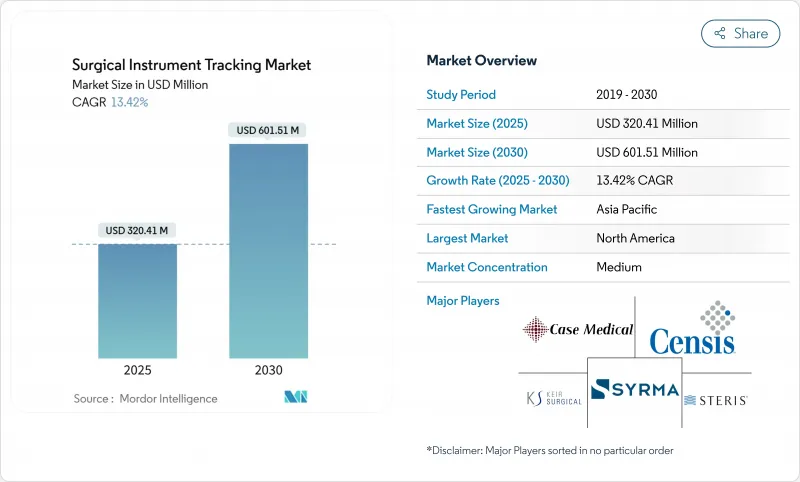

수술 기구 추적 시장은 2025년에 3억 2,041만 달러로 추정되고, 2030년에는 6억 151만 달러에 이를 것으로 예상되며, CAGR 13.42%로 성장할 전망입니다.

이 궤도는 규제 기한의 엄격화, 의료 제공업체가 매년 24억 달러를 부담하는 수술 기구의 체류에 의한 경제적 부담, 데이터 주도형 수술실(OR) 환경에 대한 급속한 축족을 반영합니다. 케어팀은 독립 트래커가 아닌 보다 광범위한 수술기 소프트웨어와 통합하는 솔루션을 점점 더 요구하고 있으며, 이 변화는 2024년에 출시된 존슨 엔드 존슨 메도텍의 Polyphonic 생태계에 나타났습니다. RFID 대응의 자동화, 디바이스 식별자(UDI) 규제의 의무화, 보험사에 의한 미사고에 대한 벌칙 등이 수술 기구 추적 시장을 2자리 확대 노선에 확실히 유지하는 핵심적인 성장 요인이 되고 있습니다.

병원과 기기 제조업체들은 현재 미국과 EU에서 중복되는 UDI 마일스톤에 직면해 있습니다. EUDAMED는 2026년 1분기에 재사용할 수 있는 장비의 데이터베이스 등록을 의무화하고 있습니다. 컴플라이언스 위반은 시장 진입을 방해하기 때문에 추적 시스템은 규제 데이터 수집과 GUDID 및 EUDAMED 교환 모두에 필수적입니다. 조달 팀은 입증된 감사 추적, 세계 고유 장비 식별자(UDI) 호환성, 듀얼 데이터베이스 연결성을 갖춘 공급업체를 선호하며 경쟁의 토우를 컴플라이언스 실적가 가장 넓은 공급업체로 좁히고 있습니다.

IoT 연결을 통해 RFID 태그는 수동 식별자에서 위치 정보, 사이클 수 및 살균 상태를 실시간으로 브로드캐스트하는 노드로 승화합니다. Innovative Perioperative Technologies는 AT&T의 세계 SIM을 활용하여 병원 네트워크 전반에 걸쳐 예지 보전 대시보드를 제공합니다. 안테나 설계의 진보로 금속이 밀집된 수술실에서의 신호 손실을 방지하고 미들웨어의 통합으로 ERP 플랫폼에 데이터를 보내 자동 재주문을 할 수 있게 되었습니다. 시설은 현재 바코드 교체뿐만 아니라 운영 인텔리전스 향상으로 프로젝트를 정당화하고 있습니다.

태그, 리더, 미들웨어 및 시스템 통합을 포함한 RFID의 완전한 도입은 사이트당 10만 달러를 초과할 수 있으며 소규모 병원의 경우 장벽이 될 수 있습니다. 그러나 Emerald사의 벤치마크에 따르면 기구의 분실 회피 및 트레이 수의 감소로 18-24개월에 투자 회수가 가능합니다. 가치있는 성형과 심장 세트로 시작하는 단계적 롤아웃을 통해 자본 비용은 여러 예산 주기에 걸쳐 ROI 증가를 동시에 증명할 수 있습니다.

