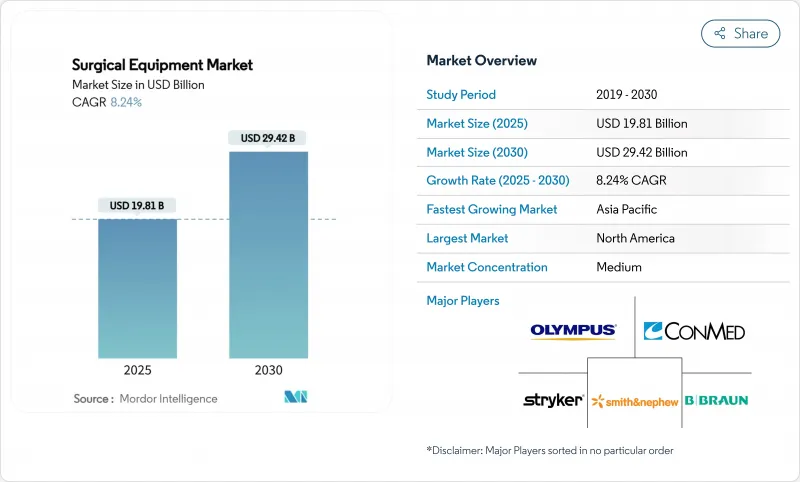

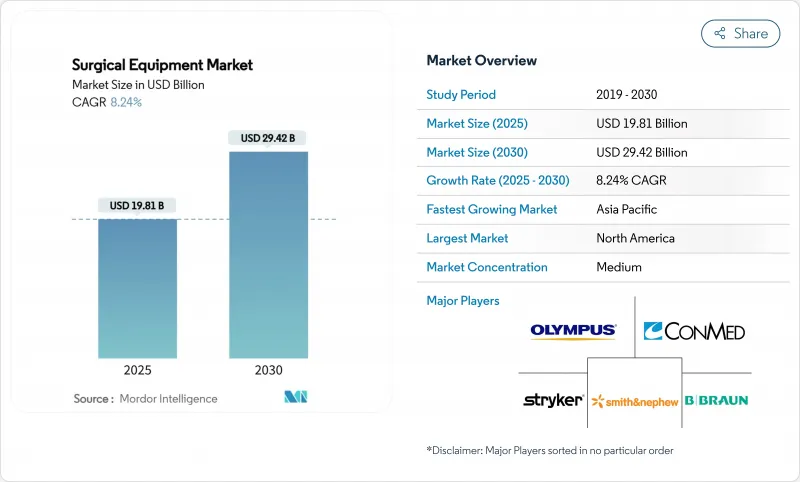

수술용 장비 시장 규모는 2025년에 198억 1,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 8.24%로 성장할 전망이며, 2030년에는 294억 2,000만 달러에 달할 것으로 예측됩니다.

수술 건수 증가, 저침습 수술의 급속한 보급, 외래수술센터(ASC)의 존재감 증가가 전망을 강화하고 있습니다. 임상의가 한 단계로 조직을 절단, 밀봉, 응고하는 기구를 요구하고 있기 때문에 전동식 및 전기 수술 기구가 제품 성장을 견인하게 됩니다. 아시아태평양은 중국과 인도의 생산 능력 증대 및 수술 건수의 꾸준한 증가를 반영하여 지역별로 가장 급속한 확대를 기록할 전망입니다. 외래 환자를 위해 설계된 컴팩트하고 워크플로에 특화된 시스템으로, 틈새 혁신자들이 기존 브랜드에 도전하고 있기 때문에 경쟁이 치열해지고 있습니다. 병원과 ASC의 자본 제약으로 인해 공급업체는 유연한 자금 조달 및 처치별 가격 설정을 하고 있으며, 수술용 장비 시장 전체의 구매 역학을 재구성하고 있습니다.

수술 건수는 계속 상승하고 있으며, 매년 약 2억 3,500만 건의 대수술이 진행되고 있습니다. 정형외과 수술, 심장혈관 수술 및 종양 외과 수술은 세계 인구가 고령화되고 만성 질환의 부담이 증가함에 따라 증가한 수술 건수를 많이 차지합니다. 제조업체 각사는 폭넓은 범용 세트를 제공하는 것이 아니라, 수술 건수가 많은 전문 분야에 특화한 기구를 제공하는 것으로, 스루풋을 향상시켜, 낭비를 생략하는 것으로 대응하고 있습니다. 정형외과 수술은 매년 7.2% 증가하고 있으며, 전동 톱, 드릴, 내비게이션 보조기구 수요에 박차를 가하고 있습니다. 심혈관 인터벤션은 연간 5.8%의 속도로 진보하고 있으며, 이미징 및 저침습 기능을 결합한 하이브리드 수술실에 대한 투자를 촉진하고 있습니다. 그 결과, 일상적인 혹사를 견딜 수 있는 신뢰성이 높은 절차에 특화된 시스템의 지속적인 요구가 높아지고 있습니다.

