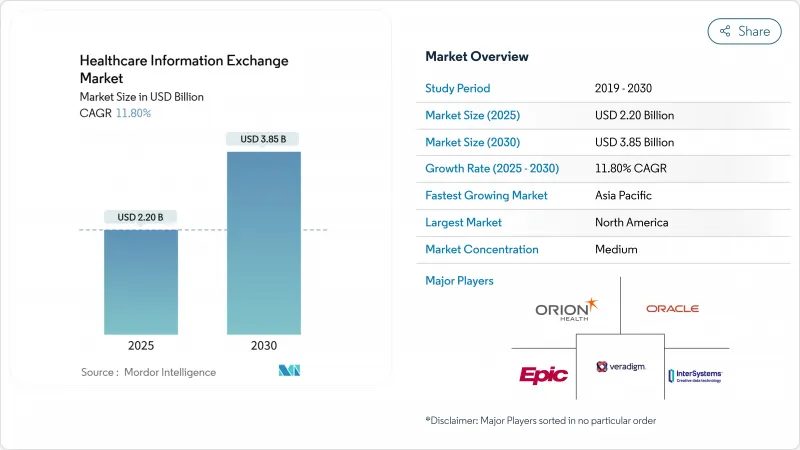

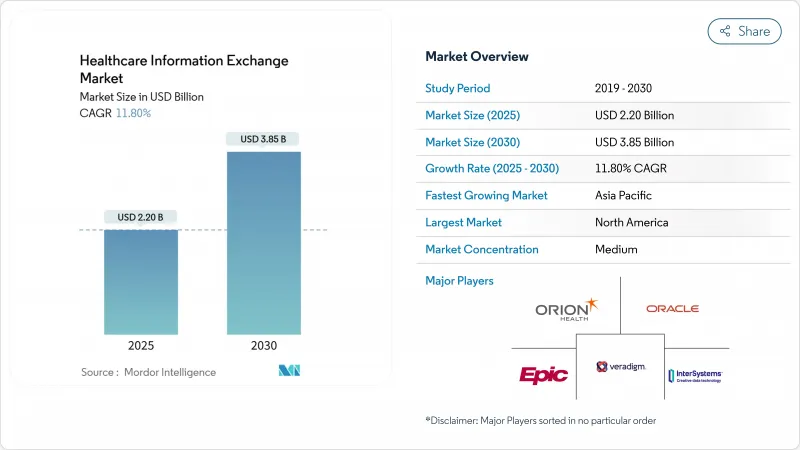

진료 정보 교류 시장 규모는 2025년에 22억 달러로 평가되었고, CAGR은 11.8%를 나타낼 것으로 예측되며 2030년에 38억 5,000만 달러에 이를 전망입니다.

이러한 급속한 확장은 더 엄격한 상호운용성 규정, 강화된 사이버 보안 경계, 가치 기반 진료 모델로의 전환 등 글로벌 디지털 헬스케어 우선순위를 반영합니다. 신뢰할 수 있는 교류 프레임워크 및 공통 협약(TEFCA)과 같은 국가적 프레임워크는 상호운용성 기대치를 강화하는 한편, 의료 제공자들은 현지 통제와 확장성 사이의 균형을 위해 하이브리드 클라우드 아키텍처에 투자하고 있습니다. 중앙 집중형 배포가 여전히 주류를 이루고 있지만, 하이브리드 접근법의 강력한 성장은 데이터 거버넌스 전략의 점진적 재설계를 시사합니다. 한편, 에픽 시스템즈(Epic Systems)의 전국적 TEFCA 도입은 경쟁 구도를 재정의하며, 경쟁사들이 플랫폼 업그레이드와 보안 강화를 가속화하도록 촉구하고 있습니다.

디지털 전환은 기본적인 EHR(전자의무기록) 도입 단계를 넘어, 의료 환경 전반에 걸쳐 실시간 데이터 교류을 가능하게 하는 전사적 상호운용성 플랫폼 단계로 진화했습니다. 병원 그룹들은 운영 효율성과 함께 환자 경험 지표를 우선시하며 표준 기반 데이터 공유 프레임워크에 대한 투자를 확대하고 있습니다. 아시아태평양 지역에서는 의료 제공자들이 고령화 인구와 농촌 지역 접근성 문제에 대응함에 따라 디지털 헬스 인프라에 대한 정부 보조금이 도입을 촉진하고 있습니다. 상호 운용성 도구는 이제 연결된 치료의 중추 신경계 역할을 하며 임상의, 지불 기관 및 공중 보건 기관을 연결합니다. 그 결과 시설 간 데이터 유동성이 가시적으로 증가하여 진료 조정성이 향상되고 중복 검사가 감소했습니다.