바코드 스캐닝은 2024년 매출의 59.91%를 차지하며 많은 시설들이 무균 처리를 위해 기존 프린터와 스캐너를 유지하고 있습니다. 그러나 RFID의 CAGR은 14.34%로 자동 카운트, 일괄 읽기, IoT 통합을 위한 재구성을 강조하고 있습니다. 포장된 트레이를 읽고 멸균기의 통과를 몇 초 안에 기록하는 RFID의 능력은 바쁜 OR에 중요한 KPI인 회전 시간을 단축합니다. 저가형 기기에는 바코드를 사용하고, 고가용 기기에는 RFID라는 하이브리드 워크플로우를 통해 병원은 완전 자동화에 대비하면서 비용과 속도의 균형을 맞출 수 있습니다. 재사용 가능한 기구에 RFID 트랜스폰더를 삽입하는 것에 대한 FDA 지침은 검증 타임라인을 길게 하지만 일단 클리어되면 접착 라벨로는 달성할 수 없는 라이프사이클 데이터를 해방합니다.

2세대 초고주파(UHF) 태그는 반복적인 오토클레이브 사이클을 견디며 1m 이상의 판독 범위를 유지하며 오독을 줄입니다. 이 시프트는 수술 기구 추적 시장이 결국 RFID로 수렴한다는 것을 시사합니다. 듀얼 테크놀로지 스캐너와 클라우드에 얽매이지 않는 미들웨어가 있는 벤더는 이 과도적인 상황에 대응하기에 가장 적합합니다.

북미는 2024년에 41.98%의 매출을 유지했으며, 초기 단계의 UDI 시행과 지불자의 never event에 대한 환불 거부에 뒷받침되었습니다. 병원은 추적 프로젝트 예산을 맺을 때 감사 대비와 소송 회피를 일상적으로 들고 있습니다. 또한 이 지역에는 주요 하드웨어 혁신자와 클라우드 EHR 공급업체가 집중되어 통합 사이클이 단축되었습니다. 미국의 새로운 주법은 OR 팩의 디지털 CoC 로그를 의무화하고 있으며 수요를 더욱 제도화하고 있습니다.

유럽은 EU MDR 시간표 아래에서 꾸준히 진행되고 있습니다. 예산은 엄격하지만 기기 식별자의 EUDAMED 업로드가 의무화되어 기기 등록의 기본 요건이 됩니다. GDPR(EU 개인정보보호규정)의 한계는 데이터 레지던시 및 암호화에 대한 공급업체의 모니터링을 강화하고 공급업체는 EU 데이터센터와 보안 API를 도입하여 여러 국가에 대한 전개를 만족시킬 수 있도록 합니다. 순환 경제(순환 경제) 목표를 포함한 지속가능성 규칙은 데이터 중심의 유지 보수를 통해 장비 수명을 연장하는 플랫폼에 인센티브를 제공합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 14.42%로 가장 급성장하고 있는 지역으로 의료 보험에 대한 접근 확대, 병원 신설, 기술 친화적인 규제 분위기에 의해 활성화되고 있습니다. 싱가포르의 AI 지원 OR 파일럿, 중국의 스마트 호스피탈 보조금, 인도의 의료기기 추적성의 관민 추진이 비옥한 토양을 창출하고 있습니다. 언어 지원을 현지화하고 구독 금융을 제공하는 공급업체는 기능의 깊이를 희생하지 않고 신흥 시장 가격에 민감합니다. 아시아태평양의 수술 기구 추적 시장 점유율 확대는 여러 시설 체인이 지역 전반에 걸쳐 전개를 확대함에 따라 북미의 우위를 줄일 가능성이 높습니다.

The surgical instrument tracking market reached USD 320.41 million in 2025 and is on course to attain USD 601.51 million by 2030, advancing at a 13.42% CAGR.

