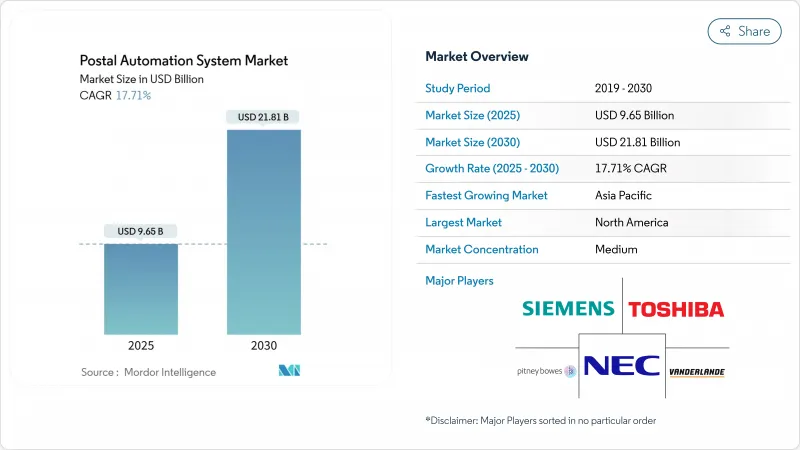

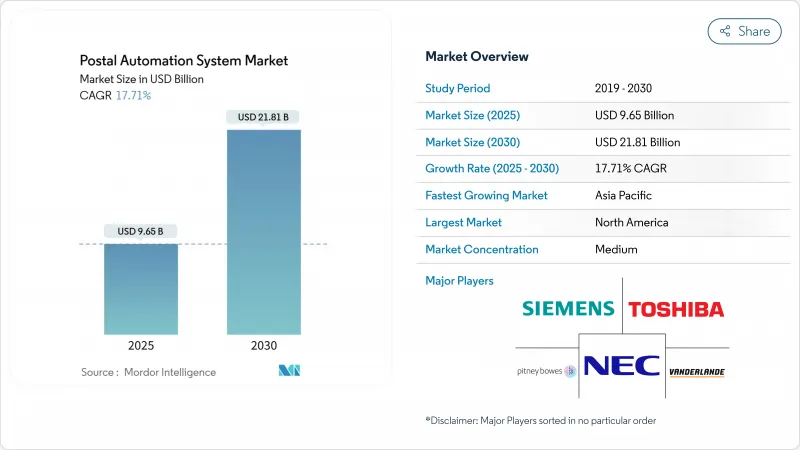

우편 자동화 시스템 시장 규모는 2025년에 96억 5,000만 달러가 되고, CAGR 17.71%를 나타내 2030년에는 218억 1,000만 달러에 달할 것으로 예상되고 있습니다.

이 성장은 국경을 넘어 전자상거래 수요 증가, 우편 근대화 프로그램, 자동화를 경제적으로 매력적으로 만드는 지속적인 인건비 압력을 반영합니다. 북미와 유럽이 최대 설치 대수를 차지하고 있는 것은 공공 부문에 의한 대규모 투자와 차세대 기기에 유리한 에너지 효율 규제 때문입니다. 아시아태평양은 중국 우정, Cainiao, 일본 우정이 농촌 및 도시 지역의 자동화 프로젝트를 가속화하고 배달 시간을 단축하고 수작업으로 인건비 절감을 실현하여 급성장하는 지역입니다. 구매의 중심은 계속 하드웨어이지만, 수요는 서비스 계약이나 성능 리스크를 공급자에게 전가하는 로보틱스 아즈아 서비스 모델로 이동하고 있습니다. Vanderlande의 Siemens Logistics 인수와 BlueCrest의 Fluence Automation 인수는 하드웨어와 소프트웨어 통합을 통한 규모의 이점을 재정의하고 있습니다.

국경을 넘는 전자상거래 소포는 증가의 일도를 따르고 있으며, 1개당 매출이 감소하더라도 미국의 소포 취급량은 2023년에는 217억개에 달했고, 효율적인 하이 스루풋 자동화의 필요성이 부각되었습니다. 아마존 로지스틱스는 취급 개수로 UPS를 쫓아, 속도에 최적화된 분류 네트워크가 시장 우위를 가져온다는 것을 증명했습니다. 중국 우정과 Cainiao는 운송장을 자동으로 읽는 비전 유도 시스템을 도입하여 농촌의 인건비를 낮추고 도시와 농촌의 서비스 격차를 줄였습니다. 자동화를 통해 인력을 늘리지 않고 대량 처리가 가능해졌으므로 운영자는 현재 1개당 비용보다 처리 밀도를 강조하고 있습니다.

