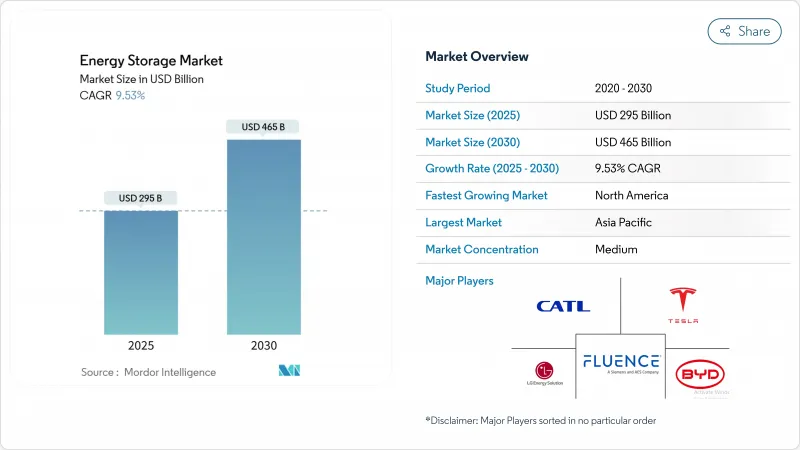

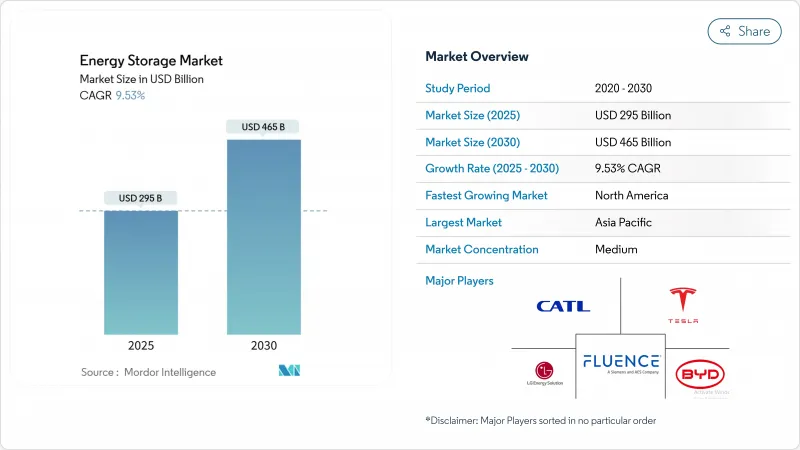

에너지 저장 시장 규모는 2025년에 2,950억 달러로 평가되었고 예측 기간 중(2025-2030년) CAGR은 9.53%를 나타낼 것으로 예측되며, 2030년에는 4,650억 달러에 달할 전망입니다.

이러한 규모 확대는 배터리 팩 가격 하락, 독립형 저장 장치에 대한 정책적 인센티브, 그리고 태양광 및 풍력 포트폴리오 확대로 인한 유연한 용량 수요 증가에 기반합니다. 리튬-인산철(LFP) 기술의 급속한 비용 감소, 6시간 이상 지속 가능한 배터리 에너지 저장 시스템(BESS)으로의 전환, 그리고 교통 수단의 가속화된 전기화는 모두 현재의 성장 궤도를 강화하고 있습니다. 경쟁 역학 역시 유동적입니다. 중국 공급업체들은 비용 리더십과 글로벌 계약을 추구하는 반면, 북미 및 유럽 통합업체들은 소프트웨어, 그리드 형성 제어, 안전 규정 준수를 강조합니다. 열, 중력, 유동 배터리와 같은 장시간 기술들은 다시간 출력 가능성과 낮은 수명 주기 비용을 중시하는 시장에서 리튬이온 배터리를 보완하기 시작했습니다.

2024년 115달러/kWh라는 사상 최저 가격은 LFP를 장시간 BESS의 핵심 화학물질로 확고히 자리매김시켰습니다. 2024년 설치량의 88%를 차지한 이 화학물질의 안전성 프로필은 허가 및 보험 장벽을 완화하는 동시에 전력사가 가스 피크 발전소를 대체하여 최대 10시간 방전이 가능하게 합니다. 중국산 공급 과잉은 구매자 협상력을 강화하며 미국과 유럽에서 멀티기가와트 규모의 조달 라운드를 가속화하고 있습니다.

미국 인플레이션 감축법(IRA)에 따른 투자 세액 공제는 2024년 11.9GW의 저장 용량 추가를 가능케 했으며, 2025년 18.2GW의 파이프라인을 확보했습니다. 유사한 추진력은 재생에너지 점유율 확대를 의무화하는 EU 재생에너지 지침 III와 흐름 배터리 혁신을 촉진하는 중국의 장시간 저장 목표에서 비롯됩니다. 캘리포니아 에너지 위원회의 장시간 시범사업 지원 2억 7천만 달러 프로그램과 같은 공공 보조금은 실험실 규모와 상업적 규모 간의 격차를 해소하고 있습니다.

