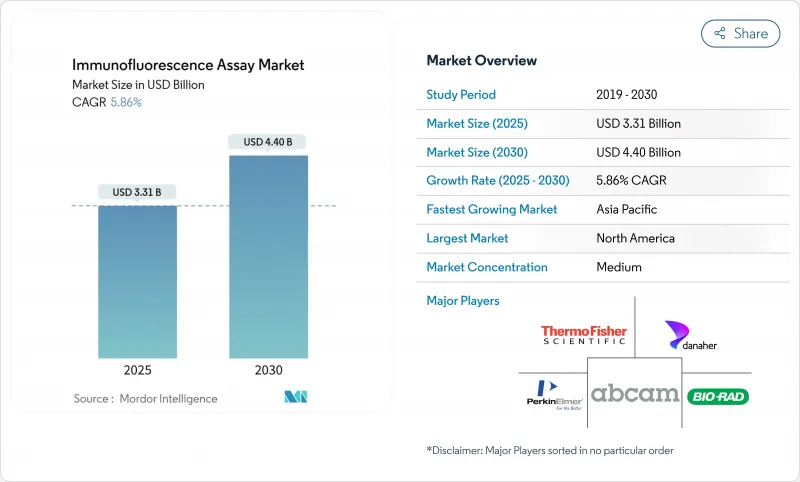

면역형광 어세이 시장 규모는 2025년에 33억 1,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.86%로, 2030년에는 44억 달러에 달할 것으로 예상됩니다.

수동 형광 현미경에서 이미지 분석을 간소화하고 진단 정확도를 높이는 AI 대응 디지털 병리 시스템으로의 전환을 반영한 성장입니다. 정밀의료에서 동반진단의 이용 확대, 감염증 서베이런스의 계속, 자원이 제한된 환경에 적합한 마이크로플루이딕스 POC(Point-of-Care) 플랫폼에 대한 투자에 의해 확대가 강화됩니다. 자동화 장비로의 설비 업그레이드, 대규모 병원 그룹의 표준화된 실험실 개발 검사 프로토콜의 채택은 면역형광 어세이 시장을 더욱 견인하고 있습니다. 그러나 고급 현미경을 통한 비용 압력과 PFAS 기반 형광증백제에 대한 폐기 규칙의 강화는 당면 채용을 억제합니다.

암의 만연과 장기간의 감염이 종양 마커와 병원체를 동시에 검출하는 멀티플렉스 면역형광 플랫폼에 대한 수요를 높이고 있습니다. 95.4%의 정확도를 보여주는 다중 암 조기 발견 검사는 집단 스크리닝에서 고감도 형광 이미징의 가치를 보여줍니다. COVID-19의 워크플로우를 적용한 결핵 요지의 병행 진보는 기존 검사 인프라를 보다 광범위한 질병 모니터링 프로그램에 재사용할 수 있음을 강조합니다. 면역형광 어세이 시장의 성장세를 뒷받침하는 것은 이중 효용 프로파일입니다.

보조금 및 의료 시스템의 현대화 계획은 특히 분산 환경에서 작동하는 휴대용 형광 리더와 같은 플랫폼의 배포를 가속화합니다. 유럽의약청(European Medicines Agency)에 의한 신규 결핵진단제의 지원은 신속하고 특이성이 높은 검사에 대한 공공 부문의 뒷받침을 강조하는 것입니다. 미국에서 FDA는 표준화된 실험실에서 개발된 검사 모니터링과 관련된 연간 35억 1,000만 달러의 이익을 추정하고 있으며, 검사실이 준수하는 자동화 장비를 채택하도록 장려하고 있습니다. 이러한 자금 조달 경로는 면역형광 어세이 시장의 구매 결정에 직접적인 영향을 미칩니다.

차세대 시퀀싱과 라벨이 없는 다중광자 이미징은 보다 높은 다중화와 정량적인 엄격성을 실현하여 기존에는 면역형광에 의존하고 있던 프로젝트를 빨아들이게 되었습니다. 체액에 직접 작용하는 마이크로플루이딕스 바이오센서는 시료량과 소요시간을 줄여 경쟁을 더욱 격화시키고 있습니다. 단일 세포 분석 기술은 세포의 불균일성과 질병 메커니즘에 대한 전례없는 인사이트를 제공하고 면역형광 애플리케이션을 보완하는 연구 능력을 제공하지만 궁극적으로 특정 면역형광 애플리케이션을 대체할 수 있습니다. 이러한 대체 플랫폼과 인공지능의 통합은 기술의 복잡성을 줄이고 진단 정확도를 향상시켜 채택을 가속화하고 있으며, 면역형광 시장의 성장에 지속적인 경쟁 압력을 제공합니다.

