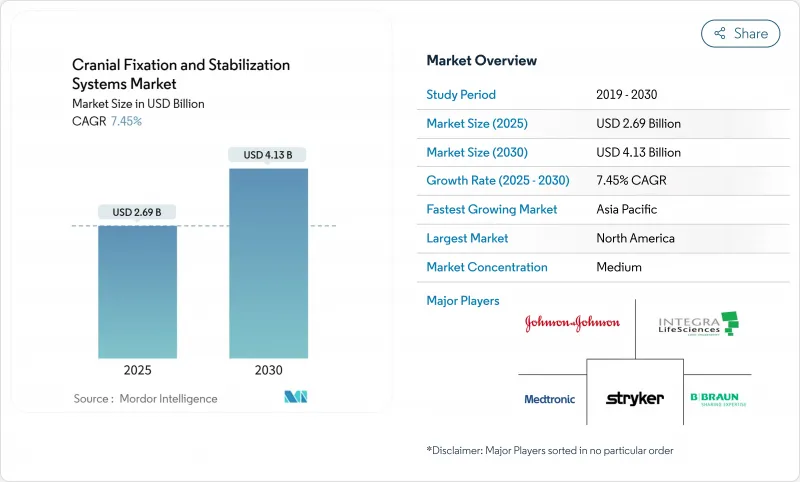

두개 고정 및 안정화 시스템 시장은 2025년에 26억 9,000만 달러로 추정되고, CAGR 7.45%로 성장할 전망이며, 2030년에는 41억 3,000만 달러에 이를 것으로 예측됩니다.

인구 동태의 고령화, 외상성 뇌손상의 꾸준한 증가, 저침습 뇌신경외과 수술의 추진이 이 궤도를 지원하고 있습니다. 3차원 프린팅은 현재 수술 시간을 단축하는 환자 전용 임플란트를 제공하며, 복합 현실 내비게이션은 궤도 계획을 2.1배로 단축하고 mm 이하의 정확도를 유지합니다. 외래수술센터(ASC)는 미국 내 11,555개 시설이 외래 뇌신경 수술에 중점을 두고 있기 때문에 수요 증가에 박차를 가하고 있습니다. ASC의 워크플로우에 매치한 경량으로 일회용의 헤드 레스트 킷이 인기를 모으고 있습니다. 한편, 티타늄 공급 불안정과 수술 후 MRI 아티팩트가 금속 임플란트에 대한 열의를 깎아 재수술과 화상 제한을 회피하는 재흡수성 폴리머 및 마그네슘 합금으로의 길을 열고 있습니다.

세계의 외상성 뇌손상(TBI) 입원 환자 수는 미국만으로도 매년 23만 5,000명 가까이에 오르며, 병원을 감압 두개 절제술의 능력 확대로 추진하고 있습니다. 선진국 시장의 25.2%에 비해 신흥국 시장에서는 38.0%라는 사망률의 격차가 수술 체류를 낳고 있습니다. 3개월 이내의 조기 두개 성형술은 수술 시간 및 출혈량을 줄이고, 단계적 개입을 허용하는 내구성 있는 고정판에 대한 수요를 강화하고 있습니다. 메디케어의 수급자는 두개 수술로 평균 9.6일 입원하고 합병증에 의한 경제적 부담의 크기를 이야기하고 있습니다.

생분해성 플레이트는 재수술을 피할 수 있습니다. PLLA-마그네슘 복합재료는 현재 190MPa의 굽힘 강도와 150kJ/m2의 내충격성을 달성하고 있습니다. 나노 MgO 첨가제는 산성 제품별로 완충하여 골아세포의 증식을 촉진합니다. 폴리유산으로 코팅된 ZK60 마그네슘 합금은 300MPa 이상의 인장 강도를 유지하며 12주 동안 완전히 흡수되지만 급격한 분해는 창부의 박리를 유발합니다. 몰리브덴 시스템은 두개골의 성장에 영향을 미치지 않고 생체 적합성을 나타내므로 소아의 두개 결합 골증의 수리가 특히 유익합니다. 규제 장애물은 여전히 남아 있지만, 장기적인 헬스케어를 절약하고 환자의 편안함이 이러한 기세를 지원합니다.

뇌신경 외과 수술의 평균 입원 비용은 3만 746달러로, 공적 지불자에게 부담을 주고 있는 한편, 고령자의 원내 사망률은 10.9%에 달하고, 디바이스의 가치에 대한 감시의 눈을 강하게 하고 있습니다. 값 비싼 임플란트는 접근 격차를 확장하고, 상환 코드는 종종 기술에 뒤처지며, 병원은 비용 흡수를 강요합니다. 훈련, 고급 이미지 처리, 더 긴 수술 시간이 추가 비용을 쌓습니다. 신흥국은 전통적인 플레이트 또는 차세대 폴리머 시스템의 엄격한 선택에 직면하고 있습니다. 제조업체는 네비게이션 하드웨어와 소모품을 번들하여 위험 분담 계약을 체결함으로써 대응하고 있습니다.