공공 부문 투자가 사상 최고 수준에 도달하고 있습니다. 미국 질병통제예방센터(CDC)는 2026년까지 공중보건 데이터 교류을 위해 2억 5,500만 달러를 배정했습니다. 대서양 건너 유럽에서는 ‘유럽 건강 데이터 공간(European Health Data Space)’ 규정을 통해 2031년까지 국경 간 교류 준비를 위해 8억 1,000만 유로를 배정했습니다. 호주는 '마이 헬스 레코드(My Health Record)'에 대한 벤더 연결을 지원하고 있으며, 일본과 한국은 상호운용성을 국가 디지털 헬스 의제의 핵심으로 삼았습니다. 정부 자금은 사용자 기반을 병원 외부로 확대하여 지역 클리닉과 연구 기관이 안전한 교류 네트워크에 참여할 수 있도록 합니다.

교류망 참여에는 상당한 초기 비용, 직원 교육, 다중 벤더 인터페이스 개발이 요구됩니다. 수익성이 낮은 지방 병원들은 명확한 보상 인센티브 없이 대규모 지출을 정당화하기 어렵다. 자금이 확보되더라도 프로젝트 복잡성으로 실질적 혜택이 지연되어 일부 기관은 단계적 도입이나 참여 제한을 선택합니다. 하이브리드 모델은 자본 부담을 줄이지만 완전히 해소하지는 못합니다. 에지 처리 및 비즈니스 연속성 계획 수립을 위해 여전히 현지 하드웨어가 필요하기 때문입니다.

중앙 집중형 아키텍처는 2024년 진료 정보 교류 시장 점유율의 46.76%를 유지했으며, 직관적인 거버넌스와 단순화된 벤더 관리로 선호되었습니다. 그러나 단일 장애 지점에 대한 우려가 증가함에 따라 하이브리드 프레임워크는 13.45%의 연평균 성장률(CAGR)을 기록하고 있습니다. 병원이 민감한 데이터를 현장에 보관하면서 국가적 연결성을 위해 클라우드 노드를 활용함에 따라 하이브리드 배포 방식의 진료 정보 교류 시장 규모는 급격히 확대될 것으로 전망됩니다. 체인지 헬스케어의 서비스 중단 사태는 과도한 중앙화의 위험성을 보여주며, 이사회 차원의 복원력 논의로 이어졌습니다. 하이브리드 도입 기업들은 주요 다운타임을 피하면서 점진적으로 마이그레이션할 수 있는 능력도 높이 평가합니다. 벤더들은 FHIR 기반 클라우드 서비스와 병행하여 로컬 데이터 거주를 허용하는 모듈형 툴킷을 출시하고 있습니다. 이 이중 레이어 모델은 재해 복구를 지원하고, 병상 애플리케이션의 지연 시간을 줄이며, 유럽 및 아시아의 데이터 현지화 의무를 충족시킵니다.

성장세는 병원들이 규제 요구사항에 따라 진화하는 유연한 토폴로지를 선호할 것임을 시사합니다. TEFCA 연결성이 성숙해짐에 따라 하이브리드 참여 기관들은 지역 데이터베이스 통제권을 포기하지 않고도 전국적 네트워크와 피어링할 수 있습니다. 한편 독일과 인도 등 엄격한 주권 규정이 적용되는 관할 구역에서 운영되는 기관들 사이에서는 연합형 구현이 지속되고 있습니다. 이러한 역학 관계는 종합적으로 하이브리드 구성을 기존 온프레미스 시스템과 완전 호스팅 솔루션 간의 가교로 자리매김하게 하여, 2030년까지 진료 정보 교류 시장이 다양한 배포 모델을 유지하도록 보장합니다.

2024년 진료 정보 교류 시장 규모에서 사설 교류망이 62.45%를 차지했으며, 이는 맞춤형 워크플로를 추구하는 병원 네트워크에 크게 기인합니다. 그러나 공공 HIE 프로그램은 안전망 클리닉의 진입 장벽을 낮추는 연방 및 주 정부 보조금에 힘입어 14.65%의 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. CDC의 데이터 현대화 계획은 공중보건 노드의 클라우드 이전 비용을 지원하는 등 이러한 변화를 잘 보여줍니다. 유럽 건강 데이터 공간(European Health Data Space) 역시 국가 기관에 인프라 구축을 주도하도록 하는 유사한 입장을 취하고 있습니다. 공공 플랫폼은 증후군 감시 및 만성질환 등록 시스템 구축을 점점 더 용이하게 하며, 이는 민간 시스템에서 종종 간과되는 기능들입니다.

