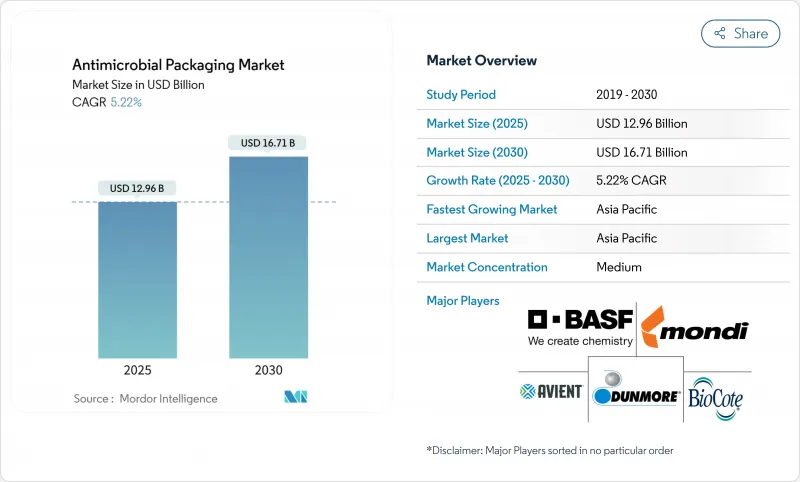

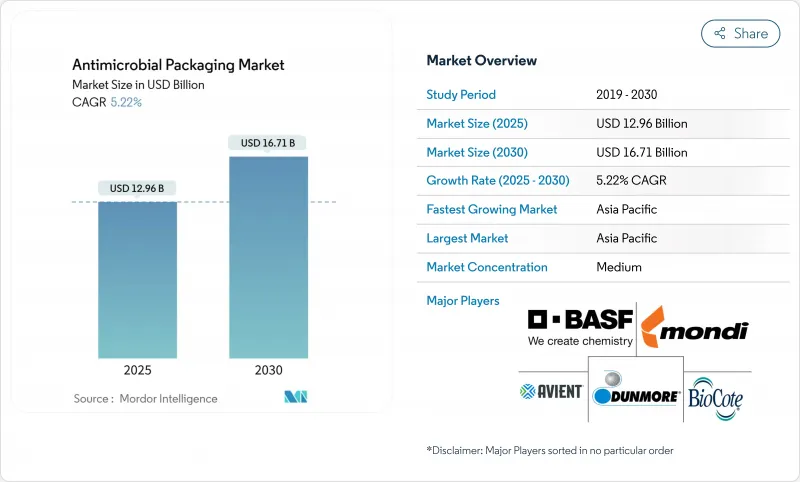

현재의 데이터에 따르면 항균 포장 시장은 2025년 129억 6,000만 달러로 평가되고, 2030년에는 167억 1,000만 달러에 이르며, CAGR 5.22%를 나타낼 것으로 예측됩니다.

수요는 보다 엄격한 식품 접촉 규제, PFAS 물질의 단계적 폐지 및 항균 기능을 주류 포장 요건으로 끌어올리는 기업의 지속가능성 의무화에 의해 추진되고 있습니다. 규제의 기운은 미생물의 효능과 환경적 신용의 균형을 맞추는 바이오의 항균제로 축발을 옮기는 계기가 되었습니다. 아시아태평양은 진화하는 위생법, 급성장하는 전자 식료품 부문, 급속한 콜드체인 업그레이드로 계속 성장의 지점이되고 있습니다. 방출 제어형 나노은 필름, 천연 화합물의 통합, 스마트 센서와의 조합 등의 기술 혁신이 병행하여 진행되어 경쟁상의 기술 혁신의 우선 순위가 변화하고 있습니다. 그 결과 항균 포장 시장은 소재, 기술 및 최종 용도 분야에 걸쳐 다양화를 계속하고 있습니다.

