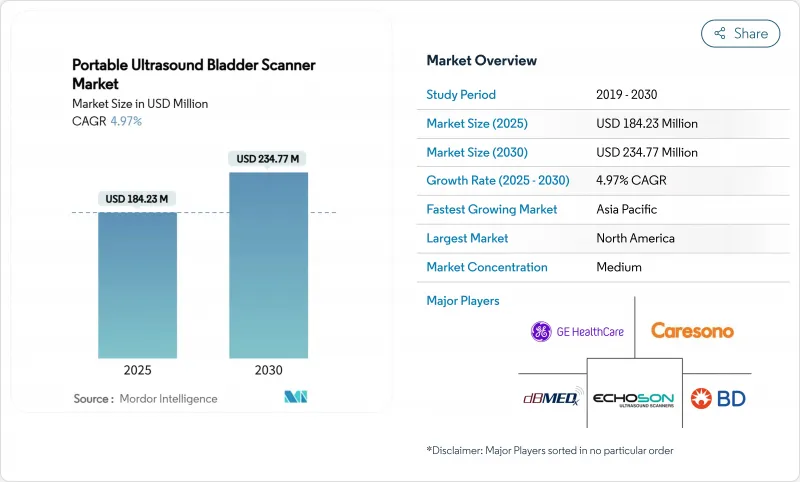

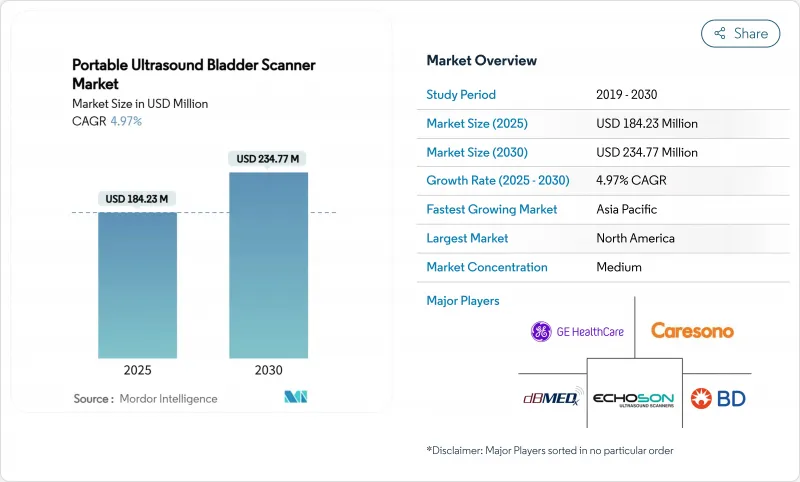

휴대용 초음파 방광 스캐너 시장 규모는 2025년에 1억 8,423만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 4.97%로, 2030년에는 2억 3,477만 달러에 달할 것으로 예상됩니다.

이 성장은 기술이 성숙하고 경쟁이 심화해도 계속되고 있습니다. 인구의 고령화, 초음파 구성 요소의 소형화, 유리한 상환 갱신이 수요를 유지하는 한편, 규제의 복잡성과 오퍼레이터 트레이닝의 격차가 채용을 억제하고 있습니다. 시장 리더는 AI를 활용한 자동화, 포트폴리오 확대, 장기 케어, 재택 케어, 외래 환경을 위한 표적 솔루션으로 대응하고 있습니다. 이러한 시장 성장 촉진요인 이외에, 시장은 보다 선명한 세분화과 지리적 확대를 목표로 하고 있습니다. 경쟁에는 세계적인 이미지 처리 대기업과 민첩한 신흥 기업이 있어, 양 그룹 모두 AI를 통합해 정밀도의 향상과 스캔 시간의 단축을 도모하고 있습니다. 가장 큰 장벽은 훈련된 사용자의 지속적인 부족이지만 이미지 캡처 및 해석을 자동화하는 AI 도구에 의해 부분적으로 상쇄됩니다.

65세 이상의 노인 수는 전례 없는 속도로 증가하고 있으며 전립선 비대증과 관련 비뇨기계 합병증의 발생률이 높아지고 있습니다. Scientific Reports는 2024년 세계에서 1억 1,250만 명의 전립선 비대증 환자가 발생했으며, 그 유병률이 가장 높은 것은 동유럽, 중앙 라틴아메리카, 안데스 라틴아메리카라고 지적했습니다. 게다가 메디케어의 데이터에 따르면, 수급자의 11.2%가 요실금이며, 숙련된 간병 시설에서는 20.6%로 상승합니다. 이러한 인구통계는 일상적인 방광 용적 모니터를 증가시켜 휴대형 초음파 방광 스캐너 시장에 임상적·경제적으로 설득력 있는 사례가 됩니다.

