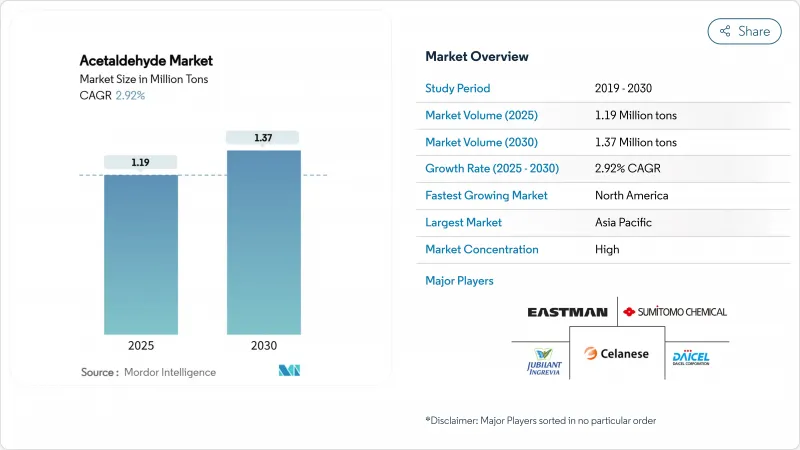

아세트알데히드 시장 규모는 2025년에 119만 톤으로 평가되었고, 예측기간 중(2025-2030년) CAGR은 2.92%를 나타낼 전망이며, 2030년에 137만 톤에 달할 것으로 예측됩니다.

이 확장은 아세트산, 피리딘 염기, 펜타에리트리톨, 아세테이트 에스터 등 고부가가치 유도체의 중간체로서 화학 물질의 확고한 역할을 반영하며, 이는 저휘발성 유기화합물(VOC) 용매 시스템, 지속 가능한 코팅, 순환형 PET 재활용 솔루션을 가능케 합니다. 아시아태평양 지역의 통합 석유화학 네트워크는 가격 발견을 계속 주도하는 반면, 북미 생산자들은 셰일 유래 에탄과 획기적인 에탄-아세트알데히드 촉매 기술을 활용해 성장세를 가속화하고 있습니다. 경쟁 구도는 원료 유연성 확보, 의약품 합성을 위한 우수한 순도 등급 달성, 고급 PET 재활용용 특수 제거 첨가제 공급이 가능한 기업들로 이동하고 있습니다. 예측 기간 동안 기술 도입, 규제 압력, 지속가능성 인증이 아세트알데하이드 시장 전반의 가치 창출을 결정할 것입니다.

제약 제조 규모가 급속히 확대되면서 복잡한 약물 분자는 아세트알데히드 유래 피리딘 중간체에 점점 더 의존하고 있습니다. 2030년까지 3.94%의 연평균 복합 성장률(CAGR)은 아세트알데히드 순도 개선이 반응 수율 향상과 FDA cGMP 요건 준수를 가능케 하는 종양학 및 신경학 치료 분야에서 이 유도체의 전략적 중요성을 강조합니다. 아시아 제네릭 제조사들은 다목적 활성제약성분(API) 라인을 확장 중이며, 이는 고순도 아세트알데히드 등급의 지역 소비 증가로 이어집니다. 맞춤형 의학 전환은 특수한 빌딩 블록을 요구하여 피리딘 사슬의 견고한 물량 성장을 보장합니다. 잔류 불순물 저감 인증을 획득한 생산자들은 프리미엄 계약을 따내며, 아세트알데히드 시장에서 품질 주도 수요의 선순환을 강화합니다.

코팅 제형 개발사들은 바이오 기반 알키드 및 고속 경화 UV 시스템으로 전환 중이며, 아세트알데히드와 포름알데히드로 합성된 펜타에리트리톨은 필수 원료로 자리매김했습니다. 북미 및 유럽 공급사들은 자동차 제조업체들이 생산 주기 단축 및 에너지 소비 절감을 위한 UV 경화성 클리어 코트를 채택함에 따라 펜타에리트리톨 수요가 가속화되고 있다고 보고합니다. 최근 연구에 따르면 펜타에리트리톨을 함유한 바이오 알키드 수지는 기존 수지(34.7%) 대비 90일 내 70%의 생분해성을 달성하여 가격 프리미엄을 뒷받침하는 지속가능성 우위를 보입니다. 코팅 산업의 저휘발성유기화합물(VOC) 요구는 아세테이트 에스터 공용매 사용을 촉진하여 아세트알데히드 가치 사슬 전반의 유도체 시너지를 강화합니다. 결과적으로 펜타에리트리톨은 증산 수요를 이끌며 아세트알데하이드 시장의 안정적 수요 기반을 형성하고 있습니다.