식품 접촉 모니터링의 세계 리셋은 항균 솔루션의 흡수를 촉진합니다. 미국 인간 식품 프로그램은 현재 레거시 PFAS의 신고를 재평가하고 있으며, 보다 안전한 대체 항균제에 활로를 발견하려고 하고 있습니다. 유럽 기관은 동시에 리스테리아균과 같은 난분해성 병원체에 경고를 내고 가공업자에게 미생물 장벽을 추가하는 포장의 채용을 촉구하고 있습니다. 이러한 의무화 흐름은 안전성과 "청정 라벨"에 대한 기대를 모두 충족시키는 천연 유래 항균제에 대한 투자를 가속화합니다. 효능과 재활용성을 증명할 수 있는 공급자를 위해, 규제 강화는 항균 포장 시장의 명확한 성장 여지를 가져옵니다.

온라인 식료품의 폭발적인 수요는 온도 관리 물류에 전례없는 스트레스를줍니다. 아시아태평양에서는 수천 개의 마이크로 완성 창고가 마지막 원 마일의 긴 여행으로 품질을 유지하는 포장이 필요합니다. 냉장 기능이 저하되면 항균층이 중요한 2차 안전 장치로 작용하여 부패의 클레임을 줄입니다. 새로운 스마트 팩은 시간-온도 표시기와 항균제를 통합하여 플랫폼이 신선도를 데이터를 기반으로 관리할 수 있도록 합니다. 당일 배송 범위가 축소됨에 따라 소매업체는 특히 위험이 높은 신선 식품에 대한 항균 기능을 조달의 전제조건으로 만드는 경향이 커지고 있습니다. 이러한 전자상거래의 기세는 항균 포장 시장의 단기적인 이익을 견고하게 만듭니다.

유럽의 살생물제 제품 규정은 나노은과 나노구리가 식품과 접촉하는 채널에 들어가기 전에 철저한 서류를 제출해야 합니다. 식품과 사료에 직접 적용이 허가된 나노금속은 아직 없기 때문에 기술 혁신자들은 수년에 걸쳐 독물학 프로그램에 직면하고 있습니다. 광범위한 데이터 요구는 시장 출시까지의 시간을 늘리고 일부 기업들은 보다 신속하게 규제 경로를 클리어할 수 있는 식물 유래의 활성 물질로 축발을 옮기도록 촉구하고 있습니다. 이 억제 효과는 항균 포장 시장에서 금속 솔루션의 단기 성장을 좁히고 있습니다.

현재, 항균 포장 시장 규모를 지지하고 있는 것은 플라스틱이며, 확장 가능한 압출 라인과 견고한 배리어 성능에 의해 2024년에는 60.32%의 매출 점유율을 획득했습니다. 그러나 2030년까지 완전한 재활용을 의무화하는 정책목표로 인해 바이오폴리머의 CAGR은 8.32%를 나타낼 것으로 예상되며, 재료 중에서 가장 빠릅니다. 키토산과 에센셜 오일로 강화된 폴리유산과 폴리하이드록시알카노에이트의 블렌드는 현재 석유화학 필름에서 발견되는 미생물의 멸종률과 비교할 수 있으며 동시에 퇴비화가 가능한 사용된 경로를 지원합니다.

항균력을 희생하지 않고 바이오폴리머의 단부재를 회수하는 폐쇄 루프 회수 방식에 대한 투자가 가속화되고 있습니다. 또한 페놀이 풍부한 다당류로 코팅된 종이 섬유는 재활용성을 유지하고 폭넓은 세균 억제 효과를 발휘한다는 조사 결과도 있습니다. 이러한 첨단 패키징은 바이오폴리머가 플라스틱 점유율을 낮추고 항균 포장 시장 전반에 걸쳐 공급업체의 포트폴리오를 재구성하게 합니다.

유기산은 2024년 매출의 45.63%를 차지했으며, 그 이유는 규제상의 친숙함과 비용 효율성에 있었습니다. 그러나 박테리오신과 효소는 CAGR 7.53%로 가속화되어 소비자가 인식하기 쉽고 라벨에 친숙한 첨가제로 전환하고 있음을 반영하고 있습니다. 박테리오신과 나노은을 조합한 시너지 시스템은 금속 투여량을 억제하면서 살균 효율을 두배로 합니다.