임상 프로토콜은 현재 감염의 감소, 환자의 편안함, 신속한 의사 결정을 선호합니다. 2024년 급성 뇌졸중 연구에서는 휴대형 방광 초음파를 채용한 후 요로 결석이 4.0%로 감소하고 동시에 입원 기간도 단축되었습니다. 메디케어의 2025년 의사 진료 보상 명세서에는 원격 진단 도구를 장려하는 원격 의료 및 간병인 교육 코드가 도입되었습니다. 이러한 개혁은 재택치료 및 지역 사회에서의 도입 촉진을 직접적으로 지원하는 것입니다.

1차 케어 및 장기 케어 시설에서는 공식적인 초음파 검사 훈련이 아직 제한되어 있습니다. 자동 방광 윤곽 드로잉과 같은 AI 기능은 학습 곡선을 단축시킬 것이며, 이러한 도구는 여전히 통합 비용과 사용자의 신뢰가 필요합니다. 소규모 의료기관에서는 진료보상이 즉시 확정되지 않는 한 투자를 주저합니다.

휴대용 초음파 방광 스캐너 시장에서 3D 스캐너는 2024년 매출의 62.43%를 차지했습니다. 그 부피 정확도는 카테터 오류 위험이 높은 탈장 사례를 포함한 복잡한 해부학적 구조에 적합합니다. 그럼에도 불구하고 알고리즘 업그레이드로 정밀도가 엄격해지기 때문에 2D 스캐너는 2025-2030년에 CAGR 8.78%를 나타낼 전망입니다. 메모리 효율성이 뛰어난 세분화은 보다 저가의 프로세서에서 실행되고, 평균 판매 가격을 밀어내어 대응 가능한 수요를 확대하고 있습니다. 조달 팀은 절대 정확도보다 가격 성능 비율을 비교하고 자원에 제약이 있는 환경에 2D를 침투시킬 수 있습니다. 따라서 휴대용 초음파 방광 스캐너 시장 규모는 3D보다 2D가 급속히 확대될 것으로 예상되지만, 후자는 여전히 급성도가 높은 병동에서 사용되는 경우가 많습니다.

핸드헬드형 폼 팩터의 진보가 2D의 기회를 더욱 넓혀줍니다. 통합된 AI는 직교 뷰의 촬영을 운영자에 의존하지 않게 하고, Wi-Fi 연결은 기록 전송을 효율화합니다. 선도적인 3D 공급업체는 소프트웨어 라이선스 및 보증 기간 연장을 번들로 지원합니다. 그 결과, 경쟁은 모든 스캐너 유형의 총 소유 비용을 개선하고 신흥 국가 전반에 걸쳐 2자리 수의 출하량 증가를 유지합니다.

북미는 휴대용 초음파 방광 스캐너 시장의 2024년 매출에서 39.81%를 차지했습니다. FDA 하락으로 시장 출시 시간이 단축되고 포트폴리오 업데이트가 신속하게 이루어졌습니다. 라틴아메리카에서는 멕시코 사립 병원이 수요의 선두에 서 있습니다.

유럽은 2위입니다. 독일은 유치 카테터의 보급률이 13.4%에 달하는 복수 시설의 간병 시설에서의 채용이 원동력이 되어, 가장 많은 개수를 기록하고 있습니다. 영국과 프랑스가 이에 이어, 원내 감염 삭감을 목표로 하는 국가의 보건 위생상의 우선사항을 활용하고 있습니다. 남유럽에서는 고령화에 의해 공적 헬스케어 예산이 늘어나고, 비용 효율적인 방광 모니터링에 대한 관심이 높아지고 있습니다.

아시아태평양은 CAGR 9.69%로 가장 빠르게 성장합니다. 중국은 1차 클리닉에 대한 국가 투자와 세계 최대 노인 집단으로부터 이익을 얻고 있습니다. 국내 벤더는 저렴한 스캐너를 공급하고 있지만, 다국적 기업이 고급 병원용을 유지하고 있습니다. 일본의 초고령화 사회는 1인당 이용률을 높이고 인도의 중산계급은 도시에서의 보급을 촉진합니다. 삼성 메디슨의 AI 푸시와 같은 전략적인수는 이 지역의 휴대용 초음파 방광 스캐너 시장을 더욱 자극합니다.

중동 및 아프리카와 남미는 꾸준하지만 불균일한 진전을 보이고 있습니다. GCC 국가의 병원 근대화에는 방광 스캐너 배치가 포함되어 있지만 농촌 지역에서의 접근이 지연됩니다. 남미에서는 브라질과 아르헨티나가 도시의 민간 네트워크 내에서 압도적인 매출을 자랑합니다. 따라서 도시와 농촌의 격차가 지역별 마케팅 전술과 애프터세일즈의 발자취를 형성하고 있습니다.

