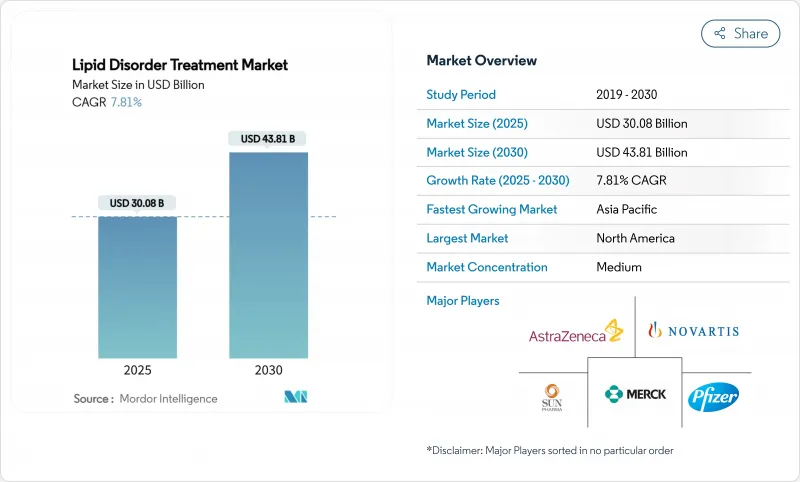

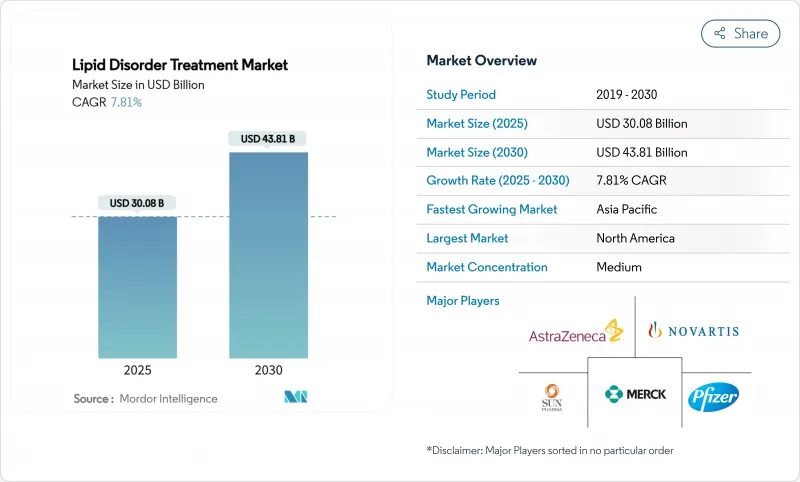

세계의 이상지질혈증 치료 시장 규모는 2025년에 300억 8,000만 달러로 추정되고, 2030년에는 438억 1,000만 달러에 달할 것으로 예측되며, 이 기간에 CAGR 7.81%로 성장이 전망됩니다.

성장이 가속화되는 배경에는 획기적인 유전자 편집 요법과 siRNA(small-interfering RNA) 요법이 있으며, 이들은 지속적인 LDL-C 대조를 약속하고, 케어 모델을 평생에 걸쳐 정제 요법에서 잠재적인 일회성 개입으로 이동시키고 있습니다. 게다가 고령화 및 비만 경향이 있는 사람들 사이에서 지질이상혈증 유병률이 확대되고 있는 것, 성과 기반의 계약을 받아들이는 지불자가 확대되고 있는 것, 치료에 대한 액세스를 용이하게 하는 디지털 약국의 보급이 진행되고 있는 것 등도 채용을 뒷받침하고 있습니다. 엘라이 릴리에 의한 버브 세라퓰틱스의 13억 달러 인수로 대표되는 M&A의 활성화는 차세대 치료법에 대한 대기업의 헌신을 나타내며 파이프라인 차별화를 둘러싼 라이벌 싸움을 격화시키고 있습니다. 지역적 기세는 아시아태평양으로 기울어지고 있으며, 인구동태 변화 및 전자상거래의 급속한 보급으로 이상지질혈증 치료 시장은 2자리 확대가 전망되고 있습니다.

