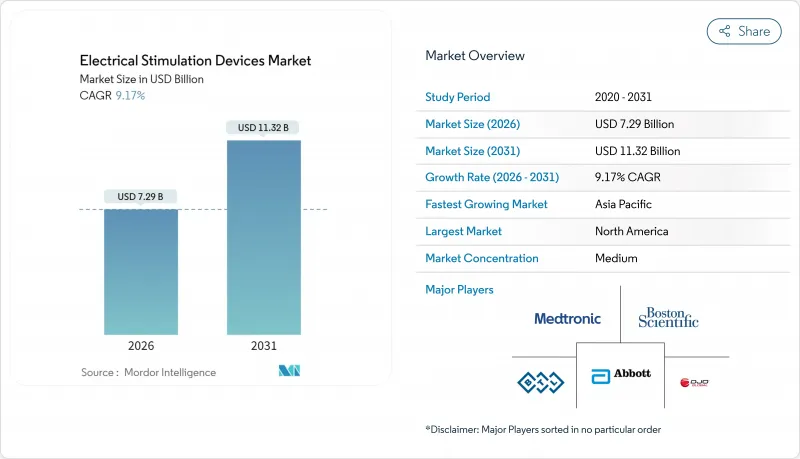

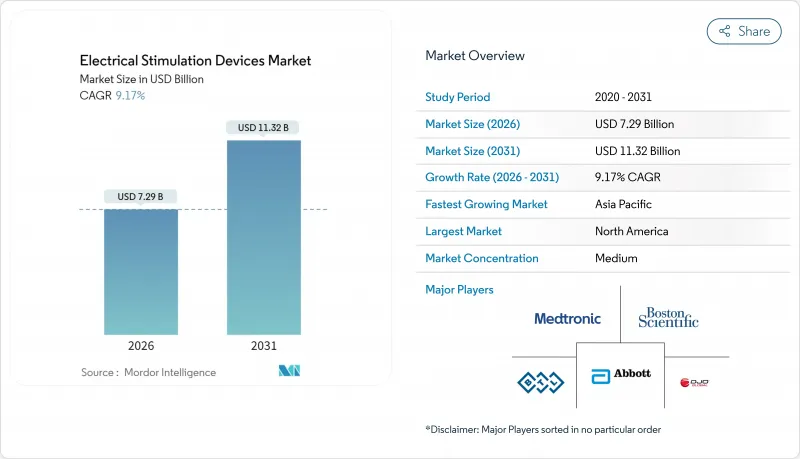

세계의 전기 자극 장치 시장은 2025년 66억 8,000만 달러로 평가되었으며, 2026년 72억 9,000만 달러에서 2031년까지 113억 2,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 9.17%로 예상됩니다.

인공지능과 바이오일렉트로닉스의 융합으로 인해 전기 자극 장치 시장은 증상이 아니라 근본 원인에 초점을 맞춘 예방적이고 고도로 개별화된 신경학적 치료로 진화하고 있습니다. 이미 수익의 51.34%를 차지하는 척수 자극 장치가 성장의 기반을 유지하는 한편, 심부 뇌 자극 장치는 10.12%의 연평균 복합 성장률(CAGR)로 다른 카테고리를 능가하고 있습니다. 병원은 여전히 주요 임상 현장이며, 48.21%의 점유율을 차지하고 있지만, 웨어러블 시스템의 보급 확대에 의해 재택치료 분야에서 채용이 CAGR 10.29%로 증가하고 있습니다. 지역별로는 북미가 수익의 42.98%를 차지하고 있으며, 유리한 상환제도와 효율적인 승인 프로세스에 지지되고 있습니다. 한편, 아시아태평양은 규제 현대화에 의해 시장에 장치 투입이 가속되고, CAGR 10.04%로 가장 급속하게 확대하고 있습니다. 업계 리더가 차별화를 도모하기 위해, 수직 통합이나 AI를 활용한 폐쇄 루프형 혁신을 전개하는 중, 경쟁의 격화가 진행되고 있습니다.

약 5,000만 명의 미국인이 만성 통증으로 고통받고 있으며 연간 6,350억 달러의 경제적 부담을 낳고 있습니다. 이 상황은 지불자에게 비용 효율적인 비 오피오이드 요법의 우선 순위를 촉구합니다. 고령화가 진행됨에 따라 수요가 더욱 높아지고, 세계 근골격계 질환은 2030년까지 25% 증가할 것으로 예측되고 있습니다. 전기 자극 장치는 평생 치료 비용을 줄이고 의존 위험을 피하기 위해 다각적 통증 프로그램의 첫 번째 선택 치료로 자리 매김되었습니다. 말초신경 자극 요법은 환자 1인당 연간 3만 221달러의 순 절약 효과, 3년간 9만 3,685달러의 누적 절약효과를 가져와 경제적 우위를 뒷받침하고 있습니다. 의료 시스템에서는 통증 관리를 증상 억제에서 신경 경로 조절로 전환하기 위해 표준 프로토콜에 대한 바이오 일렉트로닉 요법의 통합이 진행되고 있습니다.