사이클로덱스트링케이지로 보호된 에센셜 오일은 통제된 증기 방출로 수분이 많은 농산물의 부패 생물을 억제합니다. 살생물제에 대한 감시가 강화되는 가운데, 식물 유래의 약제는 전략적 가중치를 늘리고 있으며, 천연활성제는 항균 포장 시장에서 미래의 차별화에 있어 매우 중요하다고 자리잡고 있습니다.

항균 포장 시장은 소재별(플라스틱, 바이오폴리머, 기타), 항균제 유형별(유기산, 박테리오신과 효소, 기타), 기술별(활성 표면 코팅, 기타), 팩 유형별(파우치와 가방, 필름과 랩 등), 최종 사용자 산업별(음식, 헬스케어 및 의료기기, 기타), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2024년 매출액에서 41.22%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR)로 최고 8.96%를 나타내 세계 선두에 위치할 것으로 전망됩니다. 중국의 식품안전법 개정과 인도의 FSSAI 위생규범은 미생물학적 안전대책을 의무화하고 있기 때문에 자본은 선진적인 팩으로 향하고 있습니다. 일본의 가공업자는 고급 수산물 수출품에 스마트 인디케이터와 방출 제어형 항균제를 추가해 단위 이익률을 높입니다. 항균제 내성에 대항하기 위한 지역 정부의 이니셔티브는 아시아태평양의 항균 포장 시장에 대한 영향력을 더욱 강화합니다.

유럽은 EU의 포장·용기 포장 폐기물 규제에 의해 리사이클 가능성과 리사이클 함량의 준수를 강제되어 그 궤적이 형성되고 있습니다. 독일과 프랑스는 바이오 활성제의 연구 개발을 선도하고, 지중해 연안의 수출업체는 국경을 넘어 농산물 출하 시 보존성을 확보하기 위해 항균 카톤을 도입하고 있습니다. BPR은 나노메탈의 전개를 늦추는 한편, 식물 유래의 혁신을 가속화하고, 유럽을 기술 리더십의 중심에 자리잡고 있습니다.

북미는 FDA의 감독과 견조한 헬스케어 수요에 힘입어 꾸준한 성장을 유지하고 있습니다. 미국은 보조금을 PFAS 대체품으로 옮기고 천연 활성제의 항균 포장 시장 규모를 간접적으로 밀어 올리고 있습니다. 캐나다 연구기관은 수산물 공급망을 대상으로 효소 칵테일을 주입한 셀룰로오스 기반 필름을 시험적으로 생산하고 있습니다. 멕시코는 니어 쇼어링 동향을 활용하여 국내 브랜드와 미국 소매업체를 대상으로 항균 파우치 생산을 확대합니다.

Current data indicate the antimicrobial packaging market is valued at USD 12.96 billion in 2025 and is forecast to reach USD 16.71 billion by 2030, expanding at a 5.22% CAGR.

Demand is propelled by stricter food-contact regulations, the phase-out of PFAS substances, and corporate sustainability mandates that elevate antimicrobial functionality to a mainstream packaging requirement. Regulatory momentum has sparked a pivot toward bio-based antimicrobial agents that balance microbial efficacy with environmental credentials. Asia-Pacific remains the fulcrum of growth, driven by evolving sanitation laws, a booming e-grocery sector, and rapid cold-chain upgrades. Parallel advances in controlled-release nano-silver films, natural compound integration, and smart-sensor pairing are reshaping competitive innovation priorities. As a result, the antimicrobial packaging market continues to diversify across materials, technologies, and end-use sectors.

The global reset of food-contact oversight is amplifying uptake of antimicrobial solutions. The United States Human Foods Program now reassesses legacy PFAS notifications, creating an opening for safer antimicrobial alternatives. European agencies simultaneously flag persistent pathogens such as Listeria monocytogenes, compelling processors to adopt packaging that adds an extra microbial barrier. These converging mandates accelerate investment in naturally-derived agents that fulfil both safety and "clean-label" expectations. For suppliers able to document efficacy and recyclability, regulatory tightening translates into clear growth runway within the antimicrobial packaging market.

