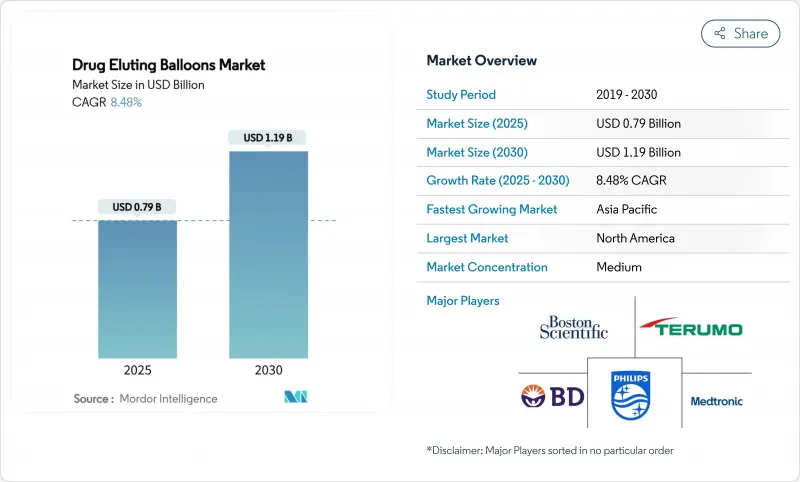

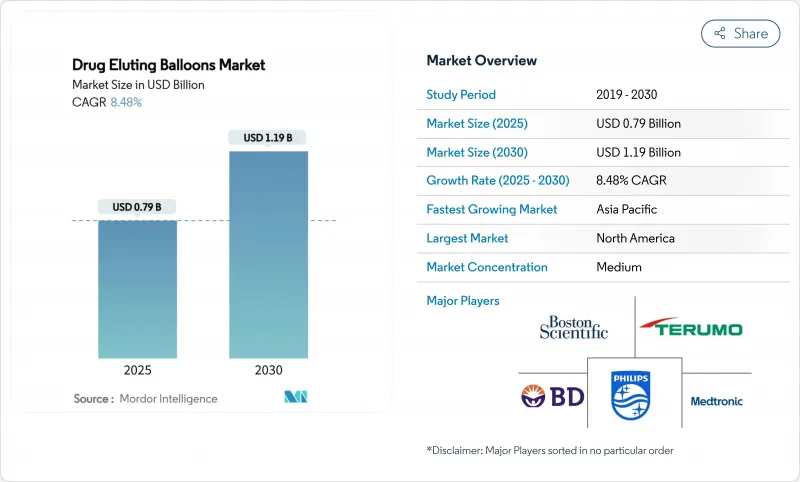

약물 용출 풍선 시장 규모는 2025년에 7억 9,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 8.48%로 성장할 전망이며, 2030년에는 11억 9,000만 달러에 달할 것으로 예측됩니다.

규제 클리어런스의 가속, 상환의 명확화, 심혈관계의 수술 건수 증가에 의해 의사의 기호는 틈새 스텐트 내 재협착 보조제로부터 주류의 혈행 재건술 툴로 계속 옮겨가고 있습니다. 파클리탁셀 제형은 여전히 주류이지만, 시롤리무스 제형은 장기 안전성 데이터의 축적과 함께 기세를 늘리고 있습니다. 외래수술센터(ASC)는 약물 용출 풍선(DEB)에 의해 영구적인 임플란트를 사용하지 않고 당일 퇴원이 가능하며, 가치 기반의 구매의무에 맞추어 매력적인 치료 환경으로 대두해 왔습니다. 관상동맥, 대퇴무와부, 무릎 아래(BTK)의 각 영역에서 임상 증거가 확대되고 있는 이 기술에 의해 약물 용출 풍선 시장은 향후 10년간, 2자리대의 안정적인 수익 확대가 전망됩니다.