세계 10억 명 이상이 신경질환으로 고통받고 있으며 유럽에서는 120만 명의 파킨슨병 환자가 심부 뇌 자극 요법의 대상이 되고 있습니다. 큰 우울증 장애 환자의 약 30%가 약물 저항성 증상을 보이고 경두개 자기 자극 요법과 미주 신경 자극 요법의 적용 기회가 확대되고 있습니다. 뇌졸중 재활에 대한 수요가 증가하는 경향이 있으며, 미국에서는 연간 79만 5천명이 뇌졸중을 경험하고 있습니다. 2025년 2월 미국 식품의약국(FDA)이 Medtronic의 BrainSense Adaptive 심부 뇌 자극 장치를 승인한 것은 정밀 신경 조절에 대한 규제당국의 지원 강화를 보여줍니다. 미주 신경 자극 요법과 체계적인 재활을 조합하면 최소 1년간 지속되는 기능적 개선을 얻을 수 있어 장기적인 가치가 입증됨과 동시에 시장 도입 전망이 향상되고 있습니다.

유럽연합의 의료기기 규칙에 따라 대기업 OEM 업체의 컴플라이언스 비용은 5,000만 유로를 넘어 중소기업에서는 비례하여 더욱 증가하여 제품 출시가 18-24개월 지연되고 있습니다. 중국 국가약품감독관리국은 2023년 1만 2,213건의 의료기기 신청을 처리했으며, 25.4% 증가로 인력 부족과 심사 기간 연장이 일어났습니다. 제안된 개혁안에서는 원산국 승인제도가 폐지되는 한편, 공동책임규칙이 추가되어 시장 진입이 복잡화되고 있습니다. 일본의 의약품 의료기기종합기구(PMDA)는 특정 신경조절 기기에 첨단 의료기기의 감독을 적용하여 임상적 증거의 요구를 강화하고 있습니다. FDA와 EMA 간의 데이터 요구사항이 다르기 때문에 조화는 불완전한 상태로 유지되며, 장치 개발자는 병렬로 여러 규제 프로세스를 수행할 수 없으며 유효한 특허 기간이 단축되는 압력이 되고 있습니다.

척수 자극 요법은 확립된 상환 제도와 풍부한 임상 증거를 배경으로 2025년 시점에서 매출의 50.82%를 유지했습니다. 심부 뇌 자극 요법은 규모가 작지만, BrainSense와 같은 적응형 시스템이 세계의 승인을 얻는 가운데, 2031년까지 연평균 복합 성장률(CAGR) 9.88%로 가장 빠르게 성장할 것으로 전망됩니다. 천골 신경 자극 요법은 요실금 치료 분야에서 꾸준한 성장을 계속하고 있으며, 미주 신경 자극 요법은 간질 치료에서 우울증과 뇌졸중 회복 치료로 적용 범위를 확대하고 있습니다. 경피적 전기신경자극(TENS)과 기능적 전기자극(FES)과 같은 소규모 카테고리는 재택의료 채용 확대로 점유율을 늘리고 있습니다. 중국에서 진행 중인 침습적 브레인 컴퓨터 인터페이스(BCI) 테스트는 하이브리드 신경 자극 플랫폼의 새로운 가능성을 보여줍니다.

지속적인 척수 자극(SCS) 장치에 유도 복합 동작 전위 모니터링의 지속적인 통합은 지속적인 통증 완화를 실현하고 1년후 환자 만족도는 92%에 도달했습니다. 말초 신경 자극은 단기간의 프로토콜에서 어깨 통증의 지속적인 개선이 확인되었습니다. 각 혁신은 경쟁 압력을 높이고 있으며, 제조업체들은 부품 원가를 관리하면서 적응 제어와 클라우드 분석의 통합을 경쟁하고 있습니다.

통증관리 분야는 2025년 매출액의 65.72%를 차지하며, 오피오이드 프리 대체요법에 대한 긴급 수요를 반영하고 있습니다. 그러나 요실금 및 골반 건강 분야는 비뇨기과 영역에서의 강력한 임상 증거와 미충족 요구를 배경으로 2031년까지 10.06%라는 높은 CAGR로 성장할 것으로 예측됩니다. 주요 골반 신경절에 대한 전기 자극은 방광 반사의 회복 제어를 나타내며 대상 환자층을 확대하고 있습니다. AI 기반 폐쇄 루프 시스템은 운동 장애 및 치료 저항성 우울증에 대한 치료를 최적화하고 정적 프로토콜에 비해 효율성을 높입니다.