2050년까지 미국 성인의 61%가 심혈관 질환을 앓을 것으로 예측되며, 비만 유병률은 2024년 43.1%에서 2050년 60.6%로, 고혈압은 51.2%에서 61%로 상승할 전망입니다. 심혈관계 질환으로 이미 연간 390만 명이 사망하고 있는 유럽에서도 비슷한 패턴이 있어 적극적인 지질 관리의 중요성이 강조되고 있습니다. 아시아의 중류계급의 부유화는 고지방식이 섭취와 앉기 쉬운 라이프스타일을 증대시켜 처방되는 지질저하요법의 보급을 가속화하고 있습니다. 그 결과 이상지질혈증 치료 시장은 1차 예방과 2차 예방 양면에서 지속적인 처방량의 성장을 경험하고 있습니다. 제약 회사는 문화에 맞는 복약 준수 프로그램과 지질 모니터링을 일상적인 웰니스 용도에 통합하는 원격 영양 서비스로 대응하고 있습니다.

세계적인 평균 수명이 증가함에 따라 2050년까지 17%의 사람들이 85세 이상이 되어 LDL-C의 누적 노출과 다질환의 이환이 증가합니다. 이미 세계 최고령 사회인 일본에서는 2030년까지 심부전 환자가 130만 명에 달할 것으로 예상되고 있으며, 심장병 특유의 치료 프로토콜이 필요합니다. 고령자는 종종 폴리파머시(다제 병용)의 과제를 안고, 스타틴의 내성도 다양하기 때문에 매일의 정제 부담을 최소화하는 저빈도의 주사약이나 유전자 편집 옵션에 대한 수요가 높아지고 있습니다. 의료 기술 평가기관은 고령자를 위한 고가이지만 내구성이 있는 치료제에 대응하기 위해 비용 효과의 역치를 개정하고 있습니다.

현실의 증거에 따르면 스타틴 사용자의 6-10%가 근육 증상이나 인식된 간 위험을 이유로 치료를 중지하고 있습니다. SLCO1B1과 같은 유전자 다형성은 표준 용량에서 불내성의 확률을 높이고 첫 번째 선택 요법의 선택을 복잡하게 합니다. 환자 조사에서는 51.5%가 처방량 증가보다 생활 습관 개선을 선호하고 17.1%가 거부의 근거로 정제 부담을 꼽았습니다. 이러한 역학은 벰페토산, 인클리실란, 에제티미브 제제와 같은 대체 약물에 대한 수요를 증가시키지만, 접근이 불균등하게 유지되면, 이상지질혈증 치료 시장 전체의 보급률을 감소시킬 수 있습니다.

가족성 고콜레스테롤혈증(FH)은 2024년 이상지질혈증 치료 시장 규모의 12.65%를 차지하였고, 2030년까지 CAGR은 가장 빠른 12.65%로 성장할 것으로 예측됩니다. 유전적 확인을 수반하지 않는 고콜레스테롤혈증은 2024년에 41.51%의 점유율을 차지해 전체적인 볼륨 리더를 유지했습니다. 캐스케이드 검사의 강화는 진단되지 않은 FH 친족을 발견하고 PCSK9 억제제와 siRNA 구조물의 처방 개시를 촉진합니다. FH의 유병률은 일반 집단에서 250명에 1명, 조발성 관상동맥 질환 환자에서는 최대 16명에 1명이며, 유전체적으로 특정 가능한 서브마켓을 형성하고 있습니다. 사회 가이드라인은 2세까지의 콜레스테롤 스크리닝을 권장하도록 되어 있으며, 소아 환자를 유전자 패널을 이용하여 확정적인 분류를 하는 지질 전문 클리닉으로 유도하고 있습니다.