전 세계적으로 펌프식 수력 발전이 여전히 약 9,000GWh를 저장하고 있지만, 유럽, 일본 및 북미 일부 지역에서는 신규 개발 가능성이 희박합니다. 허가 절차만 8년 이상 소요될 수 있어 기술의 비용 경쟁력이 약화됩니다. 폐광 갱도를 재활용하는 폐쇄형 루프 개념 및 중력 시스템(Energy Vault의 사르데냐 프로젝트 등)은 장시간 저장 옵션을 유지하기 위한 시도이지만, 아직 유사 규모에서 검증되지 않았습니다.

배터리 시스템은 2024년 에너지 저장 시장 규모에서 490억 달러를 차지했으며, 2030년까지 연평균 16.5%의 성장률을 보일 것으로 전망됩니다. kWh당 115달러 미만의 LFP 팩은 8시간 출력으로 일일 차익 거래 주기에서 기존 양수식 수력 발전과 경쟁할 수 있게 합니다. 한편, 저수지 부지 부족, 긴 허가 절차, 환경 제약으로 인해 유럽과 일본에서 신규 프로젝트가 지연되면서 펌프식 수력 발전의 에너지 저장 시장 점유율은 2024년 84%로 하락했습니다.

열, 중력, 유동 배터리는 며칠 또는 일주일 단위의 저장 수요가 있는 분야에서 주목받고 있습니다. 최근 4억 500만 달러의 자금 지원을 받은 철-공기 기술은 100시간 방전 시간을 약속하는 반면, 아연-브롬 및 바나듐 유동 스택은 리튬 공급 리스크를 회피합니다. 하이브리드 토폴로지가 확산 중입니다. 중력 또는 CAES(압축 공기 에너지 저장) 모듈이 기저 부하 방전을 공급하는 동안 배터리는 그리드 사건 발생 후 초기에 부가 서비스를 처리합니다.

에너지 저장 시장 보고서는 기술(배터리, 양수식 수력 발전, 열 에너지 저장, 압축 공기 에너지 저장, 액체 공기/극저온 저장, 플라이휠 에너지 저장, 기타), 연결성(온그리드,오프 그리드), 응용 분야(그리드 규모 유틸리티, 가정용, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류됩니다.

아시아태평양 지역은 2024년 매출의 43%를 차지했으며 공급망 확장의 핵심입니다. 중국은 2025년까지 재생에너지 비중 33% 목표에 힘입어 2024년 단일 국가로 81GWh를 설치했으며, 이는 전 세계 나머지 지역을 합친 규모보다 큽니다. 호주는 높은 지붕형 태양광 보급률과 변동성 있는 요금으로 인해 결합형 배터리의 투자 회수 기간이 단축되면서 가정용 도입을 주도하고 있습니다. 인도는 2025년 최초의 독립형 유틸리티 BESS를 도입하며 하이브리드 재생에너지 단지를 겨냥한 신흥 조달 사이클을 예고했습니다.

북미는 2030년까지 연평균 14.5% 성장률로 가장 빠르게 성장하는 지역입니다. IRA(인플레이션 감축법)의 독립형 저장 장치에 대한 직접 인센티브는 기존 태양광 연계 요건을 완화시켜 캘리포니아와 텍사스를 중심으로 기가와트급 프로젝트 파이프라인을 촉발했습니다. 미국 에너지정보청(EIA)은 2025년 배터리로 18.2GW의 신규 유틸리티 규모 용량이 공급될 것으로 전망하며, 이는 태양광 증설 규모에 이어 두 번째로 큰 규모입니다. 극한 기상 현상으로 인한 정전 사태 이후 지역별 복원력 강화에 대한 관심은 마이크로그리드 및 공동체 저장 체계 수요를 더욱 촉진하고 있습니다.

유럽의 2023년 발전 용량은 전년 대비 94% 증가한 1,720만킬로와트시가 되었습니다. 독일은 높은 소매 가격과 간소화된 허가 절차 덕분에 2024년 말까지 1.9GWh 규모의 대규모 시스템을 가동하며 시장을 주도하고 있습니다. 영국과 프랑스는 뒤처졌으나 용량 시장 수익과 계통 균형 서비스로 뒷받침되는 멀티기가와트 규모의 프로젝트 파이프라인을 보유하고 있습니다. 토탈에너지스가 독일에서 태양광과 2시간 저장장치를 결합해 일중 전력 수요를 평준화하는 100MW/200MWh 신규 사이트를 구축한 사례에서 보듯, 유럽 대륙은 주거용에서 유틸리티 규모 프로젝트로 전환 중입니다.