Explosive demand for online groceries places unprecedented stress on temperature-controlled logistics. In Asia-Pacific, thousands of micro-fulfilment warehouses now require packaging that maintains quality over extended last-mile journeys. When refrigeration falters, antimicrobial layers serve as a critical secondary safeguard, reducing spoilage claims. Emerging smart packs pair time-temperature indicators with embedded antimicrobials, giving platforms data-driven control over freshness. As same-day delivery windows shrink, retailers increasingly make antimicrobial functionality a procurement prerequisite, particularly for high-risk perishables. This e-commerce momentum solidifies near-term gains for the antimicrobial packaging market.

Europe's Biocidal Products Regulation requires exhaustive dossiers before nano-silver or nano-copper can enter food-contact channels. With no nano-metal yet authorised for direct food or feed applications, innovators face multi-year toxicology programs. Wide-ranging data demands inflate time-to-market, prompting some firms to pivot toward plant-based actives that clear regulatory pathways more swiftly. The deterrent effect narrows near-term growth for metallic solutions inside the antimicrobial packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastics currently anchor the antimicrobial packaging market size, capturing 60.32% revenue share in 2024 due to scalable extrusion lines and robust barrier performance. Yet policy targets that mandate full recyclability by 2030 propel biopolymers to an 8.32% CAGR, the fastest among materials. Poly-lactic acid and polyhydroxyalkanoate blends enhanced with chitosan or essential oils now match microbial kill rates seen in petrochemical films while supporting compostable end-of-life routes.

Investment is accelerating in closed-loop collection schemes that recover biopolymer offcuts without sacrificing antimicrobial potency. Research also evidences that paper fibres coated with phenolic-rich polysaccharides retain recyclability and deliver broad-spectrum bacterial inhibition. These advances ensure biopolymers will continue eroding plastic share, reshaping supplier portfolios throughout the antimicrobial packaging market.

Organic acids command 45.63% of 2024 revenue owing to regulatory familiarity and cost efficiency. However, bacteriocins and enzymes accelerate at 7.53% CAGR, mirroring consumer migration to recognizable, label-friendly additives. Synergistic systems marry bacteriocins with nano-silver, doubling kill efficiency while curbing metal dosage.

Essential oils protected within cyclodextrin cages provide controlled vapor release that suppresses spoilage organisms in high-moisture produce. As biocide scrutiny intensifies, plant-derived agents gain strategic heft, positioning natural actives as pivotal to future differentiation in the antimicrobial packaging market.

Antimicrobial Packaging Market is Segmented by Material (Plastics, Biopolymers, and More), Antimicrobial Agent Type (Organic Acids, Bacteriocins and Enzymes, and More), Technology (Active Surface Coating, and More), Pack Type (Pouches and Bags, Films and Wraps, and More), End-User Industry (Food and Beverages, Healthcare and Medical Devices, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific tops the global leaderboard, holding 41.22% revenue in 2024 and registering the highest 8.96% CAGR to 2030. China's Food Safety Law amendments and India's FSSAI hygiene codes mandate microbiological safeguards that funnel capital toward advanced packs. Japanese converters add smart indicators and controlled-release antimicrobials to premium seafood exports, elevating unit margins. Regional government initiatives to counter antimicrobial resistance further incentivise adoption, reinforcing Asia-Pacific's pull on the antimicrobial packaging market.

Europe follows, its trajectory shaped by the EU Packaging and Packaging Waste Regulation that forces recyclability and recycled-content compliance. Germany and France spearhead R&D into bio-based actives, whereas Mediterranean exporters deploy antimicrobial cartons to secure shelf life during cross-border produce shipments. While the BPR slows nano-metal roll-outs, it simultaneously accelerates botanical innovation, keeping Europe central to technology leadership.

North America sustains steady gains anchored by FDA oversight and robust healthcare demand. The United States channels grant funding toward PFAS alternatives, indirectly uplifting antimicrobial packaging market size for natural actives. Canadian institutes pilot cellulose-based films infused with enzyme cocktails, targeting seafood supply chains. Mexico, leveraging near-shoring trends, scales antimicrobial pouch production for both domestic brands and US retailers.