교통사고로 인한 부상이나 직장에서의 외상은 구급 현장에서의 신속한 개입을 가능하게 하는 골절 고정용 하드웨어, 휴대용 화상 처리, 내비게이션 시스템에 대한 수요를 계속 증가하고 있습니다. 외상 외과의사는 기존의 플레이트와 스크류뿐만 아니라 실시간으로 스크류 배치를 유도하고 수술 시간을 단축하며 재수술을 최소화할 수 있는 통합 플랫폼을 요구하고 있습니다. 장비 제조업체는 정형외과 안에 외상 전용의 부문을 마련해, 병원이 큰 부상 센터를 확장해, 외상 대응 킷을 재고함에 따라, 일반 정형외과 장비를 웃도는 성장을 이루고 있습니다.

최상급 로봇 플랫폼은 200만 달러 이상일 수도 있으며, 연간 서비스 계약에는 10-15%의 추가 비용이 듭니다. 소규모 병원이나 ASC에서는 구매를 늘리거나 이용률에 비용을 연동시키는 페이퍼 유스 모델을 요구하는 경우가 많습니다. 임대, 수익 공유 및 위험 풀 계약으로 인해 장벽이 점차 완화되고 있지만, 자본 집약형 시스템은 여전히 대규모 학술 센터에 집중하고 있습니다.

봉합사, 스테이플러 및 기타 폐쇄 기구는 2024년에 수술용 장비 시장 점유율의 38.24%를 차지했으며, 전문 분야 전반에 걸쳐 보편적인 역할을 담당하고 있는 것으로 나타났습니다. 매듭을 제거하는 가시 봉합사는 제왕 절개의 폐쇄 시간을 평균 1분 43초 단축하여 워크플로우의 가치를 입증합니다. 존슨 엔드 존슨의 ECHELON ENDOPATH Staple Line Reinforcement는 생체 재료의 진보가 조직을 보호하고 누출을 줄이는 방법을 보여줍니다.

동력 및 전기 수술 시스템은 2030년까지 연평균 복합 성장률(CAGR) 8.57%로 확대될 것으로 예측됩니다. 메드트로닉의 LigaSure Maryland jaw와 같은 기구는 절단과 혈관 봉쇄를 융합시켜 수술 단계를 줄이고 부수적 손상을 줄입니다. 리트랙터, 핸드헬드 포셉, 수술용 전동 공구는 여전히 필수적인 스테디셀러이지만, 프론티어는 에너지, 이미지, 배연을 통합하고 무균 영역을 간소화하는 통합 콘솔에 있습니다. 외래환자 센터가 공간 효율을 위해 다기능 타워를 채용함에 따라 동력 장비의 수술용 장비 시장 규모는 더욱 기세를 늘릴 것으로 보입니다.

북미는 2024년 매출액의 35.54%를 차지하였고, 유리한 상환과 로봇 및 AI 대응 시스템의 조기 도입이 견인했습니다. 병원은 비용 압박에 노출되었지만 ASC는 페이어 인센티브와 환자의 당일 수술 지향을 반영하여 활황을 보이고 있습니다. 자본 근대화 지연이 지속됨에 따라 장비의 평균 수명주기가 길어지고 공급자는 서비스 계약 및 임대 모델로 전환하고 있습니다. 그럼에도 불구하고, 미국과 캐나다의 센터는 차세대 로봇 수술과 디지털 수술의 실험장이 될 것입니다.

유럽은 견고한 공공 의료 제도에 의해 지원되는 광범위한 지역입니다. 독일, 프랑스, 영국은 저침습 수술 플랫폼 도입의 선진을 끊고 있습니다. 새로운 의료기기 규제는 시판 후 모니터링을 강화하고 컴플라이언스 비용을 늘리면서도 환자의 안전성을 강화하고 있습니다. 남유럽 및 동유럽 시장은 레거시 인프라를 업그레이드하고 있어 중가격대의 다용도 기기가 지지되는 캐치 업 성장 시장이 되고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 8.83%로 성장이 전망되는 급성장 지역입니다. 중국은 현재 로봇 극장의 2위를 차지한 국가이며, 지역 예산에 맞게 설계를 하는 국내 제조업체에 지지를 받고 있습니다. 일본은 1인당 수술 건수로 선도하고 있으며 인도는 세제 우대 조치와 합리화된 승인으로 연간 15%의 장비 도입을 목표로 하고 있습니다. 동남아시아 국가들은 지방의 거점에 수술실을 증설하고 있으며, 현장에서의 트레이닝 및 서비스 보증을 포함한 턴키로 번들된 장비 패키지에 대한 수요를 부추기고 있습니다.

중동 및 아프리카와 남미는 정부가 의료 예산을 외과 인프라에 더 많이 할당하기 때문에 장기적인 가능성을 지니고 있습니다. 브라질과 걸프 협력 회의의 민간 병원 체인은 로봇 시스템을 신속하게 채택하고 공공 시설이 그것에 필적하도록 노력하는 벤치 마크를 설정합니다.