USPS는 400억 달러를 투자하여 네트워크를 쇄신하여 하루의 소포처리 능력을 6,000만개까지 확대함과 동시에 우편물과 소포의 흐름을 정비하여 신뢰성을 향상시켰습니다. 얼룩말 테크놀로지스 프린터, 새로운 원격 전송 시스템, USPS Ship으로의 전환은 물리적 자동화를 지원하는 디지털 레이어를 강화합니다. 공급업체는 USPS 사양을 활용하여 유사한 솔루션을 전 세계적으로 확장하고 다른 지역에서의 채택을 가속화하는 기술 파급을 창출하고 있습니다.

개발 도상 우체국은 최신 분류기에 쉽게 연결할 수없는 구식 플랫폼에서 운영되는 경우가 많으며 프로젝트 일정을 늘리고 비용을 늘리고 있습니다. IMF는 물류 병목 현상을 반영한 결제 레일에도 비슷한 과제가 있음을 지적하며 고급 자동화가 확대되기 전에 기본적인 디지털 인프라가 필요하다는 점을 강조합니다.

하드웨어로 인한 우편물 분류 시스템 시장 규모는 자본 집약적인 컨베이어, 센서, OCR에 대한 투자를 반영하여 2024년에는 62억 달러에 달했습니다. 2030년까지 연평균 복합 성장률(CAGR) 20.8%를 나타낼 것으로 예측됩니다. 소프트웨어 라이선스는 이 두 개의 교량을 통해 라이브 퍼포먼스 대시보드, 루트 최적화, 자산 수명을 늘리는 예지 보전을 가능하게 합니다.

업적 기반 계약을 채택하여 Quadient와 BlueCrest는 처리량 수준과 가동 시간을 보장하고 위험을 공급업체로 옮깁니다. 이와 같은 약정은 중견 사업자도 선행 투자 없이 고급 기능을 이용할 수 있게 되어 우편물 분류 시스템 시장의 대응 가능한 기반이 넓어지고 있습니다. 하드웨어 지출은 여전히 크지 만 수익 구성 분석에 따르면 정액제 및 정렬별 지불 모델이 확대됨에 따라 2030년까지 서비스가 그 차이를 줄일 수 있습니다.

소포 분류기는 2024년에는 우편물 분류 시스템 시장 점유율의 42%를 차지하며, 이는 오랜 실적을 가진 크로스벨트와 틸트 트레이의 설계가 강점이 되었습니다. 그러나 성장세는 자동반송차와 협동로봇에 있으며 2030년까지의 CAGR은 24.1%를 나타낼 전망입니다. 로봇 공학은 고정 궤도의 제약을 제거하여 운영자가 계절 피크를 관리하기 위해 허브를 신속하게 재구성할 수 있도록 합니다.

La Poste의 데이터에 따르면 우편물 매출에서 차지하는 비율은 2010년의 52%에서 2024년에는 15.8%로 줄어들었고, 서한 중심의 기계에서 소포 중심의 로봇으로의 구조적 변화를 보여줍니다. 컬러 페이서 캔슬러 유닛은 대량의 우표를 처리하는 부문으로 틈새를 유지하고 있지만, AGV, 비전 시스템, 코딩 모듈을 통합한 하이브리드 사이트는 뛰어난 유연성을 제공합니다. 공급업체는 현재 플릿 관리 소프트웨어를 모바일 로봇에 번들로 제공하고 있으며 도시 허브의 부동산 제한으로 제한되는 운영자의 ROI를 향상시키고 있습니다.

북미는 시설 업그레이드에 400억 달러를 투입하고 1일 배송 능력을 6,000만개까지 끌어올리는 USPS의 'Delivering for America' 프로그램을 통해 세계 매출을 선도하고 있습니다. 캐나다도 마찬가지이며 토론토, 밴쿠버 등 대도시 허브의 노동력 부족을 완화하기 위해 로봇을 채용하고 있습니다. 안정적인 규제 체제와 예측 가능한 수하물 흐름이 투자 회수 기간을 단축하고 공급업체가 이 지역에서 조기에 제품을 배포하는 것을 선호하는 경향이 커지고 있습니다.