Precision Medicine의 보험 상환 체계는 현재 FH 요법을 평생 사건 회피에 의한 고가치 요법으로 분류하고 있습니다. 캐나다와 네덜란드에서는 친척들이 적극적으로 검진을 받고 조기에 치료를 받았을 때 비용 절감을 입증합니다. 그 결과 이상지질혈증 치료 시장은 유전적으로 확인된 FH에 대한 제1선택약으로 자리매김하는 차세대 약제에 대한 수요 증가를 기록하고 있으며, 스타틴이 효과가 없어지는 훨씬 이전부터 판매를 가속화하고 있습니다.

2024년 이상지질혈증 치료 시장에서는 스타틴계 약제의 점유율이 56.53%를 유지했으며, 제네릭 의약품과 가이드라인에 의한 기호의 정착에 지지되고 있습니다. 그러나 PCSK9 억제제는 연 2회 투여 잉크실란과 분기 1회 주사가 필요한 완전 인간형 단일클론항체의 등장에 의해 활기차고 CAGR 16.85%로 다른 모든 클래스를 웃도는 것으로 예측되고 있습니다. 매우 중요한 임상시험에서 잉크리실란은 18개월 동안 LDL-C를 50-55% 감소시켰고, 어드히어런스는 90% 이상이었습니다. 벤페산은 스타틴 불내성 환자에 대해 LDL-C를 17-28% 감소시키고 틈새 시장에서 확대하는 보조제 시장을 차지합니다. 아포(a), CETP, ANGPTL3을 표적으로 하는 안티센스 올리고뉴클레오티드는 파이프라인의 다양성을 나타내며 의사의 선택을 넓히는 다기전 경쟁을 보장합니다.

리베이트 역학의 진화 : 제조업체 각자는 현실의 LDL-C 궤적과 심혈관 결과에 연동된 가치 기반 계약을 확대하여 더 빠른 포뮬러 포지셔닝을 획득합니다. 이를 통해 이해관계자 간의 경제적 인센티브를 조정하고 위험 기반 보험 코호트에 대한 침투를 촉진합니다. 결과적으로, 이상지질혈증 치료 산업은 스타틴 제형의 양 주도형에서 생물학적 제제의 결과 주도형으로 점차 방향을 바꾸고 있습니다.

북미는 2024년 매출 점유율 36.32%를 차지했으며, 이상지질혈증 치료 시장을 독점하고 있습니다. 이것은 견고한 보험 적용, 적극적인 스크리닝, 신속한 생명 공학 도입에 의해 지원됩니다. 잉크리실란, 올레잘센, 유전자 편집 자산에 대한 획기적인 치료제 지정은 미국에서 승인을 합리화하고 CMS는 2026년부터 상환을 임상 실적 지표에 맞춥니다. PCORnet과 같은 실제 세계 증거 플랫폼은 시판 후 조사를 용이하게 하고 혁신적인 치료법에 대한 지불자의 신뢰를 강화합니다. 캐나다의 각 주에서는 공공 등록을 통해 자금을 지원하는 캐스케이드 FH 스크리닝 프로그램이 시험적으로 실시되어 대상 환자층이 확대되고 있습니다.

유럽에서는 전국적인 지질 클리닉 네트워크와 예방적 가치가 입증된 경우 고비용 주사제로 환불을 하는 지불자의 의욕에 힘입어 한 자리대 중반의 꾸준한 성장을 기록했습니다. EMA의 지침 개정은 암멧 의료 요구를 중시하고 적응증 라이선싱을 가속화하며 이상지질혈증 치료 시장이 새로운 메커니즘을 조기에 임상으로 전환시키는 데 도움이 됩니다. 그러나 독일 AMNOG 프레임워크와 프랑스 CEPS의 가격 협상은 정가를 측정할 수 있는 심혈관 결과와 연결하는 경향이 강해져 제조업체의 마진을 압박하고 있습니다.

