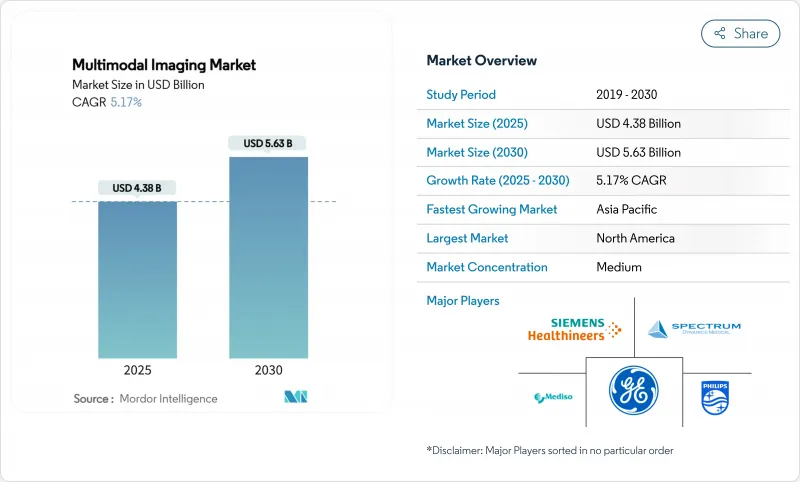

멀티모달 이미징 시장 규모는 2025년에 43억 8,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.17%로, 2030년에는 56억 3,000만 달러에 달할 것으로 예상됩니다.

의료 시스템은 해부학적 데이터와 기능적 데이터를 통합하는 하이브리드 진단 플랫폼을 강조하고 종양학 및 심장병학에서 조기 발견과 치료 모니터링의 정확성을 강화함으로써 성장이 형성됩니다. 인공지능 오버레이는 스캔 프로토콜을 자동화하고 검사 시간을 단축하며 진단의 신뢰성을 높입니다. 북미는 견조한 상환과 광범위한 방사성 의약품 사용으로 리더십을 유지하고 있지만 아시아태평양은 병원의 근대화, 만성 질환 부담, 민간 건강 관리 투자 확대를 배경으로 가장 빠른 궤도를 묘사하고 있습니다. 경쟁은 GE 헬스케어, Siemens 헬티니어스, Philips의 3개사로, 각각 클라우드 기반 애널리틱스를 활용하여 성능 차별화와 소유 비용 절감을 도모하고 있습니다. 자본 집약, 아이소토프 공급 불안정성, 데이터 통합 장애물과 같은 역풍은 뿌리 깊고 멀티모달 이미징 시장의 긍정적인 전망을 방해하고 있습니다.

암과 심혈관 질환의 이환율 증가로 고도의 진단에 대한 수요가 높아지고 있습니다. 멀티모달 이미징은 단일 모달리티 검사로는 대응할 수 없는 대사와 해부학적 상관관계를 제공하며, 이 모달리티를 예방 의료 전략의 중심에 위치시킵니다. 심혈관 MRI는 361명의 환자를 대상으로 한 연구에서 측정 가능한 비용 절감과 결과 개선에 기여하여 의료 경제적 가치를 명확히 했습니다. 이용률은 30년간 27% 상승할 것으로 예상되지만, 이는 인구 증가만을 반영한 것이 아니라, 인구동태의 고령화와 임상 프로토콜의 확대를 반영한 것입니다. 신진 대사 매핑은 종양의 조기 발견과 반응 평가를 향상시켜 종양학 PET/CT의 사용량이 직접적인 혜택을 받을 것으로 보입니다. 따라서, 비전염성 질환의 지속적인 증가는 멀티모달 이미징 시장에 지속적인 기세를 가져옵니다.

하이브리드 스캐너는 현재 프로토콜을 자동화하고 이미지를 선명하게 하기 위해 AI를 통합하고 있습니다. 지멘스 헬스 이니어즈의 Biograph Horizon은 4 X 4mm LSO 크리스탈과 진정한 비행 시간 촬영을 채택하여 선량을 억제하면서 고해상도 검사를 실현합니다. 토탈 바디 PET는 다이내믹 촬영을 가능하게 하며 촬영 윈도우를 축소하면서 뛰어난 콘트라스트를 만들어냅니다. Philips와 엔비디아는 '제로 클릭' 계획을 가능하게 하는 MR 기반 모델을 공동으로 구축하여 재현성과 처리량 향상을 실현했습니다. 이러한 진보는 기술자의 작업 부담을 줄이고 스캐너 이용률을 높이고 임상 판단 지원을 강화합니다.