This trajectory reflects tightening regulatory deadlines, the financial burden of retained surgical items that cost providers USD 2.4 billion every year, and the rapid pivot toward data-driven operating room (OR) environments. Care teams increasingly demand solutions that integrate with broader perioperative software rather than operate as stand-alone trackers, a shift illustrated by Johnson & Johnson MedTech's Polyphonic ecosystem launched in 2024. RFID-enabled automation, mandatory device-identifier (UDI) regulations, and insurer penalties for never events round out the core growth drivers that keep the surgical instrument tracking market firmly on a double-digit expansion path.

Hospitals and device makers now face overlapping UDI milestones in the US and EU, where EUDAMED requires database registration for reusable instruments in Q1 2026 . Non-compliance bars market entry, making tracking systems essential for both regulatory data capture and exchange with GUDID and EUDAMED. Procurement teams give preference to vendors with proven audit trails, global unique device identifier (UDI) compatibility, and dual-database connectivity, narrowing the competitive field to suppliers with the widest compliance footprints.

IoT connectivity elevates RFID tags from passive identifiers to nodes that broadcast location, cycle counts, and sterilization status in real time. Innovative Perioperative Technologies leverages AT&T's global SIM to deliver predictive maintenance dashboards across hospital networks. Advances in antenna design counteract signal loss in metal-dense ORs, while middleware integrations feed data into ERP platforms for automated re-ordering. Facilities now justify projects on operational-intelligence gains rather than barcode replacement alone.

A full RFID deployment-including tags, readers, middleware, and systems integration-can exceed USD 100,000 per site, a barrier for smaller hospitals. However, Emerald benchmarking shows payback in 18-24 months through lost-instrument avoidance and lower tray counts. Phased rollouts that start with high-value ortho and cardiac sets allow capital costs to span multiple budget cycles while proving incremental ROI.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Barcode scanning commanded 59.91% of 2024 revenue as many facilities retained legacy printers and scanners for sterile processing. Yet RFID's 14.34% CAGR underscores a realignment toward automated counts, bulk reading, and IoT integration that barcodes cannot match. RFID's ability to read through wrapped trays and log sterilizer passes in seconds shortens turnover times, a key KPI for busy ORs. Hybrid workflows-barcode on low-value devices, RFID on high-value sets-let hospitals balance cost and speed while preparing for full automation. FDA guidance on embedding RFID transponders in reusable instruments elongates validation timelines but, once cleared, unlocks life-cycle data unattainable with adhesive labels.

Second-generation ultra-high-frequency (UHF) tags now withstand repeated autoclave cycles and maintain read ranges beyond one meter, reducing mis-reads. The shift signals that the surgical instrument tracking market will eventually converge on RFID as default, even though barcodes remain suitable for budget-sensitive settings. Vendors positioned with dual-technology scanners and cloud-agnostic middleware are best placed to serve this transitional landscape.

The Surgical Instrument Tracking Market Report is Segmented by Technology (Barcodes, RFID), Component (Software, Hardware, Services), End User (Hospitals, Ambulatory Surgical Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 41.98% revenue leadership in 2024, propelled by early-stage UDI enforcement and payer refusal to reimburse for never events. Hospitals routinely cite audit preparedness and litigation avoidance when budgeting for tracking projects. The region also concentrates leading hardware innovators and cloud-EHR vendors, shortening integration cycles. New US state laws requiring digital chain-of-custody logs for OR packs further institutionalize demand.

Europe proceeds steadily under the EU MDR timetable. Although budgets are tighter, the compulsory EUDAMED upload of device identifiers drives a baseline requirement for instrument registration. GDPR restrictions elevate supplier scrutiny on data residency and encryption, pushing vendors to deploy EU data centers and secure APIs that satisfy multi-country deployments. Sustainability rules, including circular-economy targets, incentivize platforms that extend instrument lifespans through data-driven maintenance.

Asia-Pacific is the fastest-growing region at 14.42% CAGR through 2030, energized by expanding health-insurance access, new hospital construction, and a technology-friendly regulatory mood. Singapore's AI-assisted OR pilots, China's smart-hospital grants, and India's public-private drive for medical-device traceability create fertile ground. Suppliers that localize language support and offer subscription financing meet the price-sensitivity of emerging markets without sacrificing feature depth. The surgical instrument tracking market share gains in Asia-Pacific will likely dilute North American dominance as multi-site chains scale deployments across the region.