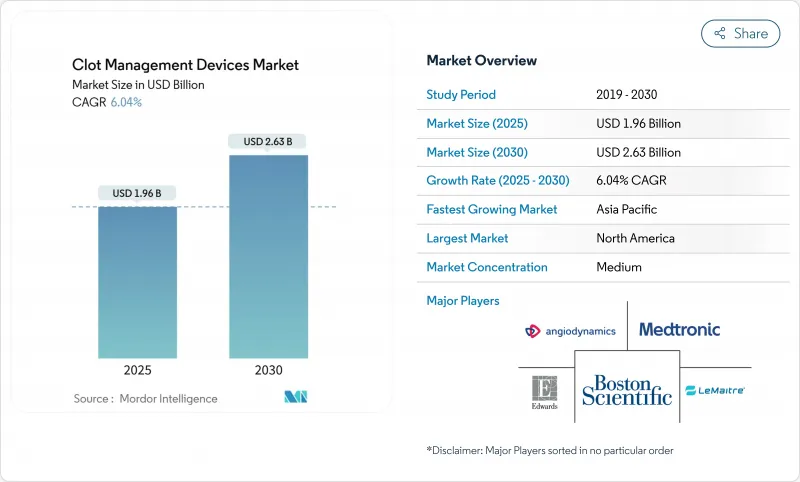

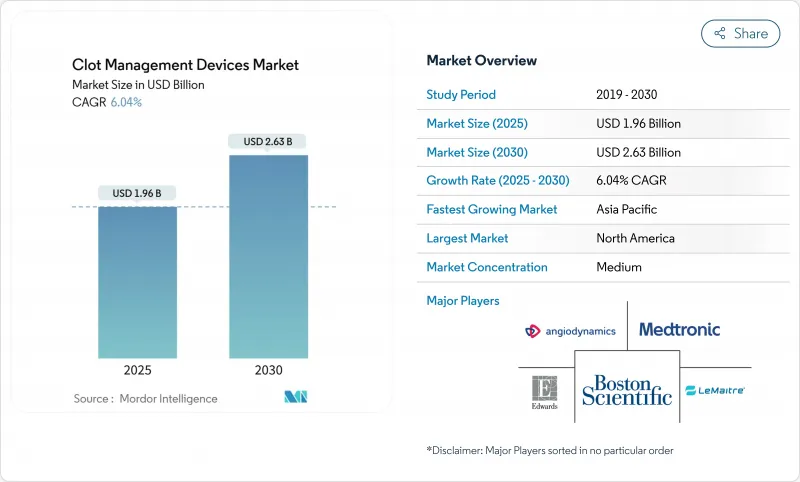

혈전 관리 기기 시장 규모는 2025년에 19억 6,000만 달러로 추정되며 예측 기간(2025-2030년)의 CAGR은 6.04%로, 2030년에는 26억 3,000만 달러에 달할 것으로 예상됩니다.

현재의 확대는 세계적인 심혈관계에 대한 부담 증가, 허혈성 및 혈전성 사건의 꾸준한 증가, 외래 환자의 저침습 혈관 인터벤션에 대한 현저한 축족에 기초합니다. 고령화 사회에 의한 인구통계학적 압력은 비만과 고혈압과 같은 라이프스타일과 관련된 위험요인과 함께 수술 건수를 증가시키는 경향이 있습니다. 첨단 기계 설계, 인공지능 유도 이미지, 고정밀 네비게이션을 통합한 기술 파이프라인은 기술의 성공률과 안전성 프로파일을 향상시켜 수요를 강화하고 있습니다. 동시에 주요 시장에서의 지불자 개혁은 기계적 혈전 제거술의 상환 범위를 확대하고 공급자가 차세대 시스템을 채택하기 위한 재정적 경로를 완화하고 있습니다. 이러한 요인들을 종합하면 혈전 관리 기기 시장은 10년 내내 1자리대 중반의 지속적인 성장이 예상됩니다.