결과적으로 정부는 민간 이해관계자들이 따라야 할 아키텍처 기준을 설정함으로써 전반적인 상호운용성 성숙도를 높이고 있습니다. 소규모 의사 그룹은 무상 가입 혜택을 통해 더 넓은 의뢰 네트워크와 의사결정 지원 자원에 접근할 수 있습니다. 이러한 요소들이 종합적으로 공공 교류 플랫폼의 위상을 높여 시장 구성을 점진적으로 재조정하는 동시에 개방형 데이터 공유의 사회적 가치를 강화하고 있습니다.

북미는 포괄적인 규제 의무와 강력한 연방 자금 지원에 힘입어 2024년 매출의 47.54%를 유지했습니다. 에픽 시스템즈가 표준화된 API를 통해 1,000개 이상의 병원을 연결함에 따라 TEFCA(Telemedicine Exchange for Care Access) 채택이 빠르게 확대되고 있습니다. 캐나다와 멕시코는 국가적 원격의료 투자에 힘입어 추가 성장을 이루고 있습니다. 체인지 헬스케어(Change Healthcare) 보안 침해로 인한 31억 달러의 피해는 병원 이사회로 하여금 사이버 보안 예산을 증액하도록 촉발했으며, 이는 필수 인프라로 간주되는 교류 구독 서비스를 강화하는 계기가 되었습니다.

유럽은 유럽 건강 데이터 공간(European Health Data Space) 규정을 통해 데이터 공유 환경을 재편하고 있으며, 2031년까지 국경 간 교류 준비를 위해 8억 1천만 유로를 배정했습니다. 핀란드와 같은 국가들은 이미 칸타(Kanta) 플랫폼을 통해 성숙한 전국적 서비스를 선보이며 다른 회원국들에게 청사진 역할을 하고 있습니다. EHDS 프레임워크는 혁신과 프라이버시 균형을 맞춘 표준화된 동의 메커니즘을 도입하여, 공급업체들이 지역 시장을 위한 데이터 보호 모듈을 강화하도록 촉진하고 있습니다.

아시아태평양 지역은 12.56%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 지역으로, 막대한 공공 투자와 인구학적 압박의 혜택을 받고 있습니다. 일본의 국가 플랫폼 구축, 호주의 마이 헬스 레코드(My Health Record) 개선, 인도의 대표적 사업인 아유슈만 바라트 디지털 미션(Ayushman Bharat Digital Mission)은 정부의 의지를 보여줍니다. 클라우드 네이티브 배포는 신흥 시장이 레거시 하드웨어 단계를 건너뛰도록 하여 신규 진입자에게 유리한 환경을 조성합니다. 원격의료 및 병원-홈 모델에 대한 벤처 캐피털 유입은 실시간 데이터 오케스트레이션 수요를 자극하여, 해당 지역의 전체 진료 정보 교류 시장 성장 기여도를 높입니다.

The health information exchange market size is valued at USD 2.20 billion in 2025 and is projected to reach USD 3.85 billion by 2030, reflecting an 11.8% CAGR.

This rapid expansion mirrors global digital-health priorities, including stricter interoperability rules, growing cybersecurity vigilance, and the shift to value-based care models. National frameworks such as the Trusted Exchange Framework and Common Agreement (TEFCA) are reinforcing interoperability expectations, while providers invest in hybrid cloud architectures to balance local control with scalability. Centralized deployments still dominate, yet the hybrid approach's strong growth signals a gradual redesign of data governance strategies. Meanwhile, Epic Systems' nationwide TEFCA roll-out is redefining competitive dynamics, prompting rivals to accelerate platform upgrades and security enhancements.

Digital transformation has moved past basic EHR roll-outs into enterprise-wide interoperability platforms that enable real-time data exchange across care settings. Hospital groups are prioritizing patient-experience metrics alongside operational efficiency, prompting greater investment in standards-based data-sharing frameworks. In Asia-Pacific, government grants for digital-health infrastructure amplify adoption as providers respond to aging populations and rural access challenges. Interoperability tools now function as the central nervous system of connected care, linking clinicians, payers, and public-health agencies. The outcome is a measurable uptick in cross-facility data liquidity, which improves care coordination and reduces redundant testing.

