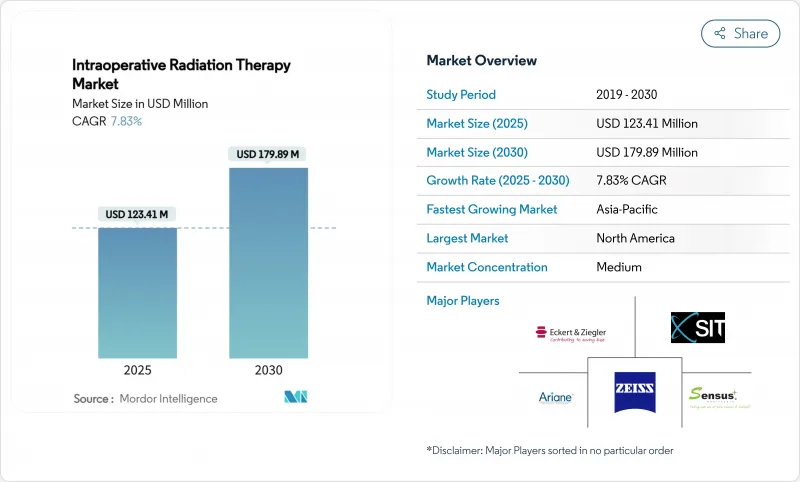

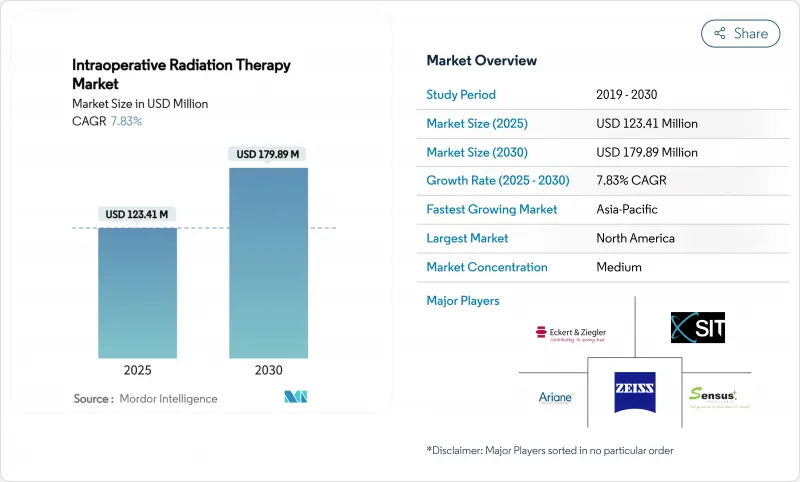

2025년 수술중 방사선 요법 시장 규모는 1억 2,341만 달러로, 2030년에는 1억 7,989만 달러에 이르고, CAGR 7.83%를 나타낼 것으로 예측됩니다.

이 성장은 선형 가속기의 능력을 해방하고, 치료 경로를 단축하며, 일괄 지불 인센티브를 따르는 단일 세션 방사선 옵션에 대한 병원 수요를 반영합니다. 소형화된 이동식 전자 가속기는 현재 표준 수술실에 설치할 수 있어 비용이 많이 드는 격납고의 개수가 불필요하게 되어 대응 가능한 서비스 부위가 확대되고 있습니다. 유방암의 국소 제어율이 동등하다는 조기 근거가 신경외과나 소화기 수술의 영상 유도 정밀도의 향상과 함께 임상적 신뢰를 지지하고 있습니다. 풀 스택 온 콜로지 플랫폼을 중심으로 하는 벤더의 통합은 서비스 지향 수익 모델과 함께 도입 지원을 강화하고 중규모 공급자의 소유 위험을 완화하고 있습니다.