뇌졸중과 심근 경색 증가 추세는 혈전 관리 기기 시장에 가장 강력한 촉임베디드니다. 세계 뇌졸중 환자는 2050년까지 2,143만 명으로 증가할 것으로 예상되고 있으며, 이러한 급증은 안전하고 효과적인 혈전 제거 솔루션에 대한 수요를 높일 것으로 보입니다. 유럽에서는 허혈성 뇌졸중이 이미 뇌졸중 전체의 85%를 차지하고 있으며, 첨단 혈전 제거 기술의 채택을 지원하고 있습니다. 미국 당뇨병 유병률은 2050년까지 16.3%에서 26.8%로 상승할 것으로 예상되며, 일상 진료에서 혈전증의 복잡성을 높이고 있습니다. 저중소득국에서는 미충족 요구가 강조되고 있으며 자원의 제약이 있음에도 불구하고 기존 시스템에 의한 재소통률은 77.93%로 성장을 지속하고, 있습니다. 현재의 의료기기는 강인한 혈전의 두 개 중 하나만 제거할 수 있기 때문에 스탠포드 대학의 milli-spinner와 같은 어려운 폐색에 대해 90% 가까운 효능을 달성하는 플랫폼이 필요합니다.

인구의 노화는 절차의 양과 필요한 기구를 재형성합니다. 허혈성 심장병에 의한 연령표준화 사망률은 부유한 나라에서는 저하되고 있지만, 인구동태의 기세로 환자수는 증가하고 있습니다. 허약, 합병증 및 출혈 위험이 증가하면 의료인은 전신 혈전 용해 요법보다 고도로 제어 가능한 기계 시스템을 선택할 수 있습니다. FLASH 레지스트리 데이터는이 기호를 강화합니다. 중등도 고위험 폐색전증에서 기계적 혈전 제거술은 48시간 후 전체 사인 사망률이 0.3%였습니다. 장비 제조업체는 현재 노인들에게 흔히 볼 수 있는 석회화된 구부러진 혈관을 탐색하기 위해 더 얇은 카테터와 고급 스티어링 도구를 개발하고 있습니다.

규제 당국은 현재 광범위한 안전 데이터 세트를 요구하고, 개발 사이클을 장기화하고, 새로운 시스템의 비용을 증가시키고 있습니다. 유럽의 새로운 의료기기 규제는 시판 후 감시를 강화하지만 노티파이드 바디의 용량을 압박하고 승인을 장기화하고 있습니다. 2025년 초 존슨 엔드 존슨 메디컬 테크의 발리펄스 카테터와 같은 일시적인 판매 중단은 규제 우려가 얼마나 신속하게 상품화를 좌절시키는지를 보여줍니다. 미국에서는 2025년 5월에 FDA가 점탄성 응고 분석기를 특수 관리 클래스 II로 지정하여 보조 기술에 대한 모니터링이 엄격해지고 있습니다. 34개 시설에서 997명의 환자를 대상으로 한 EXCELLENT 레지스트리를 포함한 대규모 연구는 신경혈관 기구의 최소한의 증거가 되었습니다.

기계적 혈전 제거술 및 경피적 혈전 제거술 시스템은 2024년 혈전 관리 기기 시장 점유율의 36.87%를 차지하며, 신경혈관, 관상 동맥 및 말초 영역에서 주력 솔루션으로 지속되었습니다. 그 다용도성과 신속한 기술 혁신이 결합되어, 의료 제공업체의 재고의 중심적인 기둥이 되고 있습니다. 혈전 관리 기기 시장은 더 높은 흡입력, 향상된 혈전 캡처 바구니 및 첫 패스의 성공을 높이는 통합 이미징을 제공하는 플랫폼의 혜택을 계속하고 있습니다. EXCELLENT 레지스트리는 EMBOTRAP 장치의 패스트 패스 재소통률 64.5%, 최종 재소통률 94.5%를 확인하여 보다 광범위한 가이드라인 지지를 뒷받침합니다. 신경혈관 색전술 및 혈전 제거 장치는 뇌졸중 발병 건수 증가와 약물 요법을 능가하는 효능 데이터에 의해 2030년까지 매년 8.59%의 성장이 전망되고 있습니다. 혈전량을 95% 감소시킨 스탠포드 대학의 밀리 스피너와 같은 산학 연계는 스텝 체인지 엔지니어링이 이 분야를 상승 궤도에 싣는 것을 예증하고 있습니다.

두 번째 레이어 카테고리는 틈새 시장이지만 안정된 위치를 유지합니다. 카테터 직접 혈전 용해 장치는 대량의 폐 색전증과 복잡한 심부정맥 혈전증으로 순수한 기계적 치료만으로는 충분하지 않은 경우 필수적입니다. 색전 풍선 카테터는 소구경의 병변 특이적 적응증에 대응하지만, IVC 필터는 안전에 대한 우려와 감시 당국의 감시 중 사용률이 저하되고 있습니다. 그럼에도 불구하고 혈전 관리 기기 시장은 장기적인 합병증 프로파일이 개선되면 신속한 제거를 위해 설계된 가치있는 가격 제거 필터의 기회를 보유하고 있습니다. 제품 전체에서는 AI를 활용한 가이던스 소프트웨어가 계속 인기를 끌고 있으며, 혈전의 특징을 실시간으로 시각화하여 최적의 장치 배치를 기대할 수 있습니다.

