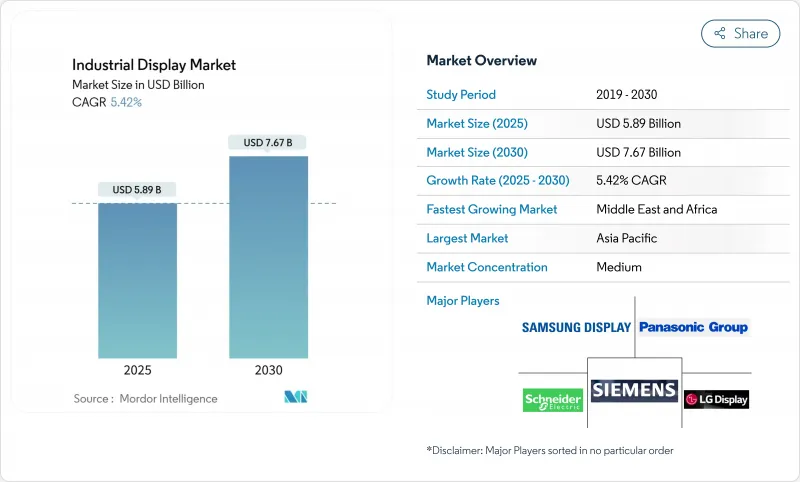

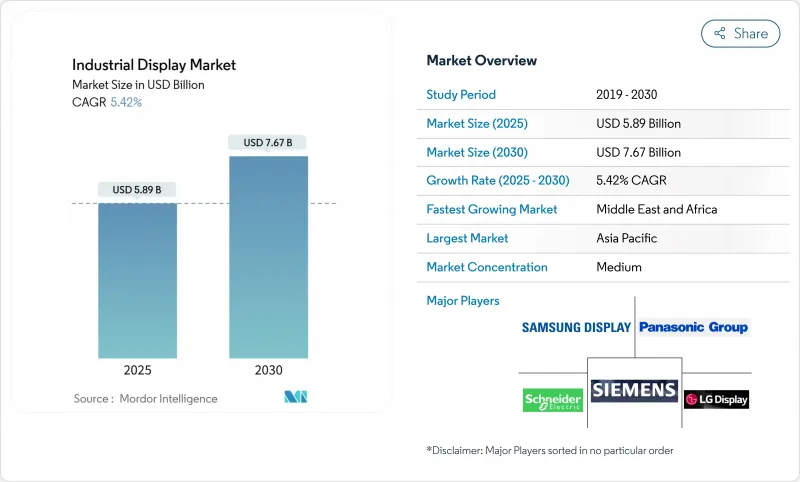

산업용 디스플레이 시장 규모는 2025년에 58억 9,000만 달러로 예측 기간 중 CAGR은 5.42%를 나타내, 2030년에는 76억 7,000만 달러에 이를 것으로 예상되고 있습니다.

운영자는 기본 읽기에서 플랜트 플로어 자산, 에지 게이트웨이 및 클라우드 분석 플랫폼을 연결하는 다층 시각화 허브로 이동하고 있습니다. 휴먼 머신 인터페이스(HMI) 콘솔은 계속해서 조달의 주류를 차지하고 있지만, 에너지 기업이 분산된 인프라를 집중적으로 모니터링하고 있기 때문에 원격 자산과 파이프라인의 시각화가 가장 급속히 확대되고 있습니다. LCD 패널은 비용 리더십을 유지하지만 OLED와 AMOLED 모듈은 제어실이 24시간 가동을 위해 저전력 소비와 우수한 대비를 요구하기 때문에 급성장하고 있습니다. 반도체 부족으로 LCD 컨트롤러의 리드 타임이 길어지고, 통합자는 기술 로드맵을 다양화하고 전략적인 부품 비축을 추구하게 됩니다. 지역별로는 아시아태평양은 부품 제조의 스케일 메리트를 활용하고 중동 및 아프리카은 석유 및 가스 거대 프로젝트를 위한 방폭 사양의 시각화에 대한 설비 투자를 가속화하고 있습니다.