암 이환율은 2030년까지 새롭게 2,400만 증례에 달할 것으로 예상되고 있으며, 많은 외조사 시설의 능력을 압도하고 있습니다. 521개의 방사선치료센터가 연간 130만명 이상의 증례에 대응하고 있으며, 치료 지연으로 이어지고 있습니다. IORT는 몇 주 동안 치료 요법을 한 번의 치료가 아니 복잡한 분할 사례에 대한 치료 프레임을 확보하고 처리량을 향상시킵니다. 인구 밀도가 높은 국가의 보건부는 휴대용 전자 장치를 수술실의 유용성을 높이는 일시적인 인프라로 간주합니다. 이 동향은 OECD 국가에서의 인구동태의 고령화에도 합치하고 있어, 합병증의 부담에 의해 장기간의 치료가 현실적이 없어지고 있습니다.

바리안의 HyperSight 이미징은 촬영 시간을 50% 단축하여 병변의 가시화를 향상시킵니다. 40Gy/s를 초과하는 FLASH 프로토콜은 정상 조직의 독성을 억제할 것으로 예상되며 치료 시간은 4-9분입니다. 인공지능 모델이 유방 온존 수술중 단단 양성 예측으로 84%의 정확도를 달성하여 재절제 위험을 감소시킵니다. 가속기의 소형화, 차폐의 경량화, 배터리 구동에 의해 저 자원 환경에서의 채용이 넓어지고 있습니다. 이러한 진보가 결합되어 전문적인 훈련의 필요성이 줄어들고, 총 수술 시간이 단축되고, 집학적인 팀을 끌어들이고 있습니다.

방사선치료의 결원률은 2022년에 10.7%에 달했고, 의료용 선량측정의 부족은 2035년까지 계속될 것으로 예측되고 있습니다. IORT에서는 외과의사, 물리학자, 치료사의 실시간 연계가 요구되지만, 이 조합은 3차 센터 이외에서는 희소합니다. 공인기관은 2017년에 실지연수의 길을 폐지했기 때문에 후보자는 수술중 실지연수가 드물게 희귀한 바칼로레아 과정에 입학을 강요받았습니다. 소규모 병원은 증례 수가 적은 가운데 전문 팀을 정당화하는 데 어려움을 겪고 있으며 지역 액세스 격차가 발생하고 있습니다. 따라서 노동력 병목 현상은 설비가 이용 가능함에도 불구하고 확대를 억제하고 있습니다.

2024년 수술중 방사선 요법 시장에서는 수십년에 걸친 유방암 검증과 합리화된 모바일 가속기 워크플로우를 배경으로 전자선 접근법이 59.91%의 점유율을 유지했습니다. 이 치료법은 병원이 이미 보유하고 있는 어플리케이터 및 품질 보증 도구의 신뢰할 수 있는 공급망을 유지합니다. 그러나 수술중 브랙세라피는 고해상도 애프터 로더와 실시간 복용량 소프트웨어가 부정강 내 적합성을 개선하기 때문에 2030년까지 연평균 복합 성장률(CAGR)은 8.34%를 나타낼 것으로 예측됩니다. 광자 기반 및 알파 입자 시드 시스템은 FDA의 시험 면제 조치에 의해 재발 교모세포종의 조기 도입이 진행되고 있으며, 3%의 틈새 영역이 형성되고 있습니다. 임상 팀은 현재 종양 지역에 맞게 치료법을 선택하고 다양한 구매 패턴을 뒷받침하고 있습니다.

전자 요법 지지자는 더 큰 유방과 골반 영역에 적합한 깊은 침투 능력을 지적하는 반면, 브랙세라피 지지자는 뇌 신경 근처의 선량 온존을 강조합니다. 알파 DaRT사의 라듐-224 시드는 파일럿 코호트에서 양호한 안전성을 보여 경쟁 압력을 높이고 있습니다. 전자 장바구니와 브라키 테라피 카트가 이미지 인프라를 공유하는 하이브리드 스위트를 공동 판매하는 공급업체는 카테고리 라인을 더욱 모호하게 만듭니다. 수술 종양학이 세분화됨에 따라 결정 기준의 중심은 고유한 물리적 선량보다는 절차 시간, 차폐 비용 및 자격의 숙련도입니다.