2024년, 시약 및 키트는 매출의 62.23%를 차지했지만, 실험실이 자동화에 축발을 두고 있는 가운데, 장비 매출은 CAGR 6.95%로 가장 급속히 성장하고 있습니다. 플랫폼 제공업체는 구독 번들에서 하드웨어와 이미지 분석 소프트웨어를 결합하여 현금흐름 장애물을 낮추고 다년간 서비스 계약을 육성하고 있습니다. 업그레이드 가능한 스펙트럼 흐름 사이토미터와 원격 모니터가 있는 슬라이드 스테이너는 모듈식 디자인이 자산 수명 주기를 늘리고 투자 회수를 가속화하는 방법을 보여줍니다.

슬라이드 로더, 캘리브레이션 비드, 바코드 스캐너 등의 액세서리 구매도 비례하여 증가합니다. AI 모듈이 안정적인 조명과 정확한 스테이지 제어를 요구함에 따라 구매자는 고해상도 대물 렌즈와 환경 인클로저를 플랫폼 현대화의 필수적인 부분으로 취급합니다. 이러한 생태계의 관점은 면역형광 어세이 시장 전체의 장기 조달 계획을 지원합니다.

자가면역 프로토콜이 확립되어 있기 때문에 2024년 점유율은 간접법이 65.63%를 유지했지만, 신속한 싱글스텝 염색을 필요로 하는 종양학 프로그램에서는 직접 면역형광이 보다 강한 관심을 보이고 있습니다. 병리 의사가 수술 중 결정 지침으로 더 짧은 분석주기를 중시하기 때문에 채용이 증가합니다. HER2 저치 유방암 검사 증가는 증폭 아티팩트가 없는 정량적 역치 설정을 직접 접합체가 어떻게 지원하는지를 보여줍니다.

간접 방법은 항핵 항체 패널과 같은 광범위한 스크리닝에 중요하며, HEp-2 기질을 활용하여 여러 자가항체 클래스를 동시에 시각화합니다. 비용 효과적인 높이와 기존의 상환 코드로 루틴 검사실에서의 우위성을 유지하고 있습니다. 그럼에도 불구하고 면역형광 어세이 시장은 급속도와 특이성이 배치 경제성을 능가하는 직접 형식으로 점유율의 전환이 진행될 것으로 예측됩니다.

북미는 2024년 세계 매출의 40.02%를 차지했으며 자동 슬라이드 스캐너의 대규모 설치 기반과 품질 시스템에 대한 기대를 명확히 하는 FDA의 지원책에 의한 혜택을 받았습니다. 1인당 건강 관리 지출이 높기 때문에 교체 사이클이 빠르며 자본 투자에 대한 세제 우대 조치가 중견 병원 도입 위험을 줄입니다. Thermofisher Scientific의 Olink사 인수(31억 달러)를 포함한 기업 활동은 플랫폼 포트폴리오를 통합하고 메뉴 폭을 넓히고 지역 리더십을 강화하고 있습니다.

유럽은 성능 주장의 조화를 촉구하는 엄격하지만 예측 가능한 IVDR의 틀에 힘입어 뒤를 이었습니다. 이 지역의 면역형광 어세이 시장 규모는 국경을 넘은 상환 협정과 대규모 바이오 마커 컨소시엄을 지원하는 Horizon Europe의 연구 자금으로부터 혜택을 받고 있습니다. IVDR의 이행 기한이 연장됨에 따라 중소기업은 제품 공급을 중단하지 않고 적합성 평가를 완료할 여유가 있었습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 7.26%로 가장 빠르게 성장하는 지역입니다. 오토비오 다이아그노스틱스(Autobio Diagnostics)와 같은 중국 국내 패자들은 분석 장비의 대량 생산을 통해 검사 단가를 낮추고 카운티 수준의 병원 접근성을 확대하고 있습니다. 인도에서는 Meril Diagnostics와 같은 국산 기업이 풍토병 감염을 위한 마이크로플루이딕스 형광 카트리지를 조정하여 농촌 시장의 두 자리 성장을 지원합니다. 정부가 지원하는 의료보험제도가 분산형 진단약에 대한 수요를 더욱 환기해 동남아시아 전역의 면역형광 어세이 시장을 뒷받침하고 있습니다.

The Immunofluorescence Assay Market size is estimated at USD 3.31 billion in 2025, and is expected to reach USD 4.40 billion by 2030, at a CAGR of 5.86% during the forecast period (2025-2030).

Growth reflects the migration from manual fluorescence microscopy to AI-enabled digital pathology systems that streamline image analysis and raise diagnostic precision. Expansion is reinforced by the wider use of companion diagnostics in precision medicine, continued infectious-disease surveillance, and investment in microfluidic point-of-care platforms suited to resource-limited settings. Capital equipment upgrades toward automated instruments, together with large hospital groups adopting standardized laboratory-developed test protocols, further propel the immunofluorescence assay market. However, cost pressure from advanced microscopes and tightened disposal rules on PFAS-based fluorophores temper near-term adoption.

