 세포를 커버하는 싱글셀 오믹스 아틀라스가 작성되어 AI 트레이닝 데이터 세트에 비교할 수 없는 어노테이션의 깊이를 제공합니다. 일본의 독립행정법인 의약품의료기기종합기구(PMDA)는 미국의 획기적 신약 지정 지표와 보조를 맞추기 위해 사키가케 패스트트랙의 개량을 계속하고 있습니다.

유럽은 공급망의 투명성을 강화하는 한편, 세포 치료에 대한 엄격한 지령에 의해 시험 개시까지의 기간이 연장되고 있습니다. 이 지역의 의약품 원약(API) 시장은 연률 5.78% 증가로 추이하고 있으며, 합성 API가 최대, 바이오 API가 급성장하고 있습니다. 병원이 동반진단제를 표준 치료 경로에 통합하고 있기 때문에 암 영역은 여전히 유럽에서 가장 역동적인 적응증이 되고 있습니다.

The cell signaling market size is valued at USD 6.29 billion in 2025 and is forecast to reach USD 9.16 billion by 2030, advancing at a 7.81% CAGR.

Growth rests on sustained capital spending for automated flow cytometers, mass spectrometers and multiplex imaging systems that generate richer cellular data with fewer manual steps. North America retains leadership on the back of generous National Institutes of Health (NIH) grants and a receptive regulatory climate, while Asia-Pacific posts the fastest gains as Japan, South Korea and China expand single-use bioreactor capacity for clinical-grade cell and gene therapies. Momentum is reinforced by the U.S. Food and Drug Administration's (FDA) 2024 clearance of Ryoncil, the first allogeneic mesenchymal stromal cell product for steroid-refractory acute graft-versus-host disease, which signals wider acceptance of cell-based interventions. Leading suppliers are sharpening artificial-intelligence modules that cut assay-development cycles and improve reagent selection, thereby raising entry barriers for smaller competitors.

The rising incidence of chronic and autoimmune disorders is redirecting capital toward modular lipid-nanoparticle platforms that generate CAR-T cells in vivo, eliminating lengthy ex-vivo manufacturing. Mesenchymal stromal cell (MSC) transplantation continues to produce compelling remission rates across rheumatoid arthritis and systemic sclerosis, fueling wider payer acceptance. As aging populations swell in high-income economies, regenerative medicine trials targeting joint degeneration and metabolic syndrome further accelerate demand for advanced pathway analyses and functional-immune readouts.

Thermo Fisher Scientific is investing USD 2 billion over four years-USD 500 million earmarked for R&D-to anchor U.S. production of high-impact analytical systems, a move mirroring similar manufacturing onshoring initiatives by rivals. In parallel, Orionis Biosciences secured USD 105 million upfront from Genentech for molecular-glue programs, underscoring venture appetite for next-generation modality platforms. Across Asia-Pacific, sovereign wealth funds have started funneling capital into cell-therapy process-development hubs, compressing technology-transfer timelines for local biologics manufacturers.

Turn-key spectral cytometers exceed USD 750,000 per unit, stretching academic grant cycles and delaying upgrades in lower-income regions. Therapeutic-grade monoclonal antibody production still costs between USD 15,000 and USD 140,000 annually for a single indication, which inflates downstream consumable budgets. Contract manufacturing organizations report sub-50% utilization rates, revealing a supply-demand mismatch that exacerbates cost-recovery challenges for platform owners.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Endocrine signaling held 34.76% of the cell signaling market in 2024, underpinning metabolic and reproductive studies that require hormone-receptor assays at organ scale. Autocrine signaling is on track for the fastest 8.9% CAGR because oncology programs increasingly dissect self-stimulating loops that govern tumor proliferation. Paracrine signaling retains relevance for tissue-repair models, while synaptic mechanisms benefit from higher neuroscience funding.

Growing mechanistic clarity around autocrine feedback has spurred design of pathway-selective inhibitors and companion diagnostics. Paracrine insights have inspired nanoparticle carriers programmed to home lymph-node chemokine gradients, an approach now in mid-phase breast-cancer trials. Together, these advances keep the cell signaling market firmly focused on translating pathway biology into precision therapeutics.

Instruments accounted for 55.67% of 2024 revenue, reflecting the hefty ticket price of analytical workstations that constitute the core lab infrastructure. Consumables, however, are poised to outpace with a 9.6% CAGR as recurring reagent orders scale with assay volume. Flow-cytometry skids, high-resolution imaging chips and microfluidic cartridges dominate replacement cycles, especially in decentralized CRO facilities.

Consumables demand also rises because recombinant antibodies outperform conventional polyclonal reagents on specificity, trimming reproducibility failures that previously cost U.S. labs up to USD 1.8 billion annually. Suppliers offering antibody-validation data sets gain customer stickiness and incremental margins.

The Cell Signaling Market Report is Segmented by Signaling Type (Endocrine Signaling, and More), Product (Instruments and Consumables), Technology (Flow Cytometry, Mass Spectrometry, and More), Pathway (AKT/PI3K Signaling, and More), Application (Drug Discovery & Development, and More), End User (Pharma & Biotech Companies, and More), Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 42.45% of global revenue in 2024, underpinned by NIH grant stability, venture capital depth and FDA guidance that shortens regulatory review for regenerative candidates. Thermo Fisher's multi-year USD 2 billion domestic build-out underscores supplier confidence in continued demand for high-throughput instrumentation. State-level legislation permitting certain unapproved stem-cell interventions introduces compliance fragmentation that large sponsors must now navigate.

Asia-Pacific leads growth at a 8.45% CAGR through 2030 as governments expand bioprocess tax incentives and roll out accelerated approval pathways for rare-disease therapies. China alone has compiled single-cell-omics atlases covering 120 million cells, offering unparalleled annotation depth for AI-training datasets. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) continues to refine its Sakigake fast-track to keep pace with U.S. breakthrough designation metrics.

Europe holds material share yet lags on speed: stringent cell-therapy directives extend trial-setup timelines, though they bolster supply-chain transparency. The region's active-pharmaceutical-ingredient (API) market is climbing 5.78% annually, with synthetic APIs largest today and biotech APIs growing fastest. Oncology remains Europe's most dynamic indication as hospitals integrate companion diagnostics into standard-of-care pathways.