두개 고정 시스템은 티타늄 플레이트, 스크류, 메쉬의 강도로 2024년 두개 고정 및 안정화 시스템 시장의 58.56%를 유지했습니다. 혁신적인 3핀 두개골 클램프는 힘을 보다 균등하게 분산시켜 관통 비대칭을 감소시킵니다. 테이블 마운트 프레임은 광학 트래커와 통합되어 외과 의사는 2.1배 빠르게 궤도를 결정할 수 있습니다. 두개 고정 및 안정화 시스템 시장 규모는 병원이 기존 재고를 갱신함에 따라 2030년까지 꾸준히 확대될 것으로 예측됩니다.

모듈형 말굽 헤드 레스트 및 일회용 ASC 키트를 포함한 안정화 시스템의 CAGR은 8.34%입니다. 복합 현실 오버레이는 내시경으로 절제하는 데 필수적인 머리 방향을 하위 mm 단위로 확인할 수 있습니다. ASC는 재처리가 필요 없는 단일 사용 프레임을 평가하여 회전 속도를 향상시킵니다. 전동 환자 테이블과의 통합은 위치 조정을 자동화하여 수요를 더욱 높여줍니다.

비재흡수성 티타늄은 2024년 두개 고정 및 안정화 시스템 시장 점유율의 72.35%를 차지했습니다. MRI 아티팩트의 우려와 190.106에 이르는 티타늄 가격 지수는 조달을 복잡하게 만듭니다. 티타늄 하드웨어의 두개 고정 및 안정화 시스템 시장 규모는 성장하지만 병원이 하이브리드 옵션으로 헤지하고 있기 때문에 성장률이 둔화되고 있습니다.

재흡수성 폴리머는 나노 MgO로 완충된 PLLA/PLGA 블렌드에 밀려 CAGR 8.95%로 상승했습니다. 소아용 임플란트는 두개골의 확대와 함께 임플란트가 용해되기 때문에 소아용 임플란트가 채용을 선도하고 있습니다. 마그네슘 합금은 유망하지만 염증성 후유증을 피하기 위해 부식을 제어해야 합니다. PEEK는 방사선 투과성이 중요한 경우 틈새 용도를 발견하지만 복잡한 재건술 외에는 비용이 많이 드는 것이 보급을 억제합니다.

북미는 첨단 수술 능력 및 지원 상환 환경으로 2024년 두개 고정 및 안정화 시스템 시장의 41.23%를 차지했습니다. 두개골의 평균 입원일수는 9.6일로 ICU의 이용이 눈에 띄고 합병증을 줄이는 장치의 경제적 가치가 부각되고 있습니다. ASC 붐은 외래 환자 수요를 유발하고 FDA 지침이 개별화된 임플란트에 대한 명확한 지침을 제공합니다.

아시아태평양의 CAGR은 11.07%로 세계에서 가장 빠릅니다. 중국과 인도의 헬스케어 투자 증가 및 노동력 스킬 업으로 의료 액세스가 확대되었습니다. 인도네시아의 뇌신경외과의 수는 인구비에서는 아직 적지만, 국경을 넘은 훈련의 대처에 의해 격차가 축소되고 있습니다. 베트남의 쵸레이 병원은 현재 연간 1,000건의 개두 수술을 실시하고 있으며, 이 지역이 외상 전용 사례 수에서 선택적 수술로 이동하고 있음을 보여줍니다.

유럽은 성숙하면서도 기회가 풍부한 시장입니다. 독일, 영국, 프랑스는 연구개발 활동의 중심이며, 주변 국가들은 수술실의 현대화를 추진하고 있습니다. 의료기기 규제에 의한 규제의 수렴은 승인 경로를 조화시켜, 국경을 넘은 기기 도입을 원활하게 합니다. 고령화로 골다공증 뼈에 최적화된 임플란트에 대한 수요가 증가하고 있습니다.

The cranial fixation and stabilization systems market stands at USD 2.69 billion in 2025 and is forecast to climb to USD 4.13 billion by 2030, reflecting a 7.45% CAGR.

Demographic aging, the steady rise in traumatic brain injuries, and the push toward minimally invasive neurosurgery underpin this trajectory. Three-dimensional printing now supplies patient-specific implants that reduce theater time, while mixed-reality navigation shortens trajectory planning by 2.1 times and preserves sub-millimetric accuracy. Ambulatory surgical centers (ASCs) fuel incremental demand as 11,555 facilities in the United States pivot toward outpatient neurosurgery. Lightweight, single-use headrest kits matched to ASC workflows are gaining traction. Meanwhile, titanium supply volatility and post-operative MRI artifacts temper enthusiasm for metal implants, opening a lane for resorbable polymers and magnesium alloys that sidestep revision surgery and imaging limitations.