에지 호환 HMI가 이더넷 기반 네트워크에서 밀리초 단위의 대기 시간 데이터를 처리할 수 있어 예기치 않은 종료를 최소화하는 예보 유지 보수 대시보드가 가능합니다. 로크웰 오토메이션은 2025년 주요 디지털화 경로로서 IIoT 아키텍처를 들었으며 컨트롤러와 시각화 엔드포인트 간의 긴밀한 결합을 꼽았습니다. HMS Networks사는 2024년에는 산업용 이더넷이 신규 노드 설치의 71%를 차지하고 PROFINET, EtherNet/IP, EtherCAT 스택을 지원하는 디스플레이 수요가 높아진다고 지적했습니다.

ISA-TR101.02-2019 기술 보고서는 이제 모든 조달 개요에 영향을 미치는 유용성과 성능 벤치마크를 성문화합니다. VarTech Systems와 같은 공급업체는 멀티터치, 음성 제어, 1,000 니트 이상의 밝기를 제공하는 C1D1 및 C1D2 인증 패널을 제공하여 안전과 기능성을 양립시킵니다. 이러한 사양은 운영자의 개입이 마이크로초 단위로 필요한 화학제품 및 의약품에서 배치 간의 무결성을 지원합니다.

방폭 인클로저, 등각 코팅, 특수 장착 키트는 시스템의 초기 비용을 증가시킵니다. Comark Corporation은 IECex를 준수함으로써 해외 플랫폼의 설비 예산이 2배가 되는 반면, 엔지니어링 일정이 몇 분기 연장될 것으로 예상했습니다.

2024년 산업용 디스플레이 시장에서는 굴착, 채광, 군사 플랫폼에서의 중요한 용도를 반영하여 IP65-67의 견고한 하우징이 31.5%의 점유율을 확보했습니다. 비디오월은 석유화학 콤비나트의 집중제어실 투자에 힘입어 연률 5.9%를 나타낼 것으로 예측됩니다. 고휘도 오픈 프레임 모듈은 키오스크 인클로저에 통합되어 있으며 패널 마운트 유닛은 머신 레벨 HMI의 주요 제품으로 유지됩니다. 산업용 디스플레이 시장에서는 내충격성과 모듈식 I/O를 조합한 벤더가 반복적으로 채용되어 신속한 교환과 최소의 다운타임을 실현하고 있습니다. 마링레이드의 제품은 MIL-STD-167의 진동 임계값과 염수 분무 프로토콜에 적합하며, 산업용 디스플레이 시장 실적를 함정과 해양 리그로 확대하고 있습니다. 바 유형이나 스트레치 스크린은 발전소의 멀티파라미터 대시보드에 대응하고 틈새 제품이기 때문에 수량은 적은 것, ASP는 높아지고 있습니다.

2류 공급업체는 견고성과 좁은 베젤 아키텍처를 융합하여 필드 패널과 명령 센터 모두에 대응하는 크로스오버 제품을 생산합니다. 발코의 4,000대의 레이저 스크린 엔터프라이즈 시네마 계약은 나중에 산업용 비디오 월로 이어지는 제조 확장성을 강조합니다. 하이브리드 인클로저는 중복 전원 공급 장치와 에지 게이트웨이를 내장하고 있으며, IEC 60079-2025의 안전 조항을 준수하는 동시에 유지보수가 가능한 산업용 디스플레이 시장을 확대하고 있습니다.

HMI 스테이션은 2024년 매출의 46.8%를 차지했으나 파이프라인과 유정 패드의 원격 측정이 중앙 집중식 NOC로 전환됨에 따라 원격 자산 가시화가 CAGR 6.4%를 초과할 것으로 보입니다. 원격 모니터링을 위한 산업용 디스플레이 시장 규모는 사막과 해외에서 위성과 LPWAN 연결이 보급됨에 따라 꾸준히 확대될 것으로 예측됩니다. 낭비가 없는 공장의 앤던 보드 및 유지보수 작업자를 위한 대화형 키오스크는 고장에서 수리까지의 사이클을 단축하는 인간 중심의 시각적 워크플로우를 강화합니다. 제어실의 비디오 월은 베젤리스 LCD와 신흥 마이크로 LED 어레이가 몰입형 상황 인식 환경을 구축하는 프리미엄 클래스를 구성하고 있습니다. AI 주도 분석 플랫폼과 통합함으로써 운영자는 화면에 직접 표시되는 처방 프롬프트에 따라 행동하여 운영자의 피로와 오류의 발생을 줄일 수 있습니다.