현재, 세계의 아세트산 제조 능력의 85% 이상이 메탄올 카보닐화 공정을 채택하여 아세트알데하이드 중간체 사용을 배제하고 기존 수요 기반을 약화시키고 있습니다. Rh 및 Ir 촉매 공정은 우수한 선택성과 에너지 효율을 제공하여 아세트알데히드 기반 아세트산에 대한 신규 투자를 위축시킵니다. 동아시아 거대 기업들의 증설은 이러한 추세를 더욱 부각시켜 아세트알데히드 CAGR 전망치에서 0.4% 포인트를 감소시킵니다. 이러한 장기적 하락을 상쇄하기 위해 생산자들은 고부가가치 피리딘, 펜타에리트리톨, PET 재활용 첨가제 시장으로 진출하며 아세트알데히드 시장 내 포트폴리오 우선순위를 재정의하고 있습니다.

2024년 아세트산은 아세트알데히드 시장 점유율의 28.39%를 유지했으나, 메탄올 카보닐화 공정에 의한 구조적 대체로 인해 물량 성장률은 여전히 부진한 상태입니다. 반면, 아시아태평양 지역의 제약 생산량 급증에 힘입어 피리딘 및 피리딘 염기 시장은 2030년까지 연평균 3.94%의 견실한 성장률을 기록할 전망입니다. 페인트 산업의 펜타에리트리톨 수요 증가가 점진적 확장을 이끌고 있으며, 아세테이트 에스터는 저휘발성 유기화합물(저VOC) 시스템 규제를 충족시키는 핵심 요소다. 종합적으로 특수 유도체 시장은 성숙한 아세트산 시장의 정체에도 불구하고 아세트알데히드 시장 규모를 안정적으로 유지하고 있습니다.

고부가가치 틈새 시장으로의 전환은 순도 요구를 높여 정제 컬럼, 분자체, 연속 증류 제어에 대한 자본 투자를 유도합니다. 공정 내 분석 기술을 숙달한 생산자는 계약 프리미엄을 확보하는 반면, 뒤처진 기업은 일반 상품 시장으로 전락할 위험에 직면합니다. 부틸렌글리콜, 클로랄, 과아세트산은 여전히 틈새 시장이지만, 화장품, 제약, 수처리 분야의 지속적인 수요로 자산 활용도는 양호한 상태를 유지합니다. 이러한 계층화된 유도체 포트폴리오는 일반 상품의 물량과 특수 제품의 마진을 균형 있게 조화시켜 아세트알데히드 시장의 장기적 회복탄력성을 정의합니다.

아세트알데히드 보고서는 유도체(피리딘 및 피리딘 염기, 펜타에리트리톨, 아세트산, 아세테이트 에스터 등), 최종 사용자 산업(접착제, 식품 및 음료, 도료 및 코팅, 제약, 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 전망은 물량(톤) 기준으로 제공됩니다.

아시아태평양 지역은 2024년 글로벌 수요의 57.81%를 차지했으며, 이는 중국의 세계적 규모의 석유화학 단지 및 통합된 방향족-아세틸 체인에 기반을 두고 있습니다. 일본의 다이셀(Daicel) 코퍼레이션은 기술적 정교함을 강화하고 있으며, 인도의 고다바리 바이오리파이너리즈(Godavari Biorefineries)는 석유화학 및 바이오 기반 흐름을 연결합니다.

북미는 2030년까지 연평균 3.18% 성장률을 기록할 전망으로, 에탄-아세트알데하이드 촉매 기술과 순환 화학에 대한 명확한 규제 지원이 이를 뒷받침합니다. 셀라네즈의 클리어 레이크 플랫폼과 지역 PET 재활용 시설 확장은 저탄소·고순도 생산으로의 전환을 보여주는 사례입니다.

유럽의 지속가능성 이념은 고성능 파생상품에 대한 틈새 수요를 유지하는 반면, 남미와 중동 및 아프리카는 에탄올 고부가가치화 및 원료 우위 석유화학 허브를 통해 점진적으로 생산 능력을 확대하고 있습니다. 이러한 지역적 모자이크는 성숙한 대량 시장과 개척지 성장을 균형 있게 조화시켜 아세트알데히드 시장의 글로벌 분산을 강화합니다.

The Acetaldehyde Market size is estimated at 1.19 million tons in 2025 and is expected to reach 1.37 million tons by 2030, at a CAGR of 2.92% during the forecast period (2025-2030).