아시아태평양은 CAGR 10.61%에서 가장 급성장하고 있는 지역으로 중국의 고령화 및 인도 중산계급 확대가 그 원동력이 되고 있습니다. 중국에서는 2024년 정부의 상환 리스트에 PCSK9 억제제가 추가되어 환자의 자기 부담이 60% 삭감되고 처방의 변천이 유발됩니다. 일본에서는 고령환자에 맞춘 심장 원격 재활과 재택 주사 프로그램에 투자하여 지속률을 높여가고 있습니다. 한편 인도에서는 e-pharmacy 규제에 의해 전국적인 콜레스테롤 요법의 통신 판매가 합법화되어 농촌 지역의 접근 격차가 해소됩니다. 이러한 동향을 종합하면 아시아태평양은 2030년까지 이상지질혈증 치료 시장 규모 확대에 크게 기여하게 됩니다.

The global lipid disorder treatment market size reached USD 30.08 billion in 2025 and is forecast to climb to USD 43.81 billion by 2030, translating into a 7.81% CAGR over the period.

Accelerated growth stems from breakthrough gene-editing and small-interfering RNA (siRNA) therapies that promise durable LDL-C control, shifting care models away from lifelong pill regimens toward potential one-time interventions. Adoption is further propelled by expanding dyslipidemia prevalence among aging and obesity-prone populations, widening payer acceptance of outcomes-based contracts, and rising digital-pharmacy penetration that eases therapy access. Heightened M&A activity-typified by Eli Lilly's USD 1.3 billion purchase of Verve Therapeutics-signals large-cap commitment to next-generation modalities and intensifies rivalry around pipeline differentiation. Regional momentum is tilting toward Asia-Pacific, where demographic transitions and rapid e-commerce uptake position the lipid disorder treatment market for double-digit expansion.

Cardiovascular disease is projected to affect 61% of U.S. adults by 2050, with obesity prevalence climbing from 43.1% in 2024 to 60.6% in 2050 and hypertension from 51.2% to 61%. Comparable patterns in Europe, where cardiovascular disease already causes 3.9 million deaths annually, underscore the centrality of aggressive lipid management. Rising middle-class wealth in Asia amplifies high-fat dietary intake and sedentary lifestyles, accelerating uptake of prescription lipid-lowering therapies. Consequently, the lipid disorder treatment market is experiencing sustained prescription volume growth across both primary and secondary prevention settings. Pharmaceutical companies are responding with culturally tailored adherence programs and tele-nutrition services that integrate lipid monitoring into everyday wellness applications.

Global life expectancy gains mean 17% of people will be >= 85 years old by 2050, amplifying cumulative LDL-C exposure and polymorbidity. Japan, already the world's oldest society, expects heart failure cases to reach 1.3 million by 2030, prompting cardiogeriatric-specific treatment protocols. Older adults often present polypharmacy challenges and variable statin tolerance, fueling demand for lower-frequency injectables and gene-editing options that minimize daily pill burdens. Health-technology-assessment agencies are revising cost-effectiveness thresholds to accommodate high-priced but durable therapeutics for seniors.

Real-world evidence indicates 6-10% of statin users discontinue therapy due to muscle symptoms or perceived hepatic risk. Genetic polymorphisms such as SLCO1B1 increase intolerance odds at standard doses, complicating first-line therapy selection. Patient surveys reveal that 51.5% prefer lifestyle changes over prescription escalation, and 17.1% cite pill burden as rationale for rejection. These dynamics heighten demand for alternatives like bempedoic acid, inclisiran, and ezetimibe combinations that occupy premium reimbursed positions but can erode overall lipid disorder treatment market penetration if access remains uneven.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Familial hypercholesterolemia (FH) accounted for 12.65% of the lipid disorder treatment market size in 2024 and is expected to deliver the fastest 12.65% CAGR through 2030. Hypercholesterolemia without genetic confirmation retained overall volume leadership, holding 41.51% share in 2024. Enhanced cascade testing uncovers undiagnosed FH relatives, driving prescription initiation of PCSK9 inhibitors and siRNA constructs. FH prevalence of 1 in 250 general population and up to 1 in 16 among premature coronary-artery-disease patients creates a sizable, genomically identifiable submarket. Societal guidelines increasingly recommend universal cholesterol screening by age 2, funneling pediatric cases into specialized lipid clinics that employ gene panels for definitive classification.