하이브리드 스캐너는 수백만 달러의 지출과 전문적인 유지 관리가 필요하므로 예산에 제약이 있는 환경에서의 도입을 방해합니다. 응급실에서의 연구에 따르면 멀티모달 CT는 현기증 진단의 확실성을 높이지만 경제적 부담은 종합적인 도입을 방해합니다. 클리닉 보상의 틀은 종종 혁신을 추종하기 때문에 투자 회수의 위험을 증가시키고 멀티모달 이미징 시장 전체의 보급을 제한합니다. 이미징 시장은 공급자가 서비스의 품질 기준을 유지하면서 이러한 비용 문제를 해결하기 위해 규모의 경제를 추구하기 위해 통합 압력에 직면하고 있습니다.

PET/CT 시스템은 광범위한 임상 가이드라인과 성숙한 상환경로에 힘입어 2024년 멀티모달 이미징 시장 점유율의 61.86%를 차지했습니다. 이 기술은 암의 병기 분류, 심근 관류, 신경 대사 평가를 지원하며 병원 워크 플로우에 필수적입니다. PET/CT의 멀티모달 이미징 시장 규모는 종양과의 사례수의 확대와 함께 밀접하게 성장하고 있습니다. 벤더는 검출기 재료, 긴 축 방향 시야, AI 지원에 의한 프로토콜 최적화로 차별화를 도모해 방사선량의 저감과 처리량의 향상을 실현하고 있습니다.

PET/MR은 현재 규모가 작은 것, 비교할 수 없는 연조직 콘트라스트와 전리 피폭의 저감에 지지되어 CAGR은 6.16%로 성장을 지속하고, 있습니다. Philips SmartSpeed Precise와 같은 딥러닝을 통한 재구성의 진보는 검사 시간을 단축하고, SNR을 향상시키고, PET/MR을 보다 워크플로우에 적합하게 하고 있습니다. PET/MR의 멀티모달 이미징 시장 규모는 종양센터가 소아 및 신경종양 적응증에 이 모달리티를 채택하기 때문에 향후 수년간 확대될 것으로 예측됩니다. SPECT/CT는 아이소토프 비용이 관리하기 쉬운 골전이와 심장 관류로 수요를 유지하고 있습니다. 초음파/CT를 포함한 틈새 조합은 인터벤셔널 스위트에서 전문적인 역할을 담당하고 멀티모달 이미징 시장에서 기술 믹스를 완성하고 있습니다.

북미의 멀티모달 이미징 시장 규모는 2024년에 17억 6,000만 달러에 달하고, 세계 점유율 40.16%에 해당했습니다. 학술의료센터에 집중하는 전문지식이 기술 보급을 가속화하고, 국경을 넘은 연계가 캐나다의 능력을 높입니다. 멕시코의 사립 병원은 의료 관광에 의한 시장 개척을 포착하고 하이브리드 스캐너 수요 증가를 전망합니다.

아시아태평양의 CAGR은 6.84%로 가장 높습니다. 중국은 PET/CT 도입을 의무화하는 대규모 종양학과 순환기학 프로그램에 자금을 제공하고, 일본은 노인 인구를 위해 진단의 우수성을 유지하기 위해 노후화된 스캐너를 업그레이드합니다. 인도의 민간 네트워크는 1급 도시에 디지털 PET/CT와 1.5T 헬륨 프리 MRI를 도입하여 액세스를 확대합니다. 호주와 한국은 유럽과 미국의 다른 회사에 필적하는 최첨단 플랫폼을 도입하여 지역적 기세를 강화하고 있습니다.

유럽은 성숙하면서도 확대 기조를 유지하고 독일이 현지 생산과 연구 개발을 통해 혁신의 선두에 서 있습니다. 유럽 의료 기술 평가 규칙(European Health Technology Assessment Regulation)을 기반으로 한 통합 평가 프레임워크는 조달을 간소화하고 지속적인 도입을 지원합니다. 남유럽 국가들은 EU가 자금을 제공하는 원격 영상 진단 이니셔티브를 전개하고, 농촌의 진료소와 도시의 중심지를 연결하고, 휴대용 PET/CT를 통합하여 진료 범위를 넓히고 있습니다. 이러한 역학이 결합되어 유럽의 멀티모달 이미징 시장은 안정적인 성장을 이어가고 있습니다.

The Multimodal Imaging Market size is estimated at USD 4.38 billion in 2025, and is expected to reach USD 5.63 billion by 2030, at a CAGR of 5.17% during the forecast period (2025-2030).

Growth is shaped by health-system emphasis on hybrid diagnostic platforms that merge anatomical and functional data, strengthening early detection and treatment-monitoring accuracy in oncology and cardiology. Artificial-intelligence overlays automate scan protocols, shorten exam times, and elevate diagnostic confidence, while regulatory approvals for next-generation devices accelerate market adoption. North America retains leadership through robust reimbursement and wide theranostic radiopharmaceutical use, yet Asia-Pacific delivers the fastest trajectory on the back of hospital modernization, chronic-disease burden, and expanding private healthcare investment. The competitive field remains moderately consolidated around GE Healthcare, Siemens Healthineers, and Philips, each leveraging cloud-based analytics to differentiate performance and reduce ownership costs. Persistent headwinds-capital intensity, isotope-supply volatility, and data-integration hurdles-temper the otherwise positive outlook for the multimodal imaging market.