OnePetro의 현장 시험에서 입증된 분산형 태양광 스크린은 송전망에 접근할 수 없는 지역에서의 실행 가능성을 증명하여 원격지 채굴지역에서 산업용 디스플레이 시장의 설치 기반을 확대합니다. 사이버 보안 우선순위가 높아짐에 따라 디스플레이는 화면상의 데이터 흐름을 보호하기 위한 하드웨어 루트 오브 트러스트 모듈과의 조합이 증가하고 있습니다.

아시아태평양은 중국의 공장 자동화 추진과 정밀 부품의 일본 리더십에 힘입어 2024년 매출의 37%를 차지했습니다. 삼성디스플레이와 LG디스플레이는 세계적인 OLED 공장을 운영하고 있으며, 이 지역의 산업용 디스플레이 시장에서 공급의 우위성을 확고히 하고 있습니다. 구성 요소 정부는 패널 공장 확장을 가속화하는 설비 투자 세액 공제를 지지하고 있으며, 반도체 부족 시기에도 안정적인 패널 공급을 보장합니다.

중동 및 아프리카는 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 6.3%를 나타낼 전망입니다. 걸프 지역의 수십억 달러 규모의 탄화수소 프로젝트는 IEC 60079-2025의 인증을 받은 본질 안전 방폭 스크린에 의존하고 있으며, 방폭 하드웨어 산업용 디스플레이 시장 규모를 확대하고 있습니다. 국영 석유 회사는 중앙 NOC와 지역 마이크로 컨트롤 룸을 결합하고 사막의 온도에서 고휘도를 유지하는 동기화 된 비디오 벽을 요구합니다.

북미에서는 에너지 효율과 사이버 보안 강화를 요구하는 중세 공장에 리노베이션 파도가 밀려 들고 있습니다. CRT 및 저항막 터치 패널에서 IP 기반 유리 표면으로의 적극적인 교체가 공장이 디지털 성능 보드를 채택함에 따라 산업용 디스플레이 시장을 밀어 올립니다. 유럽에서는 EN ISO 9241-210 사용성 지침을 준수하는 인체 공학적 HMI 레이아웃에 초점을 맞춘 인더스트리 4.0 청사진이 진행되어 운영자의 복리 후생이 촉진됩니다. 남미의 광업과 수력 발전 부문은 고지대와 습도를 견디는 튼튼한 패널을 수입하여 지리적 수익을 더욱 다양화하고 있습니다.

The industrial display market size stands at USD 5.89 billion in 2025 and is projected to reach USD 7.67 billion by 2030, reflecting a 5.42% CAGR over the forecast period.

Operators are moving from basic read-outs to multi-layered visualization hubs that connect plant-floor assets, edge gateways and cloud analytics platforms. Human-machine interface (HMI) consoles continue to dominate procurement, yet remote asset and pipeline visualization is scaling the fastest as energy firms centralize oversight of dispersed infrastructure. LCD panels preserve cost leadership, while OLED and AMOLED modules post the quickest growth as control rooms demand lower power draw and superior contrast for round-the-clock duty. Semiconductor shortages lengthen LCD controller lead times, pushing integrators to diversify technology roadmaps and pursue strategic component reserves. Regionally, Asia-Pacific leverages economies of scale in component fabrication, whereas the Middle East and Africa accelerates capital expenditure on explosion-proof visualization for oil and gas megaprojects.

Edge-ready HMIs now process millisecond latency data from Ethernet-based networks, enabling predictive maintenance dashboards that minimize unplanned shutdowns. Rockwell Automation identifies IIoT architecture as the principal digitization pathway for 2025, citing tighter coupling between controllers and visualization endpoints. HMS Networks confirms momentum, noting that Industrial Ethernet supplied 71% of new node installations in 2024, catalyzing demand for displays that support PROFINET, EtherNet/IP and EtherCAT stacks.