Precision-medicine reimbursement frameworks now classify FH therapies as high-value due to lifetime event avoidance. Payer pilots in Canada and the Netherlands demonstrate cost savings when relatives are proactively screened and treated early. Consequently, the lipid disorder treatment market registers escalating demand for next-generation agents positioned as first-line for genetically confirmed FH, accelerating sales traction well before statin failure.

Statins maintained 56.53% share of the lipid disorder treatment market in 2024, buoyed by generics and entrenched guideline preference. However, PCSK9 inhibitors are projected to outpace all other classes at a 16.85% CAGR, energized by twice-yearly inclisiran and upcoming fully human monoclonal antibodies requiring quarterly injections. In pivotal trials, inclisiran sustained 50-55% LDL-C reductions over 18 months with adherence above 90%. Bempedoic acid offers 17-28% LDL-C lowering for statin-intolerant patients, occupying a niche yet expanding adjunct market. Antisense oligonucleotides targeting apo(a), CETP, and ANGPTL3 present pipeline diversity, ensuring multi-mechanistic competition that broadens physician choice.

Rebate dynamics evolve: manufacturers extend value-based contracts pegged to real-world LDL-C trajectories and cardiovascular outcomes, thus gaining earlier formulary positioning. This aligns economic incentives across stakeholders and augments penetration into risk-based insurance cohorts. As a result, the lipid disorder treatment industry increasingly pivots from volume-driven statin scripts to outcome-anchored biologic regimens.

The Lipid Disorder Treatment Market Report is Segmented by Indication (Hypercholesterolemia, Familial Combined Hyperlipidemia, and More), Drug Class (PCSK9 Inhibitors, and More), Distribution Channel (Hospital Pharmacies, and More), Route of Administration (Oral and Parenteral), Patient Type (Primary Hyperlipidemia, and More), and Geography North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America dominated the lipid disorder treatment market with 36.32% revenue share in 2024, underpinned by robust insurance coverage, proactive screening, and rapid biotech adoption. Breakthrough therapy designations for inclisiran, olezarsen, and gene-editing assets streamline U.S. approvals, while CMS is aligning reimbursement to clinical performance metrics starting 2026. Real-world evidence platforms such as PCORnet facilitate post-marketing surveillance, strengthening payer confidence in innovative modalities. Canadian provinces pilot cascade FH screening programs funded through public registries, widening eligible patient pools.

Europe posted steady, mid-single-digit growth, sustained by national lipid-clinic networks and payer willingness to reimburse high-cost injectables when preventive value is demonstrable. EMA guideline revisions emphasize unmet medical need and accelerate adaptive licensing, helping the lipid disorder treatment market transition new mechanisms into clinical practice sooner. However, pricing negotiations in Germany's AMNOG framework and France's CEPS increasingly tie list prices to measurable cardiovascular outcomes, pressuring manufacturer margins.

Asia-Pacific is the fastest-growing region at a 10.61% CAGR, driven by China's aging demographic and India's expanding middle class. Government reimbursement lists in China added PCSK9 inhibitors in 2024, cutting patient co-pay by 60% and triggering prescription inflection. Japan invests in cardiac telerehabilitation and home-injection programs tailored for elderly patients, raising persistence rates. Meanwhile, e-pharmacy regulations in India legitimize nationwide mail-order cholesterol therapies, closing rural access gaps. Collectively, these trends cement Asia-Pacific as a prime contributor to incremental lipid disorder treatment market size through 2030.