The Energy Storage Market size is estimated at USD 295 billion in 2025, and is expected to reach USD 465 billion by 2030, at a CAGR of 9.53% during the forecast period (2025-2030).

This scale-up rests on falling battery pack prices, policy incentives that reward standalone storage, and a rising need for flexible capacity as solar and wind portfolios expand. Rapid cost declines in lithium-iron-phosphate (LFP) technology, the pivot to >6-hour battery energy storage systems (BESS), and the accelerating electrification of transport all reinforce the current growth trajectory. Competitive dynamics are equally fluid: Chinese suppliers are pursuing cost leadership and global contracts, while North American and European integrators emphasize software, grid-forming controls, and safety compliance. Longer-duration technologies-thermal, gravity, and flow batteries-are beginning to complement lithium-ion in markets that prize multi-hour dispatchability and low lifetime cost.

Record lows of USD 115/kWh in 2024 firmly repositioned LFP as the anchor chemistry for long-duration BESS. With 88% share of 2024 installations, the chemistry's safety profile is easing permitting and insurance barriers while enabling utilities to displace gas peakers for up to 10 hours of discharge. Chinese oversupply is reinforcing buyer leverage, accelerating multigigawatt procurement rounds in the United States and Europe.

Investment tax credits under the U.S. Inflation Reduction Act (IRA) unlocked 11.9 GW of storage additions in 2024 and a pipeline of 18.2 GW for 2025. Similar momentum stems from the EU Renewable Energy Directive III, which mandates higher renewables penetration, and China's long-duration storage targets that foster flow-battery innovation. Public grants, such as the California Energy Commission's USD 270 million program for long-duration pilots, are bridging the gap between lab and commercial scale.

Although pumped hydro still stores about 9,000 GWh worldwide, greenfield prospects are scarce in Europe, Japan, and parts of North America. Permitting can exceed 8 years, eroding the technology's cost advantage. Closed-loop concepts and gravity systems repurposing disused mine shafts, such as Energy Vault's Sardinia project, aim to keep long-duration options alive but remain unproven at comparable scale.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Battery systems delivered USD 49 billion of the energy storage market size in 2024 and are forecast to expand at a 16.5% CAGR through 2030. LFP packs under USD 115/kWh are allowing 8-hour dispatch to compete with conventional pumped hydro for daily arbitrage cycles. Meanwhile, the energy storage market share of pumped-storage hydroelectricity slipped to 84% in 2024 as reservoir-site scarcity, long permitting cycles, and environmental constraints stalled new projects in Europe and Japan.

Thermal, gravity, and flow batteries are gaining traction where multi-day or week-long storage is desired. Iron-air technology, backed by USD 405 million of recent funding, promises 100-hour discharge windows, while zinc-bromine and vanadium flow stacks avoid lithium supply risks. Hybrid topologies are proliferating: gravity or CAES modules supply baseload discharge while batteries handle ancillary services in the first minutes after a grid event.

The Energy Storage Market Report is Segmented by Technology (Batteries, Pumped-Storage Hydroelectricity, Thermal Energy Storage, Compressed Air Energy Storage, Liquid Air/Cryogenic Storage, Flywheel Energy Storage, and Others), Connectivity (On-Grid and Off-Grid), Application (Grid-Scale Utility, Residential Behind-The-Meter, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa)

Asia-Pacific retained 43% of 2024 revenue and is central to supply-chain scale-up. China alone installed 81 GWh in 2024-more than the rest of the world combined-bolstered by its 33% renewable-energy share target for 2025. Australia leads residential adoption as high rooftop-solar penetration and volatile tariffs accelerate payback for paired batteries. India's first stand-alone utility BESS in 2025 signals an emerging procurement cycle aimed at hybrid renewable parks.

North America is the fastest-growing region at a projected 14.5% CAGR through 2030. The IRA's direct incentive for stand-alone storage flattened the previous solar-coupling requirement, unleashing gigawatt-scale pipelines centered in California and Texas. The U.S. Energy Information Administration expects batteries to supply 18.2 GW of new utility-scale capacity in 2025, second only to solar additions. Regional focus on resilience after extreme-weather outages further reinforces demand for microgrids and community-storage schemes.

Europe recorded a 94% y-o-y capacity jump in 2023, reaching 17.2 GWh. Germany dominates with 1.9 GWh of large-scale systems in operation by late-2024, aided by high retail prices and streamlined permitting. The United Kingdom and France trail but have multigigawatt pipelines backed by capacity-market revenue and grid-balancing services. The continent's shift from residential to utility-scale projects is evident in TotalEnergies' new 100 MW/200 MWh German site that pairs solar with two-hour storage for intraday smoothing.