유럽은 에너지 효율이 높은 기기를 우선하여 교체 사이클을 가속화하는 넷제로 산업법에 힘입어 견조한 성장을 이루고 있습니다. 독일에서는 우편법이 개정되어 독일 포스트가 유연하게 경로를 최적화할 수 있게 되는 한편, DHL은 우편으로 63%, 소포로 40% 시장 점유율을 획득해, 전국적인 자동화에 스케일 메리트를 가져오고 있습니다. 영국에서는 DHL 전자상거래와 에브리의 합병이 승인되어 연간 10억 개 이상의 소포를 처리하는 통합 네트워크가 형성되고 추가 자동화 투자가 이루어집니다.

아시아태평양은 중국 우정과 Cainiao의 자동화 전개와 운전자 부족에 대한 대책으로서 일본이 제안한 500㎞의 자동화 컨베이어 네트워크에 추진되어 가장 빠른 CAGR을 나타낼 전망입니다. 한국은 선진적인 통신 인프라를 활용해 RFID 대응의 구분을 전개하고, 인도는 프로젝트·비용을 인상하는 기기 관세와 격투하고 있습니다. 인구가 분산된 호주에서는 장거리 수송 능력을 유연하게 확장할 수 있는 로봇 공학에 대한 관심이 높아지고 있습니다.

라틴아메리카는 변동이 있습니다. 멕시코는 USMCA의 근접성으로부터 혜택을 누리고 북부 허브에서 자동화를 정당화하는 국경을 넘어 소포의 흐름을 이끌고 있습니다. 브라질의 컴플라이언스 프로그램은 전자상거래의 성장을 지원하지만, 수입 자동화에 대한 관세는 여전히 총 소유 비용을 늘리고 있습니다. 아르헨티나의 경제 변동은 투자 결정주기를 늘리고 하이 엔드 솔루션 시장 침투를 제한합니다.

중동 및 아프리카는 아직 개발 도상이지만 유망합니다. 걸프 국가들은 컴팩트한 모듈식 시스템을 필요로 하는 도시형 마이크로플루필먼트 시설에 투자하고 있지만, 아프리카에서는 레거시 IT 장애물이 도입을 늦추고 있습니다. 우편 인프라의 현대화를 목표로 한 국제 원조 프로그램은 특히 스마트폰 주도 상거래가 주요 도시 회랑에서 확대됨에 따라 미래 수요를 파악할 수 있습니다.

The postal automation system systems market size was valued at USD 9.65 billion in 2025 and is forecast to grow at a 17.71% CAGR, reaching USD 21.81 billion by 2030.

Growth reflects rising cross-border e-commerce demand, postal modernization programs and sustained labor cost pressures that make automation economically attractive. North America and Europe account for the largest installed base because of sizeable public-sector investments and energy-efficiency regulations that favor next-generation equipment. Asia-Pacific is the fastest-growing region as China Post, Cainiao and Japan Post accelerate rural and urban automation projects, shortening delivery times and lowering manual labor costs. Hardware continues to dominate purchases, yet demand is shifting toward service contracts and robotics-as-a-service models that transfer performance risk to suppliers. Competitive intensity is moderate, with Vanderlande's purchase of Siemens Logistics and BlueCrest's acquisition of Fluence Automation redefining scale advantages in integrated hardware-software offerings.

E-commerce parcels crossing borders continue to climb, with US parcel volumes reaching 21.7 billion in 2023 even as revenue per piece declined, underscoring the need for efficient high-throughput automation. Amazon Logistics overtook UPS on volume, proving that speed-optimized sorting networks confer a market edge. China Post and Cainiao lowered rural labor costs by deploying vision-guided systems that read waybills automatically, narrowing the urban-rural service gap. Operators now focus on processing density rather than cost per piece, since automation enables higher volumes without proportional staffing increases.