Cancer prevalence and lingering infectious-disease burdens elevate demand for multiplex immunofluorescence platforms that detect tumor markers and pathogens in the same run. Multi-cancer early-detection tests demonstrating 95.4% accuracy showcase the value of high-sensitivity fluorescence imaging in population screening. Parallel advances in tuberculosis point-of-care assays adapted from COVID-19 workflows highlight how existing test infrastructure can be repurposed to serve broader disease-monitoring programs. This dual-utility profile underpins the growth momentum observed across the immunofluorescence assay market.

Targeted grants and health-system modernization schemes accelerate platform rollouts, notably portable fluorescence readers that function in decentralized settings. The European Medicines Agency's backing of novel tuberculosis diagnostics underscores a public-sector push for rapid, high-specificity tests. In the United States, the FDA estimates USD 3.51 billion annualized benefits tied to standardized laboratory-developed test oversight, encouraging labs to adopt compliant automated instruments. Such funding channels directly influence purchase decisions in the immunofluorescence assay market.

Next-generation sequencing and label-free multiphoton imaging now deliver higher multiplexing and quantitative rigor, siphoning projects that would traditionally rely on immunofluorescence. Microfluidic biosensors that work directly with body fluids further tighten competition by trimming sample volume and turnaround time. Single-cell analysis technologies are providing unprecedented insights into cellular heterogeneity and disease mechanisms, offering research capabilities that complement but may eventually supersede certain immunofluorescence applications. The integration of artificial intelligence with these alternative platforms is accelerating their adoption by reducing technical complexity and improving diagnostic accuracy, creating sustained competitive pressure on immunofluorescence market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2024, reagents and kits generated 62.23% of revenue, yet instrument sales are rising fastest at 6.95% CAGR as labs pivot to automation. Platform providers couple hardware with image-analysis software in subscription bundles, smoothing cash-flow hurdles and nurturing multi-year service contracts. Upgradable spectral-flow cytometers and remote-monitored slide stainers exemplify how modular designs stretch asset lifecycles and speed return on investment.

Accessory purchases scale proportionally, covering slide loaders, calibration beads, and barcode scanners. As AI modules demand consistent illumination and precise stage control, buyers increasingly treat high-resolution objectives and environmental enclosures as integral parts of platform modernization. This ecosystem view anchors long-range procurement plans across the immunofluorescence assay market.

Indirect techniques kept 65.63% share in 2024 thanks to established autoimmune protocols, yet direct immunofluorescence exhibits stronger appetite from oncology programs requiring rapid single-step staining. Adoption climbs as pathologists value shorter assay cycles when guiding intraoperative decisions. Rising HER2-low breast-cancer testing illustrates how direct conjugates support quantitative thresholding without amplification artifacts.

Indirect methods retain importance for broad screens such as antinuclear antibody panels, leveraging HEp-2 substrates to visualize multiple autoantibody classes concurrently. Their cost-effectiveness and existing reimbursement codes ensure continued dominance in routine labs. Still, the immunofluorescence assay market anticipates incremental share migration to direct formats where turnaround and specificity trump batch economy.

The Immunofluorescence Assay Market Report is Segmented by Product (Reagents and Kits, Instruments, Accessories), Immunofluorescence Type (Indirect Immunofluorescence, Direct Immunofluorescence), Application (Cancer Diagnostics and Research, and More), End User (Hospital and Reference Laboratories, and More), and Geography (North America, Europe, and More. The Market Forecasts are Provided in Terms of Value (USD).

North America held 40.02% of global revenue in 2024, benefiting from large installed bases of automated slide scanners and a supportive FDA pathway that clarifies quality-system expectations. High per-capita healthcare spending enables faster replacement cycles, and tax incentives for capital investment reduce adoption risk for mid-sized hospitals. Corporate activity, such as Thermo Fisher Scientific's USD 3.1 billion purchase of Olink, consolidates platform portfolios and widens menu offerings, reinforcing regional leadership.

Europe follows closely, aided by stringent but predictable IVDR frameworks that encourage harmonized performance claims. The immunofluorescence assay market size for the region benefits from cross-border reimbursement pacts and Horizon Europe research funding that underwrites large biomarker consortia. Extended IVDR transition deadlines give SMEs breathing room to complete conformity assessments without halting product availability.

Asia-Pacific is the fastest-growing territory at 7.26% CAGR through 2030. China's domestic champions, such as Autobio Diagnostics, scale high-volume analyzer production, lowering cost-per-test and expanding access in county-level hospitals. India sees indigenous firms like Meril Diagnostics tailoring microfluidic fluorescence cartridges for endemic infections, supporting double-digit rural market growth. Government-sponsored health-insurance schemes further unlock demand for decentralized diagnostics, propelling the immunofluorescence assay market across Southeast Asia.