자본 매출은 2024년 매출의 67.21%를 차지했으며, 가속기 및 실시간 이미지 처리 콘솔의 반복 교환 사이클에 지원됩니다. 성숙시장의 병원은 진화하는 AI 통합계획 소프트웨어에 대응하기 위해 7-8년마다 플릿 갱신을 실시해 2자리대의 단가 성장을 유지하고 있습니다. 그러나 서비스 라인의 CAGR은 8.45%로 물리 지원, 원격 QA, 직원 인증을 번들로 제공하는 턴키 패키지에 대한 공급자의 의욕을 반영합니다. 수술중 방사선 요법 산업은 공급업체가 가동 시간을 보장하고 임상 품질 지표를 공유하는 성과 기반 서비스 계약으로 전환하고 있습니다.

Varian ARIA CORE와 같은 시스템 수준의 통합 플랫폼은 병리학, 이미지 및 선량 측정 데이터를 오버레이하여 사일로화된 워크플로우를 줄입니다. Software-as-a-Service 및 예측 보전 분석의 구독 모델은 현재 경상 매출의 22%를 차지하며 공급업체의 수익 변동을 평활화하고 있습니다. 액세서리 카테고리 - 살균 카트, 차폐 드레이프 및 도킹 스테이션 -은 고객에게 친환경 에코시스템으로 둘러싸인 이익률이 높은 소모품입니다. 설치 대수가 가시성을 높이는 한편, 특히 인원 배치에 제약이 있는 지역에서는 서비스 능력이 입찰의 낙찰을 좌우하는 경우가 많아지고 있습니다.

The Intraoperative Radiation Therapy Report는 방법(전자선 IORT, 수술중 브레이크 테라피, 기타 방법), 제품 및 서비스(제품 및 서비스), 용도(유방암, 뇌종양, 기타), 최종 사용자(병원, 전문 클리닉 등), 지역(북미, 기타)으로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 명확한 HCPCS 코드와 번들 결제 조종사가 자본 투자 위험을 줄이기 위해 2024년 수술중 방사선 요법 시장 점유율을 42.45%로 유지했습니다. 미국에서는 통합 의료 제공 네트워크가 스케일 메리트를 활용하여 다년간의 서비스 계약을 협상하고 캐나다에서는 각 주가 IORT를 주 암 의료 기관 로드맵에 포함하고 있습니다. 교외 제공업체 네트워크에서는 이동 단위가 하룻밤 동안 캠퍼스를 순회하기 때문에 이용률이 85%를 넘어 자산 수익률이 향상된 것으로 보고되었습니다. 11개 주에서는 단회 투여 유방 부스트가 저분할 외 조사 요법과 동등하게 보험 상환되게 되어 보급이 가속되고 있습니다.

유럽에서는 국경을 넘어서는 기기인증의 뒷받침을 받아 꾸준한 보급이 유지되고 있지만, DRG의 지불에 편차가 있습니다. 독일과 이탈리아의 유선외과학회는 IORT를 선택한 환자의 표준치료로 하는 컨센서스 가이드라인을 발표하고 보험상환을 지지하고 있습니다. 영국의 국민보건서비스의 파일럿 스터디에서는 2024년의 평균 레이트로 환산했을 경우, 1례당 2,300파운드(2,930달러)의 순 절약이 되고, 그 주요 요인은 운송 서비스의 삭감입니다. 스칸디나비아 국가에서는 인구가 분산되어 동계 여행이 어려워지므로 1인당 이용률이 높습니다. 그러나 중·동유럽의 소규모 시장은 자본 예산의 제한에 직면하고 있으며, 장비의 갱신이 늦어지고 있습니다.

아시아태평양은 중국의 국가 아이소토프 로드맵과 일본의 고령화에 의해 2030년까지의 CAGR이 8.88%를 나타낼 것으로 예측됩니다. 정부 보조금을 통한 조달 체계는 지방 수준의 방사선 요법 허브에 자금을 제공하며, 매주 블록 스케줄링을 통해 수술실이 위성 병원에 서비스를 제공합니다. 대만에는 8개의 양자선 센터가 있으며, 수술중 치료 도입을 위한 지역 전문 지식을 창출하고 있습니다. 인도의 타타 메모리얼 체인은 농촌 지역의 아웃리치 프로그램에서 이동식 전자 치료 장치를 가동시켜 도시의 리니어크에 비해 환자의 평균 이동 거리를 53% 단축하고 있습니다. 필리핀에서는 1억 1,000만명의 시민에 대해 방사선 종양의가 113명밖에 없고, 트레이닝의 필요성이 부각되고 있습니다.