USPS committed USD 40 billion to revamp its network, expanding daily package capacity to 60 million items and aligning mail and parcel flows for improved reliability. Zebra Technologies printers, a new remote forwarding system, and the USPS Ship migration reinforce the digital layer underpinning physical automation. Suppliers leverage USPS specifications to scale similar solutions globally, creating a technology spill-over that accelerates adoption in other regions.

Developing posts often run on ageing platforms that cannot easily connect to modern sorters, extending project timelines and raising costs. The IMF highlights similar challenges in payment rails that mirror logistics bottlenecks, stressing a need for basic digital infrastructure before advanced automation can scale.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The mail sorting systems market size attributed to hardware reached USD 6.2 billion in 2024, reflecting capital-intensive conveyor, sensor and OCR investments. Services produced a smaller revenue base but are projected to grow at a 20.8% CAGR to 2030 as operators favor managed outcomes over outright equipment ownership. Software licenses bridge the two, enabling live performance dashboards, route optimization and predictive maintenance that extend asset life.

Adoption of outcome-based contracts shifts risk to vendors, with Quadient and BlueCrest guaranteeing throughput levels and uptime. These arrangements allow even mid-tier operators to access sophisticated capabilities without upfront capital, broadening the addressable base for the mail sorting systems market. Hardware spending will remain sizeable, yet revenue mix analysis shows services closing the gap by 2030 as subscription and pay-per-sort models scale.

Parcel sorters commanded 42% of the mail sorting systems market share in 2024 on the strength of long-established cross-belt and tilt-tray designs. Growth momentum, however, lies with automated guided vehicles and collaborative robots that post a 24.1% CAGR through 2030. Robotics removes fixed-track constraints, letting operators re-configure hubs quickly to manage seasonal peaks.

La Poste's data show mail contributing only 15.8% of revenue in 2024, down from 52% in 2010, signaling a structural shift away from letter-centric machinery toward parcel-centric robotics. Culler-facer-canceller units retain a niche in high-volume philatelic segments, but hybrid sites integrating AGVs, vision systems and coding modules deliver superior flexibility. Vendors now bundle fleet-management software with mobile robots, improving ROI for operators constrained by real estate limits in urban hubs.

The Postal Automation Systems Market Report is Segmented by Solution (Hardware, Software, Services), Technology (Parcel Sorters, Letter Sorters, AGV and Robotics, and More), Application (Parcel Sorting, Mail Sorting, Last-Mile Automation, and More), End User (Postal Operators, CEP Companies, E-Commerce Centers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America leads global revenue owing to the USPS "Delivering for America" program that injects USD 40 billion into facility upgrades and boosts daily capacity to 60 million packages. Canada follows a similar trajectory, adopting robotics to mitigate labor shortages in large urban hubs such as Toronto and Vancouver. Stable regulatory regimes and predictable parcel flows shorten payback periods, reinforcing vendor preference for early product rollouts in the region.

Europe contributes robust growth underpinned by the Net Zero Industry Act, which prioritizes energy-efficient equipment and accelerates replacement cycles. Germany's updated postal law gives Deutsche Post flexibility to optimize routes, while DHL holds 63% mail and 40% parcel market shares, creating economies of scale for nationwide automation. The United Kingdom's approval of the DHL eCommerce-Evri merger forms a combined network processing more than 1 billion parcels annually, anchoring further automation investments.

Asia-Pacific records the fastest CAGR, propelled by China Post and Cainiao's automation deployments and Japan's proposed 500-kilometer automated conveyor network to counter driver shortages. South Korea leverages advanced telecom infrastructure to roll out RFID-enabled sortation, while India wrestles with equipment tariffs that raise project costs. Australia's dispersed population boosts interest in robotics that can flexibly scale capacity across long distances.

Latin America delivers uneven performance. Mexico benefits from USMCA proximity, attracting cross-border parcel flows that justify automation in northern hubs. Brazil's compliance program supports e-commerce growth, yet tariffs on imported automation remain a drag on total cost of ownership. Argentina's economic volatility prolongs investment decision cycles, limiting market penetration for high-end solutions.

The Middle East and Africa remain nascent but promising. Gulf states invest in urban micro-fulfillment facilities that demand compact modular systems, while Africa faces legacy IT hurdles that slow deployments. International aid programs targeting postal infrastructure modernization could unlock future demand, especially as smartphone-led commerce expands across major urban corridors.