This expansion reflects the chemical's entrenched role as an intermediate for high-value derivatives such as acetic acid, pyridine bases, pentaerythritol, and acetate esters that enable low-VOC solvent systems, sustainable coatings, and circular PET recycling solutions. Asia-Pacific's integrated petrochemical networks continue to shape price discovery, while North American producers gain momentum by leveraging shale-derived ethane and breakthrough ethane-to-acetaldehyde catalysis. Competitive positioning is shifting toward players that can secure feedstock flexibility, achieve superior purity grades for pharmaceutical syntheses, and offer specialized scavenging additives for advanced PET recycling. Over the forecast horizon, technology adoption, regulatory pressure, and sustainability credentials will determine value capture across the acetaldehyde market.

Pharmaceutical manufacturing is scaling rapidly, and complex drug molecules increasingly rely on acetaldehyde-derived pyridine intermediates. The 3.94% CAGR to 2030 underscores the derivative's strategic relevance for oncology and neurology therapies, where acetaldehyde purity improvements deliver higher reaction yields and regulatory compliance with FDA cGMP requirements. Asian generic producers are expanding multi-purpose active-pharmaceutical-ingredient lines, which lifts regional consumption of high-purity acetaldehyde grades. The personalized-medicine shift calls for specialized building blocks, ensuring robust volume growth for pyridine chains. Producers that can certify low residual impurities win premium contracts, reinforcing a virtuous cycle of quality-driven demand in the acetaldehyde market.

Coatings formulators pivot toward bio-based alkyd and fast-curing UV systems, and pentaerythritol, synthesized from acetaldehyde and formaldehyde, has become indispensable. North American and European suppliers report accelerating off-takes as automakers adopt UV-curable clear coats that shorten production cycles and cut energy consumption. Recent research showed bio-alkyds featuring pentaerythritol achieve 70% biodegradability in 90 days versus 34.7% for conventional resins, a sustainability edge that supports price premiums. The coatings industry's low-VOC imperative boosts acetate-ester co-solvents, reinforcing derivative synergies along the acetaldehyde value chain. Consequently, pentaerythritol draws incremental capacity additions, anchoring stable demand in the acetaldehyde market.

More than 85% of global acetic-acid capacity now employs methanol carbonylation, obviating acetaldehyde intermediacy and eroding a legacy demand pillar. The Rh- and Ir-catalyzed route delivers superior selectivity and energy efficiency, depressing new investments in acetaldehyde-based acetic acid. Incremental expansions by East-Asian giants accentuate the swing, removing 0.4 percentage points from the acetaldehyde CAGR forecast. To offset this secular decline, producers push into higher-value pyridine, pentaerythritol, and PET-recycling additives, redefining portfolio priorities within the acetaldehyde market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Acetic acid retained a 28.39% slice of the acetaldehyde market share in 2024, but its volume growth remains muted amid structural substitution by methanol carbonylation. Conversely, pyridine and pyridine bases are set to register a robust 3.94% CAGR through 2030, propelled by surging pharmaceutical output in Asia-Pacific. The paints sector's appetite for pentaerythritol drives incremental additions, while acetate esters underpin compliant low-VOC systems. Collectively, specialty derivatives insulate the acetaldehyde market size against stagnation in the mature acetic-acid pool.

The migration to high-value niches heightens purity requirements, inviting capital investments in purification columns, molecular sieves, and continuous distillation control. Producers that master in-process analytics secure contract premiums, while laggards risk relegation to commodity pools. Butylene glycol, chloral, and peracetic acid remain niche outlets, yet continued demand from cosmetics, pharmaceuticals, and water treatment keeps asset utilization healthy. This tiered derivative portfolio balances commodity volume with specialty margins, defining long-run resilience for the acetaldehyde market.

The Acetaldehyde Report is Segmented by Derivative (Pyridine and Pyridine Bases, Pentaerythritol, Acetic Acid, Acetate Esters, and More), End-User Industry (Adhesives, Food and Beverage, Paints and Coatings, Pharmaceuticals, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific commanded 57.81% of global demand in 2024, anchored by China's world-scale petrochemical complexes and integrated aromatics-to-acetyl chains. Japan's Daicel Corporation augments technological sophistication, while India's Godavari Biorefineries bridges petrochemical and bio-based streams.

North America is poised for a 3.18% CAGR through 2030, underpinned by ethane-to-acetaldehyde catalysts and clear regulatory tailwinds for circular chemistry. Celanese's Clear Lake platform and regional PET-recycling build-outs exemplify the pivot to low-carbon, high-purity production.

Europe's sustainability ethos sustains niche demand for high-performance derivatives, while South America and Middle-East and Africa gradually scale capacity via ethanol upgrading and feedstock-advantaged petrochemical hubs. This regional mosaic balances mature bulk markets with frontier growth, reinforcing global dispersion of the acetaldehyde market.