남미와 중동 및 아프리카는 여전히 새로운 비즈니스 기회입니다. 칠레의 관민 파트너십은 하이브리드 OR에 자금을 제공하고 사우디아라비아는 Vision 2030에 종양학 현대화 자금을 계상하고 있습니다. 통화 변동과 수입 관세가 경제 규모가 작은 국가를 방해하고 있지만, 중고 장비 시장과 벤더 금융으로 인한 임대가 진입 장벽을 낮추고 있습니다. 걸프 국가의 임상 학회는 유럽의 지침을 현지 진료에 반영하고 규제 당국의 규제 경로를 원활하게하고 있습니다. 인구동태의 변화와 암멧의 필요가 결합되어 노동력의 파이프라인이 실현되면 양 지역은 장기적인 시장 확대 엔진으로 자리매김할 수 있습니다.

The intraoperative radiation therapy market size stood at USD 123.41 million in 2025 and is forecast to reach USD 179.89 million by 2030, advancing at a 7.83% CAGR.

The growth reflects hospital demand for single-session radiation options that free linear-accelerator capacity, shorten care pathways and align with bundled-payment incentives. Miniaturised mobile electron accelerators now slot into standard operating rooms, eliminating costly bunker retro-fits and expanding addressable sites of service. Early evidence of equivalent local-control rates in breast cancer, combined with improving image-guided accuracy for neurosurgical and gastro-intestinal procedures, sustains clinical confidence. Vendor consolidation around full-stack oncology platforms, coupled with service-oriented revenue models, enhances implementation support and reduces ownership risk for mid-size providers.

Cancer incidence is projected to hit 24 million new cases by 2030, overwhelming capacity at many external-beam facilities . Emerging economies such as India illustrate the gap: 521 radiotherapy centers serve more than 1.3 million annual cases, leading to treatment delays. IORT compresses multi-week regimens into a single procedure, freeing slots for complex fractionated cases and improving throughput. Health ministries in high-density nations increasingly view portable electron units as stop-gap infrastructure that multiplies surgical suites' utility. The trend also aligns with demographic ageing in OECD economies, where comorbidity burdens make prolonged courses impractical.

Integration of surgical robotics with radiation delivery now enables margin-controlled dosing within minutes; Varian's HyperSight imaging cuts acquisition time by 50% and enhances lesion visualization . FLASH protocols delivering >40 Gy/s show promise for limiting normal-tissue toxicity, with trial treatment times of 4-9 minutes . Artificial-intelligence models achieve 84% accuracy in predicting positive margins during breast-conserving surgery, reducing re-excision risk. Miniaturised accelerators, lighter shielding, and battery operation broaden adoption in low-resource settings. Together, these advances reduce specialized training needs and shrink total procedural duration, attracting multidisciplinary teams.

Radiation therapist vacancy rates reached 10.7% in 2022, and medical dosimetrist deficits are projected to persist through 2035. IORT demands real-time collaboration among surgeons, physicists, and therapists, a combination scarce outside tertiary centers. Accreditation bodies eliminated on-the-job pathways in 2017, forcing candidates into scarce baccalaureate programs that seldom offer hands-on intraoperative exposure. Smaller hospitals struggle to justify dedicated teams amid low case volumes, creating regional access gaps. Workforce bottlenecks, therefore, temper expansion despite equipment availability.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Electron approaches retained 59.91% share of the intraoperative radiation therapy market in 2024 on the back of decades-long breast-cancer validation and streamlined mobile-accelerator workflows. The modality sustains a reliable supply chain for applicators and quality-assurance tools that hospitals already stock. Intraoperative brachytherapy, however, is expected to post an 8.34% CAGR through 2030 as high-definition afterloaders and real-time dosimetry software improve conformity in irregular cavities. Photon-based and alpha-particle seed systems represent a nascent 3% niche, with FDA investigational exemptions driving early uptake in recurrent glioblastoma. Clinical teams now match method to tumor geography, fuelling diversified purchasing patterns.