허혈성 심장 질환은 여전히 세계에서 연령 표준화 장애의 주요 원인이며, 인구 증가가 사망률 증가를 상쇄하기 때문에 절대 사례 수는 증가의 길을 따라가고 있습니다. 다지 병변이 나이가 많고 합병증이 많은 환자에게 무겁게 걸리는 동안 임상의는 혈관 외상을 최소화하고 약물 요법을 단축할 수 있는 혈액 순환 재건술이 필요합니다. 약물 용출 풍선 시장은 DEB가 금속 비계를 남긴 채 항 증식제를 전달하기 때문에 구부러진 혈관과 석회화가 심한 혈관에서 재 시술의 위험을 줄일 수 있다는 이점이 있습니다. 지금까지 충분한 치료를 받지 못한 BTK 질환은 DEB가 통상의 혈관성형술에 비해 사지의 구제에 효과적임이 입증되어 특히 이익을 올리고 있습니다.

65세 이상의 환자는 경피적 인터벤션을 받는 환자 중에서 가장 빠르게 증가하는 코호트이지만 출혈 위험이 높고 장기 항혈소판 약물 이중 요법에 내성이 없는 환자입니다. DEB는 영구적인 임플란트를 사용하지 않고 국부적인 약물 전달을 가능하게 하고, 노인의 안전성을 선호하는 항혈소판 요법을 보다 단기간에 수행할 수 있게 합니다. 관상동맥 DEB를 지지하는 일본의 2023년 합의는 급속히 고령화가 진행되는 지역이 스텐트를 사용하지 않는 접근법을 어떻게 정당화하고 있는지를 보여줍니다. 노인들은 종종 석회화된 사행한 해부학적 구조를 가지므로 DEB의 얇은 횡단 능력은 이 층에서 약물 용출 풍선 시장의 이용을 더욱 촉진합니다.

약물 용출 풍선의 개발은 임상시험, 규제 당국 신청, 제조 인프라에 대한 많은 투자가 필요하기 때문에 시장 진입 장벽으로 경쟁력이 제한됩니다. 게다가 독물학 연구 및 전용 코팅 장비가 필요하기 때문에 개발 예산이 1억 달러를 초과하여 신규 진입이 제한될 수 있습니다. 레거시 스텐트와의 효능 비교 의무화는 추가 비용을 증가시키고 손익 분기점의 임계값을 늘리고 포트폴리오의 다양화를 지연시킵니다. 중소기업은 대기업에 라이선스를 부여하고 자산 매각을 하는 경우가 많아 지적 재산이 집중되어 약물 용출 풍선 시장에서 가격 경쟁이 완화됩니다. 다운스트림에서는 임상적 요구가 있음에도 불구하고 비용이 많이 드는 가격이 비용에 중점을 둔 시스템으로의 침투를 방해하고 있습니다.

스텐트 유치가 혈관의 움직임이나 외부로부터의 압박에 의한 기계적 과제에 직면하는 대퇴 슬와부 및 슬하 용도에 있어서, 그 임상적 유용성이 확립되어 있는 것을 반영해, 2024년의 말초용 약물 용출 풍선 시장 점유율은 58.86%에 이르렀습니다. SELUTION SFA Japan 시험에서는 12개월 후의 1차 개존률이 87.9%였기 때문에 어려운 해부학적 영역에서 말초용 약물 용출 풍선의 효능이 입증되었습니다. 초기 파클리탁셀 제형이 대퇴 무릎 동맥 병변으로 데뷔하여 임상의에 익숙해져 왔기 때문에 말초 치료에서는 더 많은 도입 실적이 있습니다. 그러나 관상동맥 파이프라인은 de-novo와 소혈관 증거의 확대에 힘입어 상환 장애물이 감소함에 따라 수익 격차가 줄어들 것입니다.

관상 동맥 약물 용출 풍선은 임상 증거의 확대 및 관상 동맥 스텐트 내 재협착 및 소혈관 질환에서의 사용을 정당화하는 최근 FDA 승인에 견인되어 2030년까지 연평균 복합 성장률(CAGR)이 9.92%로 가장 높은 성장 궤도를 나타냅니다. 신장과 비뇨기에 대한 용도를 포함한 다른 제품도 새로운 기회를 보여주었으며, Abbot의 Esprit BTK 시스템은 2024년 4월에 승인되어 특수한 해부학적 용도에 대한 규제 당국의 지원을 입증했습니다.