Rising incidence of cancer and cardiovascular disorders keeps demand for sophisticated diagnostics high. Multimodal imaging delivers metabolic-anatomical correlation that single-modality exams cannot match, positioning the modality at the centre of preventive-care strategies. Cardiovascular MRI contributed measurable cost savings and outcome gains in a 361-patient study, underscoring health-economic value. Utilisation is projected to climb 27% in 30 years, reflecting demographic ageing and expanding clinical protocols rather than population growth alone. Oncology PET/CT volumes will benefit directly, as metabolic mapping improves early tumour detection and response assessment. The sustained rise in non-communicable disease prevalence therefore injects durable momentum into the multimodal imaging market.

Hybrid scanners now integrate AI to automate protocols and sharpen image clarity. Siemens Healthineers' Biograph Horizon employs 4 X 4 mm LSO crystals and true time-of-flight, delivering high-resolution studies at reduced dose. Total-body PET enables dynamic acquisition, producing superior contrast while shrinking acquisition windows. Philips and NVIDIA jointly built MR foundation models that allow "zero-click" planning, promoting reproducibility and faster throughput. Such advances reduce technologist workload, increase scanner utilisation, and strengthen clinical-decision support-elements that fuel uptake across the multimodal imaging market.

Hybrid scanners require multi-million-dollar outlays and specialised upkeep, hampering acquisition in budget-constrained settings. Emergency-department studies show that although multimodal CT elevates diagnostic certainty for dizziness, economic burden deters blanket implementation. Reimbursement frameworks often trail innovation, amplifying payback risk and limiting diffusion across the multimodal imaging market. The diagnostic imaging market faces consolidation pressures as providers seek economies of scale to manage these cost challenges while maintaining service quality standards.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PET/CT systems accounted for 61.86% of the multimodal imaging market share in 2024, supported by broad clinical guidelines and mature reimbursement pathways. This technology underpins cancer staging, myocardial perfusion, and neurological metabolism evaluation, making it indispensable for hospital workflows. The multimodal imaging market size for PET/CT is growing closely with expanding oncology caseloads. Vendors differentiate via detector materials, longer axial field-of-view, and AI-assisted protocol optimisation to shrink radiation dose and speed throughput.

PET/MR, though currently smaller, records a 6.16% CAGR, buoyed by unparalleled soft-tissue contrast and reduced ionising exposure. Advances in deep-learning reconstruction, such as Philips SmartSpeed Precise, now cut exam times and improve SNR, making PET/MR more workflow-friendly. The multimodal imaging market size for PET/MR is projected to grow in the coming years as oncology centres adopt the modality for paediatric and neuro-oncology indications. SPECT/CT sustains demand in bone metastasis and cardiology perfusion, where isotope costs remain manageable. Niche combinations, including ultrasound/CT, hold specialised roles in interventional suites, rounding out the technology mix within the multimodal imaging market.

The Multimodal Imaging Market Report is Segmented by Technology (PET/CT Systems, SPECT/CT Systems, PET/MR Systems, Others), Application (Oncology, Cardiology, Neurology, Ophthalmology, Musculoskeletal Disorders, Others), End-User (Hospitals, Diagnostic Imaging Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America's multimodal imaging market size reached USD 1.76 billion in 2024, equivalent to 40.16% global share, reflecting comprehensive insurance coverage and rapid AI workflow integration. Concentrated expertise at academic medical centres accelerates technology diffusion, while cross-border collaborations enhance Canadian capacity. Mexico's private hospitals seize market openings generated by medical tourism, adding incremental demand for hybrid scanners.

Asia-Pacific posts the highest CAGR at 6.84%. China funds large-scale oncology and cardiology programmes that mandate PET/CT inclusion, whereas Japan upgrades ageing scanners to maintain diagnostic excellence for an elderly population. India's private networks install digital PET/CT and 1.5T helium-free MRI in tier-1 cities, widening access. Australia and South Korea adopt cutting-edge platforms comparable to Western peers, reinforcing regional momentum.

Europe maintains a mature yet expanding base, with Germany spearheading innovation through local manufacturing and R&D. Unified valuation frameworks under the European Health Technology Assessment Regulation streamline procurement, underpinning continued adoption. Southern European nations deploy EU-funded tele-imaging initiatives that link rural clinics to urban centres, integrating portable PET/CT to extend reach. Collectively these dynamics keep Europe's multimodal imaging market on a stable growth.