Electron advocates point to deeper penetration abilities that suit larger breast or pelvic fields, whereas brachytherapy proponents highlight dosimetric sparing near cranial nerves. Alpha DaRT's radium-224 seeds showed favorable safety in pilot cohorts, adding competitive pressure. Vendors co-marketing hybrid suites-where electron and brachytherapy carts share imaging infrastructure-further blur categorical lines. As surgical oncology subspecialises, decision criteria center on procedure time, shielding costs and credentialing familiarity rather than intrinsic physical dosimetry.

Capital sales delivered 67.21% of 2024 revenue, underpinned by repeat replacement cycles for accelerators and real-time imaging consoles. Hospitals in mature markets refresh fleets every 7-8 years to comply with evolving AI-integrated planning software, sustaining double-digit unit price growth. Yet service lines are on an 8.45% CAGR trajectory, reflecting provider appetite for turnkey packages that bundle physics support, remote QA and staff certification. The intraoperative radiation therapy industry has shifted toward outcome-based service contracts, where vendors assume uptime guarantees and share clinical-quality metrics.

System-level integration platforms like Varian ARIA CORE overlay data from pathology, imaging and dosimetry, reducing siloed workflows. Subscription models for software-as-a-service and predictive maintenance analytics now contribute 22% of recurring sales, smoothing vendor revenue volatility. Accessory categories-sterile carts, shielded drapes, docking stations-offer high-margin consumables that lock customers into proprietary ecosystems. While unit installations drive visibility, service competence increasingly determines tender awards, especially in resource-constrained regions where staffing depth is limited.

The Intraoperative Radiation Therapy Report is Segmented by Method (Electron IORT, Intraoperative Brachytherapy, Other Methods), Products and Services (Products and Services), Application (Breast Cancer, Brain Tumor, and More), End User (Hospitals, Specialty Clinics, Others), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America preserved 42.45% intraoperative radiation therapy market share in 2024 as clear HCPCS codes and bundled-payment pilots de-risk capital investment. U.S. integrated delivery networks leverage economies of scale to negotiate multiyear service contracts, while Canadian provinces include IORT in provincial cancer agency roadmaps. Provider networks in suburban settings report utilisation rates exceeding 85% because mobile units rotate among campuses overnight, extending return on assets. Eleven states now reimburse single-dose breast boosts at parity with hypofractionated external-beam regimens, accelerating penetration.

Europe maintains steady adoption on the back of cross-border device certification, though heterogenous DRG payments create variability. German and Italian breast-surgeon societies publish consensus guidelines that frame IORT as standard of care for selected patients, underpinning reimbursement. UK National Health Service pilot studies document net savings of GBP 2,300 (USD 2,930) per case after currency conversion at 2024 average rates, largely from reduced transport services. Scandinavian countries show high per-capita utilisation due to dispersed populations and winter travel challenges. However, smaller Central-Eastern markets face capital budget caps that delay fleet renewal.

Asia-Pacific is projected to log an 8.88% CAGR to 2030, powered by China's national isotope roadmap and Japan's ageing demography. Government-subsidised procurement schemes fund province-level radiotherapy hubs where intraoperative suites serve satellite hospitals via weekly block scheduling. Taiwan hosts eight proton centers, creating regional expertise that cross-pollinates intraoperative adoption. India's Tata Memorial chain operates mobile electron units in rural outreach programs, cutting average patient travel distance by 53% compared with city-based linacs. Despite strong momentum, workforce shortages persist: the Philippines counts only 113 radiation oncologists for 110 million citizens, underscoring training imperatives.

South America and the Middle East & Africa remain emerging opportunities. Chile's public-private partnerships finance hybrid ORs, while Saudi Arabia earmarks oncology modernization funds in Vision 2030. Currency volatility and import tariffs hamper smaller economies, yet used-equipment markets and vendor-financed leases lower entry barriers. Clinical societies across the Gulf states translate European guidelines to local practice, smoothing regulatory pathways. Over the forecast, unmet need combined with demographic shifts positions both regions as long-term volume engines if workforce pipelines materialize.