Public-sector investment is reaching unprecedented levels. The U.S. Centers for Disease Control and Prevention earmarked USD 255 million for public-health data exchange through 2026. Across the Atlantic, the European Health Data Space regulation set aside EUR 810 million for cross-border exchange readiness by 2031. Australia is financing vendor connections to My Health Record, while Japan and South Korea have placed interoperability at the heart of national digital-health agendas. Government funds are widening the user base beyond hospitals, enabling community clinics and research bodies to join secure exchange networks.

Joining an exchange often demands substantial upfront fees, staff training, and multi-vendor interface development. Rural hospitals with thin margins struggle to justify large expenditures without clear reimbursement incentives. Even when funding is available, project complexity can delay tangible benefits, leading some organizations to stagger roll-outs or limit participation. Hybrid models reduce-but do not eliminate-capital pressure, as local hardware is still required for edge processing and business-continuity planning.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Centralized architectures retained 46.76% of health information exchange market share in 2024, favored for straightforward governance and simpler vendor management. Yet hybrid frameworks are pacing at a 13.45% CAGR, reflecting mounting concern over single points of failure. The health information exchange market size for hybrid deployments is projected to expand sharply as hospitals keep sensitive data on-site while using cloud nodes for national connectivity. Change Healthcare's outage illustrated the risks of over-centralization, prompting board-level discussions on resiliency. Hybrid adopters also value the ability to migrate incrementally, avoiding major downtime. Vendors are releasing modular toolkits that allow local data residency alongside FHIR-based cloud services. This dual-layer model supports disaster recovery, reduces latency for bedside applications, and meets data-localization mandates in Europe and Asia.

Growth momentum indicates hospitals will favor flexible topologies that evolve with regulatory requirements. As TEFCA connectivity matures, hybrid participants can peer with nationwide networks without relinquishing local database control. Meanwhile, federated implementations persist among institutions operating in jurisdictions with stringent sovereignty rules, such as Germany and India. Collectively, these dynamics position the hybrid configuration as a bridge between traditional on-premise systems and fully hosted solutions, ensuring the health information exchange market retains deployment-model diversity through 2030.

Private exchanges accounted for 62.45% of the health information exchange market size in 2024, largely driven by hospital networks seeking bespoke workflows. Public HIE programs, however, are forecast for a 14.65% CAGR, buoyed by federal and state grants that lower barriers for safety-net clinics. CDC's Data Modernization Initiative exemplifies this shift, underwriting cloud migration costs for public-health nodes. The European Health Data Space takes a similar stance, assigning national authorities to spearhead infrastructure build-out. Public platforms increasingly facilitate syndromic surveillance and chronic-disease registries, functions often overlooked in private systems.

As a result, governments are setting architectural baselines that private stakeholders must match, thereby lifting overall interoperability maturity. Smaller physician groups benefit from no-cost onboarding, gaining access to wider referral networks and decision-support assets. These factors collectively raise the profile of public exchanges, gradually rebalancing market composition while reinforcing the societal value of open data sharing.

The Health Information Exchange Market Report is Segmented by Implementation Model (Centralized / Consolidated, and More), Setup Type (Private and Public), Application (Internal Interfacing, and More), Exchange Type (Direct Exchange, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 47.54% of 2024 revenue, driven by comprehensive regulatory mandates and robust federal funding. TEFCA adoption is expanding quickly as Epic Systems connects more than 1,000 hospitals through standardized APIs. Canada and Mexico add further growth, supported by national telehealth investments. The USD 3.1 billion fallout from the Change Healthcare breach spurred hospital boards to increase cybersecurity budgets, reinforcing exchange subscriptions viewed as essential infrastructure.

Europe is reshaping its data-sharing landscape under the European Health Data Space regulation, which earmarked EUR 810 million for cross-border exchange readiness through 2031. Countries such as Finland already demonstrate mature nationwide services through the Kanta platform, acting as blueprints for other member states. The EHDS framework introduces standardized consent mechanisms that balance innovation with privacy, prompting vendors to enhance data-protection modules for the regional market.

Asia-Pacific, the fastest-growing region at 12.56% CAGR, benefits from heavy public investment and demographic pressures. Japan's national platform build-out, Australia's My Health Record enhancements, and India's flagship Ayushman Bharat Digital Mission illustrate government commitment. Cloud-native deployments allow emerging markets to skip legacy hardware phases, creating fertile ground for new entrants. Venture capital flows to telehealth and hospital-at-home models also stimulate demand for real-time data orchestration, bolstering the region's contribution to overall health information exchange market growth.