The Surgical Equipment Market size is estimated at USD 19.81 billion in 2025, and is expected to reach USD 29.42 billion by 2030, at a CAGR of 8.24% during the forecast period (2025-2030).

Rising procedure volumes strengthen the outlook, rapid uptake of minimally invasive techniques, and the growing presence of ambulatory surgical centers (ASCs). Powered and electrosurgical devices are set to lead product growth as clinicians seek instruments that cut, seal, and coagulate tissue in a single step. Asia-Pacific is on course to record the fastest regional expansion, reflecting capacity build-outs in China and India alongside steadily rising surgical volumes. Competitive intensity is growing as niche innovators challenge established brands with compact, workflow-specific systems designed for outpatient settings. Capital constraints in hospitals and ASCs are nudging suppliers toward flexible financing and per-procedure pricing, reshaping purchasing dynamics across the surgical equipment market.

Procedure counts continue to climb, with roughly 235 million major operations performed each year. Orthopedic, cardiovascular, and oncology surgeries account for much of the incremental volume as global populations age and the burden of chronic disease rises. Manufacturers are responding by tailoring instruments to high-volume specialties rather than offering broad, general-purpose sets, improving throughput and reducing waste. Orthopedic procedures are growing 7.2% annually, spurring demand for powered saws, drills, and navigation aids. Cardiovascular interventions are advancing 5.8% per year, prompting investment in hybrid operating rooms that combine imaging and minimally invasive capabilities. The net effect is a sustained need for reliable, procedure-specific systems that can withstand heavy daily utilization.

Road-traffic injuries and workplace trauma continue to elevate demand for fracture fixation hardware, portable imaging, and navigation systems that enable rapid intervention in emergency settings. Beyond traditional plates and screws, trauma surgeons now seek integrated platforms capable of guiding screw placement in real time, shortening operative windows, and limiting repeat surgeries. Device makers have carved out a dedicated trauma segment within orthopedics, with growth outpacing general orthopedic equipment as hospitals expand major-injury centers and stock trauma-ready kits.

A top-tier robotic platform can cost more than USD 2 million, with annual service contracts adding 10-15%. Smaller hospitals and ASCs often defer purchases or seek pay-per-use models that link expenses to utilization. Leasing, profit-sharing, and risk-pooling agreements are gradually easing barriers, yet capital-intense systems remain concentrated in large academic centers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Sutures, staplers, and other closure devices held 38.24% of the surgical equipment market share in 2024, underlining their universal role across specialties. Barbed sutures that eliminate knot-tying have shaved an average 1 minute 43 seconds off cesarean section closure times, demonstrating workflow value. Johnson & Johnson's ECHELON ENDOPATH Staple Line Reinforcement illustrates how biomaterial advances can protect tissue and reduce leaks.

Powered and electrosurgical systems are projected to expand at an 8.57% CAGR through 2030. Instruments such as Medtronic's LigaSure Maryland jaw blend cutting and vessel-sealing, cutting operative steps, and collateral damage. Retractors, handheld forceps, and surgical power tools remain essential staples, but the frontier lies in integrated consoles that merge energy, imaging, and smoke evacuation, streamlining the sterile field. The surgical equipment market size for powered devices is likely to gain further momentum as outpatient centers adopt multifunction towers for space efficiency.

The Surgical Equipment Market Report is Segmented by Product (Handheld Surgical Instruments, Powered & Electrosurgical Devices, Sutures, and More), Application (Orthopedic & Trauma, Cardiovascular & Thoracic, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America held 35.54% of 2024 revenue, driven by favorable reimbursement and early adoption of robotic and AI-enabled systems. Hospitals are under cost pressure, but ASCs are flourishing, reflecting payer incentives and patient preference for same-day procedures. Ongoing capital modernization delays have increased the average equipment life cycle, pushing providers toward service contracts and rental models. Nonetheless, U.S. and Canadian centers remain the proving ground for next-generation robotic and digital-surgery suites.

Europe presents a broad landscape anchored by robust public health systems. Germany, France, and the United Kingdom spearhead uptake of minimally invasive platforms. New Medical Device Regulations strengthen post-market oversight, raising compliance costs yet bolstering patient safety. Southern and Eastern European markets, upgrading legacy infrastructure, represent catch-up growth pockets where mid-priced, versatile instruments gain favor.

Asia-Pacific is the fastest-growing zone, advancing at an 8.83% CAGR through 2030. China is now the second-largest buyer of robotic theaters, supported by domestic manufacturers who tailor designs to local budgets. Japan leads in procedure volumes per capita, while India targets 15% annual device adoption via tax incentives and streamlined approvals. Southeast Asian nations are adding surgical suites in provincial hubs, fueling demand for turnkey, bundled equipment packages that include on-site training and service warranties.

The Middle East & Africa and South America offer long-range potential as governments allocate larger health budgets to surgical infrastructure. Private-sector hospital chains in Brazil and the Gulf Cooperation Council are early adopters of robotic systems, setting benchmarks that public facilities strive to match.