시롤리무스 기반 제제로의 전환은 2030년까지 연평균 복합 성장률(CAGR) 9.68%로 가속화되어 임상의가 안전성 프로파일을 개선하고 치료 영역을 넓힌 대체 제제를 요구하는 가운데, 2024년에는 파클리탁셀의 79.12% 시장 점유율에 과제합니다. 코디스가 MedAlliance를 11억 달러로 인수함에 따라 시롤리무스를 지속적으로 방출하는 독자적인 마이크로 리저버 약물 전달을 활용한 SELUTION SLR 기술이 가져왔습니다.

이중 병용 제제와 신규 약제 제제는 단독 플랫폼의 한계를 해결할 수 있는 실험적 접근이지만 임상 증거는 여전히 제한되어 있습니다. 파클리탁셀은 확립된 임상 데이터와 제조 규모에 따라 우위를 유지하고 있지만, FDA 지침이 과다 사망 위험을 지우고 있음에도 불구하고, 최근 사망 신호와 관련된 안전에 대한 우려가 의사의 선호에 계속 영향을 미치고 있습니다.

북미는 FDA의 획기적인 관상동맥 DEB 승인과 CMS의 패스스루 지불 창설을 통해 쌍둥이 도입 장벽이 해소됨에 따라 2024년 매출의 42.56%를 차지했습니다. 선도적인 제조업체의 존재, 광범위한 테스트 인프라 및 확립된 ASC 네트워크는 꾸준하지만 완만한 미래 성장을 지원합니다.

유럽에서는 임상 노하우가 확립되어 있는 것, 파클리탁셀의 서베이런스가 엄격해지고 있어, 시롤리무스 플랫폼의 규모가 확대될 때까지는 치료 건수가 늘어나 고민할 가능성이 있습니다. 독일과 이탈리아는 여전히 기술의 선두 주자이며 남유럽 예산 중심 시스템은 DEB의 비용 효과를 최신 스텐트와 비교하고 있습니다.

인구 동태의 고령화 및 카테터 실험실의 급속한 확대가 교차하는 가운데 아시아태평양의 CAGR은 10.42%로 가장 높을 것으로 예측됩니다. 관상 동맥에서의 사용 확대를 뒷받침하는 일본의 국가적 합의, 중국의 신속한 승인, 인도의 중간층 수요 증가는 약물 용출 풍선 시장의 비옥한 토양을 형성합니다. MicroPort와 같은 지역 제조업체들은 국내 공급을 강화하고 보급을 가속화하는 가격 경쟁을 자극합니다. 중동 및 아프리카와 남미는 모두 기준선은 작지만 각각 걸프 협력회의 국가와 브라질에서 선택적인 힘을 보이고 있습니다. 인프라 업그레이드와 민간 심장혈관 센터가 접근을 넓히지만, 상환 지연 및 환율 변동은 당면 궤도를 완만하게 만듭니다.

The Drug Eluting Balloons Market size is estimated at USD 0.79 billion in 2025, and is expected to reach USD 1.19 billion by 2030, at a CAGR of 8.48% during the forecast period (2025-2030).

Accelerated regulatory clearances, expanding reimbursement clarity, and rising cardiovascular procedure volumes continue to shift physician preference from niche in-stent restenosis adjuncts toward mainstream revascularization tools. Paclitaxel formulations still dominate volumes, yet sirolimus platforms gain momentum as long-term safety data accumulate. Ambulatory surgery centers (ASCs) emerge as attractive care settings because drug-eluting balloons (DEBs) allow same-day discharge without permanent implants, aligning with value-based purchasing mandates. The technology's expanding clinical evidence across coronary, femoropopliteal, and below-the-knee (BTK) territories positions the drug eluting balloon market for steady double-digit revenue upside through the decade.

Ischemic heart disease remains the leading source of age-standardized disability worldwide, and absolute case volumes keep rising because population growth offsets mortality gains. As multi-vessel disease burdens older, more-comorbid patients, clinicians require revascularization modalities that minimize vessel trauma and shorten pharmacotherapy. Drug eluting balloon market adoption benefits because DEBs deliver antiproliferative drugs without leaving metal scaffolds, reducing repeat-intervention risk in tortuous or heavily calcified segments. BTK disease, historically underserved, sees particular gains as DEBs demonstrate limb-salvage advantages over plain angioplasty.