The Portable Ultrasound Bladder Scanner Market size is estimated at USD 184.23 million in 2025, and is expected to reach USD 234.77 million by 2030, at a CAGR of 4.97% during the forecast period (2025-2030).

This growth continues even as the technology matures and competition intensifies. Aging populations, miniaturization of ultrasound components and favorable reimbursement updates sustain demand, while regulatory complexity and operator-training gaps temper adoption. Market leaders are responding with AI-enabled automation, portfolio expansion and targeted solutions for long-term care, home-care and ambulatory environments. Alongside these drivers, the market is witnessing sharper segmentation dynamics and geographic expansion. Competition features global imaging giants and agile start-ups; both groups are embedding AI to improve accuracy and cut scan time. The single biggest barrier is the persistent shortage of trained users, partly offset by AI tools that automate image capture and interpretation.

The number of people aged 65 years and older is climbing at an unprecedented pace, escalating incidence of benign prostatic hyperplasia and related urinary complications. Scientific Reports highlighted 112.5 million BPH cases globally in 2024, with highest prevalence in Eastern Europe, Central Latin America and Andean Latin America. Medicare data further indicate urinary incontinence in 11.2% of beneficiaries, rising to 20.6% in skilled nursing facilities. These demographics elevate routine bladder-volume monitoring, making a compelling clinical and economic case for the portable ultrasound bladder scanner market.

Clinical protocols now prioritize infection reduction, patient comfort and rapid decision-making. A 2024 acute-stroke study showed UTIs falling to 4.0% after portable bladder ultrasound adoption, while length-of-stay dropped simultaneously. Medicare's 2025 Physician Fee Schedule introduced telehealth and caregiver-training codes that encourage remote diagnosis tools. These reforms directly support accelerated uptake in home-care and community settings.

Formal ultrasound training remains limited across primary-care and long-term care facilities. Although AI features such as automated bladder outlining cut learning curves, these tools still require integration spending and user confidence. Smaller providers hesitate to invest without immediate reimbursement certainty.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

3D scanners held 62.43% of 2024 revenue within the portable ultrasound bladder scanner market. Their volumetric precision suits complex anatomy, including prolapse cases where catheterization error risk is high. Nonetheless, 2D scanners are scaling at 8.78% CAGR during 2025-2030 as algorithmic upgrades tighten accuracy bands. Memory-efficient segmentation now runs on lower-cost processors, driving down average selling prices and widening addressable demand. Procurement teams increasingly compare price-performance ratios rather than absolute accuracy, allowing 2D to penetrate resource-constrained settings. The portable ultrasound bladder scanner market size for 2D systems is therefore projected to expand faster than for 3D, though the latter retains hospital preference for high-acuity wards.

Advances in handheld form factors compound the 2D opportunity. Integrated AI makes capturing orthogonal views less operator-dependent, while Wi-Fi connectivity streamlines record transfer. Leading 3D vendors respond by bundling software licenses and extended warranties. Resulting competition improves total cost of ownership for all scanner types, sustaining double-digit shipment growth across emerging economies.

The Portable Ultrasound Bladder Scanner Market is Segmented by Type (2D Portable Ultrasound Bladder Scanner, 3D Portable Ultrasound Bladder Scanner), Device Type (Handheld Portable, Mobile-Cart, Bench-Top), End-User (Hospitals & Clinics, Diagnostic Imaging Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America leads with 39.81% 2024 revenue in the portable ultrasound bladder scanner market, powered by Medicare beneficiaries' high urinary-incontinence prevalence and supportive device coding. FDA down-classification has shortened time-to-market, fostering quicker portfolio refreshes. Canada trails the United States yet follows similar adoption trajectories, whereas Mexico's private hospitals spearhead demand within Latin America.

Europe ranks second. Germany posts the highest unit volumes, driven by multi-facility nursing home adoption where indwelling catheter prevalence reached 13.4%. The United Kingdom and France follow, leveraging national health priorities that target hospital-acquired infection reduction. Southern Europe accelerates as aging demographics stretch public healthcare budgets, elevating interest in cost-effective bladder monitoring.

Asia-Pacific delivers the swiftest growth at 9.69% CAGR. China benefits from state investments in primary clinics and the world's largest elderly cohort. Domestic vendors supply affordable scanners, but multinationals retain premium hospital tiers. Japan's super-aged society drives high per-capita utilization, while India's growing middle class catalyzes urban uptake. Strategic acquisitions, such as Samsung Medison's AI push, further stimulate the regional portable ultrasound bladder scanner market.

Middle East & Africa and South America show steady but uneven progress. GCC states' hospital modernizations include bladder-scanner deployments, yet rural access lags. Brazil and Argentina dominate South American sales within private urban networks. Urban-rural divides therefore shape localized marketing tactics and after-sales footprints.