북미는 2024년 혈전 관리 기기 시장의 45.84%를 차지해 수익 공헌의 선두를 유지했습니다. 확고한 보험 상환, 뇌졸중 1차 치료 시설의 인증 보급, 외래 시설의 성숙한 네트워크가 다른 지역을 능가하는 사용 수준을 지원합니다. 메드트로닉의 Symplicity Spyral 카테터와 같은 장비에 대한 CMS 패스스루 승인은 채택 파이프라인을 더욱 강화합니다. 그럼에도 불구하고, IVC 필터 분야에서는 법적인 문제로 인해 제조업체 각사가 경계감을 강화하고 있어 필터 설계의 단기적인 혁신이 억제될 가능성도 있습니다.

유럽 점유율은 2위로, 1자리대 중반의 건전한 성장을 기록하고 있습니다. 실시상의 병목은 있는 것, 유럽 MDR의 강화에 의해 추적 가능성와 데이터의 투명성이 향상해, 임상의의 신뢰가 장기적으로 안정할 것이 기대됩니다. 색전방지술과 혈전제거술의 보험상환은 11개 EU 회원국에 따라 다르지만 전반적인 보험상환율은 상승세입니다. 34 시설의 EXCELLENT 레지스트리로 대표되는 고품질의 임상 인프라는 다 시설에서의 검증과 시판 후의 연구를 가속화하여 각국의 보조금 결정에 반영하고 있습니다.

아시아태평양은 2025-2030년 CAGR이 7.04%를 나타낼 것으로 예측되는 급성장 지역입니다. 심혈관 이환율 증가, 보험 보급률의 향상, 대규모 병원의 현대화가 기기의 도입을 촉진합니다. 신흥국에서는 필요와 능력의 격차가 가장 두드러집니다. 중저소득국가의 환경에서는 제한된 자원에도 불구하고 77.93%의 재소통이 입증되었으며, 수기자금이 개선되면 잠재적인 수요가 상당하다는 것을 보여줍니다. 다국적 기업은 국내 판매업체와 협력하여 이동식 트레이닝 랩을 배치하여 임상의의 보급을 가속화하는 한편, 현지 제조업체는 연구개발을 확대하여 가격에 민감한 분야에 대응하고 있습니다. 이러한 요인들로부터 아시아태평양은 향후 5년간 혈전 관리 기기 시장의 수익을 증가시키는 주요 지역 엔진이 될 것입니다.

The Clot Management Devices Market size is estimated at USD 1.96 billion in 2025, and is expected to reach USD 2.63 billion by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

The current expansion rests on the mounting global cardiovascular burden, the steady rise of ischemic and thrombotic events, and a marked pivot toward outpatient, minimally invasive vascular interventions. Demographic pressure from aging societies, coupled with lifestyle-related risk factors such as obesity and hypertension, keeps procedure volumes on an upward trajectory. Technology pipelines that integrate advanced mechanical designs, artificial intelligence-guided imaging, and high-precision navigation reinforce demand by improving procedural success rates and safety profiles. Simultaneously, payer reform in key markets is widening reimbursement coverage for mechanical thrombectomy, easing the financial pathway for providers to adopt next-generation systems. These factors collectively position the clot management devices market for durable mid-single-digit growth through the decade.

Escalating incidences of stroke and myocardial infarction represent the most powerful catalyst for the clot management devices market. Global stroke cases are projected to rise to 21.43 million by 2050, a surge that will swell demand for safe, effective thrombectomy solutions. In Europe, ischemic strokes already account for 85% of all stroke events, sustaining adoption of advanced retriever technology. Metabolic risks compound the challenge: United States diabetes prevalence is forecast to climb from 16.3% to 26.8% by 2050, raising thrombotic complexity in day-to-day practice. Lower-middle-income countries highlight unmet needs, recording 77.93% recanalization rates with existing systems despite resource limitations. Current devices resolve barely one out of two tough clots, opening the door for platforms like Stanford University's milli-spinner, which achieves near-90% efficacy on difficult occlusions.