The ISA-TR101.02-2019 technical report codifies usability and performance benchmarks that now influence every procurement brief. Suppliers such as VarTech Systems deliver C1D1 and C1D2 certified panels offering multi-touch, voice control and >1,000 nit brightness, aligning safety with functionality. These specifications support batch-to-batch integrity in chemicals and pharmaceuticals where micro-seconds matter for operator intervention.

Explosion-proof enclosures, conformal coatings, and specialized mounting kits elevate upfront system outlays. Comark Corporation projects that IECEx compliance can double equipment budgets for offshore platforms while extending engineering schedules by several quarters.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Rugged housings rated to IP65-67 secured a 31.5% slice of the industrial display market in 2024, reflecting critical-duty requirements in drilling, mining and military platforms. Video walls are projected to compound at 5.9% annually, fueled by centralized control-room investment across petrochemical complexes. High-brightness open-frame modules integrate into kiosk enclosures, while panel-mount units remain the workhorse for machine-level HMIs. The industrial display market repeatedly favors vendors that combine shock resistance with modular I/O, ensuring rapid swap-out and minimal downtime. Marine-grade variants meet MIL-STD-167 vibration thresholds and salt-spray protocols, extending the industrial display market footprint to naval vessels and offshore rigs. Bar-type and stretch screens address multi-parameter dashboards in power plants, a niche translating to higher ASPs despite lower volumes.

Second-tier suppliers are blending ruggedization with narrow-bezel architectures, creating cross-over products that serve both field panels and command centers. Barco's enterprise cinema contract for 4,000 laser screens underscores manufacturing scalability that later translates into industrial video walls. Hybrid enclosures now embed redundant power supplies and edge gateways, aligning with IEC 60079-2025 safety clauses while enlarging the serviceable industrial display market.

HMI stations delivered 46.8% of 2024 revenue, but remote asset visualization will outpace at a 6.4% CAGR as pipeline and well-pad telemetry shifts to centralized NOCs. The industrial display market size for remote monitoring is forecast to expand steadily as satellite and LPWAN connectivity proliferate in deserts and offshore locations. Andon boards in lean plants and interactive kiosks for maintenance crews reinforce human-centric visual workflows that shorten fault-to-fix cycles. Control-room video walls constitute the premium class where bezel-less LCD or emerging Micro-LED arrays craft immersive situational awareness environments. Integration with AI-driven analytics platforms means operators now act on prescriptive prompts rendered directly on the screen, reducing operator fatigue and error incidence.

Distributed solar-powered screens demonstrated by OnePetro field trials prove viability in regions lacking grid access, widening the install base of the industrial display market in remote extraction zones. As cybersecurity rises in priority, displays are increasingly paired with hardware-root-of-trust modules to secure on-screen data flows, a requirement accentuated in cross-border pipeline operations.

The Industrial Display Market Report is Segmented by Type (Rugged Displays, Open Frame Monitors, and More), Application (Human-Machine Interface, Remote Asset and Pipeline Monitoring, and More), Technology (LCD, LED Backlit LCD, and More), Panel Size (Up To 14 Inch, 14 Inch - 21 Inch, and More), End-Use Industry (Manufacturing, Energy and Power, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 37% revenue in 2024, underpinned by China's factory automation drive and Japan's leadership in precision components. Samsung Display and LG Display operate global-scale OLED fabs, cementing the region's supply advantage across the industrial display market. Component governments back capex tax credits that accelerate panel plant expansions, ensuring steady panel availability even during semiconductor shortages.

The Middle East and Africa is poised for the fastest 6.3% CAGR to 2030. Multi-billion-dollar hydrocarbon projects across the Gulf rely on intrinsically safe screens certified under IEC 60079-2025, enlarging the industrial display market size for explosion-proof hardware. National oil companies pair centralized NOCs with regional micro-control rooms, demanding synchronized video walls that sustain high brightness amid desert temperatures.

North America witnesses a retrofit wave across mid-century factories seeking energy efficiencies and cybersecurity hardening. Proactive replacement of CRTs and resistive-touch panels with IP-based glass surfaces boosts the industrial display market as factories embrace digital performance boards. Europe advances Industry 4.0 blueprints with a focus on ergonomic HMI layouts compliant with EN ISO 9241-210 usability guidance, promoting operator well-being. South America's mining and hydroelectric sectors import hardy panels rated for high altitude and humidity, further diversifying geographic revenue.