위마비 완화부터 체중 관리 지원까지 새롭게 대두하는 소화기 및 대사 영역에서의 응용은 지금까지 충분히 커버되지 않았던 질환 영역을 개척해, 전기 자극 장치 시장 범위를 확대하고 있습니다.

북미는 종합적인 상환 제도, 확립된 임상 전문 지식 및 상업화를 가속화하는 FDA의 혁신적인 장치 프로그램을 통해 2025년 수익의 42.45%를 차지했습니다. 이개 미주 신경 자극 요법에 대한 HPCPS 코드의 추가로 안정적인 현금 흐름이 강화되고, 오피오이드 위기에 의해 비 약물 치료에 의한 통증 관리가 정책 과제로 지속적으로 다루어지고 있습니다. 보스턴, 미네아폴리스, 샌프란시스코 베이 지역에 집중하는 R&D 거점에서는 OEM 제조업체, 대학 병원, 벤처 캐피탈이 협력하여 제품의 반복적인 개발 사이클을 가속화하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 9.81%로 가장 급속한 진전을 기록하고 있습니다. 중국국가약품감독관리국은 2023년 1만 2,213건의 의료기기 신청을 처리하고 원산지 증명을 폐지하는 법안 초안에 따라 해외 기업의 등록기간 단축이 기대됩니다. 정부 주도의 고적층 제조 클러스터에 대한 투자와 고령화 사회가 결합되어 첨단 신경조절 기술에 대한 수요를 촉진하고 있습니다. 일본의 의약품 의료기기 종합기구(PMDA)는 엄격하면서도 투명성이 높은 심사 체제에 의해 의료기기의 품질을 높게 유지하고 있어, 이것이 3차 의료시설에서의 조기 도입을 촉진하고 있습니다. 상하이에서 진행 중인 브레인 컴퓨터 인터페이스(BCI) 임상시험은 차세대 인터페이스에 의한 기존 플랫폼의 비약적 진화를 목표로 하는 지역의 의욕을 돋보이게 하고 있습니다.

유럽에서는 꾸준한 성장이 지속되고 있습니다. 의료기기규칙(MDR)은 컴플라이언스의 복잡성을 늘리는 한편 환자의 신뢰를 높이고 있습니다. 독일에서는 견실한 국민보험제도에 힘입어 정신과 치료에서 반복경두개 자기자극요법의 도입이 확대되고 있습니다. 프랑스와 이탈리아는 가치 기반 조달을 활용하여 만성 통증 치료 경로에 척수 자극 요법을 통합하고 있습니다. 동유럽 시장에서는 기능적 전기 자극 모듈을 포함한 뇌졸중 재활에 대한 EU 자금 지원으로 접근이 확대되고 있습니다. 브라질과 사우디아라비아가 의료기기 승인을 효율화하고 칠레가 세계의 임상 네트워크와 연계한 심부뇌 자극 연구 거점으로서의 지위를 확립하는 가운데 라틴아메리카, 중동, 아프리카에서는 새로운 기회가 열리고 있습니다.

The electrical stimulation devices market was valued at USD 6.68 billion in 2025 and estimated to grow from USD 7.29 billion in 2026 to reach USD 11.32 billion by 2031, at a CAGR of 9.17% during the forecast period (2026-2031).

The combination of artificial intelligence and bioelectronics is pushing the electrical stimulation devices market toward proactive, highly personalized neurological care that targets root causes rather than symptoms. Spinal cord stimulation devices, which already account for 51.34% of revenue, continue to anchor growth, while deep brain stimulation devices outpace all other categories at a 10.12% CAGR. Hospitals remain the principal clinical setting with a 48.21% share, yet stronger adoption of wearable systems is propelling home-care uptake at a 10.29% CAGR. Regionally, North America holds 42.98% of revenue, supported by favorable reimbursement and streamlined approvals, whereas Asia-Pacific expands fastest at a 10.04% CAGR as regulatory modernization accelerates device launches. Competitive intensity is climbing as industry leaders deploy vertical integration and AI-enabled closed-loop innovations to secure differentiation.

Around 50 million Americans live with chronic pain, generating an annual economic burden of USD 635 billion that encourages payers to prioritize cost-effective, non-opioid therapies. Aging populations intensify demand because global musculoskeletal disorders are expected to rise 25% by 2030. Electrical stimulation devices reduce lifetime treatment costs and avoid addiction risks, positioning the electrical stimulation devices market as a first-line intervention in multidisciplinary pain programs. Peripheral nerve stimulation delivers net annual savings of USD 30,221 per patient and cumulative savings of USD 93,685 over three years, reinforcing its economic appeal. Health systems increasingly integrate bioelectronic therapy with standard protocols to shift pain management from symptom suppression to neural pathway modulation.