Global traumatic brain injury (TBI) admissions hover near 235,000 in the United States alone each year, pushing hospitals to expand decompressive craniectomy capacity. Mortality disparities-38.0% in developing regions versus 25.2% in developed markets-swell the surgical backlog. Early cranioplasty within three months cuts operative time and blood loss, reinforcing demand for durable fixation plates that tolerate staged interventions. Medicare beneficiaries average 9.6-day stays for cranial surgery, underscoring the economic burden of complications.

Biodegradable plates avert second operations, a critical advantage when payers tighten reimbursement. PLLA-magnesium composites now achieve 190 MPa bending strength with 150 kJ/m2 impact resistance. Nano-MgO additives buffer acidic by-products, promoting osteoblast proliferation. ZK60 magnesium alloy, coated in poly-l-lactic acid, preserves >300 MPa tensile strength and fully resorbs in 12 weeks, though swift degradation can trigger wound dehiscence. Pediatric craniosynostosis repair particularly benefits, as molybdenum systems show biocompatibility without impacting skull growth. Regulatory hurdles remain, yet long-term healthcare savings and patient comfort sustain momentum.

Average inpatient charges of USD 30,746 for cranial surgery strain public payers, while in-hospital mortality of 10.9% among seniors amplifies scrutiny of device value. Premium implants widen access gaps; reimbursement codes often lag technology, forcing hospitals to absorb costs. Training, advanced imaging, and longer theater times add layers of expense. Emerging economies face stark choices between legacy plates and next-generation polymer systems. Manufacturers counter by bundling navigation hardware and disposables under risk-sharing contracts.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cranial fixation systems retained 58.56% of the cranial fixation and stabilization systems market in 2024 on the strength of titanium plates, screws, and mesh. Innovative three-pin skull clamps now distribute force more evenly, reducing penetration asymmetries. Table-mounted frames integrate with optical trackers so surgeons finalize trajectories 2.1 times faster. The cranial fixation and stabilization systems market size for fixation hardware is projected to advance steadily through 2030 as hospitals refresh legacy inventories.

Stabilization systems, including modular horseshoe headrests and disposable ASC kits, post an 8.34% CAGR. Mixed-reality overlays allow sub-millimetric verification of head orientation, crucial for endoscopic resections. ASCs value single-use frames that bypass reprocessing, improving turnover. Integration with motorized patient tables further boosts demand by automating positional adjustments.

Non-resorbable titanium commanded 72.35% of the cranial fixation and stabilization systems market share in 2024. MRI artifact concerns and titanium price indices hitting 190.106 complicate procurement. The cranial fixation and stabilization systems market size for titanium hardware grows but at a slower clip as hospitals hedge with hybrid options.

Resorbable polymers climb at 8.95% CAGR, propelled by PLLA/PLGA blends buffered with nano-MgO. Pediatric units lead adoption because implants dissolve as skulls expand. Magnesium alloys show promise yet require controlled corrosion to avoid inflammatory sequelae. PEEK finds niche use where radiolucency is critical, though premium cost tempers uptake outside complex reconstructions.

The Cranial Fixation and Stabilization Systems Market is Segmented by Product Type (Cranial Fixation System, Cranial Stabilization Systems), Material Type (Resorbable Fixation Systems, Nonresorbable Fixation Systems and More), and by End User (Hospitals, and More), by Indication (Traumatic Brain Injury, and More), Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 41.23% of the cranial fixation and stabilization systems market in 2024 owing to advanced surgical capacity and a supportive reimbursement climate. Average cranial admissions span 9.6 days with notable ICU utilization, highlighting economic value in devices that reduce complications. The ASC boom channels outpatient demand, while FDA guidance gives clarity for personalized implants.

Asia-Pacific posts an 11.07% CAGR, the fastest worldwide. Rising healthcare investment in China and India, coupled with workforce upskilling, widens access. Indonesia's neurosurgeon count remains low relative to population, but cross-border training initiatives are narrowing gaps. Vietnam's Cho Ray Hospital now conducts 1,000 craniotomies annually, marking the region's shift from trauma-only caseloads to elective procedures.

Europe reflects a mature yet opportunity-rich market. Germany, the United Kingdom, and France anchor R&D activity, while peripheral nations modernize theater suites. Regulatory convergence through the Medical Device Regulation harmonizes approval pathways, thus smoothing cross-border device adoption. Aging populations magnify demand for implants optimized for osteoporotic bone