Population aging reshapes procedure volumes and device requirements. While age-standardized mortality from ischemic heart disease is falling in affluent nations, absolute patient counts are rising due to demographic momentum. Frailty, comorbidities, and elevated bleeding risk push providers toward highly controllable mechanical systems rather than systemic thrombolysis. FLASH registry data reinforce this preference: mechanical thrombectomy in intermediate-high-risk pulmonary embolism delivered 0.3% all-cause mortality at 48 hours. Device makers now engineer slimmer catheters and advanced steering tools to navigate calcified, tortuous vessels commonly found in older adults.

Regulators now demand expansive safety datasets, lengthening development cycles and raising costs for novel systems. Europe's new Medical Device Regulation strengthens post-market surveillance but has strained notified-body capacity, prolonging approvals. Temporary sales pauses-such as Johnson & Johnson MedTech's Varipulse catheter in early 2025 demonstrate how quickly regulatory concerns can derail commercialization. In the United States, the FDA placed viscoelastic coagulation analyzers into Class II with special controls in May 2025, underscoring stricter oversight even for adjunct technologies. Large-scale studies, including the EXCELLENT registry with 997 patients across 34 sites, have become the minimum evidence bar for neurovascular devices.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Mechanical and percutaneous thrombectomy systems commanded 36.87% of the clot management devices market share in 2024 and remain the workhorse solutions across neurovascular, coronary, and peripheral territories. Their versatility, combined with rapid technical iteration, makes them a central pillar of provider inventories. The clot management devices market continues to benefit from platforms offering higher aspiration power, improved clot-capture baskets, and integrated imaging that elevates first-pass success. The EXCELLENT registry confirmed first-pass recanalization of 64.5% and final rates of 94.5% for EMBOTRAP devices, supporting broader guideline endorsement Stroke. Neurovascular embolectomy and thrombectomy devices are set to grow 8.59% annually through 2030, lifted by rising stroke volumes and efficacy data that surpass pharmacologic therapies. Academic-industry partnerships, such as Stanford's milli-spinner achieving 95% clot-volume reduction, exemplify how step-change engineering will keep the segment on an upward trajectory.

Second-tier categories hold niche, yet stable, positions. Catheter-directed thrombolysis devices remain vital for massive pulmonary embolism and complex deep-vein thrombosis when purely mechanical options are insufficient. Embolectomy balloon catheters address small-caliber, lesion-specific indications, while IVC filters experience usage decay amid safety concerns and observer scrutiny. Nevertheless, the clot management devices market retains opportunities for value-priced retrieval filters designed for rapid extraction, provided long-term complication profiles improve. Across products, AI-augmented guidance software continues to gain traction, promising real-time visualization of clot characteristics and optimized device deployment.

The Clot Management Devices Market is Segmented by Product (Embolectomy Balloon Catheters, Catheter-Directed Thrombolysis Devices, Mechanical/Percutaneous Thrombectomy Devices, Inferior Vena Cava (IVC) Filters, and More), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remained the leading revenue contributor, capturing 45.84% of the clot management devices market in 2024. Robust reimbursement, widespread primary-stroke-center certification, and a mature network of ambulatory facilities underpin usage levels that outpace other regions. CMS pass-through approvals for devices such as Medtronic's Symplicity Spyral catheter further strengthen the adoption pipeline. Nevertheless, legal exposures in the IVC filter segment create an undercurrent of caution among manufacturers, potentially curbing near-term innovation in filter design.

Europe delivers the second-largest share and records healthy mid-single-digit expansion. Despite implementation bottlenecks, the enhanced European MDR fosters improved traceability and data transparency, which are expected to stabilize clinician confidence over time. Reimbursement for embolic-protection and thrombectomy varies among the 11 scrutinized EU states, yet overall payment coverage is trending upward. High-quality clinical infrastructures illustrated by the 34-site EXCELLENT registry accelerate multicenter validations and post-market studies that feed national funding decisions.

Asia-Pacific is the fastest-growing region at a projected 7.04% CAGR for 2025-2030. Rising cardiovascular incidence, improving insurance penetration, and large-scale hospital modernization drive equipment uptake. Emerging economies show the starkest need-capacity gap: lower-middle-income settings demonstrated 77.93% recanalization despite limited resources, indicating sizable latent demand once procedural financing improves. Multinationals collaborate with domestic distributors and deploy mobile training labs to speed clinician adoption, while local manufacturers expand R&D to address price-sensitive segments. These factors make Asia-Pacific the primary geographic engine for incremental clot management devices market revenue over the next five years.