More than 1 billion people worldwide suffer from neurological disorders, and 1.2 million European patients with Parkinson's disease qualify for deep brain stimulation. Roughly 30% of individuals with major depressive disorder exhibit drug-resistant symptoms, widening the addressable opportunity for transcranial magnetic stimulation and vagus nerve stimulation. Stroke rehabilitation demand is rising as 795,000 Americans experience strokes annually. The FDA approval of Medtronic's BrainSense Adaptive deep brain stimulation in February 2025 signals stronger regulatory support for precision neuromodulation . Vagus nerve stimulation paired with structured rehab produces sustained functional gains for at least one year, validating long-term value and boosting market adoption prospects .

The European Union's Medical Device Regulation raised compliance expenditures above EUR 50 million for large OEMs and proportionately more for smaller firms, delaying product launches by 18-24 months. China's National Medical Products Administration processed 12,213 device applications in 2023, a 25.4% rise that stretched staff and extended reviews. Proposed reforms abolish country-of-origin approvals yet add joint-liability rules, complicating market entry. Japan's Pharmaceuticals and Medical Devices Agency applies advanced-therapy oversight to certain neuromodulation devices, increasing clinical evidence demands. Divergent data requirements between the FDA and EMA keep harmonization incomplete, pressuring device developers to run parallel regulatory tracks that shorten effective patent life.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Spinal cord stimulation retained 50.82% of revenue in 2025, underpinned by established reimbursement and extensive clinical evidence. Deep brain stimulation, though smaller, grows fastest at a 9.88% CAGR through 2031 as adaptive systems like BrainSense secure global approvals. Sacral nerve stimulation continues steady growth for incontinence therapy, while vagus nerve stimulation broadens beyond epilepsy into depression and stroke recovery. Smaller categories such as transcutaneous electrical nerve stimulation and functional electrical stimulation secure share gains through home-care adoption. Invasive brain-computer interface trials under way in China showcase the next frontier for hybrid neurostimulation platforms.

Continued integration of evoked compound action potential monitoring in SCS devices delivers sustained pain relief with 92% one-year patient satisfaction. Peripheral nerve stimulation validates short-duration protocols yielding durable shoulder-pain improvements. Each innovation increases competitive pressure as manufacturers race to embed adaptive control and cloud analytics while controlling bill of materials costs.

Pain management contributed 65.72% of revenue in 2025, reflecting urgent demand for opioid-free alternatives. Incontinence and pelvic health, however, grow a faster 10.06% CAGR to 2031 on the back of stronger clinical evidence and unmet need in urology. Electrical stimulation of the major pelvic ganglion shows restorative control of bladder reflexes, widening the addressable patient pool. AI-based closed-loop systems optimize therapy for movement disorders and treatment-resistant depression, boosting efficacy versus static protocols.

Emerging gastrointestinal and metabolic uses, from gastroparesis relief to weight-control support, widen the scope of the electrical stimulation devices market by tapping previously underserved conditions.

The Electrical Stimulation Devices Market Report is Segmented by Device Type (Deep Brain Stimulation, Spinal Cord Stimulation, and More), Application (Pain Management, Musculoskeletal Disorders, and More), End-User (Hospitals, Ascs, Home-Care, Others), Product Portability (Implantable, External), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

North America delivered 42.45% of 2025 revenue due to comprehensive reimbursement, established clinical expertise, and the FDA's Breakthrough Devices Program that expedites commercialization. Recent HCPCS code additions for auricular vagus nerve stimulation bolster stable cash flows, and the opioid crisis keeps non-pharmacological pain management on policy agendas. Concentrated R&D hubs around Boston, Minneapolis, and the San Francisco Bay Area accelerate iterative product cycles by linking OEMs, academic hospitals, and venture capital.

Asia-Pacific records the quickest advance with a 9.81% CAGR through 2031. China's National Medical Products Administration processed 12,213 device filings in 2023, and draft legislation abolishing country-of-origin proof can shorten foreign registration. Government-backed investment in high-end manufacturing clusters, along with an aging population, fuels demand for advanced neuromodulation. Japan's rigorous but transparent Pharmaceuticals and Medical Devices Agency keeps device quality high, which encourages early adoption in tertiary centers. Ongoing BCI trials in Shanghai highlight regional aspirations to leapfrog established platforms with next-generation interfaces.

Europe sustains measured growth. The Medical Device Regulation increases compliance complexity yet raises patient confidence. Germany expands repetitive transcranial magnetic stimulation adoption for psychiatric care, supported by solid national insurance. France and Italy leverage value-based procurement to integrate spinal cord stimulation into chronic pain pathways. Eastern European markets widen access with EU funding for stroke rehabilitation that includes functional electrical stimulation modules. Latin America, the Middle East, and Africa open new opportunities as Brazil and Saudi Arabia streamline device approvals, and Chile positions itself as a deep brain stimulation research site linked to global clinical networks.