Patients >=65 years now represent the fastest-growing cohort undergoing percutaneous interventions, yet they carry heightened bleeding risk and intolerance to prolonged dual antiplatelet regimens. DEBs allow local drug delivery without permanent implants, enabling shorter antiplatelet courses that align with geriatric safety priorities. Japan's 2023 consensus endorsing coronary DEBs illustrates how rapidly ageing regions legitimize stent-free approaches. Because seniors often present calcified and tortuous anatomy, the device's low-profile crossing ability further drives drug eluting balloon market utilisation in this demographic.

Drug-eluting balloon development requires substantial investment in clinical trials, regulatory submissions, and manufacturing infrastructure that creates barriers to market entry and limits competitive intensity. It further requires toxicology work and purpose-built coating facilities that can push development budgets beyond USD 100 million, limiting new entrants. Comparative-effectiveness mandates versus legacy stents add further cost, elevating break-even thresholds and slowing portfolio diversification. Smaller firms often license or sell assets to majors, concentrating intellectual property and tempering price competition within the drug-eluting balloon market. Downstream, premium prices impede penetration in cost-sensitive systems despite clinical need.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Peripheral drug-eluting balloons command 58.86% market share in 2024, reflecting their established clinical utility in femoropopliteal and below-the-knee applications where stent placement faces mechanical challenges from vessel movement and external compression. The SELUTION SFA Japan trial's demonstration of 87.9% primary patency at 12 months reinforces peripheral drug-coated balloon efficacy in challenging anatomical territories. Peripheral procedures retain a larger installed base because early paclitaxel devices debuted in femoropopliteal lesions, creating clinician familiarity. Yet the coronary pipeline, supported by expanded de-novo and small-vessel evidence, should narrow the revenue gap as reimbursement hurdles fall.

Coronary drug-eluting balloons show the highest growth trajectory at 9.92% CAGR through 2030, driven by expanding clinical evidence and recent FDA approvals that legitimize their use in coronary in-stent restenosis and small vessel disease. Other products including renal and urology applications represent emerging opportunities, with Abbott's Esprit BTK system approval in April 2024 demonstrating regulatory support for specialized anatomical applications.

The transition toward sirolimus-based formulations accelerates at 9.68% CAGR through 2030, challenging paclitaxel's 79.12% market share in 2024 as clinicians seek alternatives with improved safety profiles and broader therapeutic windows. Cordis's USD 1.1 billion acquisition of MedAlliance brought SELUTION SLR technology, utilizing proprietary MicroReservoir drug delivery for sustained sirolimus release.

Dual-drug and novel agent formulations represent experimental approaches that may address limitations of single-agent platforms, though clinical evidence remains limited. Paclitaxel maintains dominance through established clinical data and manufacturing scale, yet safety concerns following recent mortality signals continue influencing physician preferences despite FDA guidance clearing excess mortality risk.

The Drug Eluting Balloons Market Report is Segmented by Product (Coronary Drug-Eluting Balloon, Peripheral Drug-Eluting Balloon, Other Products), Drug Type (Paclitaxel-Based Balloons, and More), Coating Technology (FreePac, Transpac, and More), Lesion Type (In-Stent Restenosis, and More), End User (Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 42.56% of 2024 revenue following the FDA's landmark coronary DEB approval and CMS pass-through payment creation, which together eliminated twin adoption barriers. The presence of leading manufacturers, extensive trial infrastructure, and established ASC networks underpin steady but moderate future growth.

Europe maintains entrenched clinical know-how yet faces stricter paclitaxel surveillance that may temper volumes until sirolimus platforms scale. Germany and Italy remain procedural leaders, while budget-conscious systems in Southern Europe weigh DEB cost-utility versus modern stents.

Asia-Pacific is projected to post the highest 10.42% CAGR as ageing demographics intersect with rapid cath-lab expansion. Japan's national consensus endorsing broader coronary use, China's expedited approvals, and India's rising middle-class demand together create fertile ground for the drug eluting balloon market. Regional manufacturers such as MicroPort bolster domestic supply and stimulate price competition that accelerates penetration. Middle East & Africa and South America together deliver smaller baselines but show selective strength in Gulf Cooperation Council states and Brazil, respectively. Infrastructure upgrades and private-sector cardiovascular centres widen access, yet reimbursement lags and currency volatility moderate the near-term trajectory.